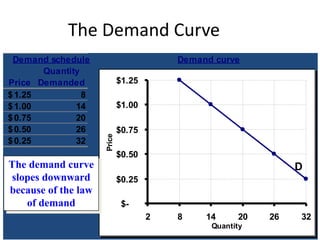

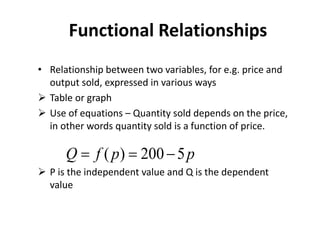

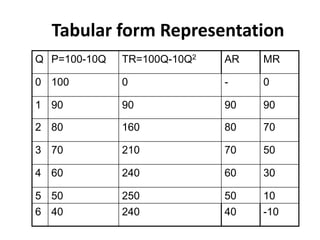

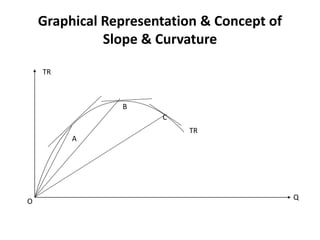

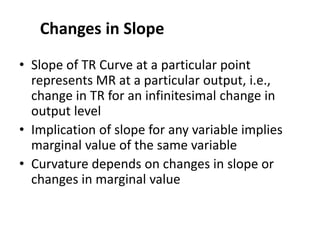

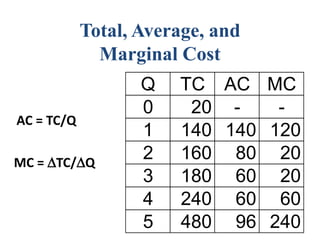

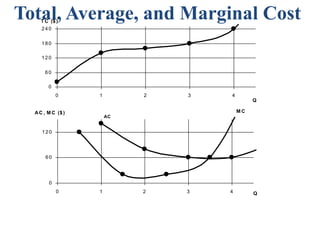

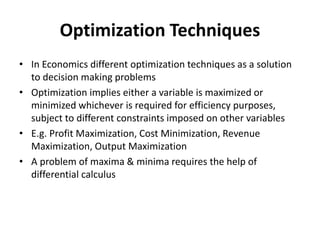

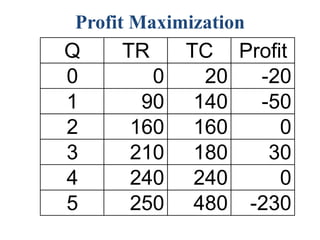

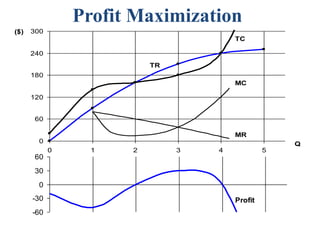

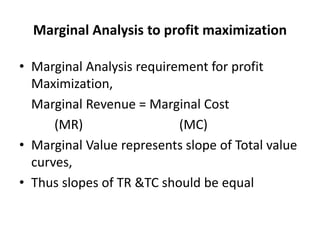

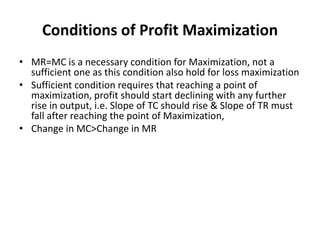

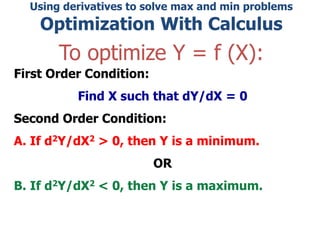

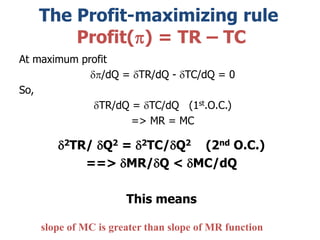

Models in economics provide simplified representations of real-world situations to better understand them. A key assumption in models is that all other relevant factors remain unchanged. The law of demand states that as price increases, quantity demanded decreases, and vice versa. Demand can be shown through schedules, curves, and functions relating price and quantity. Profit is maximized where marginal revenue equals marginal cost, satisfying both the first- and second-order conditions through the slopes of the total revenue and total cost curves.