Download to read offline

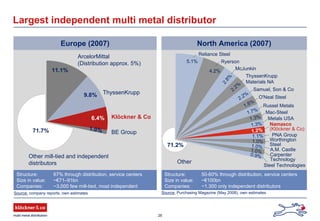

+49 203 307 2123 Fax: +49 203 307 2040 E-mail: christina.kiessling@kloeckner.com E-mail: jenny.hilgers@kloeckner.com Klöckner & Co SE Am Silberpalais 1 47057 Duisburg Germany www.kloeckner.com IR contact details 26 Largest independent multi metal distributor - Leading independent distributor of steel and metal products - Broad product portfolio including steel, stainless steel, aluminum and other metals - Strong market positions in Europe and North America - Over 160 service