This document provides an overview of the Islamic financing contract of Istisna'.

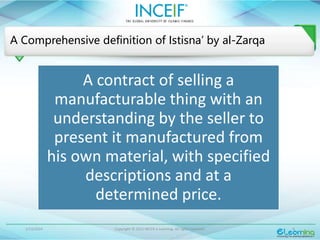

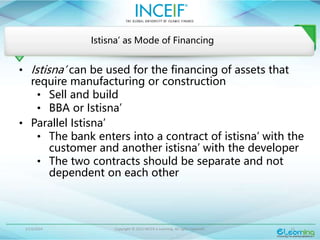

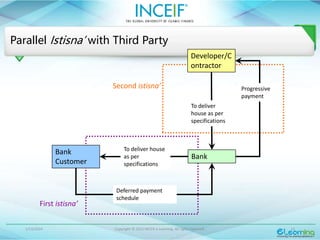

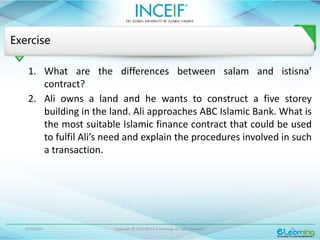

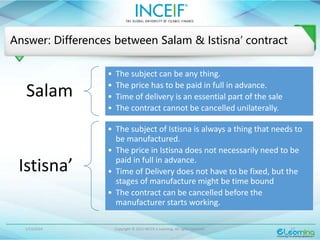

Istisna' is a contract where a person sells a specific product that involves both raw materials and labor for a known price, to be delivered at a specified future date. It is used to finance the manufacturing or construction of assets.

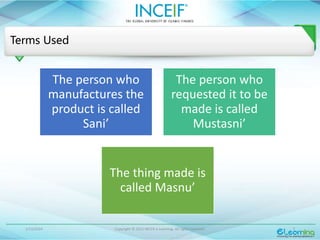

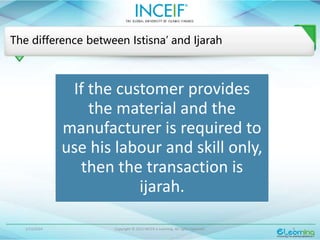

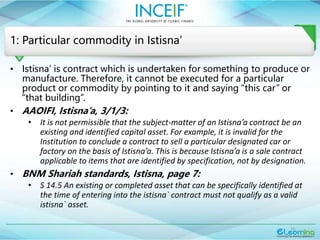

The key characteristics of Istisna' discussed are: it must involve both raw materials and labor; the item must be precisely described; delivery dates and payment terms must be specified; and the contract is binding on both parties. Istisna' is distinguished from other contracts like Salam, Ijarah, and Ju'alah. Issues around the nature of the commodity,