Legislation behind Introduction of Section 43B(h) of Income Tax Act.docx

•Download as DOCX, PDF•

0 likes•53 views

Legislation behind Introduction of Section 43B(h) of Income Tax Act

Recommended

Recommended

More Related Content

Similar to Legislation behind Introduction of Section 43B(h) of Income Tax Act.docx

Similar to Legislation behind Introduction of Section 43B(h) of Income Tax Act.docx (20)

More from Ankur Mathur

Recently uploaded

Recently uploaded (20)

Legislation behind Introduction of Section 43B(h) of Income Tax Act.docx

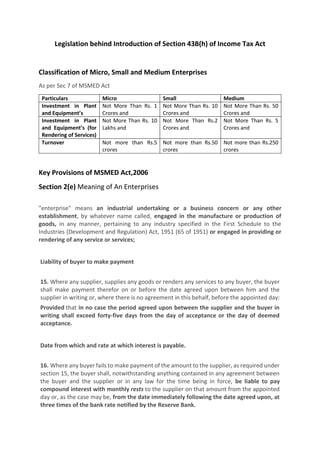

- 1. Legislation behind Introduction of Section 43B(h) of Income Tax Act Classification of Micro, Small and Medium Enterprises As per Sec 7 of MSMED Act Particulars Micro Small Medium Investment in Plant and Equipment’s Not More Than Rs. 1 Crores and Not More Than Rs. 10 Crores and Not More Than Rs. 50 Crores and Investment in Plant and Equipment’s (for Rendering of Services) Not More Than Rs. 10 Lakhs and Not More Than Rs.2 Crores and Not More Than Rs. 5 Crores and Turnover Not more than Rs.5 crores Not more than Rs.50 crores Not more than Rs.250 crores Key Provisions of MSMED Act,2006 Section 2(e) Meaning of An Enterprises "enterprise" means an industrial undertaking or a business concern or any other establishment, by whatever name called, engaged in the manufacture or production of goods, in any manner, pertaining to any industry specified in the First Schedule to the Industries (Development and Regulation) Act, 1951 (65 of 1951) or engaged in providing or rendering of any service or services; Liability of buyer to make payment 15. Where any supplier, supplies any goods or renders any services to any buyer, the buyer shall make payment therefor on or before the date agreed upon between him and the supplier in writing or, where there is no agreement in this behalf, before the appointed day: Provided that in no case the period agreed upon between the supplier and the buyer in writing shall exceed forty-five days from the day of acceptance or the day of deemed acceptance. Date from which and rate at which interest is payable. 16. Where any buyer fails to make payment of the amount to the supplier, as required under section 15, the buyer shall, notwithstanding anything contained in any agreement between the buyer and the supplier or in any law for the time being in force, be liable to pay compound interest with monthly rests to the supplier on that amount from the appointed day or, as the case may be, from the date immediately following the date agreed upon, at three times of the bank rate notified by the Reserve Bank.

- 2. Requirement to specify unpaid amount with interest in the annual statement of accounts. 22. Where any buyer is required to get his annual accounts audited under any law for the time being in force, such buyer shall furnish the following additional information in his annual statement of accounts, namely: — i. the principal amount and the interest due thereon (to be shown separately) remaining unpaid to any supplier as at the end of each accounting year; ii. the amount of interest paid by the buyer in terms of section 16, along with the amounts of the payment made to the supplier beyond the appointed day during each accounting year; iii. the amount of interest due and payable for the period of delay in making payment (which have been paid but beyond the appointed day during the year) but without adding the interest specified under this Act; iv. the amount of interest accrued and remaining unpaid at the end of each accounting year; and v. the amount of further interest remaining due and payable even in the succeeding years, until such date when the interest dues as above are actually paid to the small enterprise, for the purpose of disallowance as a deductible expenditure under section 23. Interest not to be allowed as deduction from income. 23. Notwithstanding anything contained in the Income-tax Act, 1961 (43 of 1961), the amount of interest payable or paid by any buyer, under or in accordance with the provisions of this Act, shall not, for the purposes of computation of income under the Income-tax Act, 1961, be allowed as deduction. Overriding effect. 24. The provisions of sections 15 to 23 shall have effect notwithstanding anything inconsistent therewith contained in any other law for the time being in force.

