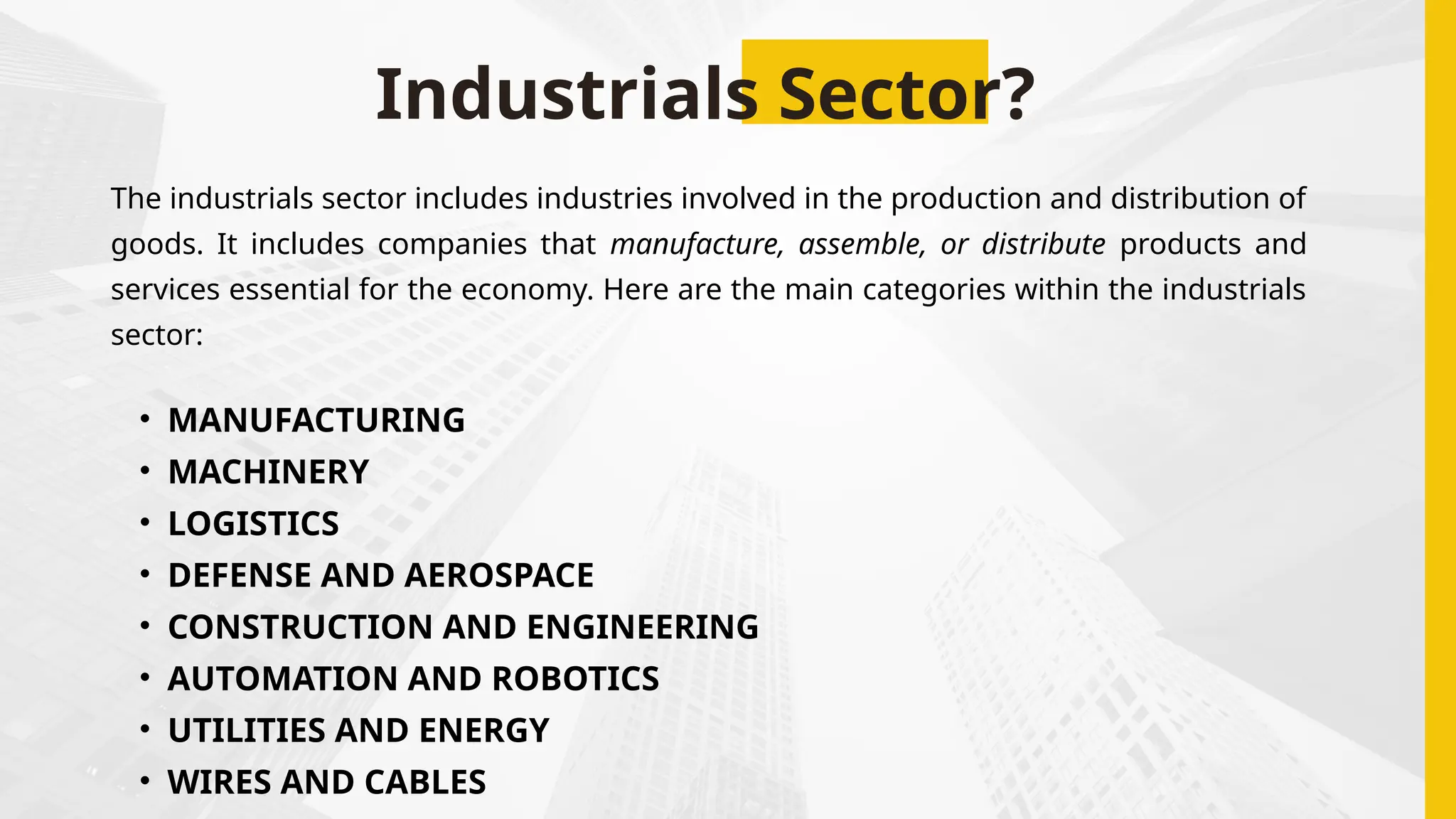

Industrials Sector?

The industrialssector includes industries involved in the production and distribution of

goods. It includes companies that manufacture, assemble, or distribute products and

services essential for the economy. Here are the main categories within the industrials

sector:

• MANUFACTURING

• MACHINERY

• LOGISTICS

• DEFENSE AND AEROSPACE

• CONSTRUCTION AND ENGINEERING

• AUTOMATION AND ROBOTICS

• UTILITIES AND ENERGY

• WIRES AND CABLES

3.

Why it isimportant?

Economic Growth: Major contributor to GDP.

Job Creation: Generates millions of jobs.

Innovation: Drives research and development.

Global Trade: Facilitates exports and imports.

Infrastructure Development: Supports essential infrastructure.

Resource Utilization: Promotes efficient resource management.

Economic Resilience: Diversifies economies against shocks.

Regional Development: Stimulates urban and rural growth.

National Security: Vital for defense manufacturing.

6.

DEFENSE AND AEROSPACE

•The industries that design, develop, produce, and maintain airplanes,

spacecraft, missiles, and military systems are referred to as aerospace and

defense industries.

• These sectors are essential to the evolution of technology, global economic

growth, and national security.

• While the defense industry is mostly concerned with military capabilities

and national security, the aerospace sector has both civilian and military

uses.

• The aerospace and defense market is driven by several factors including

growing air travel demand, technological advancements, increasing space

activities, rising military modernization and increasing investment in the

aerospace and defense industry.

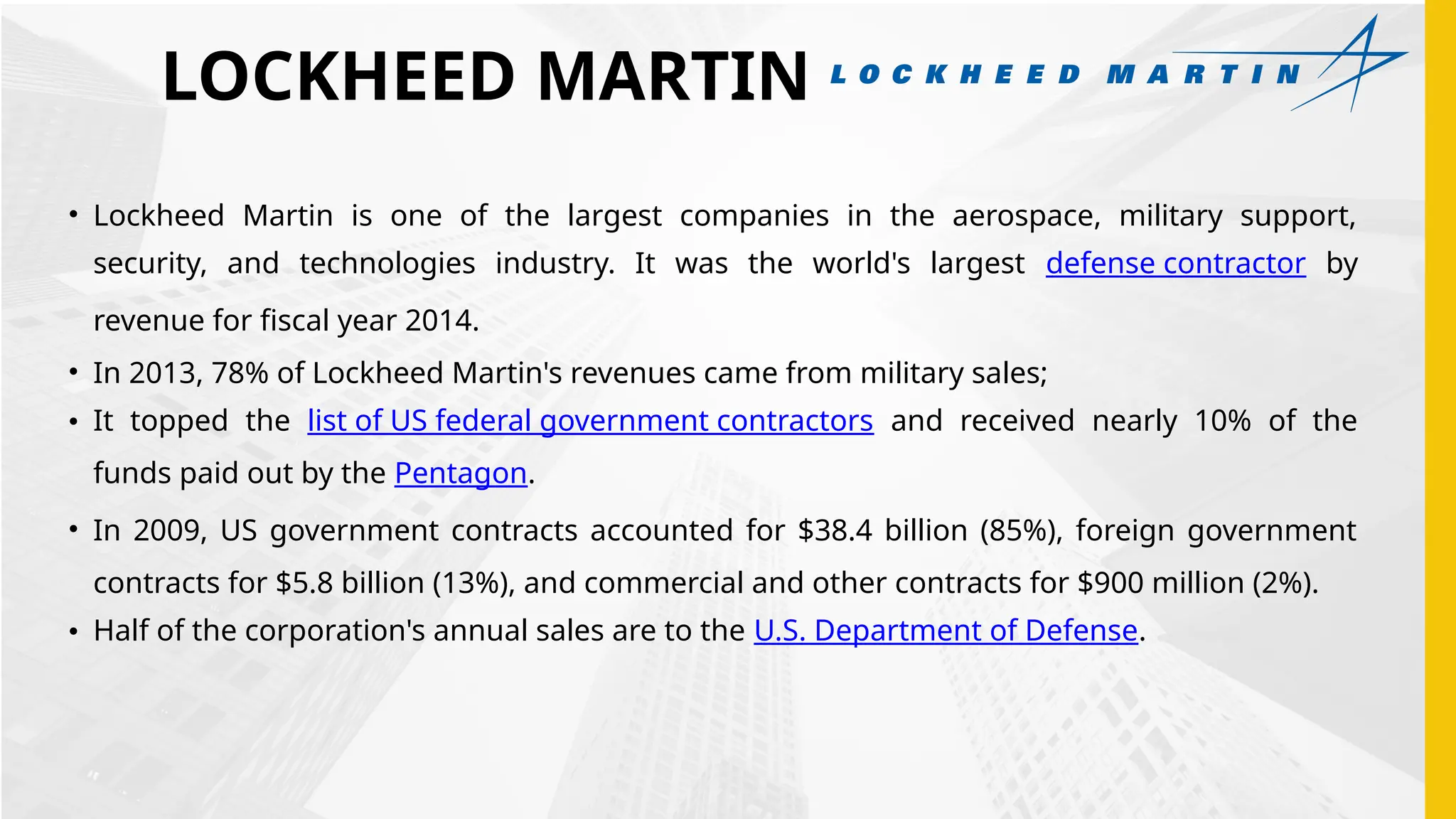

LOCKHEED MARTIN

• LockheedMartin is one of the largest companies in the aerospace, military support,

security, and technologies industry. It was the world's largest defense contractor by

revenue for fiscal year 2014.

• In 2013, 78% of Lockheed Martin's revenues came from military sales;

• It topped the list of US federal government contractors and received nearly 10% of the

funds paid out by the Pentagon.

• In 2009, US government contracts accounted for $38.4 billion (85%), foreign government

contracts for $5.8 billion (13%), and commercial and other contracts for $900 million (2%).

• Half of the corporation's annual sales are to the U.S. Department of Defense.

• Increasing airtravel demand drives market growth

• A greater demand for air travel is a result of the expanding global economy and growing

middle class, which drives the rise of commercial aviation and the requirement for new

aircraft.

• By 2036, the aviation sector will have generated $1.5 trillion in GDP and 15.5 million direct

employments for the global economy if its current development trajectory is maintained.

• Upon accounting for the effects of international tourism, these figures may increase to 97.8

million employment and $5.7 trillion in GDP.

• Over 200,000 aircraft a day are anticipated to take off and land worldwide by the middle of the

2030s.

AEROSPACE AND DEFENSE MARKET: GROWTH DRIVERS

16.

AEROSPACE AND DEFENSEMARKET: RESTRAINTS

• Emission and environmental impact hampers market growth

• The aerospace sector has problems in developing more environmentally friendly and

sustainable technology due to increased scrutiny of emissions and environmental effects.

• For instance, according to the International Energy Agency, with its growth in the last several

decades outpacing that of rail, road, or shipping, aviation accounted for 2% of the world's

energy-related CO2 emissions in 2022.

• Following the Covid-19 epidemic, demand for international travel has recovered, and as a

result, aircraft emissions in 2022 reached about 800 Mt CO2 or 80% of the level before the

pandemic.

17.

AEROSPACE AND DEFENSEMARKET: OPPORTUNITIES

• Growing defense spending provides a lucrative opportunity for market growth

• The growing defense spending in the countries like US, China, and India is expected to propel

the market growth during the forecast period.

• According to rankings, the US is the top defense exporter and producer in the world. US

military spending rose to USD 801 billion from USD 778.23 billion the year before, an almost

2.9% rise. With 38% of all military spending last year, the United States remained the largest

spender worldwide.

• The Department of Defense (DoD) has a budget authorization of about USD 722 billion for FY

2022, up USD 17 billion from USD 705 billion in 2020.

18.

AEROSPACE AND DEFENSEMARKET: CHALLENGES

• Regulatory compliance and technological concerns pose a major challenge to market growth

• Adherence to strict safety and security protocols, particularly in the aviation domain, can

provide obstacles for enterprises, hence impacting the schedules and expenses associated

with product development.

• Complicated and time-consuming procedures are frequently involved in the development of

cutting-edge aerospace and defense technology, which causes delays and cost overruns.

