Downloaded 37 times

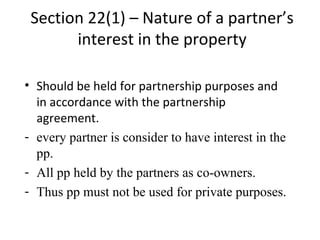

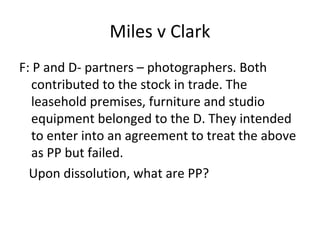

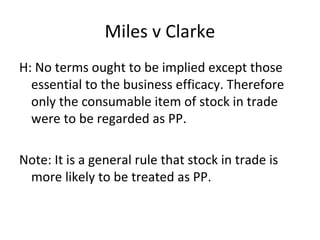

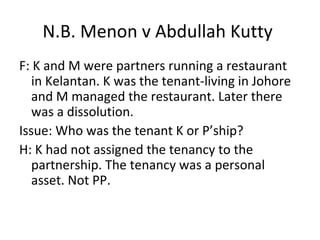

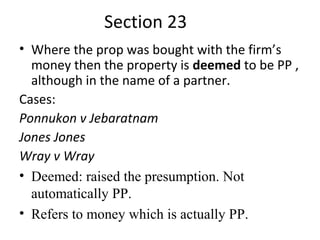

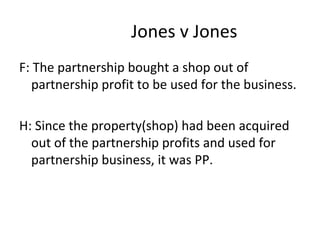

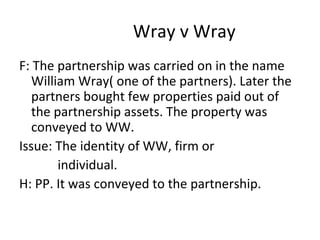

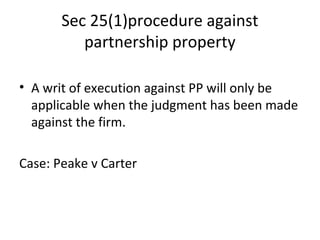

The document discusses partnership property, defining it as assets belonging to a partnership and outlining the conditions under which property is considered part of the partnership. It highlights various cases to illustrate how property is classified as partnership property or individual partner property, focusing on acquisition circumstances, use, and the partnership agreement. Legal provisions such as sections 22, 23, and 25 are referenced to explain the rights and interests of partners in partnership property and the implications for personal debts of partners.