Acknowledgement

of Country

We acknowledgethat Country for Aboriginal peoples is an

interconnected set of ancient and sophisticated relationships.

The University of Wollongong spreads across many interrelated

Aboriginal Countries that are bound by this sacred landscape,

and intimate relationship with that landscape since creation.

From Sydney to the Southern Highlands, to the South Coast.

From fresh water to bitter water to salt. From City to Urban to Rural.

The University Acknowledges the devastating impact of colonisation

on our campuses’ footprint and commit ourselves to truth-telling,

healing and education.

3.

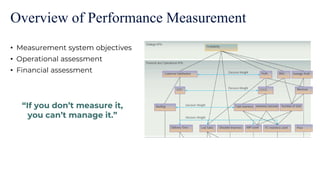

Overview of PerformanceMeasurement

• Measurement system objectives

• Operational assessment

• Financial assessment

4.

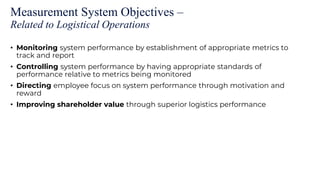

Measurement System Objectives–

Related to Logistical Operations

• Monitoring system performance by establishment of appropriate metrics to

track and report

• Controlling system performance by having appropriate standards of

performance relative to metrics being monitored

• Directing employee focus on system performance through motivation and

reward

• Improving shareholder value through superior logistics performance

Functional Perspective onLogistics Measures –

Major Categories

• Cost

• Customer service

• Quality

• Productivity

• Asset management

8.

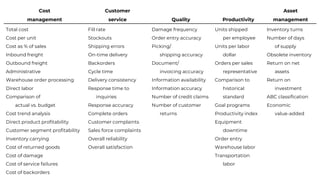

Cost

management

Customer

service Quality Productivity

Asset

management

Totalcost

Cost per unit

Cost as % of sales

Inbound freight

Outbound freight

Administrative

Warehouse order processing

Direct labor

Comparison of

actual vs. budget

Cost trend analysis

Direct product profitability

Customer segment profitability

Inventory carrying

Cost of returned goods

Cost of damage

Cost of service failures

Cost of backorders

Fill rate

Stockouts

Shipping errors

On-time delivery

Backorders

Cycle time

Delivery consistency

Response time to

inquiries

Response accuracy

Complete orders

Customer complaints

Sales force complaints

Overall reliability

Overall satisfaction

Damage frequency

Order entry accuracy

Picking/

shipping accuracy

Document/

invoicing accuracy

Information availability

Information accuracy

Number of credit claims

Number of customer

returns

Units shipped

per employee

Units per labor

dollar

Orders per sales

representative

Comparison to

historical

standard

Goal programs

Productivity index

Equipment

downtime

Order entry

Warehouse labor

Transportation

labor

Inventory turns

Number of days

of supply

Obsolete inventory

Return on net

assets

Return on

investment

ABC classification

Economic

value-added

9.

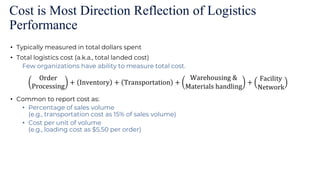

Cost is MostDirection Reflection of Logistics

Performance

• Typically measured in total dollars spent

• Total logistics cost (a.k.a., total landed cost)

Few organizations have ability to measure total cost.

• Common to report cost as:

• Percentage of sales volume

(e.g., transportation cost as 15% of sales volume)

• Cost per unit of volume

(e.g., loading cost as $5.50 per order)

Order

Processing

+ Inventory + Transportation +

Warehousing &

Materials handling

+

Facility

Network

10.

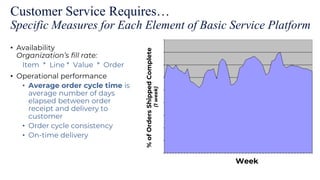

Customer Service Requires…

SpecificMeasures for Each Element of Basic Service Platform

• Availability

Organization’s fill rate:

Item * Line * Value * Order

• Operational performance

• Average order cycle time is

average number of days

elapsed between order

receipt and delivery to

customer

• Order cycle consistency

• On-time delivery

%

of

Orders

Shipped

Complete

(1

week)

Week

11.