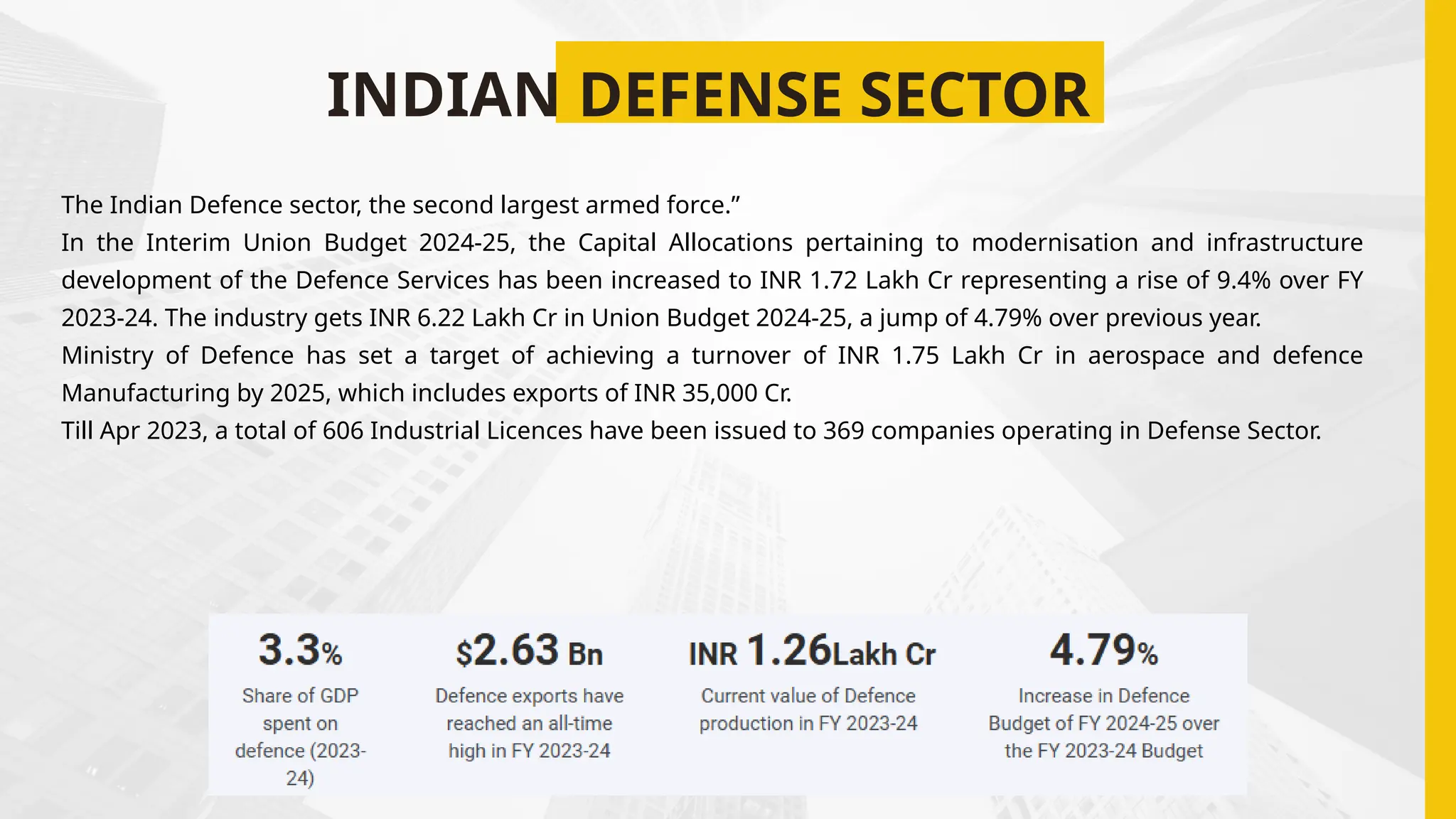

INDIAN DEFENSE SECTOR

TheIndian Defence sector, the second largest armed force.”

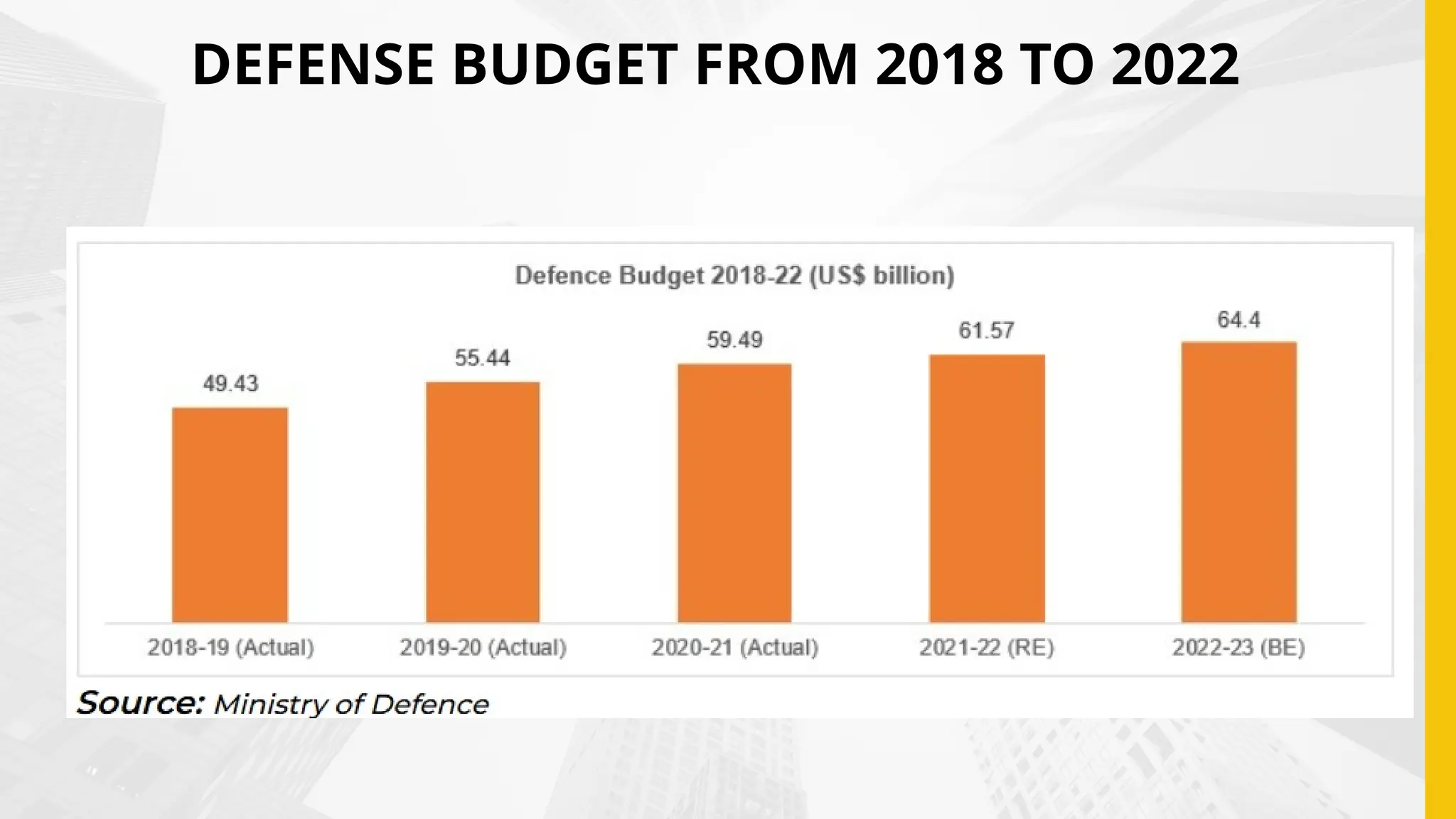

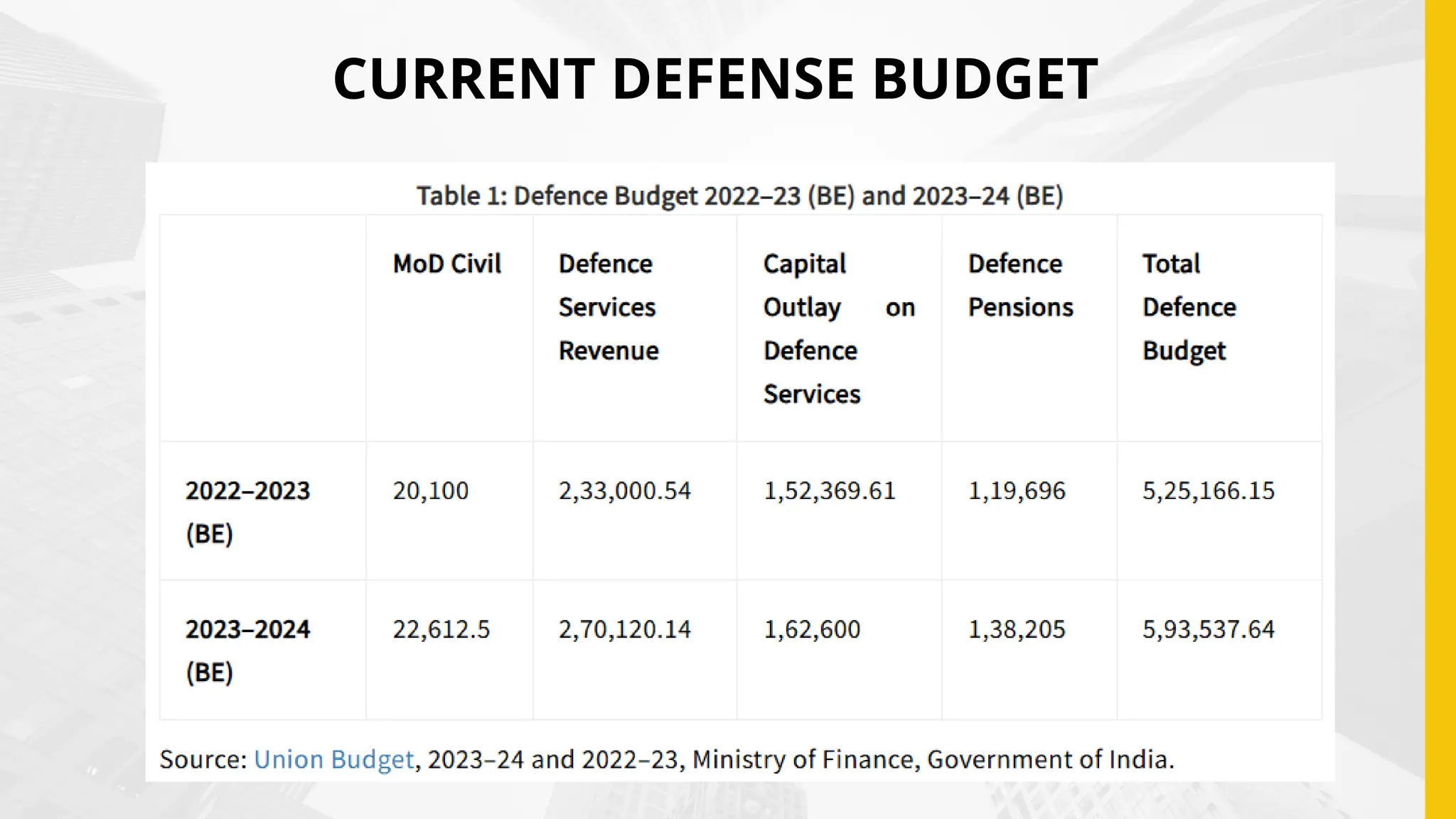

In the Interim Union Budget 2024-25, the Capital Allocations pertaining to modernisation and infrastructure

development of the Defence Services has been increased to INR 1.72 Lakh Cr representing a rise of 9.4% over FY

2023-24. The industry gets INR 6.22 Lakh Cr in Union Budget 2024-25, a jump of 4.79% over previous year.

Ministry of Defence has set a target of achieving a turnover of INR 1.75 Lakh Cr in aerospace and defence

Manufacturing by 2025, which includes exports of INR 35,000 Cr.

Till Apr 2023, a total of 606 Industrial Licences have been issued to 369 companies operating in Defense Sector.

