INTRODUCTION

Peanut katli isa traditional Indian sweet crafed from

peanuts, sugar, milk powder, and ghee.

It serves as a cost-effective alternative to the more

expensive kaju katli (cashew sweet), offering similar

taste and texture at a fraction of the price.

Its growing popularity is driven by affordability,

nutritional value, and appeal among both traditional

sweet lovers and health-conscious consumers

4.

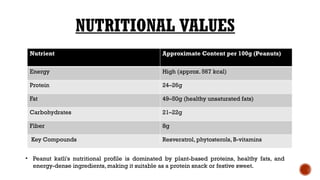

NUTRITIONAL VALUES

Nutrient ApproximateContent per 100g (Peanuts)

Energy High (approx. 567 kcal)

Protein 24–26g

Fat 49–50g (healthy unsaturated fats)

Carbohydrates 21–22g

Fiber 8g

Key Compounds Resveratrol, phytosterols, B-vitamins

• Peanut katli's nutritional profile is dominated by plant-based proteins, healthy fats, and

energy-dense ingredients, making it suitable as a protein snack or festive sweet.

5.

MARKET SURVEY

ConsumerTrends: Demand for budget-friendly, protein-rich,

and specialty sweets is rising.

Channels:Traditional sweet shops, groceries, supermarkets,

online platforms, direct festival/event sales.

Consumer Behavior: Continued preference for ready-to-eat

sweets; increasing online purchases but strong hold for

traditional retailers.

6.

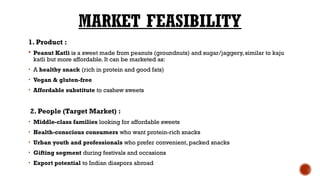

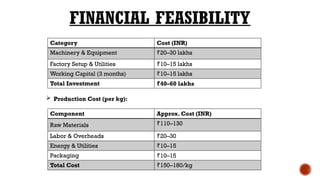

MARKET FEASIBILITY

1. Product:

Peanut Katli is a sweet made from peanuts (groundnuts) and sugar/jaggery, similar to kaju

katli but more affordable. It can be marketed as:

• A healthy snack (rich in protein and good fats)

• Vegan & gluten-free

• Affordable substitute to cashew sweets

2. People (Target Market) :

• Middle-class families looking for affordable sweets

• Health-conscious consumers who want protein-rich snacks

• Urban youth and professionals who prefer convenient, packed snacks

• Gifting segment during festivals and occasions

• Export potential to Indian diaspora abroad

7.

3. Place (DistributionChannels) :

• Retail outlets: Local grocery stores, sweet shops.

• Supermarkets & Hypermarkets: Big Bazaar, Reliance Fresh, etc.

• Online platforms: Amazon, Flipkart, BigBasket.

• Export channels: Especially to Gulf countries, US, UK.

Specialty food stores: Organic and health food stores.

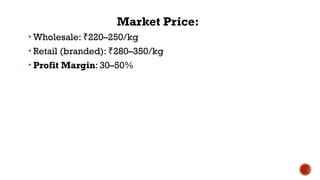

4. Price :

• Penetration pricing strategy: Lower price than kaju katli to attract customers

• Value packs: Larger sizes at discounted rates

• Premium line:With organic ingredients or gift packaging at a higher price

• Competitive pricing with other similar sweets like soan papdi or besan barfi.

8.

5. Promotion :

•Social media campaigns: Highlight health benefits, nostalgia, affordability.

• Festive promotions: Discounts, combo packs during Diwali, Rakhi, etc.

• Free samples in supermarkets and local stores.

• Influencer marketing: Food bloggers,YouTubers.

• Packaging with traditional motifs and modern appeal.

• Point of Sale (POS) materials in retail outlets.

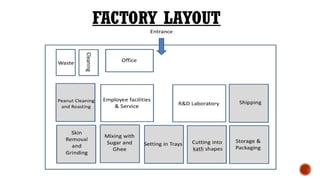

6. Process :

• Standardized production using semi-automatic machines for hygiene & consistency.

• Quality checks at various stages (raw peanut selection, roasting, grinding).

• Packaging using vacuum or nitrogen flushing to ensure longer shelf life.

• Logistics for timely distribution and restocking.

• Customer feedback system via QR codes or online forms.

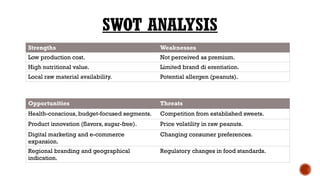

SWOT ANALYSIS

Strengths Weaknesses

Lowproduction cost. Not perceived as premium.

High nutritional value. Limited brand di erentiation.

Local raw material availability. Potential allergen (peanuts).

Opportunities Threats

Health-conscious, budget-focused segments. Competition from established sweets.

Product innovation (flavors, sugar-free). Price volatility in raw peanuts.

Digital marketing and e-commerce

expansion.

Changing consumer preferences.

Regional branding and geographical

indication.

Regulatory changes in food standards.

11.

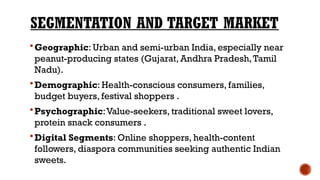

SEGMENTATION AND TARGETMARKET

Geographic: Urban and semi-urban India, especially near

peanut-producing states (Gujarat, Andhra Pradesh,Tamil

Nadu).

Demographic: Health-conscious consumers, families,

budget buyers, festival shoppers .

Psychographic:Value-seekers, traditional sweet lovers,

protein snack consumers .

Digital Segments: Online shoppers, health-content

followers, diaspora communities seeking authentic Indian

sweets.

ENVIRONMENTAL FEASIBILITY

Sustainability:Minimal waste generation; peanut shells can be

repurposed or composted.

Resource Effciency: Local sourcing reduces transportation footprint.

Compliance: Adherence to FSSAI and local pollution norms.

Socio-Economic Feasibility

Employment: Supports local job creation in processing, packaging,

and sales. Farmer.

Benefit: Expands demand for locally grown peanuts.

Community Impact: A ordable sweet option, supports rural and

semi-urban economies.

16.

THE FUTURE PRODUCTS

Innovations:

Sugar-free or low-sugar peanut katli (for diabetic/health markets).

Flavored variants (chocolate, sa ron, cardamom).

Premium packaging for gifting and export.

Regionally branded products highlighting local peanut varieties and traditional methods.

Digital-first product lines with QR codes linking to nutritional information and origin

stories.

Market Potential:

As nutrition and affordability remain key drivers, peanut katli is well positioned for

growth, both domestically and in overseas markets with diaspora demand.

17.

CONCLUSION

Peanut katli demonstratesstrong feasibility across

technical,financial, environmental, and socio economic

dimensions.

It leverages India's robust peanut supply, offers a nutritious

and affordable product, and aligns with consumer trends

toward protein-rich, budget-friendly sweets.

With opportunities for product innovation, regional

branding, digital marketing, and expanding market

channels, peanut katli is poised to strengthen its position in

the Indian confectionery market and beyond.