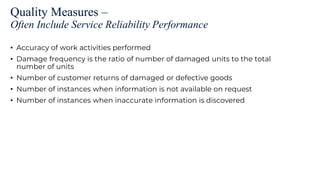

Quality Measures –

OftenInclude Service Reliability Performance

• Accuracy of work activities performed

• Damage frequency is the ratio of number of damaged units to the total

number of units

• Number of customer returns of damaged or defective goods

• Number of instances when information is not available on request

• Number of instances when inaccurate information is discovered

12.

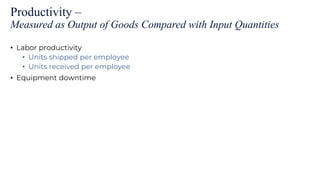

Productivity –

Measured asOutput of Goods Compared with Input Quantities

• Labor productivity

• Units shipped per employee

• Units received per employee

• Equipment downtime

13.

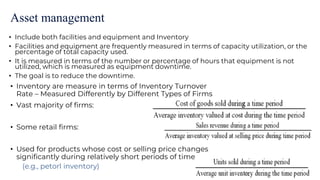

Asset management

• Inventoryare measure in terms of Inventory Turnover

Rate – Measured Differently by Different Types of Firms

• Vast majority of firms:

• Some retail firms:

• Used for products whose cost or selling price changes

significantly during relatively short periods of time

(e.g., petorl inventory)

• Include both facilities and equipment and Inventory

• Facilities and equipment are frequently measured in terms of capacity utilization, or the

percentage of total capacity used.

• It is measured in terms of the number or percentage of hours that equipment is not

utilized, which is measured as equipment downtime.

• The goal is to reduce the downtime.

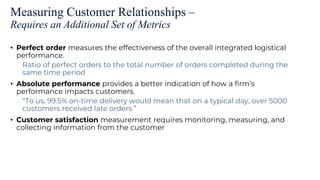

Measuring Customer Relationships–

Requires an Additional Set of Metrics

• Perfect order measures the effectiveness of the overall integrated logistical

performance.

Ratio of perfect orders to the total number of orders completed during the

same time period

• Absolute performance provides a better indication of how a firm’s

performance impacts customers.

“To us, 99.5% on-time delivery would mean that on a typical day, over 5000

customers received late orders.”

• Customer satisfaction measurement requires monitoring, measuring, and

collecting information from the customer

16.

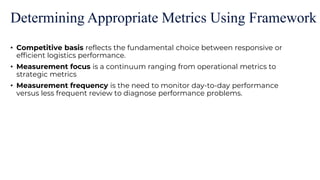

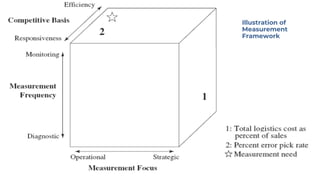

Determining Appropriate MetricsUsing Framework

• Competitive basis reflects the fundamental choice between responsive or

efficient logistics performance.

• Measurement focus is a continuum ranging from operational metrics to

strategic metrics

• Measurement frequency is the need to monitor day-to-day performance

versus less frequent review to diagnose performance problems.

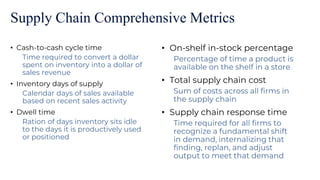

Supply Chain ComprehensiveMetrics

• Cash-to-cash cycle time

Time required to convert a dollar

spent on inventory into a dollar of

sales revenue

• Inventory days of supply

Calendar days of sales available

based on recent sales activity

• Dwell time

Ration of days inventory sits idle

to the days it is productively used

or positioned

• On-shelf in-stock percentage

Percentage of time a product is

available on the shelf in a store

• Total supply chain cost

Sum of costs across all firms in

the supply chain

• Supply chain response time

Time required for all firms to

recognize a fundamental shift

in demand, internalizing that

finding, replan, and adjust

output to meet that demand

19.

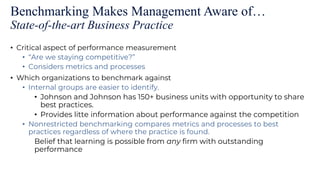

Benchmarking Makes ManagementAware of…

State-of-the-art Business Practice

• Critical aspect of performance measurement

• “Are we staying competitive?”

• Considers metrics and processes

• Which organizations to benchmark against

• Internal groups are easier to identify.