CURRENT HIGHLIGHTS OFBUDGET OF DEFENSE

SECTOR IN INDIA

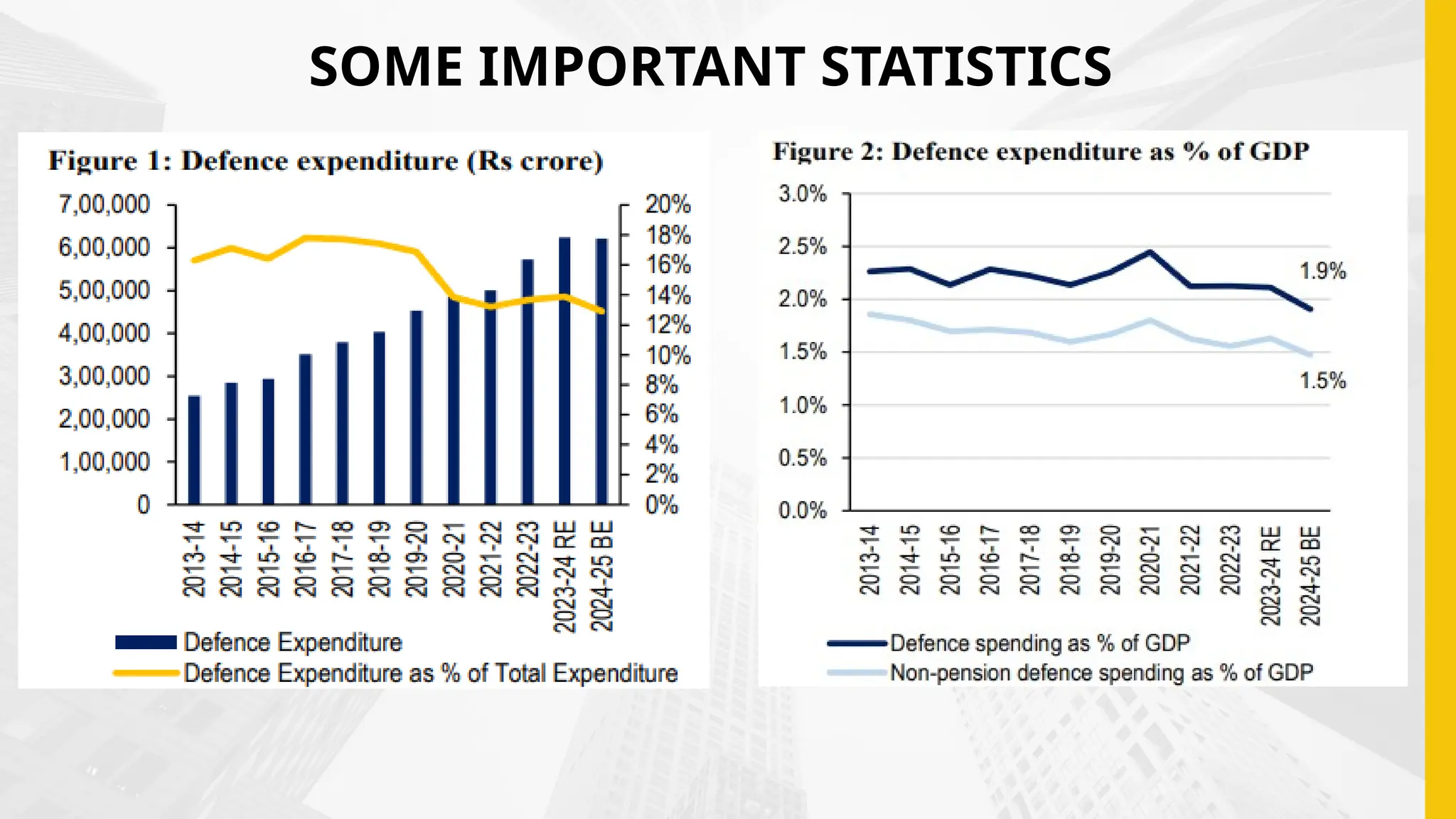

• India among top global military spenders but expenditure declines as share of budget

• Budget allocation lower than projected needs of the armed forces

• More than 20% of the defence budget is spent on pension

• Capital outlay has remained below 30% of the defence budget

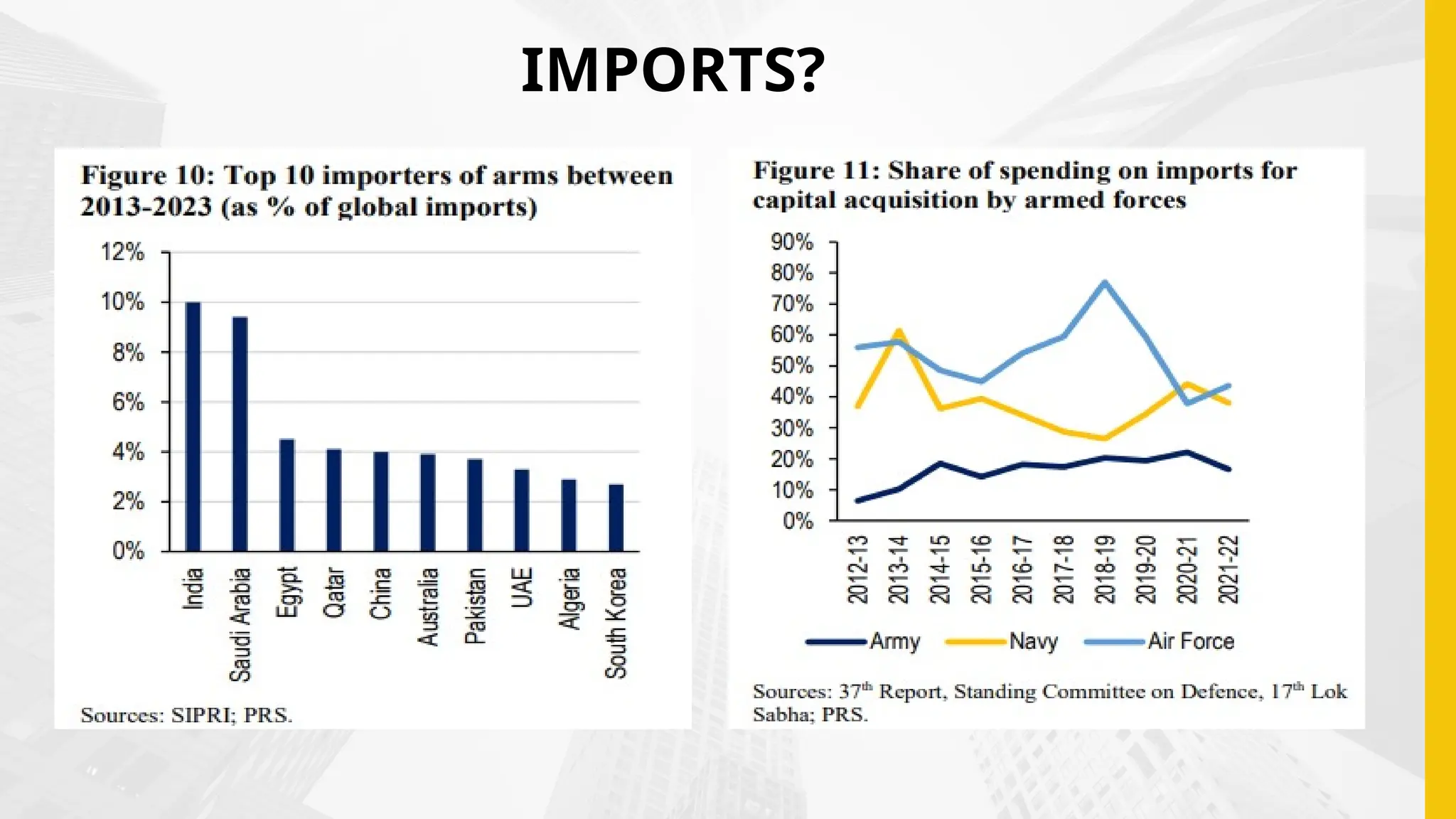

• Navy: Significant increase in funds allocated for modernisation over last decade

• Air Force: Funds allocated for modernisation may not be sufficient to replace ageing

planes

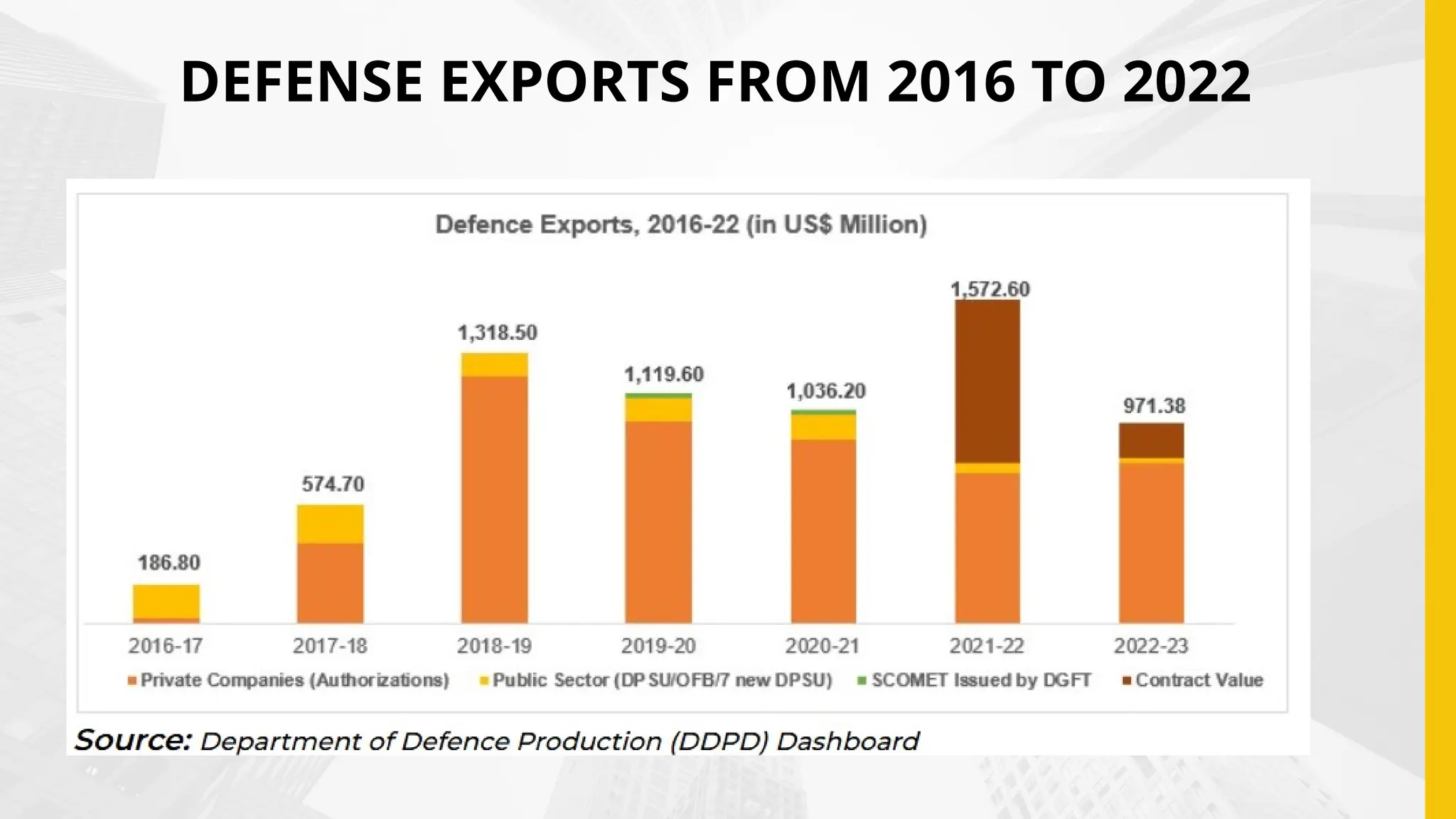

• India continues to be the largest importer of arms in the world

• Defence exports have increased but India’s share in global exports miniscule

• Share of defence budget spent on R&D has decreased in recent years

WHERE DO THISSECTOR STAND IN NEXT 5 YEARS?

