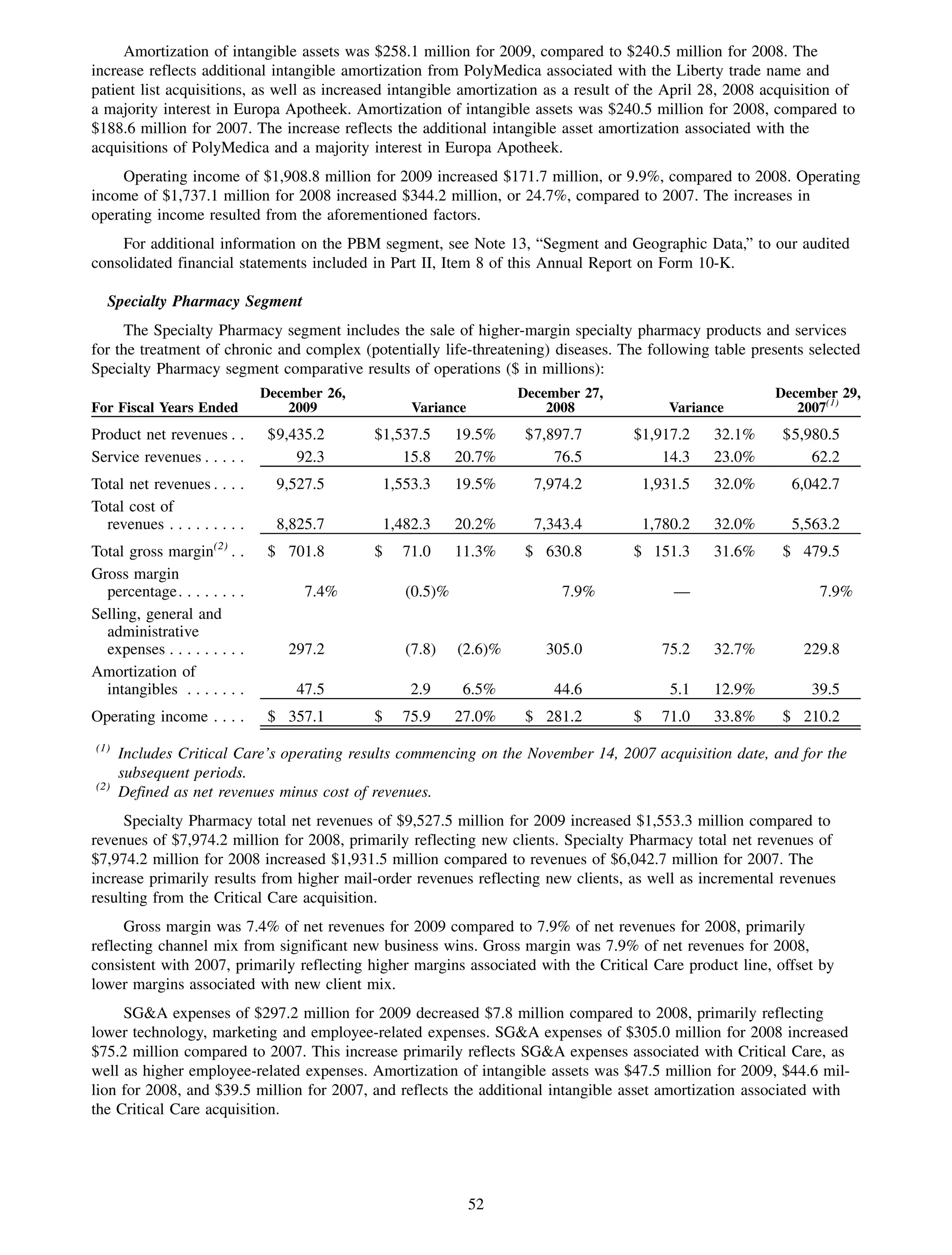

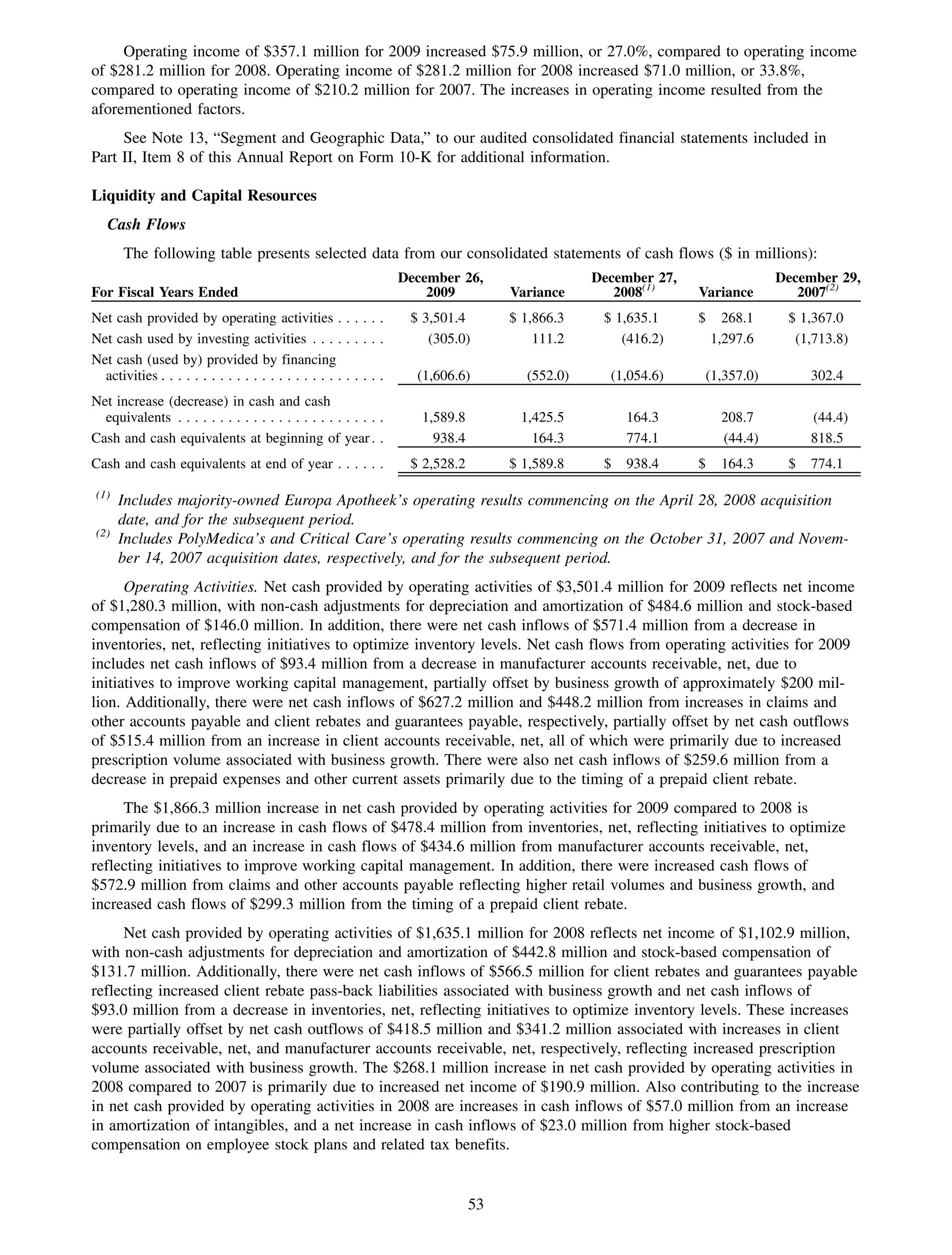

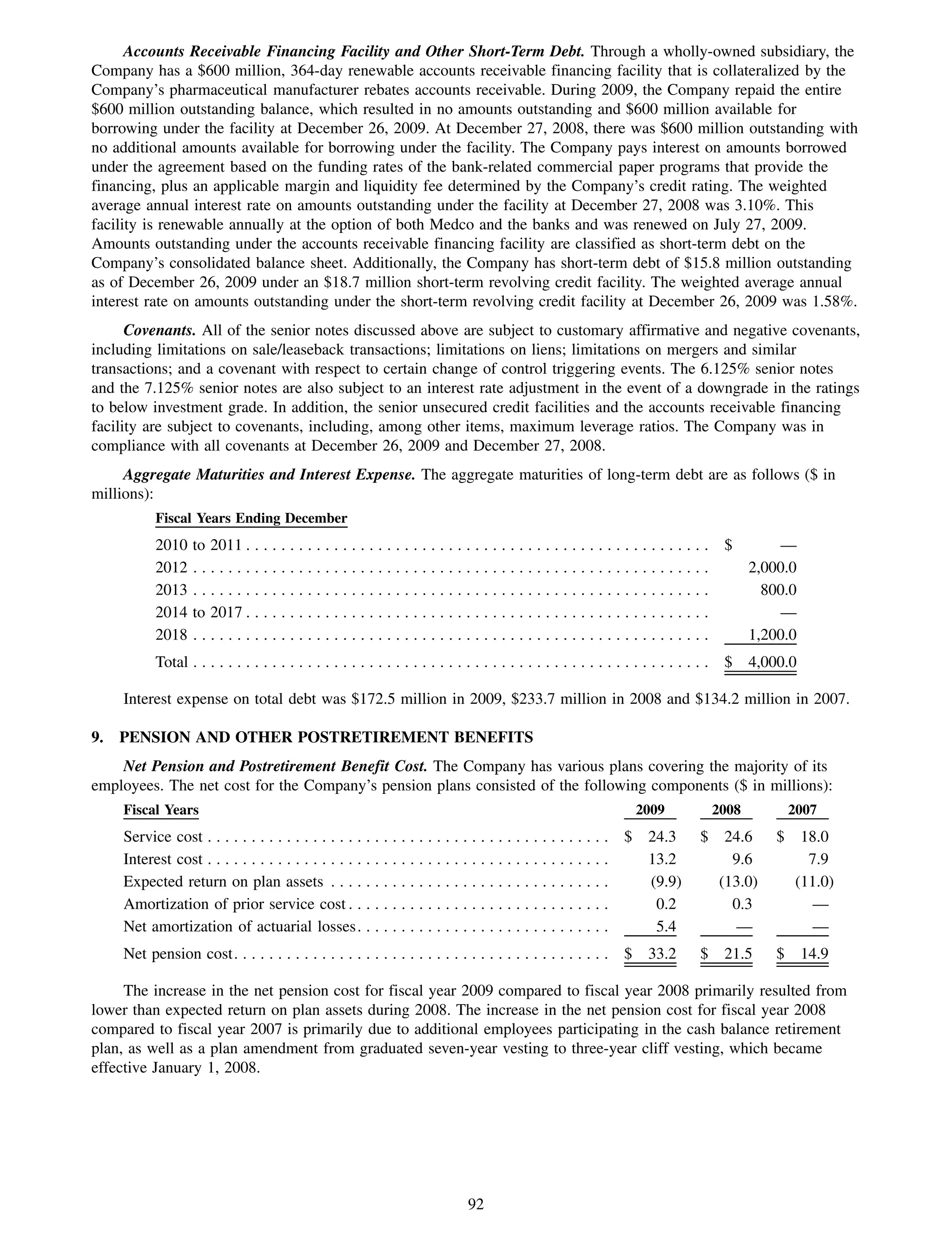

