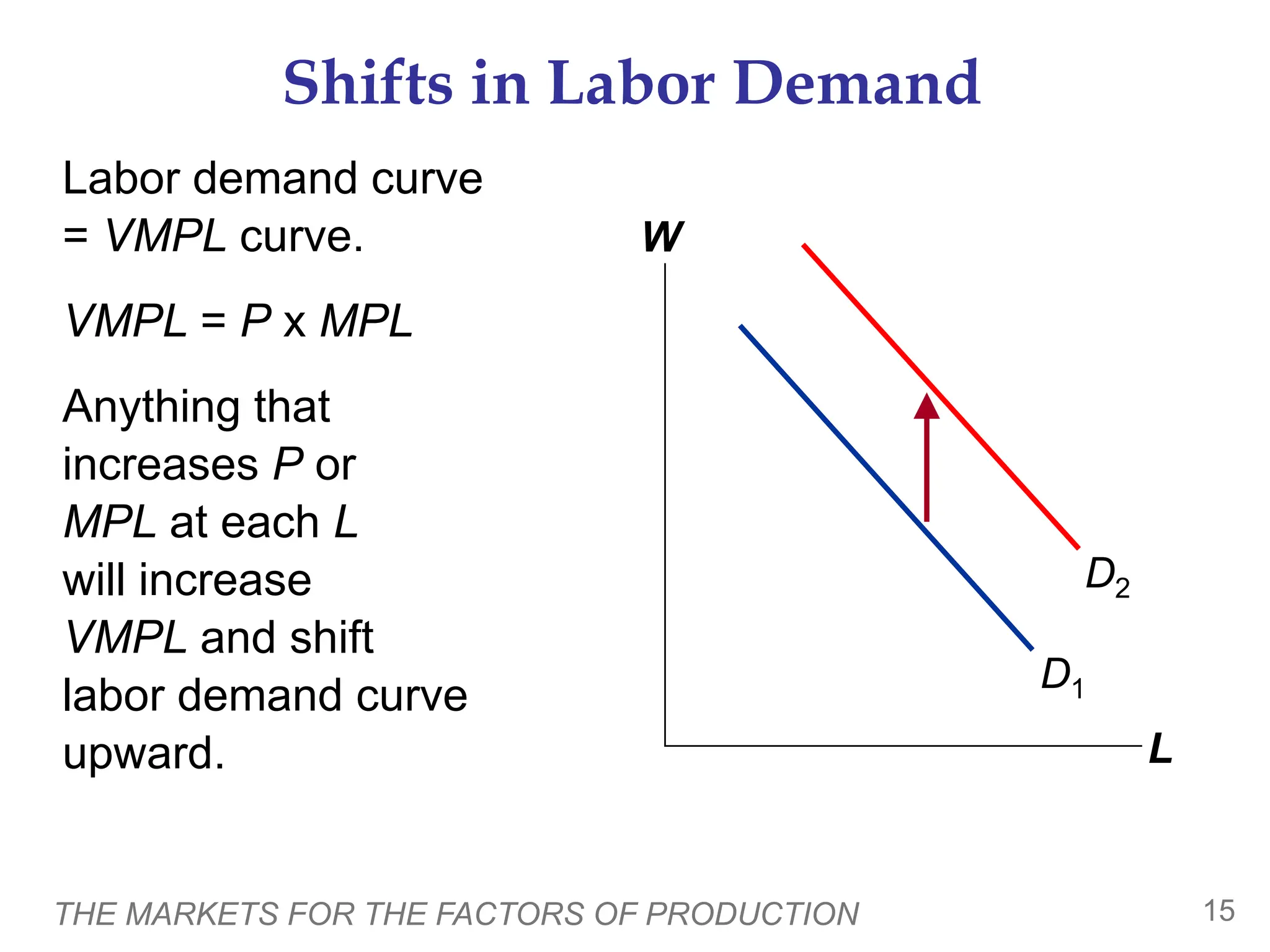

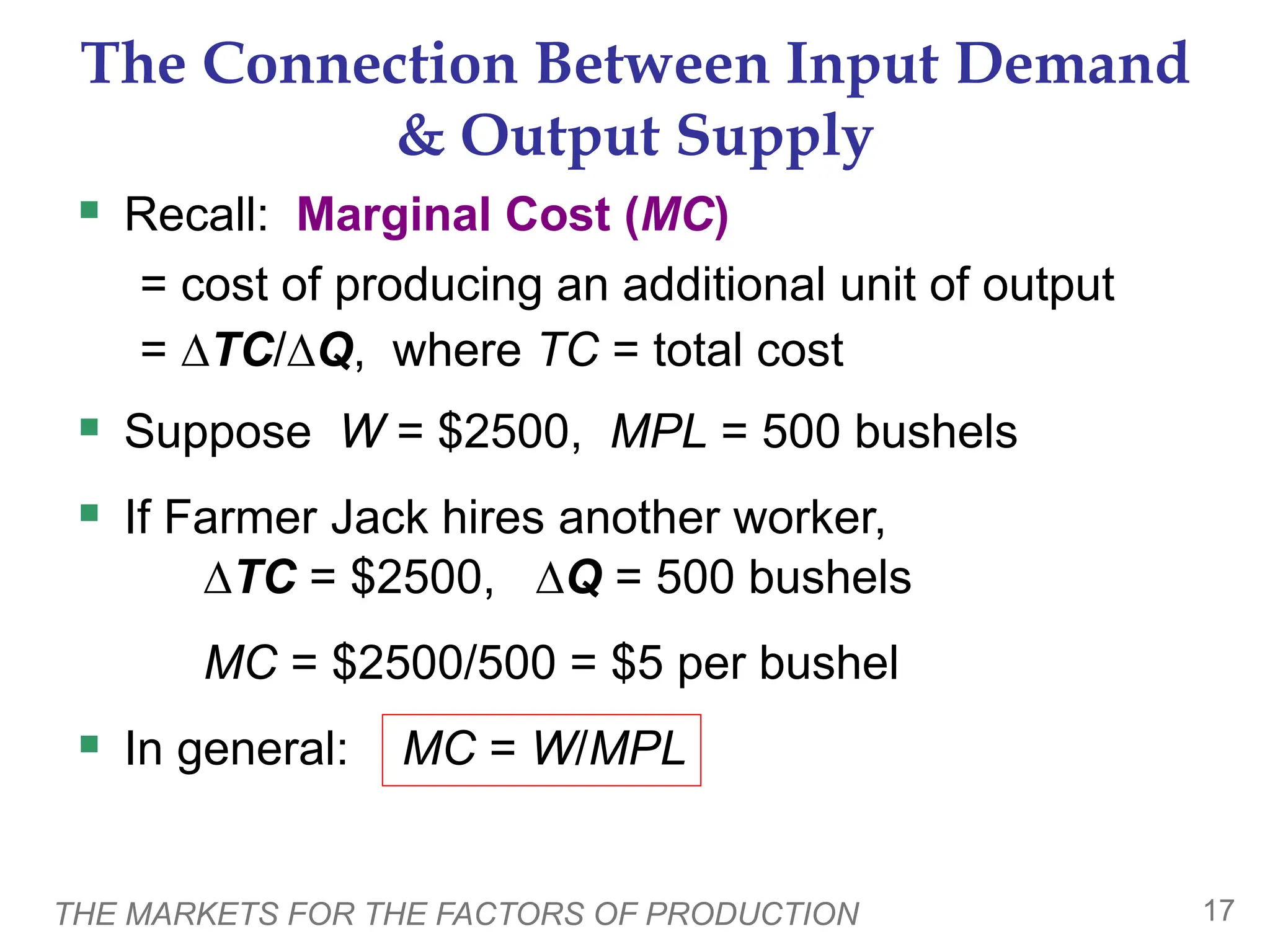

This document discusses the markets for factors of production such as labor, land, and capital. It uses the example of a farmer, Farmer Jack, who hires labor. It explains that a firm's demand for labor depends on the marginal product of labor (MPL) and the value of the marginal product (VMPL), which is the MPL times the price of output. The wage adjusts to equal the VMPL in order to maximize profits. The supply of labor depends on workers' trade-off between work and leisure. The chapter also discusses how technological changes and other factors can shift the demand and supply curves for labor.