• Increased Indigenous Production

• Advanced Technologies

• Enhanced Collaboration

• Improved Logistics and Efficiency

• Modernized Forces

• Focus on Cyber and Space Defense:

• Skilled Workforce

#8 Parul

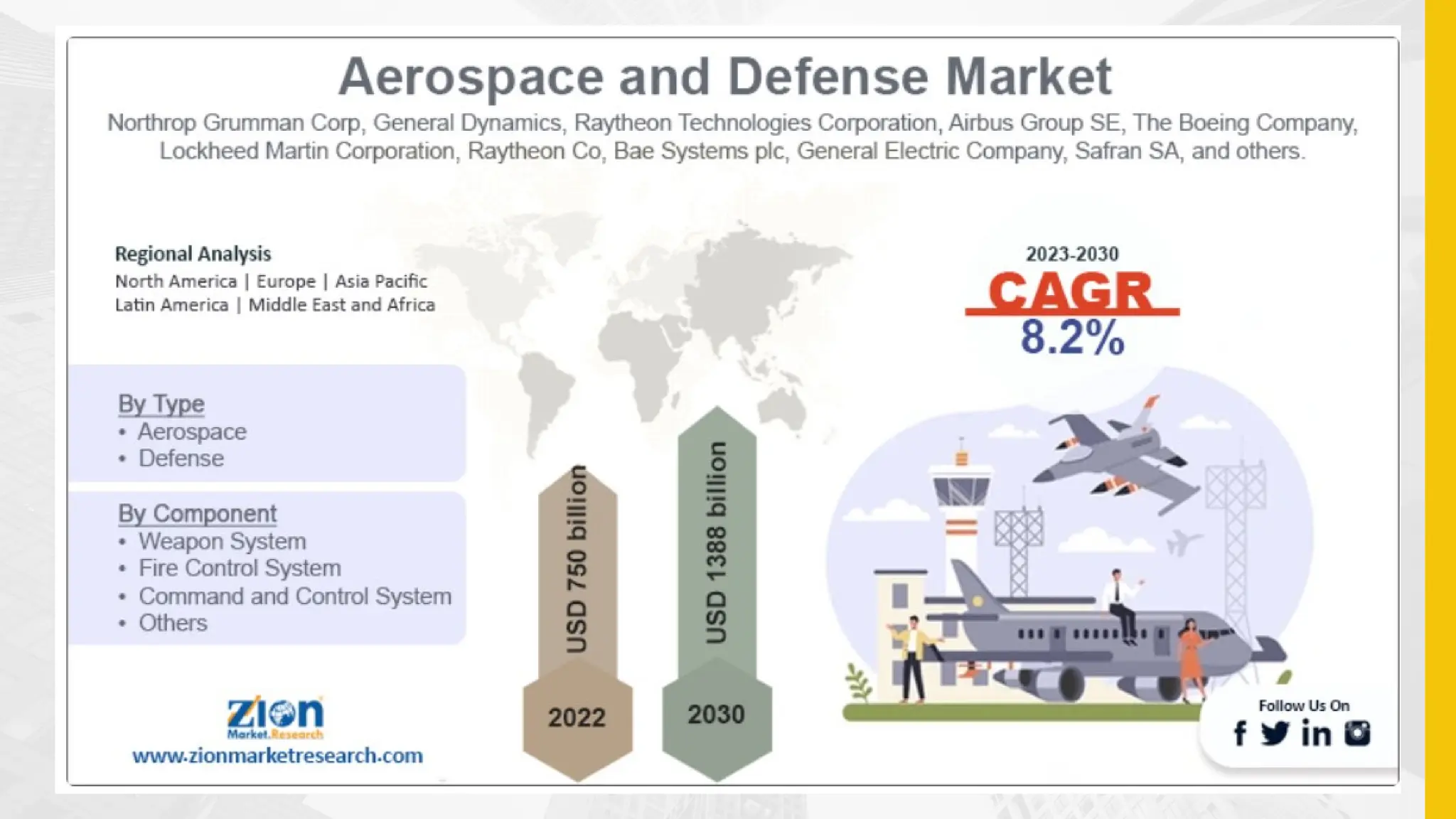

As per the analysis, the global aerospace and defense market is estimated to grow annually at a CAGR of around 8.2% over the forecast period (2023-2030).

In terms of revenue, the global aerospace and defense market size was valued at around USD 750 billion in 2022 and is projected to reach USD 1388 billion, by 2030.

The growing investment in the aerospace and defense sector is expected to drive the revenue growth of the aerospace and defense industry.

#9 J

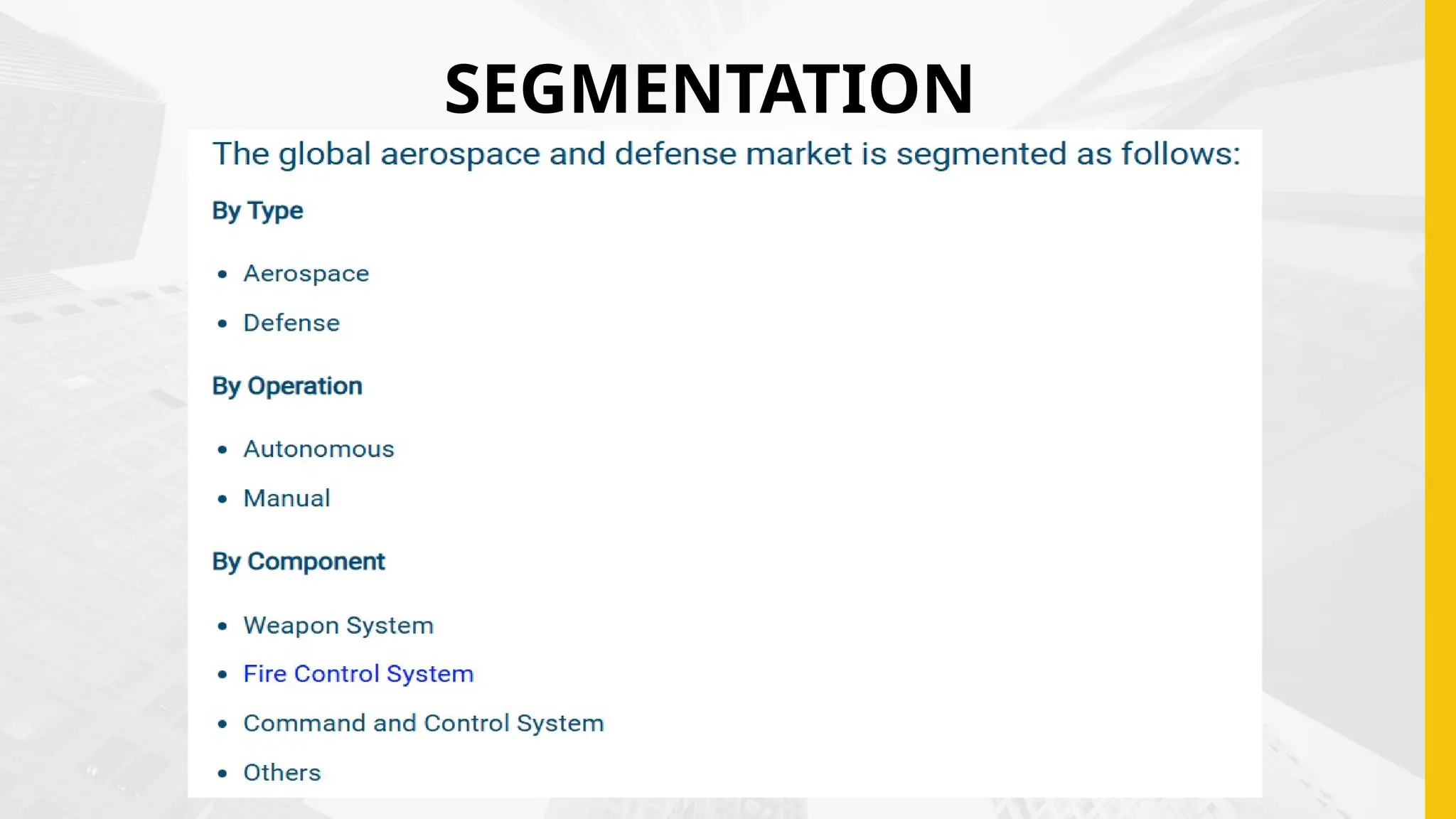

Based on the type, the defense segment is expected to hold a prominent market share over the forecast period.

Based on the operation, the autonomous segment is expected to grow at the fastest rate over the projected period.

Based on the components, the weapon system segment is expected to capture a significant market share during the forecast.

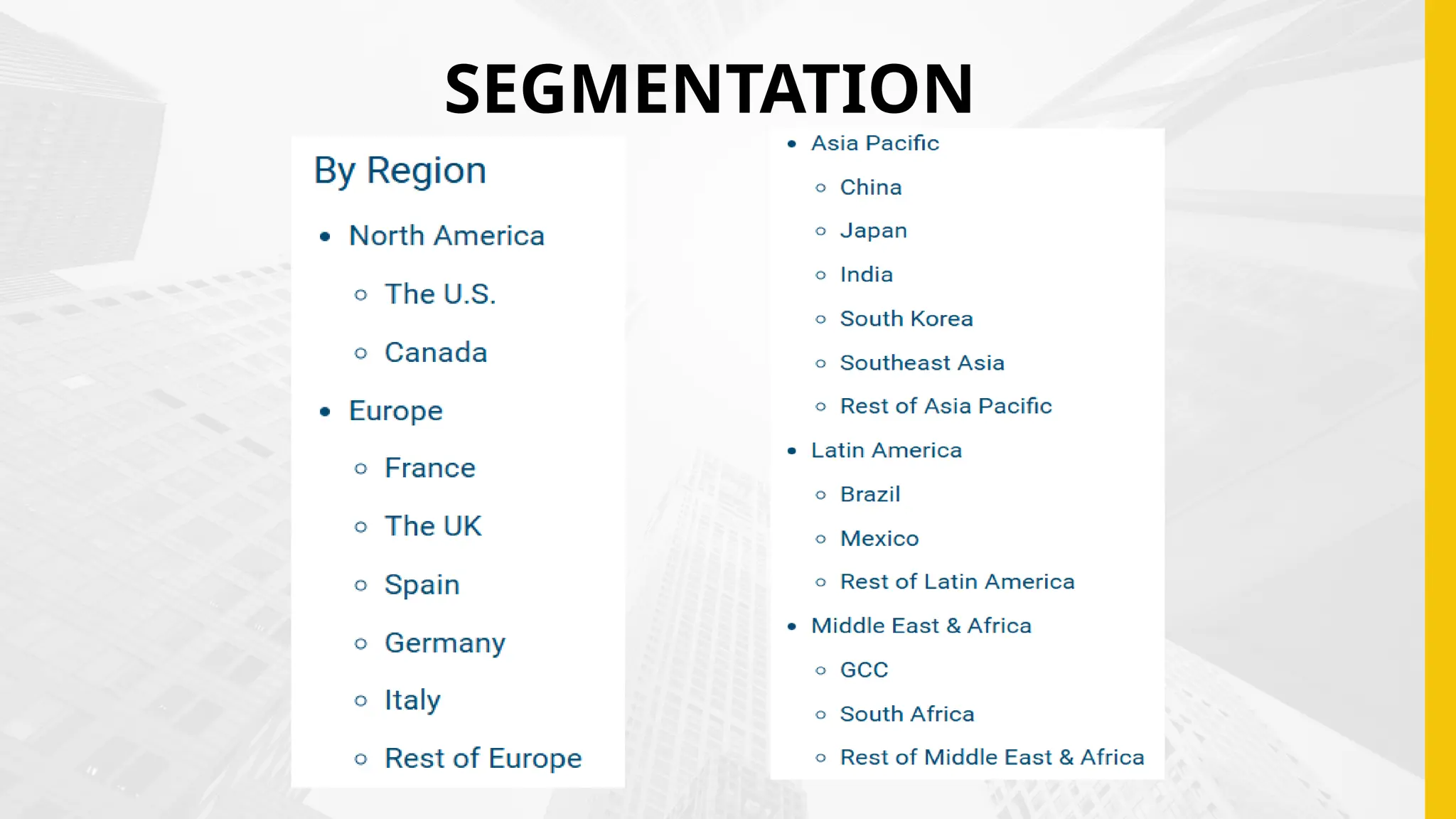

Based on region, North America is expected to dominate the market during the forecast period.

