Downloaded 50 times

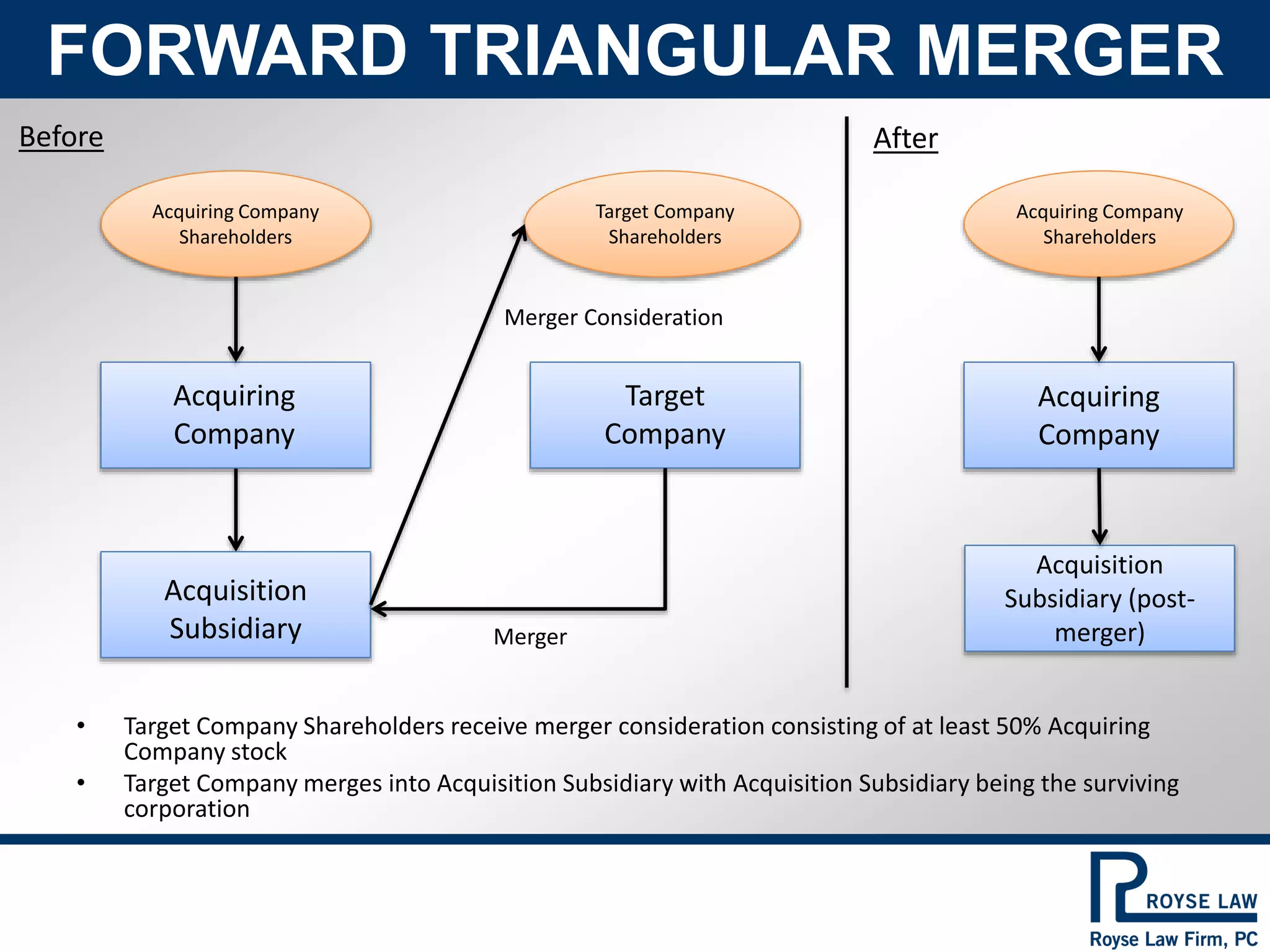

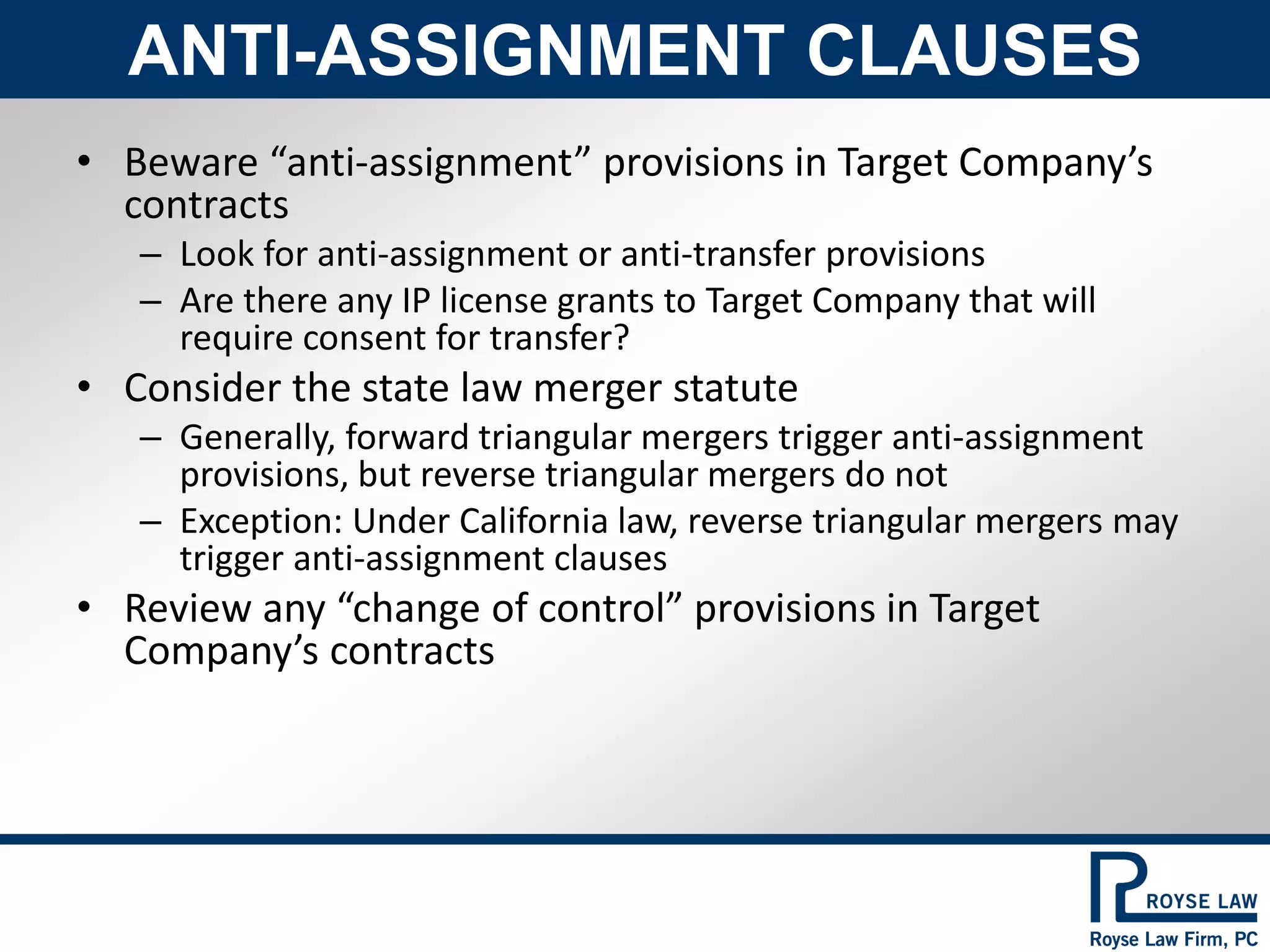

The document outlines IRS compliance regarding tax advice in relation to mergers, specifically forward and reverse triangular mergers. It details the legal steps, benefits, and implications of both types of mergers, including how each triggers anti-assignment clauses in contracts. Additionally, it emphasizes the strategic choice between forward and reverse mergers based on tax consequences and shareholder approvals.