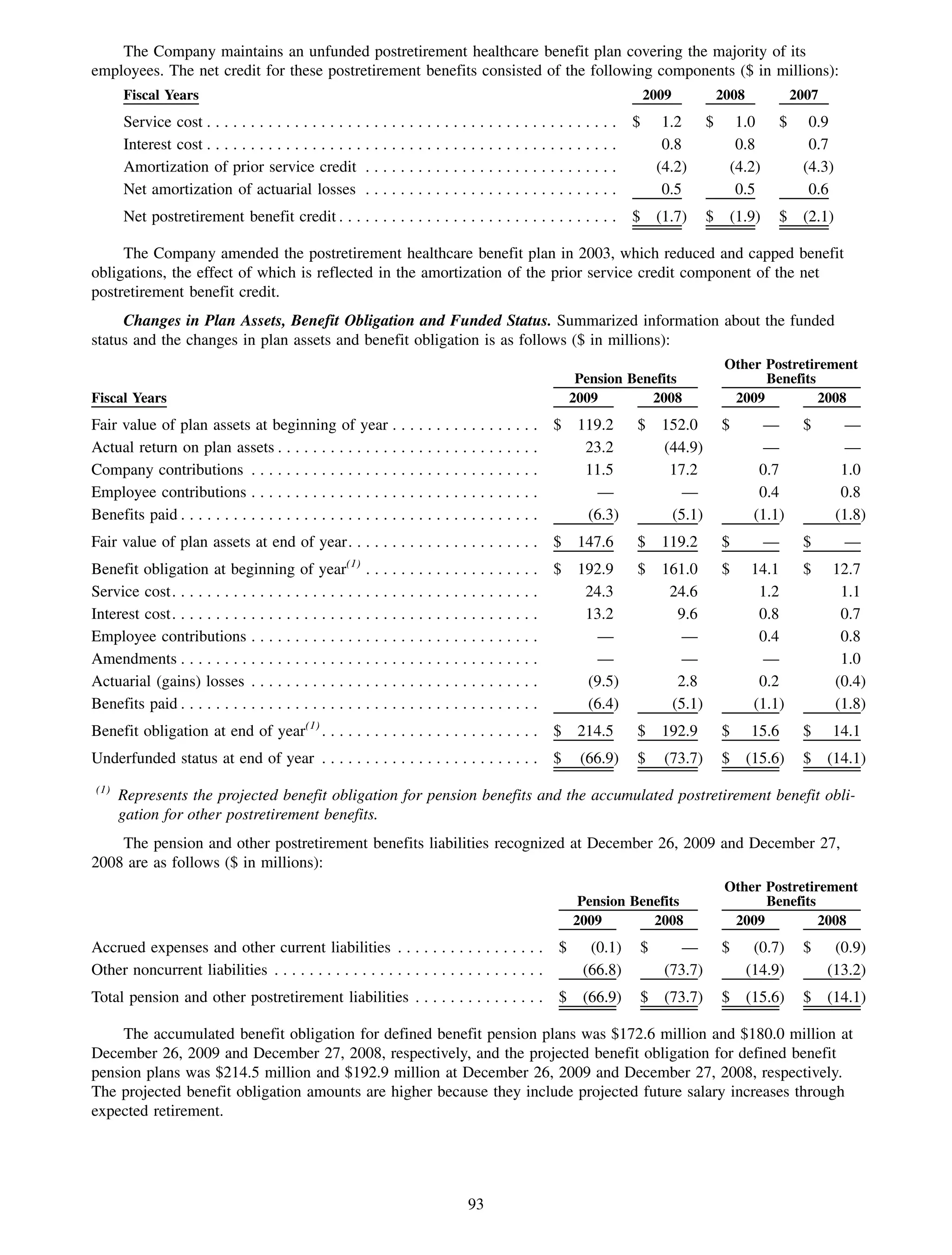

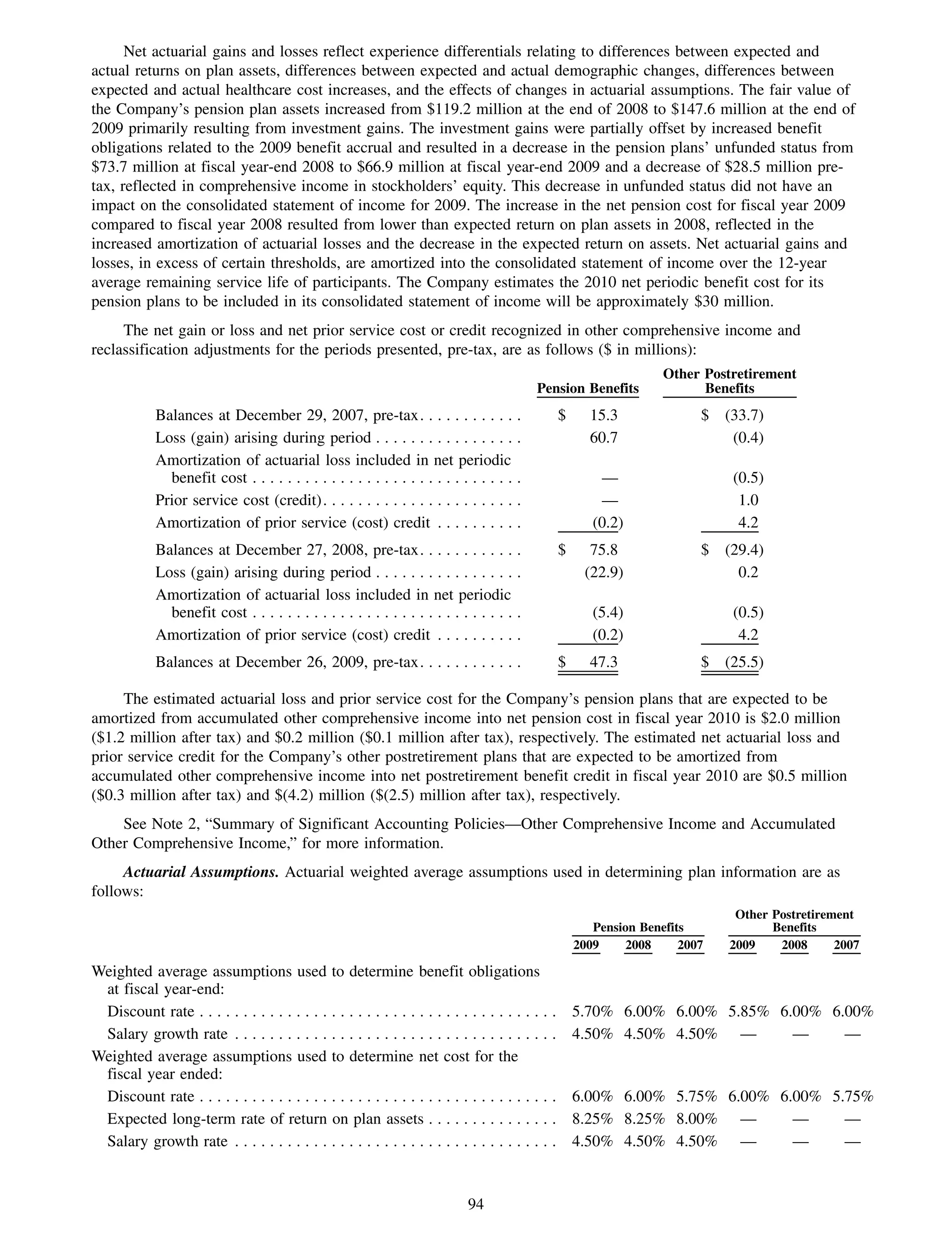

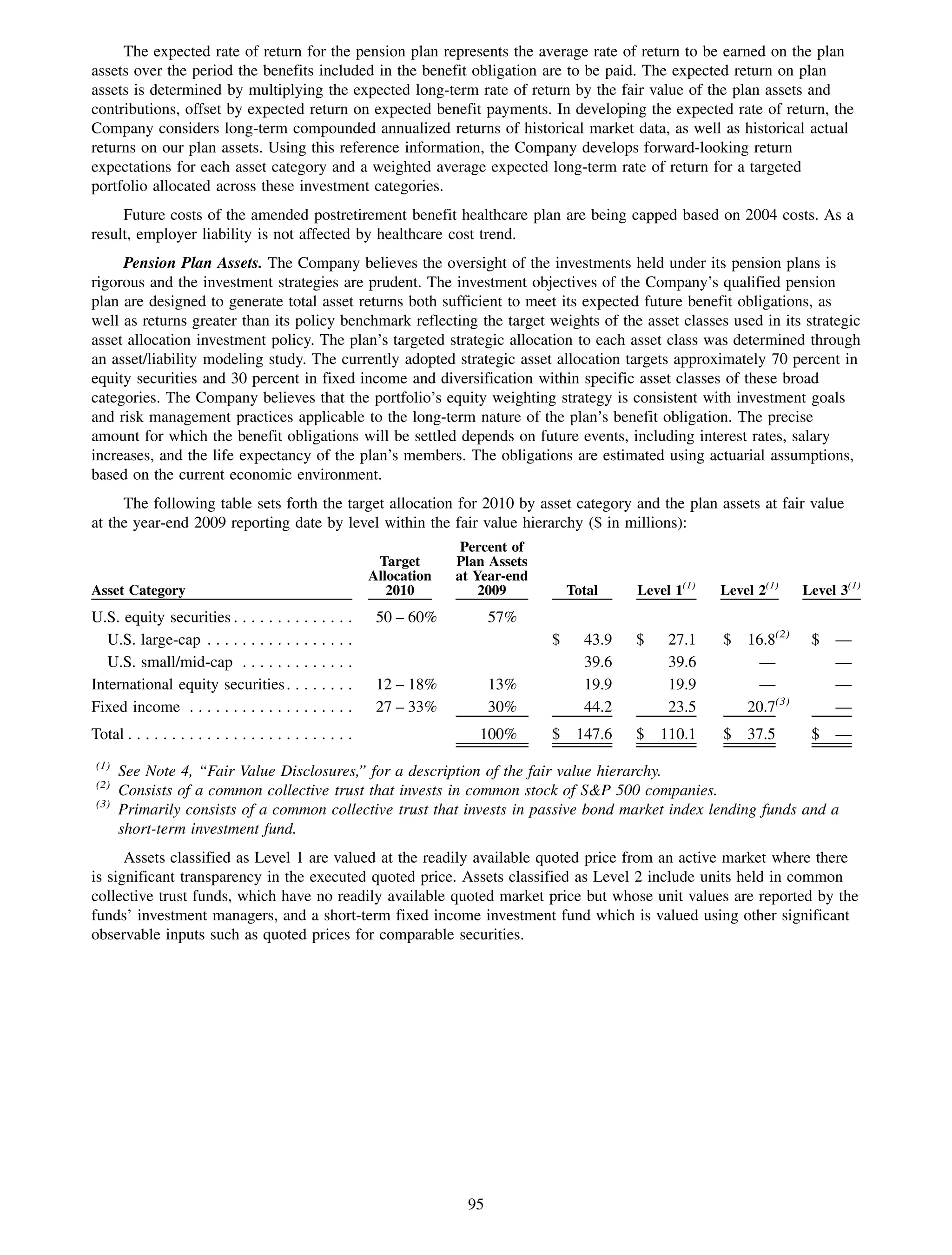

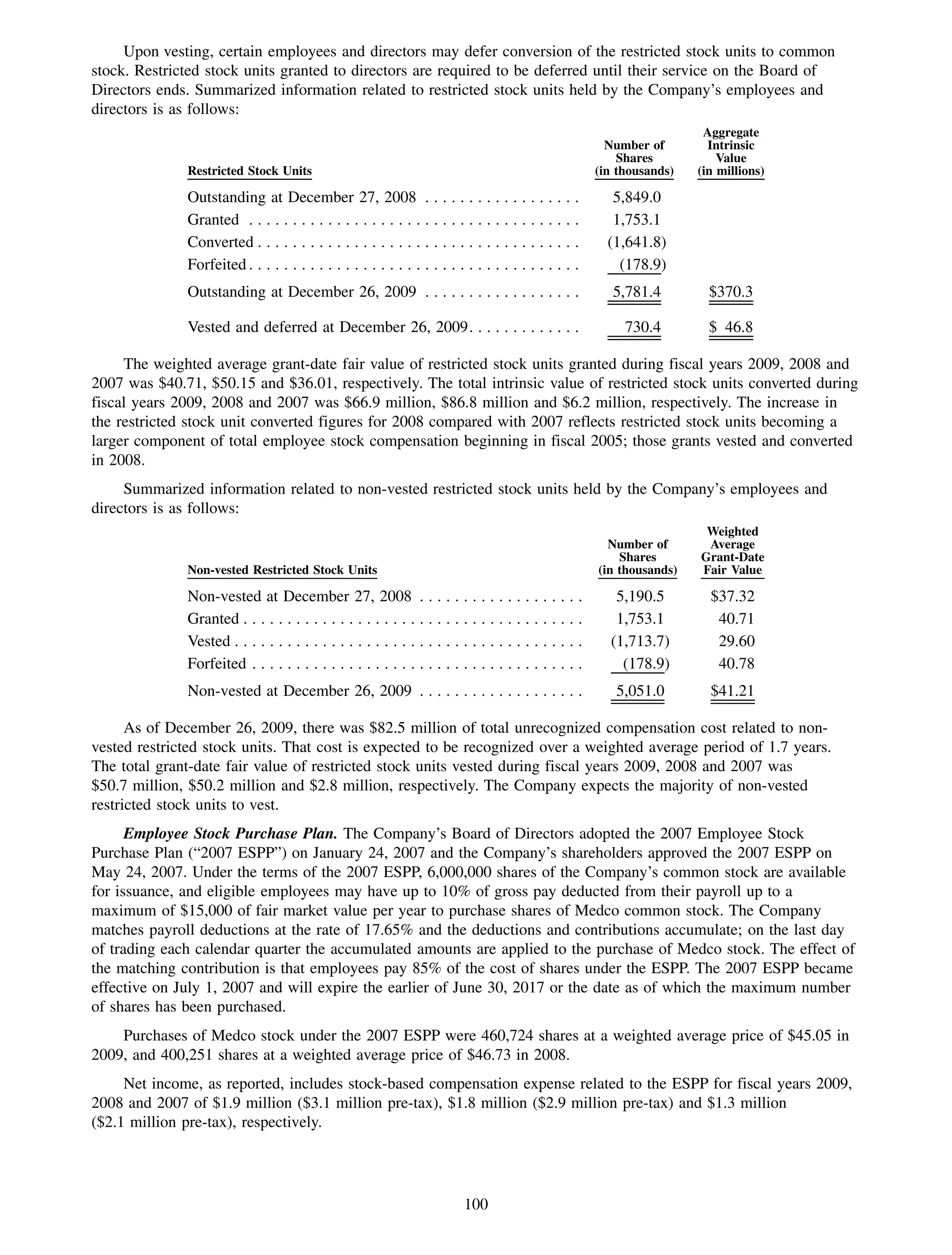