#33 J

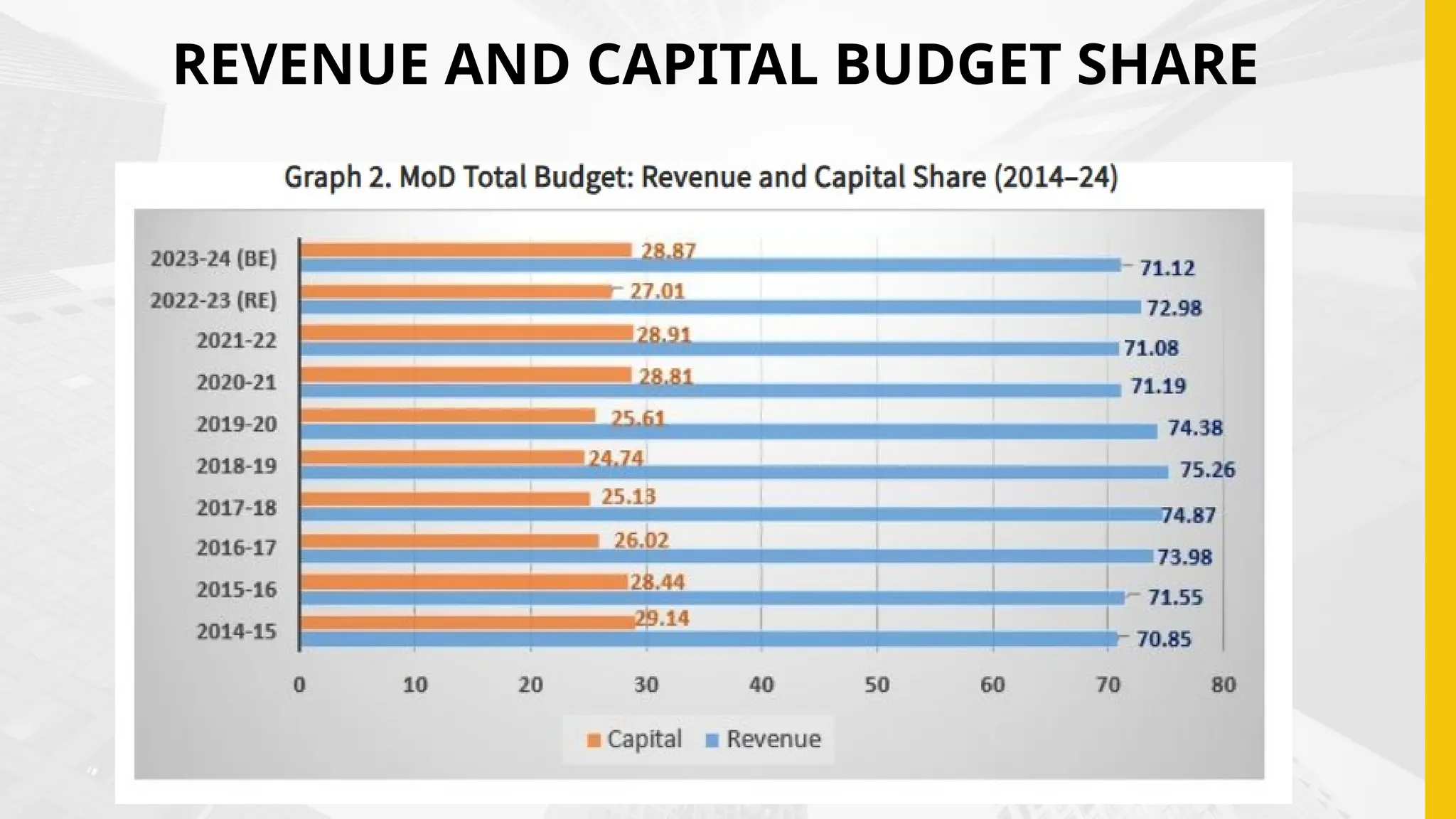

THIS GRAPH GIVES THE BREAKDOWN OF REVENUE AND CAPITAL EXPENDITURE FROM 2014 TO 2024. DURING THE PERIOD 2016–20, REVENUE EXPENDITURE WAS OVER 72 PER CENT OF THE TOTAL ALLOCATIONS, AND EVEN EXCEEDED 75 PER CENT IN 2018–19. THE CAPITAL SHARE OF THE BUDGET WAS OVER 29 PER CENT IN 2014–15 AND IS ESTIMATED TO BE NEARLY 29 PER CENT IN BE 2023–24. IN 2018–19, IT FELL BELOW 25 PER CENT AS A PERCENTAGE OF TOTAL ALLOCATIONS.