- 3. Non-Applicability of Sec 43B(h) This Section is not Applicable to Medium Enterprises Not Applicable on outstanding as on 31/03/2023 Section 43B(h) of Income Tax Act,1961 43B(h): - Any sum payable by the assessee to a micro or small enterprises, beyond the time limit specified in section 15 of the Micro, small and Medium Enterprises Development Act 2006. shall be allowed as deduction only on actual payment. Provided that nothing contained in this section [except the provisions of clause(h)] shall apply in relation to any sum which is actually paid by the assessee on or before the due date applicable in his case for furnishing the return of income under sub-section (1) of section 139 in respect of the previous year in which the liability to pay such sum was incurred as aforesaid and the evidence of such payment is furnished by the assessee along with such return Important Provisions As per clause 22 of the Tax Audit requires Tax Auditor to report the amount of interest inadmissible u/s 23 of the Micro, Small and Medium Enterprises Development Act, 2006 (MSMED, Act 2006). As per the definition of enterprises, only persons dealing in either Manufacturing of Goods or providing any services will be classified as an Enterprise. One could surely take a stand that trader /Retailer/Distributor, etc would not be classified as an Enterprise and would not be covered under the Micro or Small Enterprise definition Micro and Small Enterprise Facilitation Council (MSEFC) have been approached by Traders to get the benefits of provisions of delayed payments as per MSMED Act, 2006 available to MSEs. As per Office Memorandum No. No. 5/2(2)/2021-E/P & G/Policy (E-19025) date 02/07/2021 , the benefits to Retail and Wholesale trade MSMEs are restricted upto Priority Sector Lending only, and any other benefits, including provisions of delayed payments as per MSMED Act, 2006, are excluded. There may be a situation that an assessee issues a cheque to the MSME supplier and due to some reason MSME supplier don’t encash it within the due date. In light of the judgment of Hon’ble High Court of Punjab and Haryana in case of CIT v. Hindustan Wire Products Ltd. [2002] 120 Taxman 744 (Punjab & Haryana), disallowance u/s. 43B of the Act should not be attracted. However, the company will be required to prove that default of supplier in encashing the cheque through following documents – a) Copy of cheque with date of payment b) Copy of delivery of cheque to supplier.

- 4. If creditors are outstanding as on March 31 for a period exceeding 45 days or 15 days, as the case may be, the that expenses will be disallowed for the relevant year, and it will be allowed in the year in which the said payment is made. Generally, as per section 43B disallowances, expenses are allowed as deduction if it is paid on or before due date of filing return of income as prescribed under section 139. It is not the case with section 43B(h) disallowances, where in it will be allowed as expenses in the year in which the same is paid. Currently, MCA vide notification “Specified Companies (Furnishing of Information about payment to micro and small enterprise suppliers) Order, 2019” dated 22nd January 2019, mandates that, all specified companies who buy goods or avail services from micro and small enterprises and whose payments to such suppliers have exceeded 45 days shall submit a half yearly return(eform MSME Form I) to the ministry of corporate affairs (MCA) stating the following:- the outstanding amount due and the reasons for delay; The Interest paid on delayed payment under section 16 of the act, to be disallowed while calculating income of the assessee and the same to be reported in clause 22 of part B in Form 3CD of Tax audit report. If Section 43B(h) applicable and assessee fails to deduct TDS on 194Q is not deducted and payment is not made within the stipulated time of 45 days, the whole amount will be disallowed u/s 43B(h) and not 40(ia) as 43B(h) disallows whole amount, 40ia is not applicable as it talks about deduction from expenses claimed. If expense is disallowed, there is no question of claiming it in return. Non-Deduction of TDS is reported under Form 3CD and Disallowance u/s 43B is shown in Clause 26 of Tax Audit Report. Adjustment is made in the computation of Income and Income Tax Provision is calculated accordingly along with the adequate reporting under Income Tax Act. Disallowance u/s. 43B of the Act in respect of an amount payable to MSMEs suppliers will not be attracted if the amount payable to MSMEs suppliers is cleared before the end of the financial year. Purchase on or before 16th March 2024 will attract disallowance u/s. 43B of the IT Act if payment is not cleared before the end of that financial year. (Provided no due date has been agreed in writing). Purchase after 16th March 2024 will not attract disallowance u/s 43B, if paid within the stipulated time frame. Ankur Mathur B.Com(Hons), Semi Qualified CA