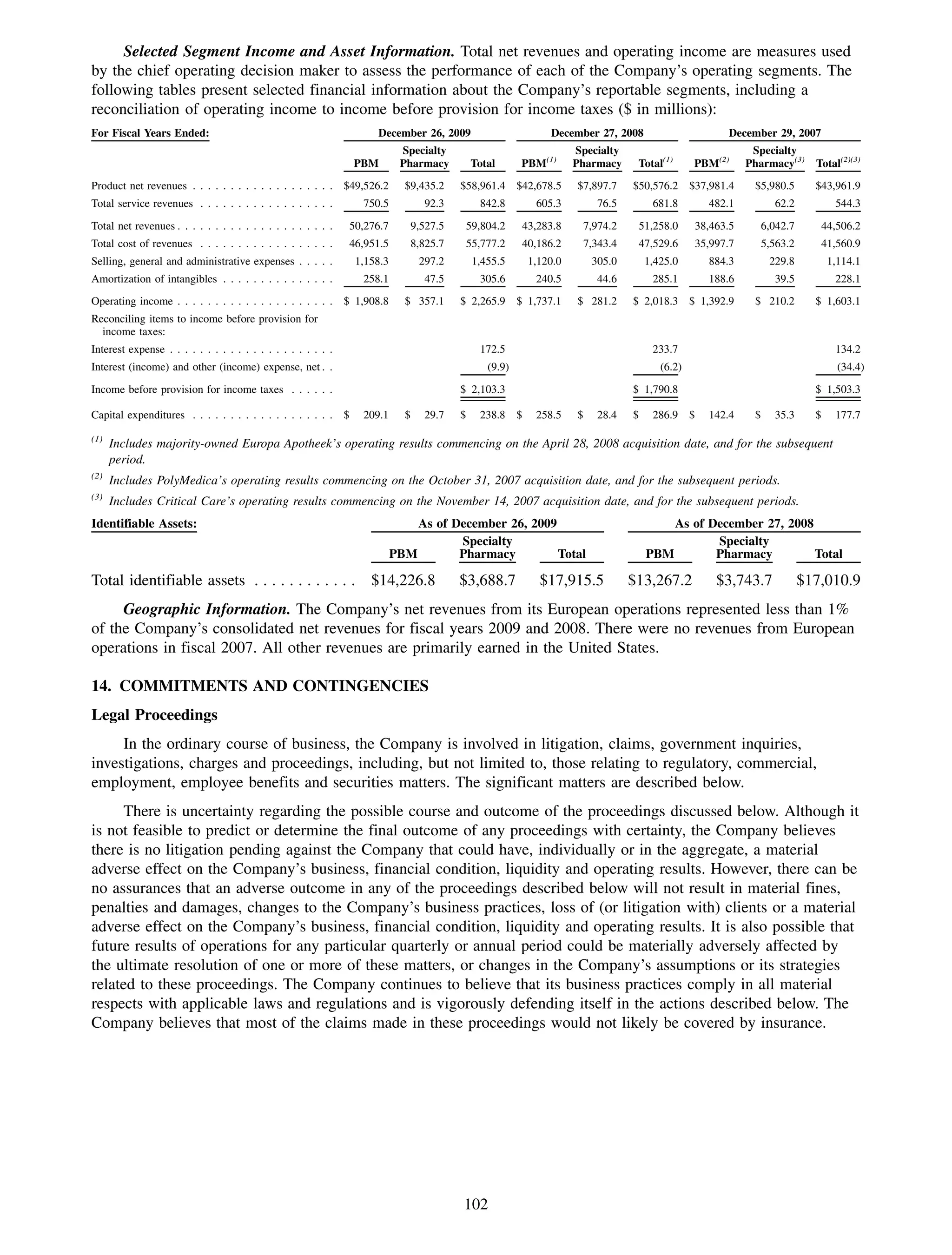

Downloaded 25 times

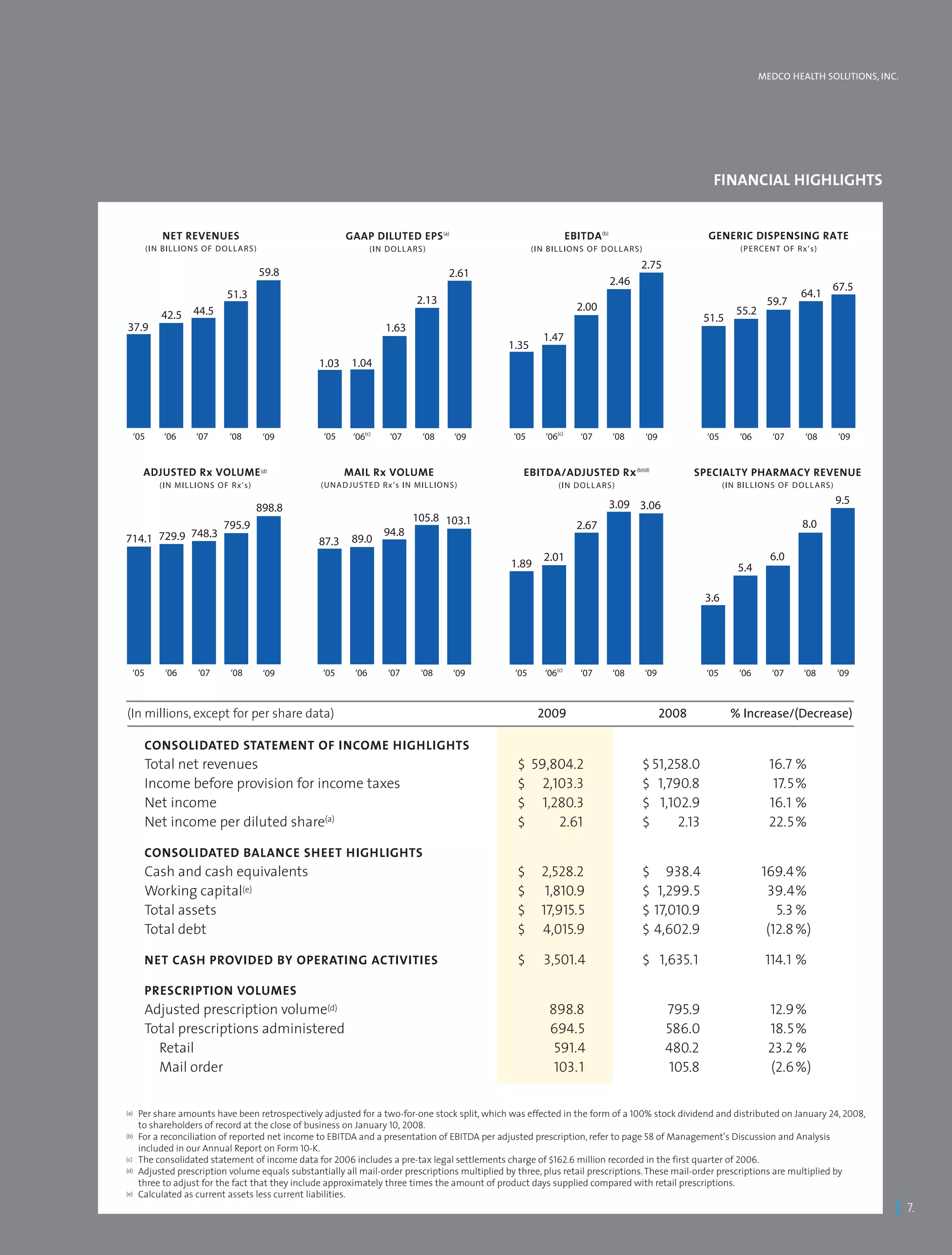

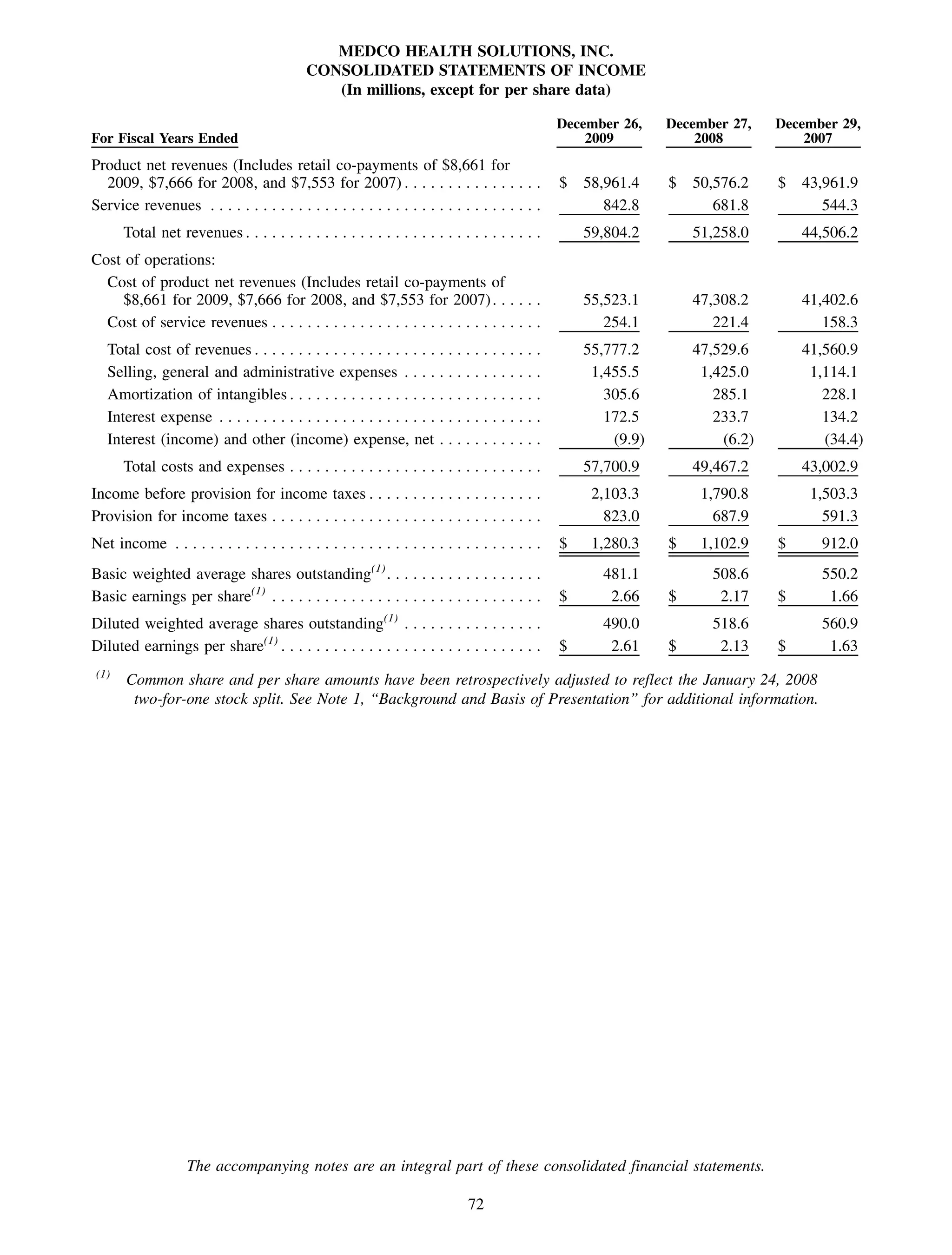