#35 P

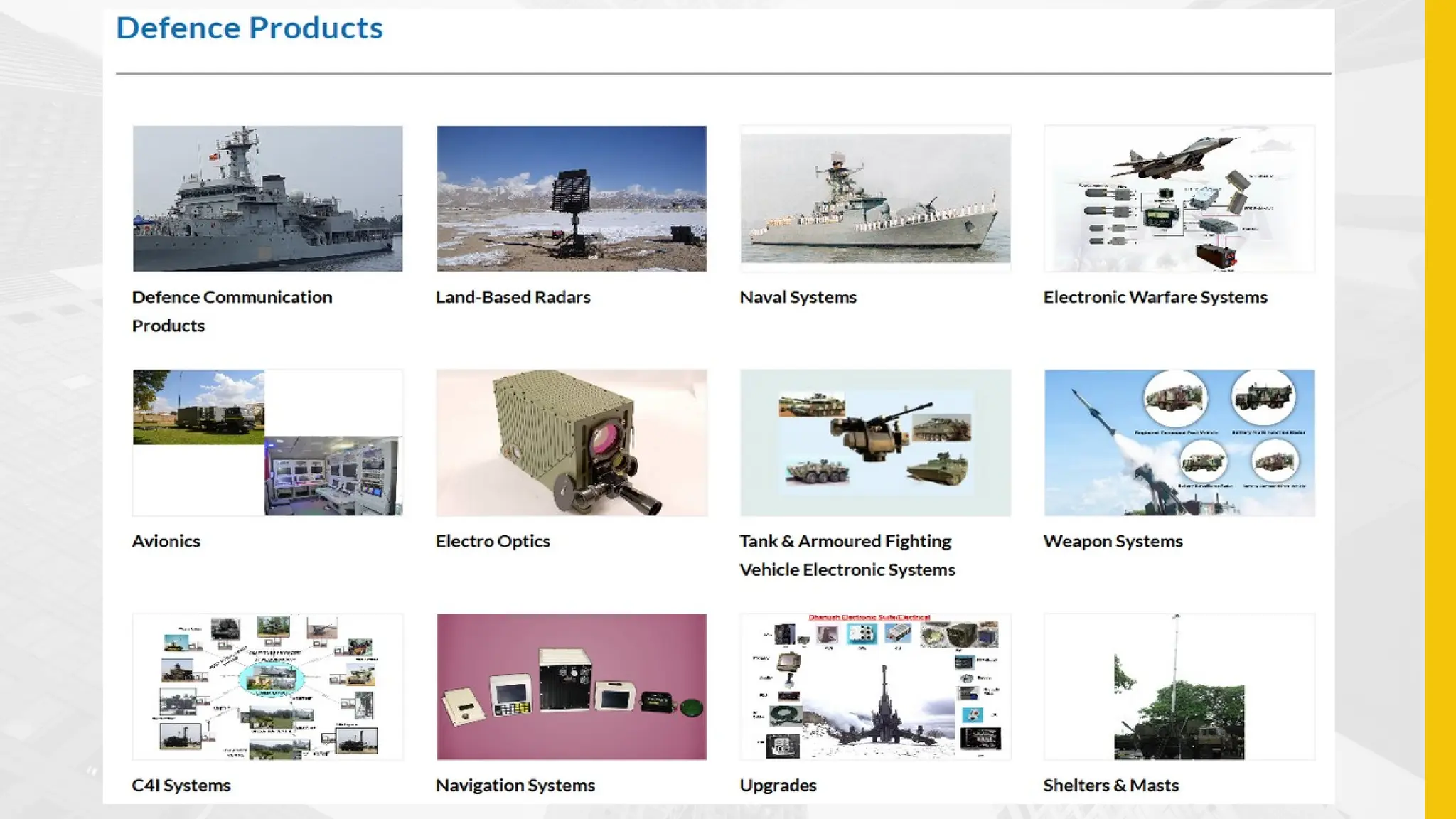

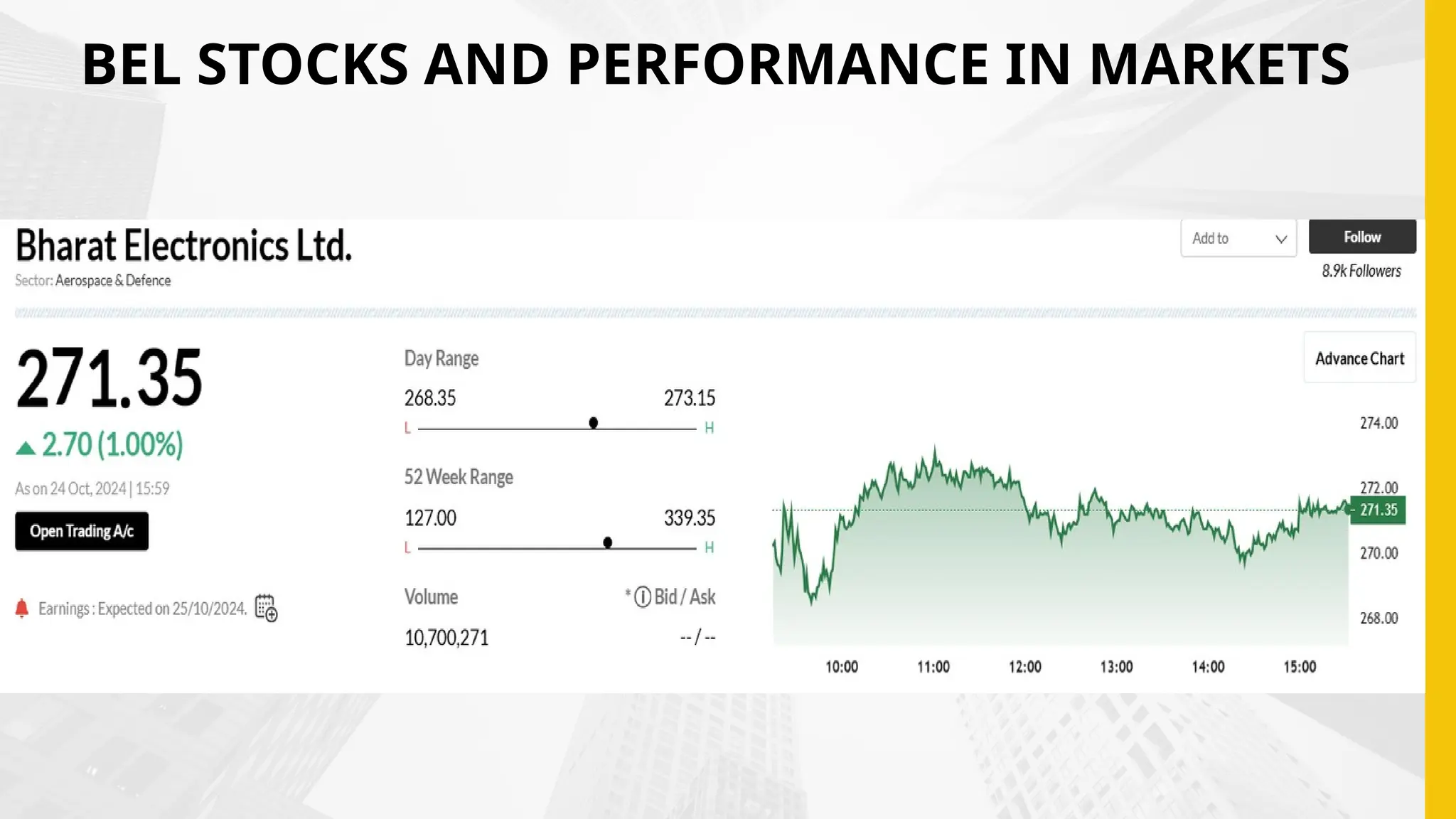

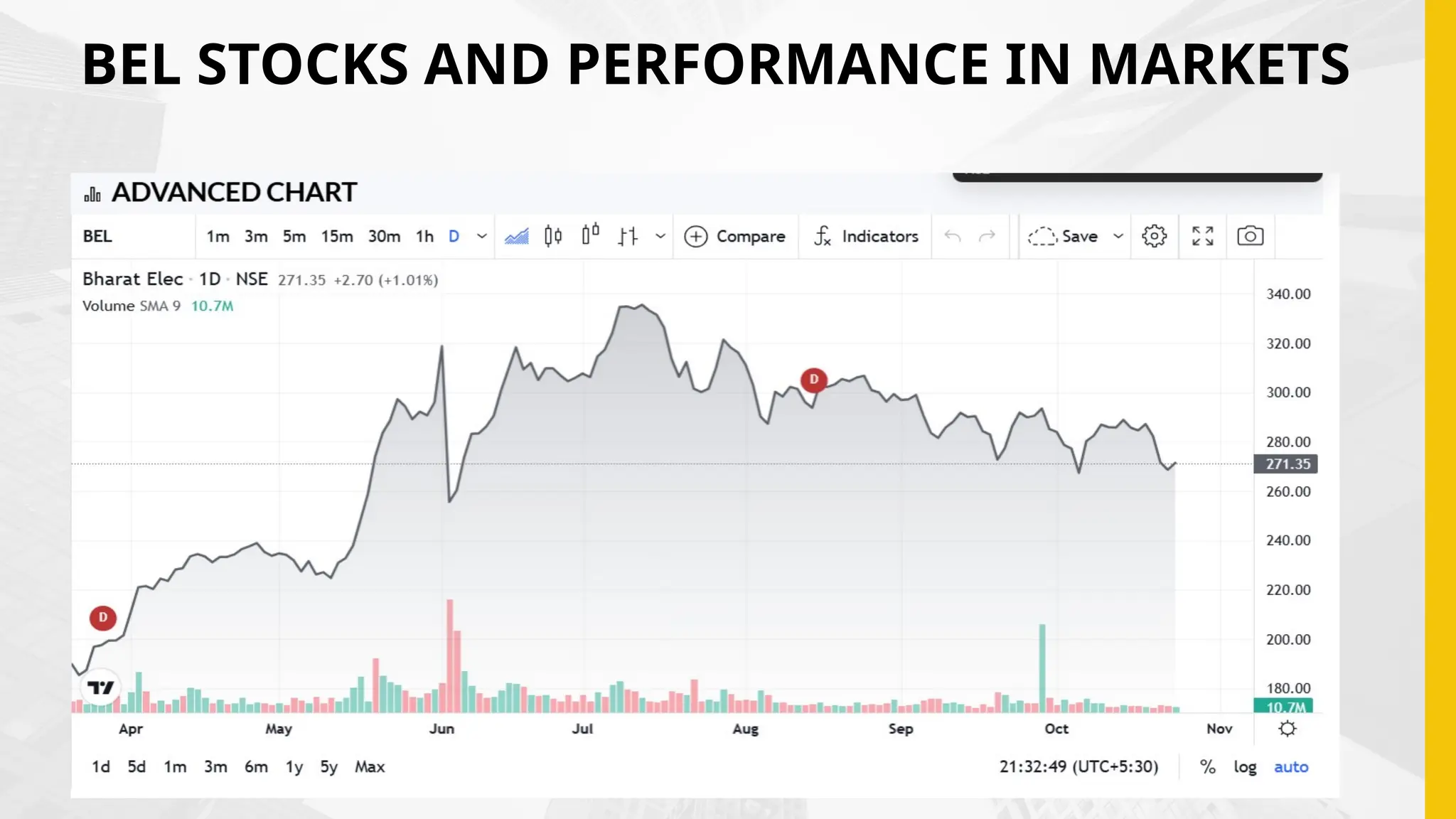

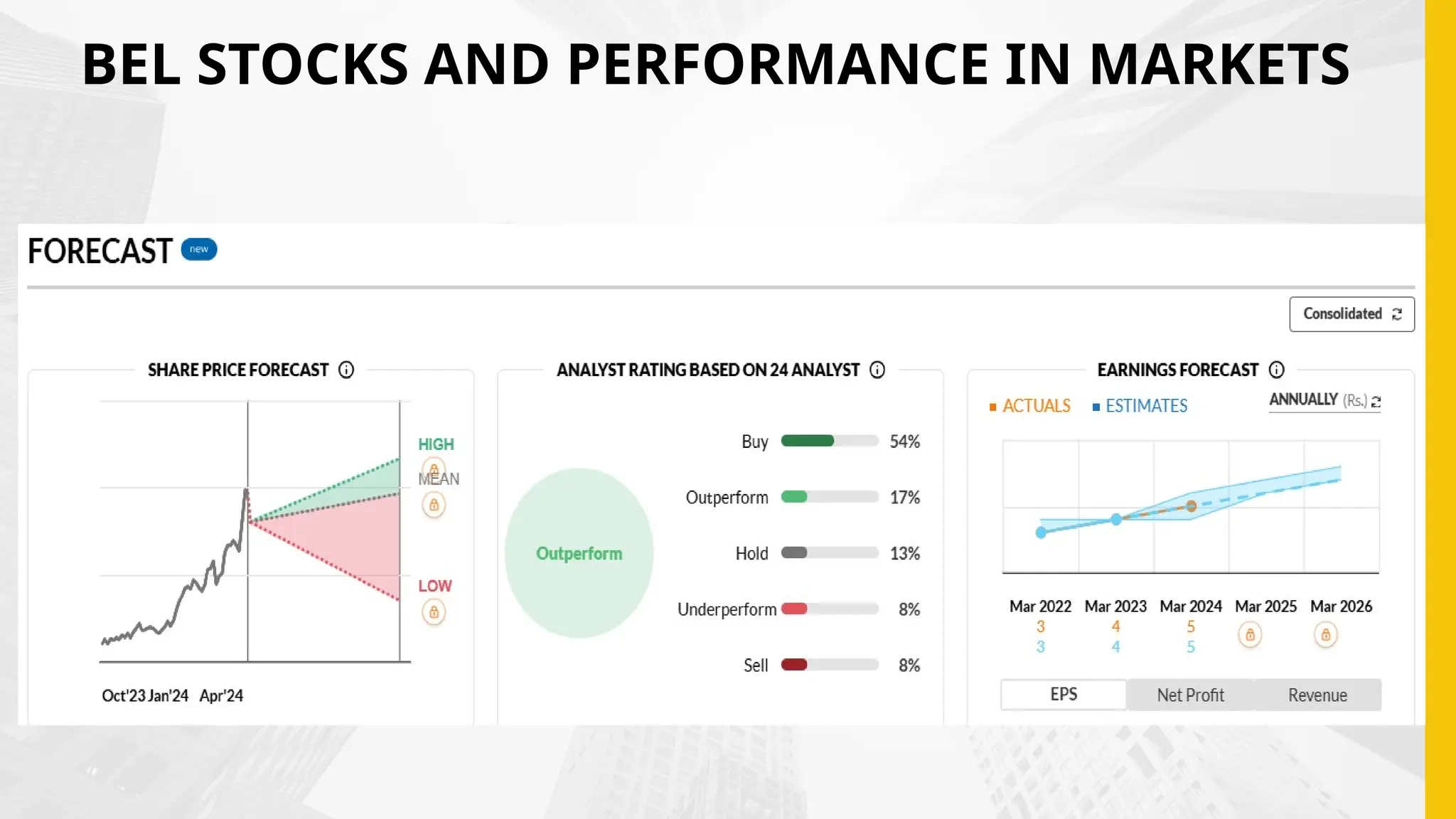

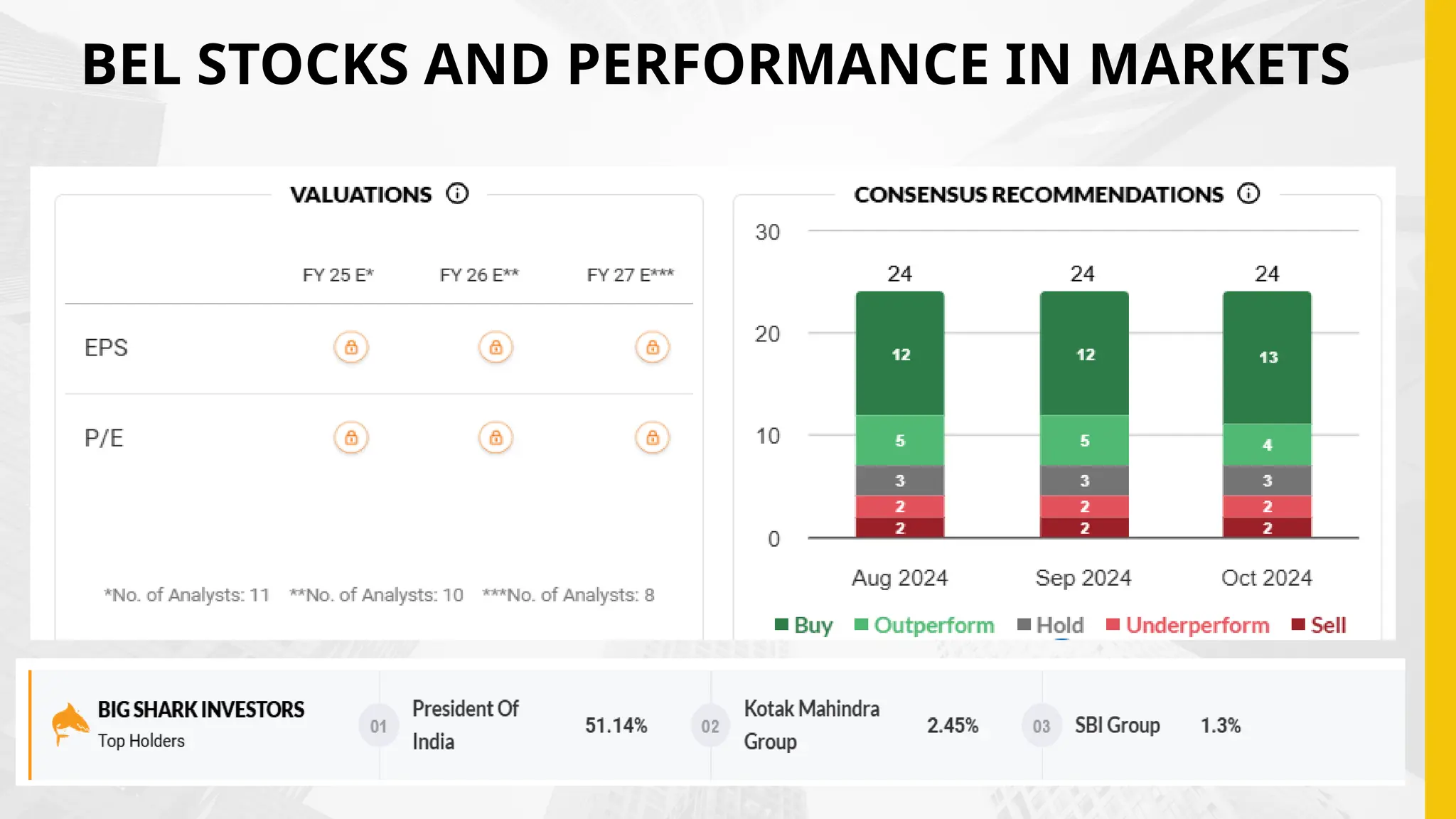

