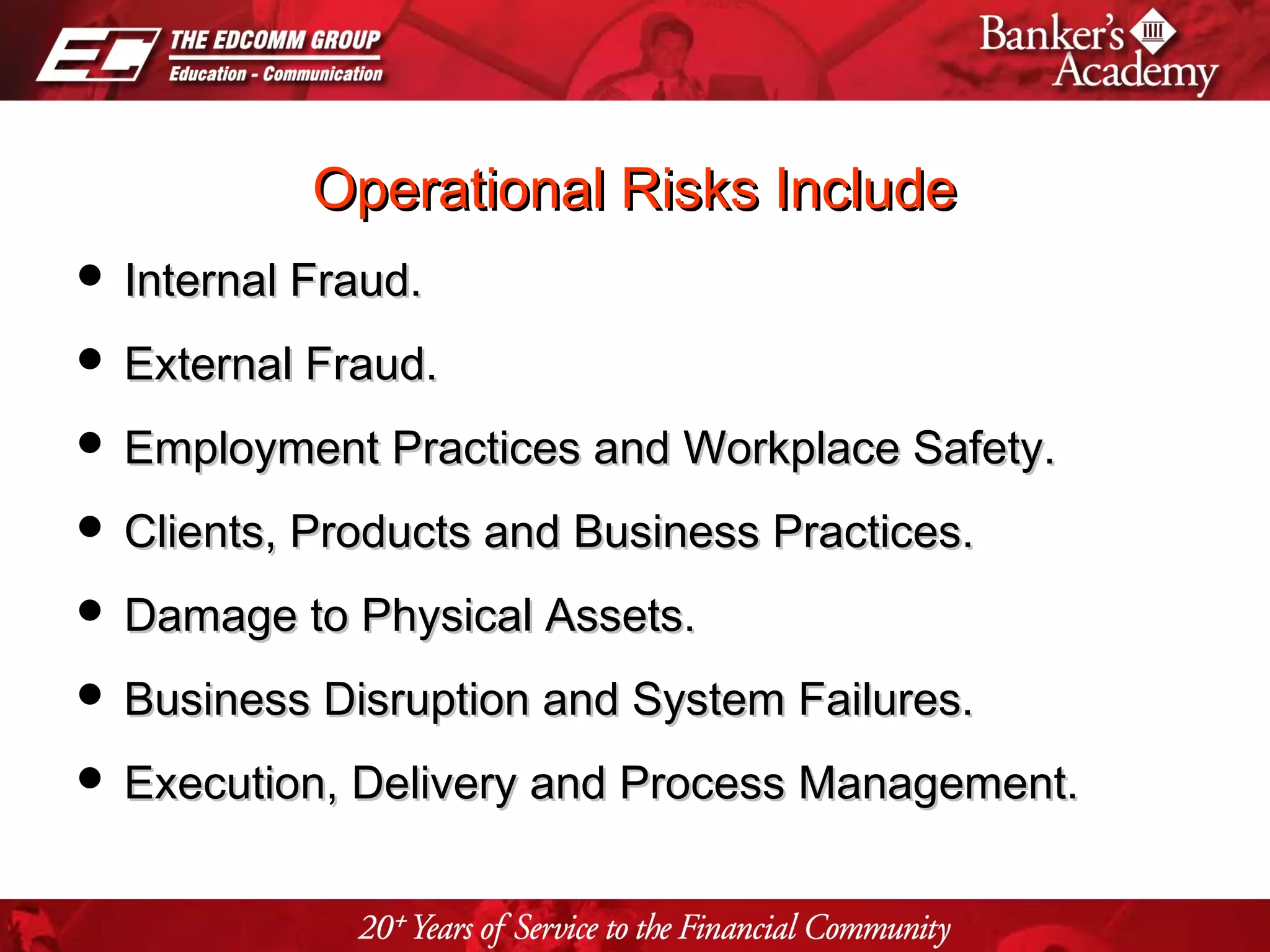

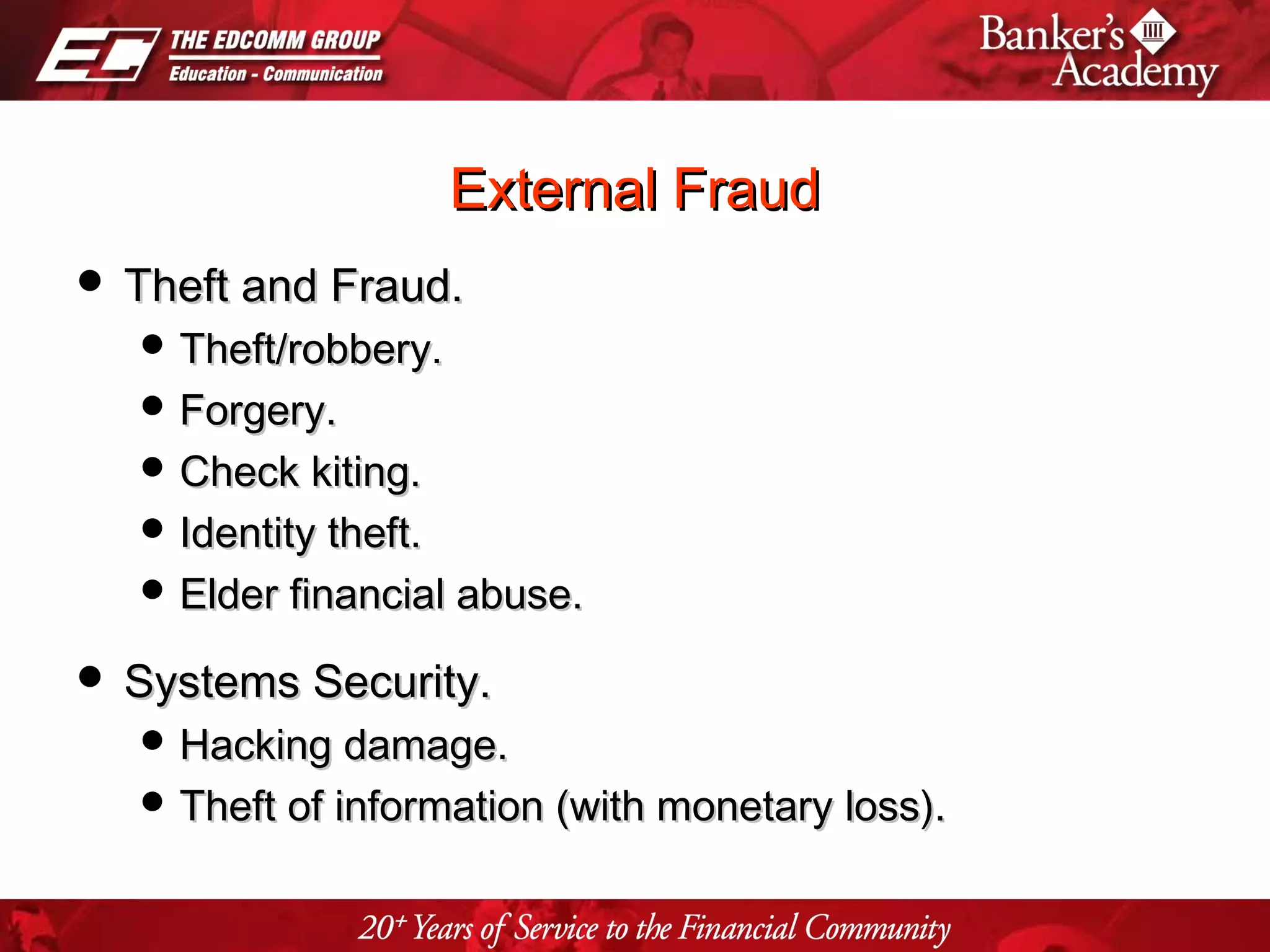

This document discusses various risks associated with online banking and technology-based banking products and services. It addresses operational risk, credit risk, and reputational risk. Operational risks include internal fraud, external fraud, business disruptions, system failures, and more. Credit risk relates to uncertainty in a counterparty's ability to meet obligations. Reputational risk could result from negative publicity, whether true or not, that leads to loss of customers, revenues, and increased costs. Effective risk management, including risk assessment and mitigation strategies, is important for banks offering online and technology-based services.