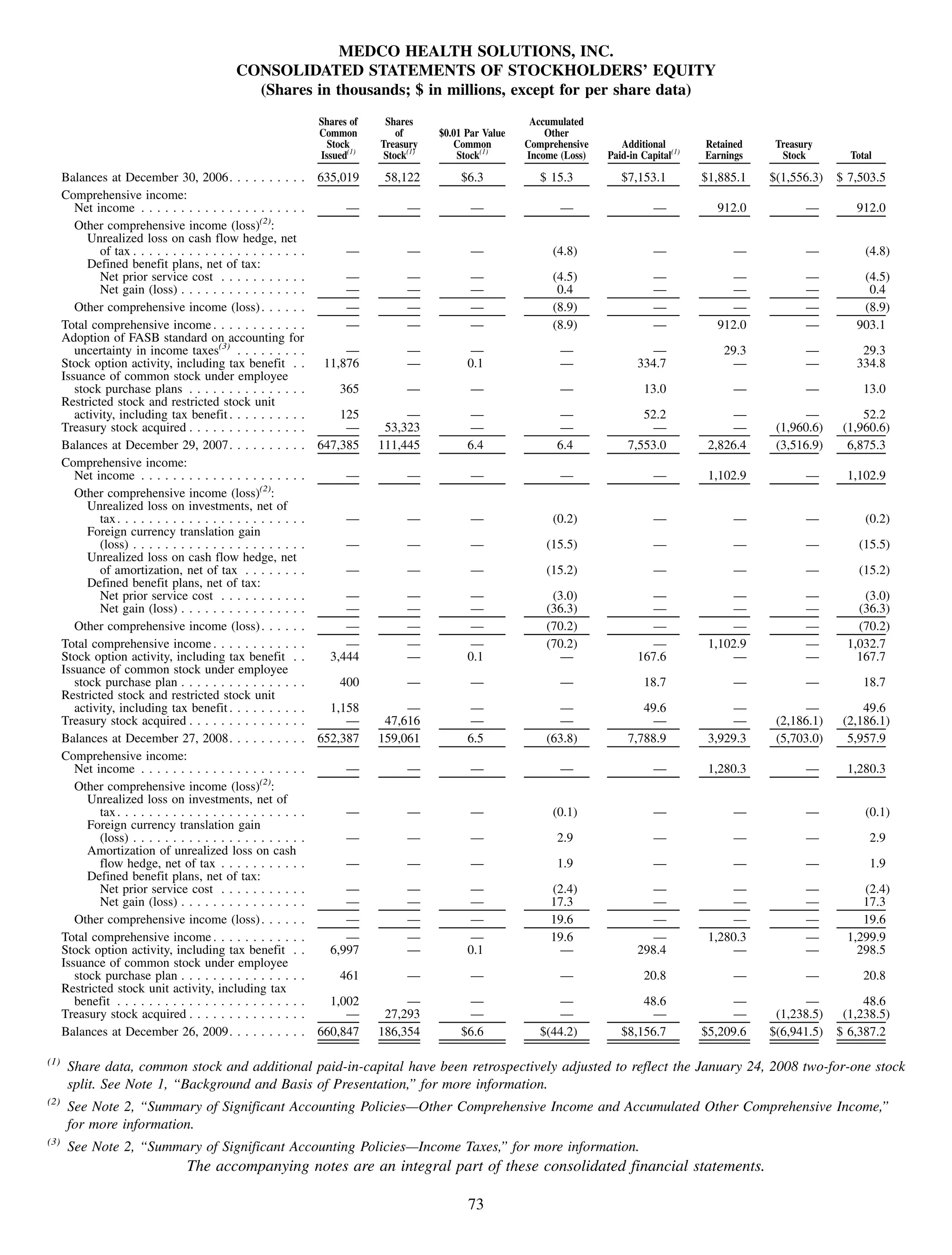

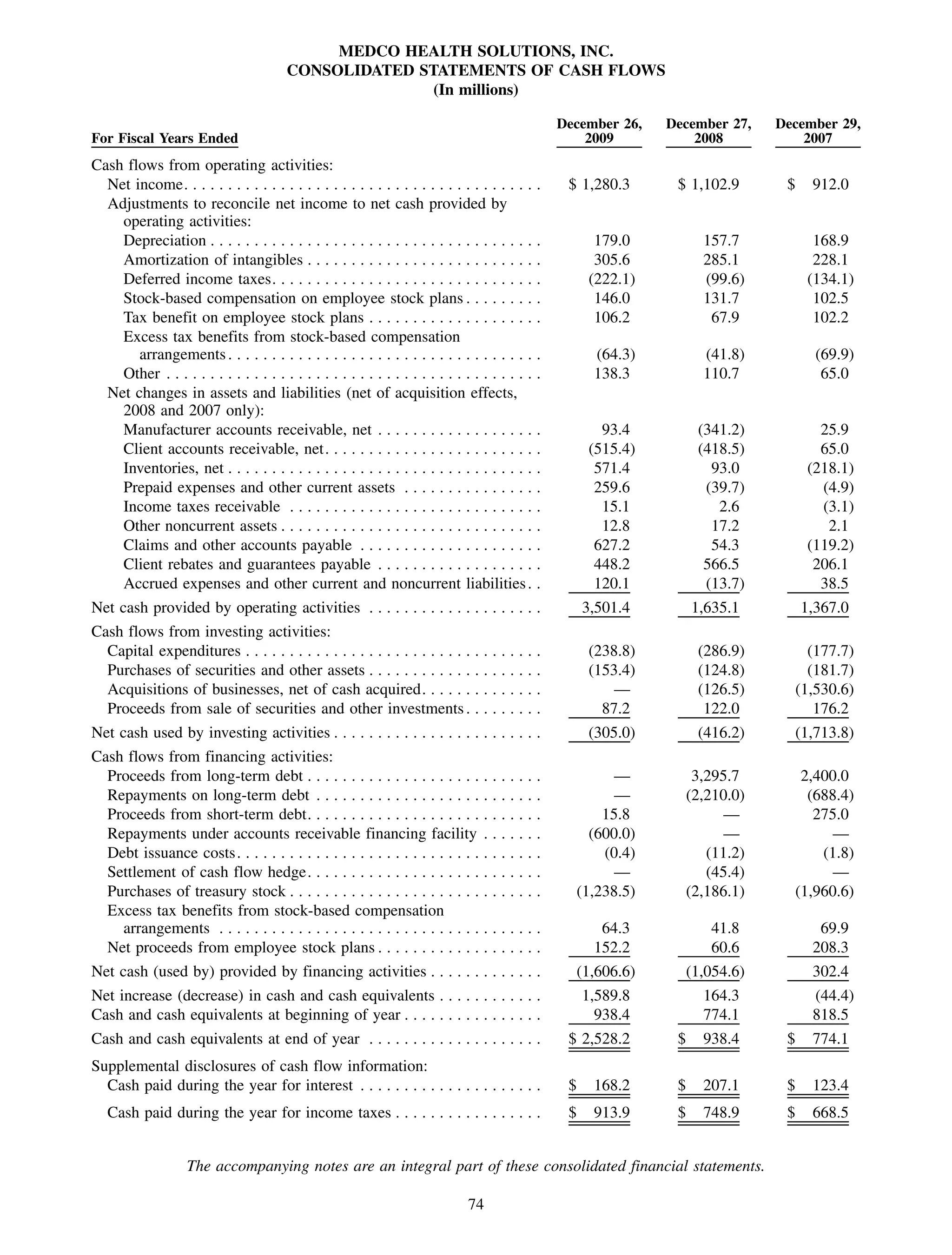

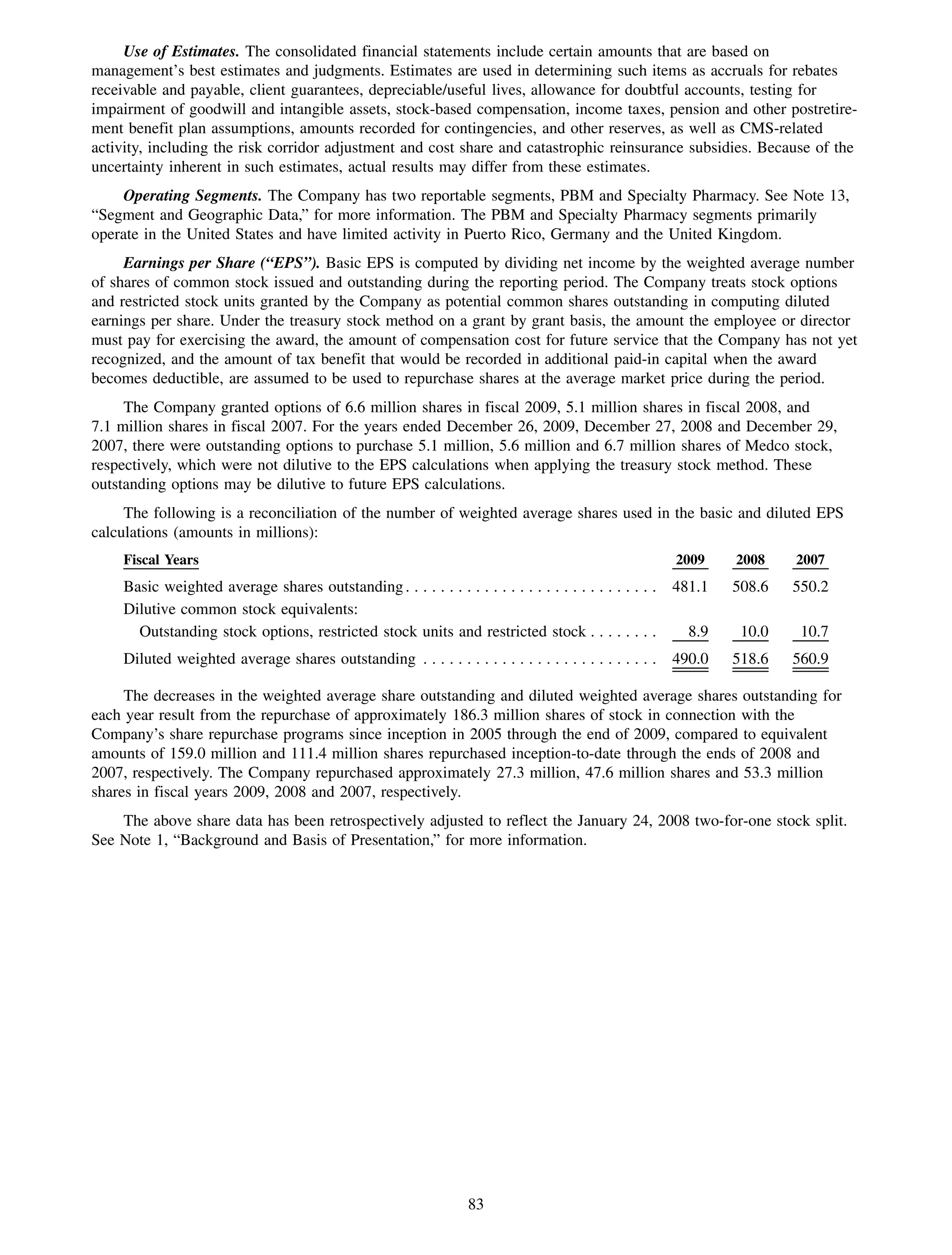

This 2009 annual report summarizes Medco Health Solutions' financial and operational performance for the year. Key highlights include record revenues of $59.8 billion, net income of $1.28 billion, and adjusted prescription volume of 898.8 million. The company saw growth in specialty pharmacy revenues and generic dispensing rates. Medco also advanced initiatives in areas like pharmacogenomics, international expansion, and a new online health store. The report discusses Medco's focus on making medicine smarter through clinical leadership and innovation.