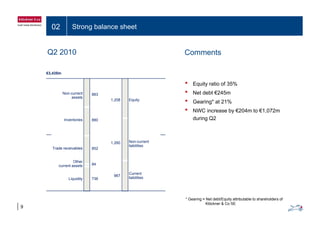

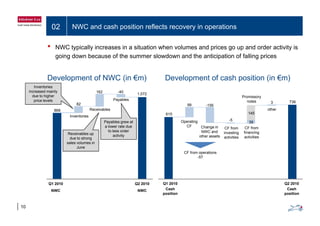

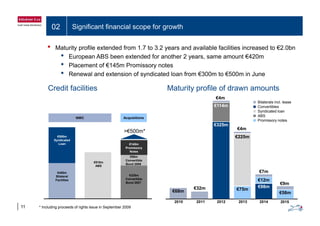

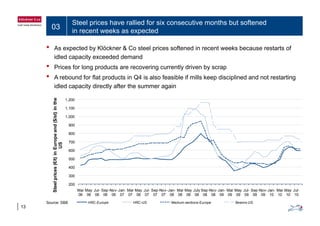

Download to read offline

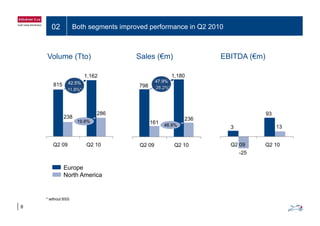

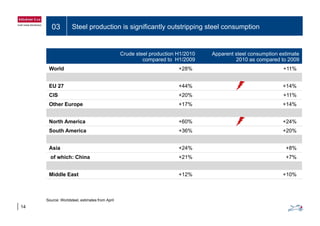

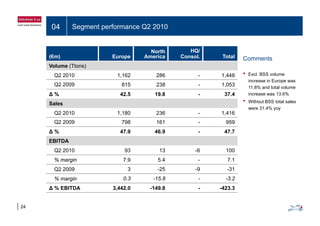

Klöckner & Co SE is a leading steel and metal distributor with a network of around 250 distribution locations in Europe and North America. In Q2 2010, Klöckner saw strong growth with sales up 37.4% to €1.4 billion and EBITDA increasing 423.3% to €100 million compared to Q2 2009, driven by economic recovery, price increases, cost cutting, and acquisitions. Klöckner expects volumes to be seasonally lower in Q3 but full year sales to increase over 25% and EBITDA to exceed €200 million, supported by continued economic growth and integration of acquisitions.