• Johnson and Johnson has 150+ business units with opportunity to share

best practices.

• Provides litte information about performance against the competition

• Nonrestricted benchmarking compares metrics and processes to best

practices regardless of where the practice is found.

Belief that learning is possible from any firm with outstanding

performance

Financial Assessment –

Neededto Link Supply Chain Performance to Financial Results

Critical tools for financial assessment

• Cost-revenue analysis

• Strategic profit model

22.

Cost-revenue Analysis –

Neededto Provide a Financial View of Integrated Logistics

• Accounting deficiencies make this difficult.

• Tools like activity-based costing (ABC) can help us better identify and control

logistics expenses

• Key Problems with Traditional Accounting

• Natural Account Aggregation.

• Transportation Expenditures

• Inventory Costs

• Three approaches are available to identify and control logistics expenses.

• Contribution

• Net profit

• Activity-based costing

23.

Contribution Analysis –

RequiresAll Costs be Identified as Fixed or Variable

• Fixed costs are those that do not directly change with volume.

• Variable costs are those that change as a result of volume.

• Direct costs are those specifically incurred because of the existence of the

segment of analysis

(e.g., product, customer, channel)

• Indirect costs exist because of more than one segment of business

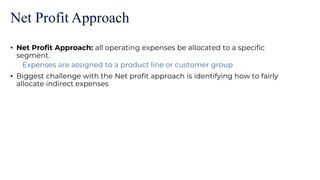

Net Profit Approach

•Net Profit Approach: all operating expenses be allocated to a specific

segment.

Expenses are assigned to a product line or customer group

• Biggest challenge with the Net profit approach is identifying how to fairly

allocate indirect expenses

26.

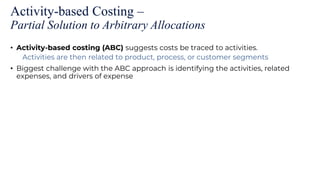

Activity-based Costing –

PartialSolution to Arbitrary Allocations

• Activity-based costing (ABC) suggests costs be traced to activities.

Activities are then related to product, process, or customer segments

• Biggest challenge with the ABC approach is identifying the activities, related

expenses, and drivers of expense

27.

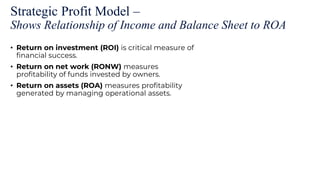

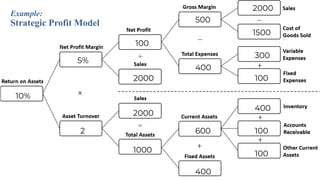

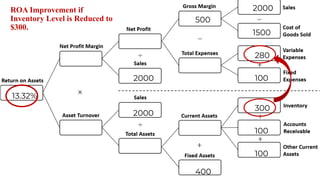

Strategic Profit Model–

Shows Relationship of Income and Balance Sheet to ROA

• Return on investment (ROI) is critical measure of

financial success.

• Return on net work (RONW) measures

profitability of funds invested by owners.

• Return on assets (ROA) measures profitability

generated by managing operational assets.

28.

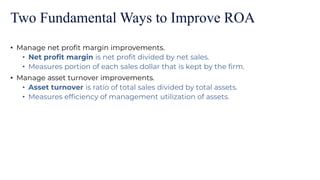

Two Fundamental Waysto Improve ROA

• Manage net profit margin improvements.

• Net profit margin is net profit divided by net sales.

• Measures portion of each sales dollar that is kept by the firm.

• Manage asset turnover improvements.

• Asset turnover is ratio of total sales divided by total assets.

• Measures efficiency of management utilization of assets.

![11. perf[1]. measrs (1)](https://cdn.slidesharecdn.com/ss_thumbnails/11-perf1-measrs1-110707064611-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Chapter 3 Performance Measures [Autosaved].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/chapter3performancemeasuresautosaved-250911044211-e0023b94-thumbnail.jpg?width=640&height=640&fit=bounds)

![Chapter 3 Performance Measures [Autosaved].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/chapter3performancemeasuresautosaved-250911045149-875c1566-thumbnail.jpg?width=640&height=640&fit=bounds)

![Chapter 3 Performance Measures [Autosaved].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/chapter3performancemeasuresautosaved-250911043631-784e40fa-thumbnail.jpg?width=640&height=640&fit=bounds)