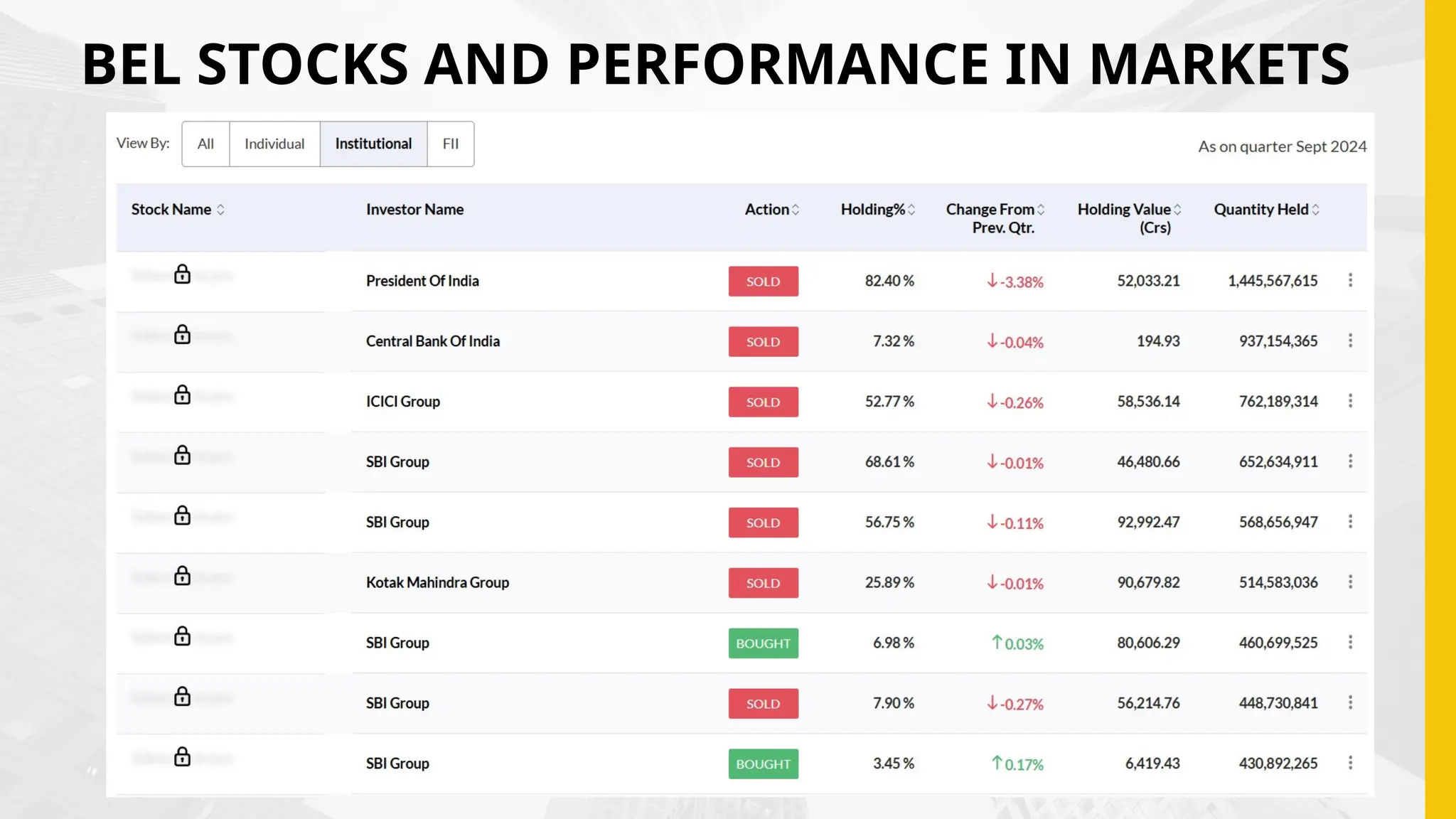

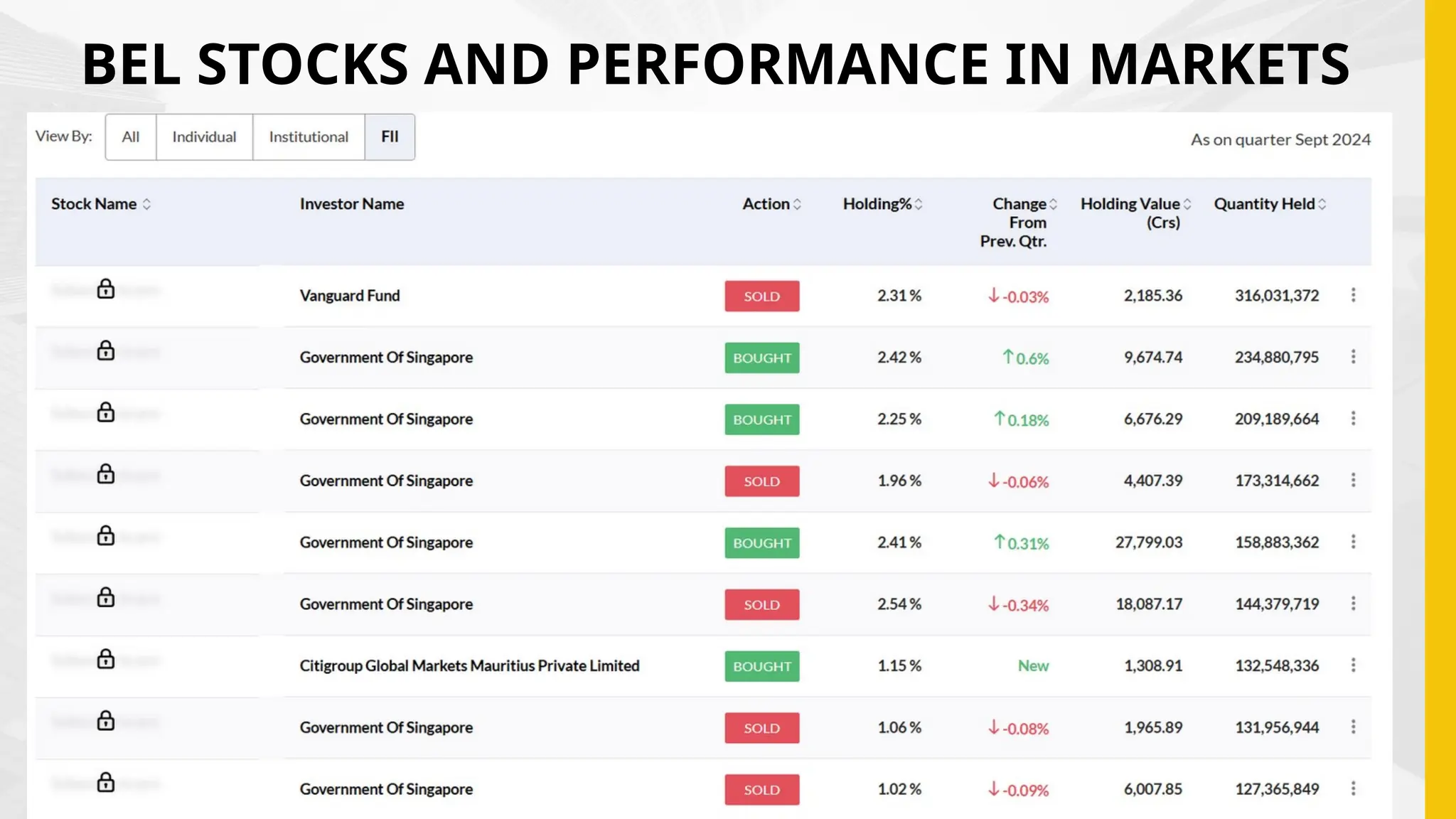

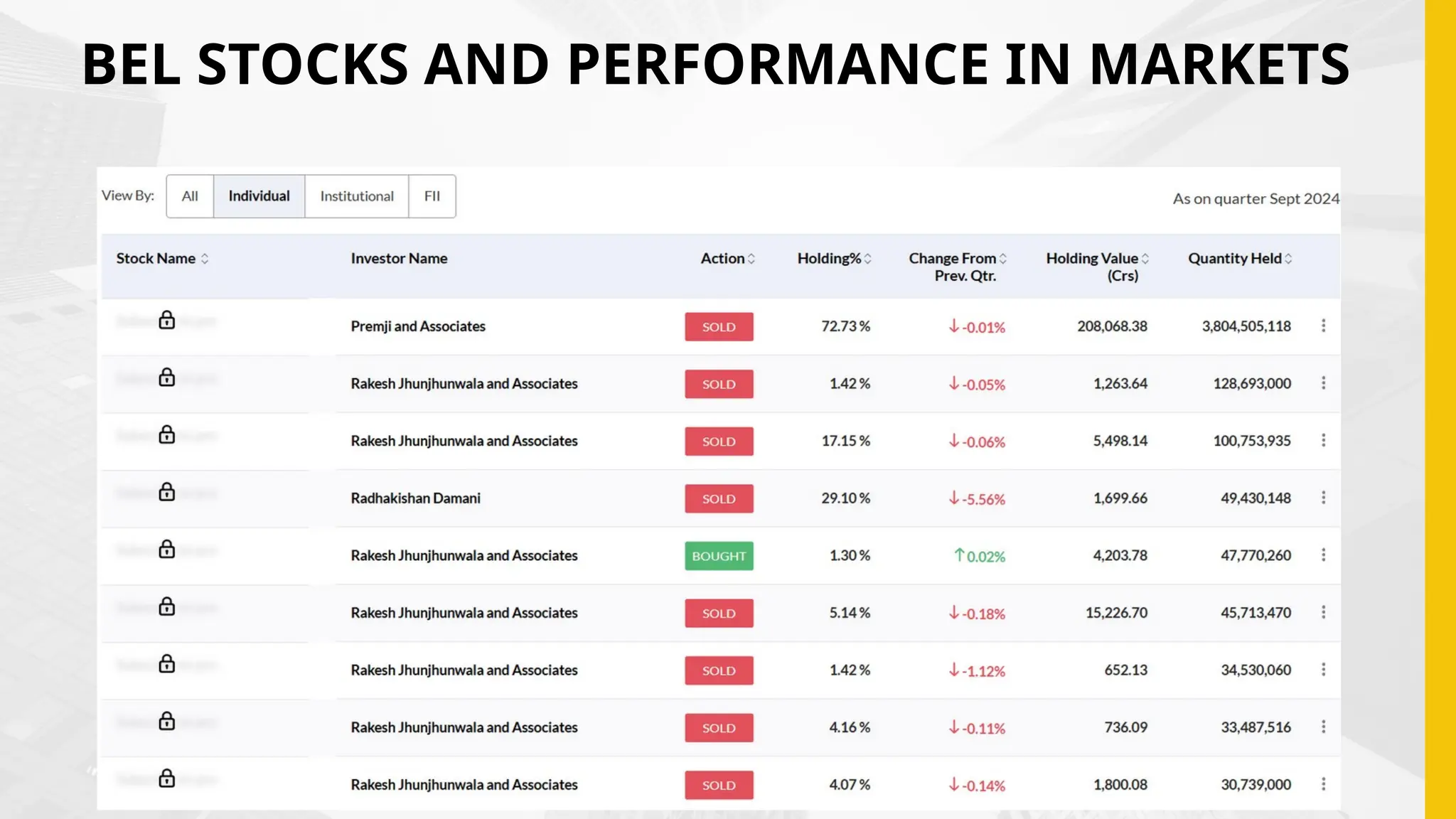

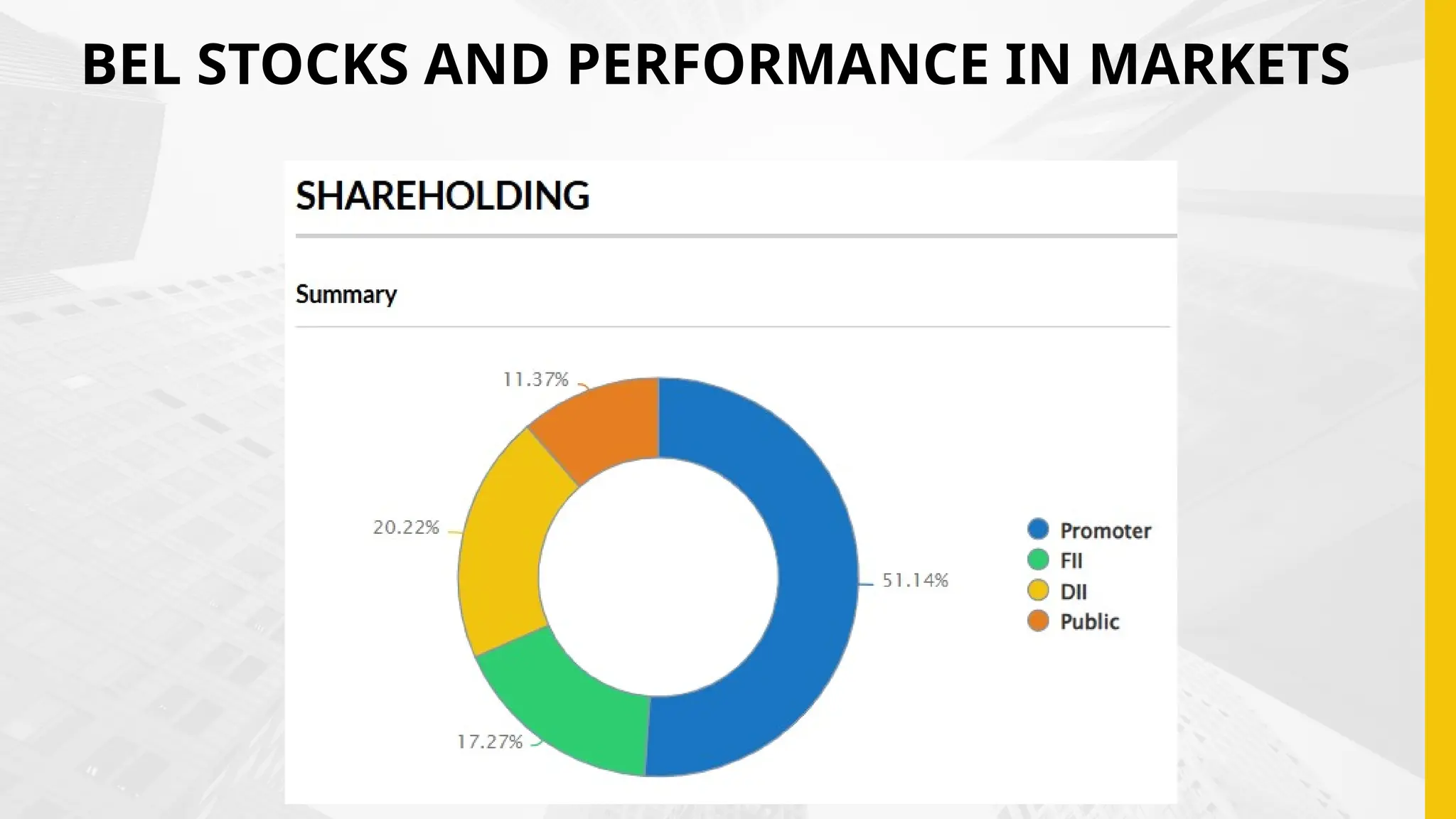

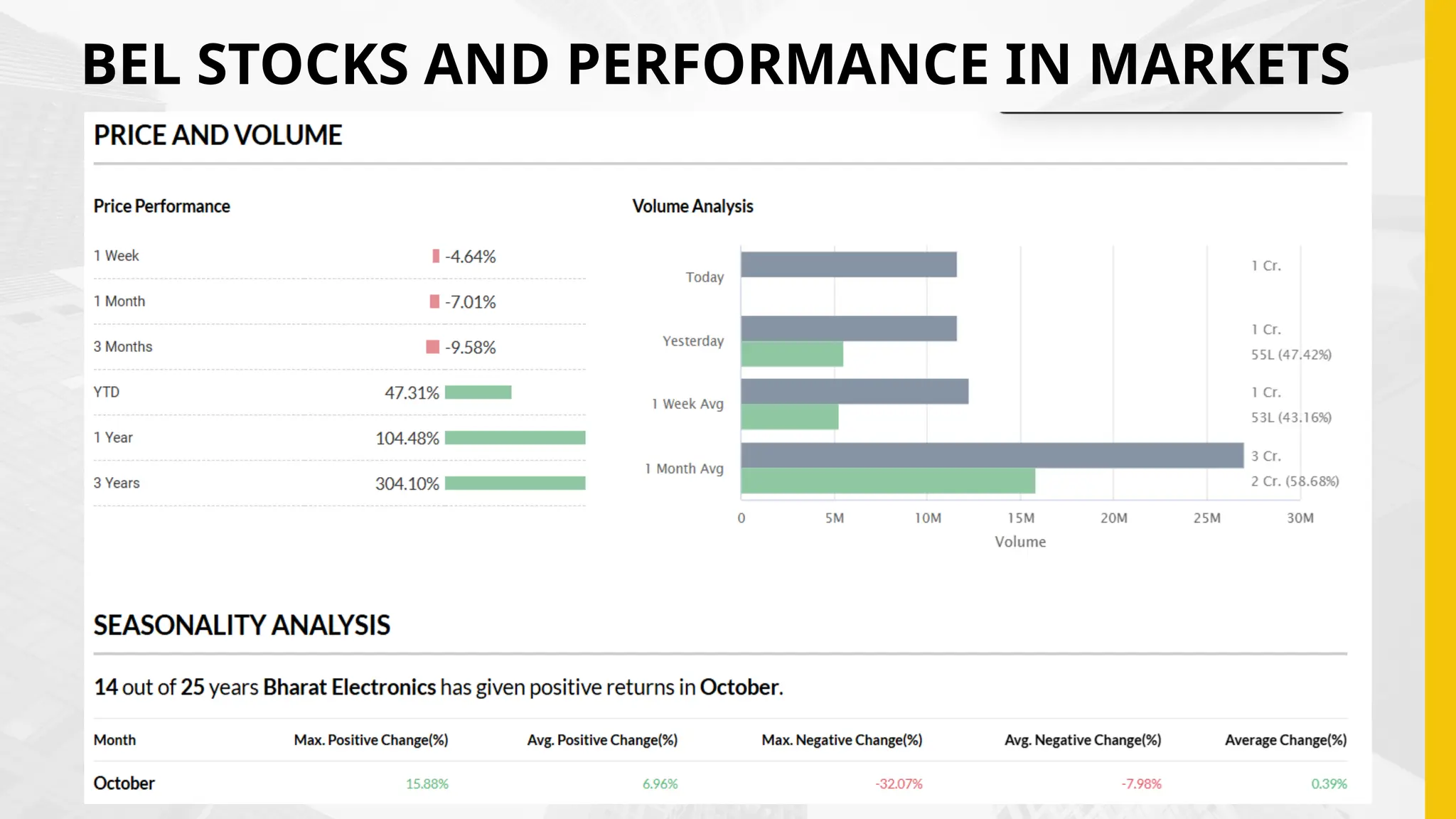

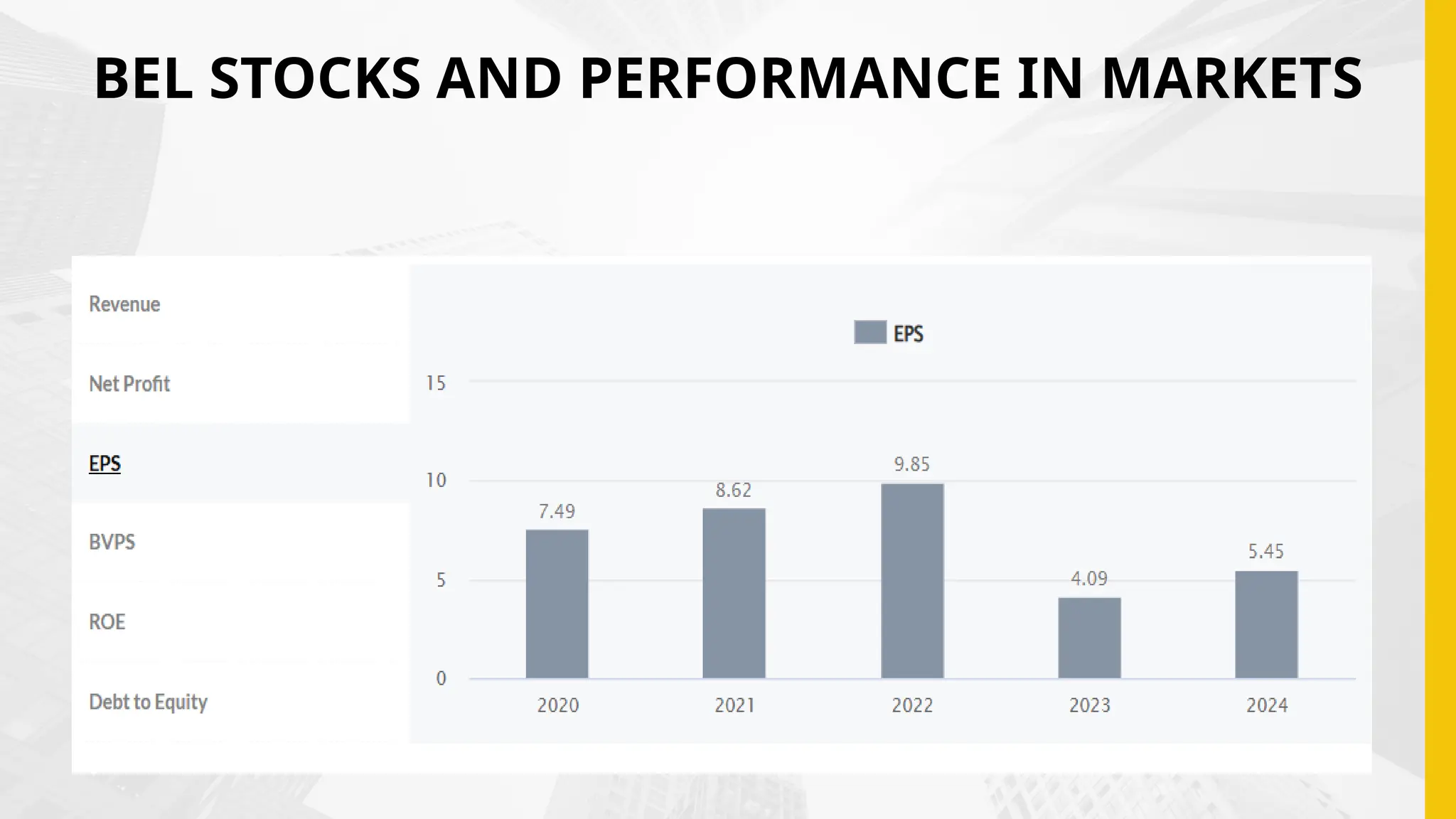

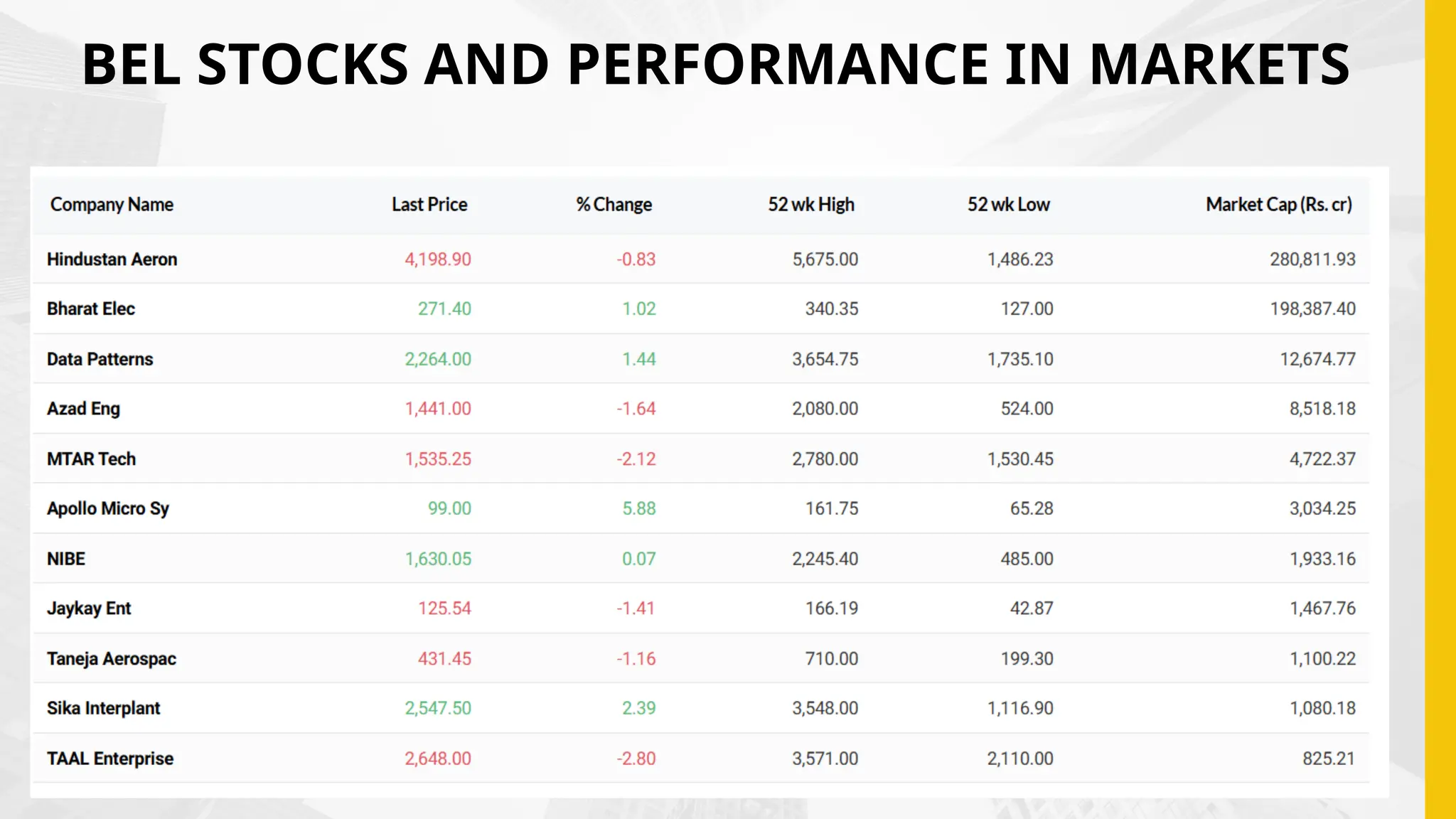

BHARAT ELECTRONICS LIMITED (BEL) IS A NAVRATNA PSU UNDER THE MINISTRY OF DEFENCE, GOVERNMENT OF INDIA. IT MANUFACTURES STATE-OF-THE-ART ELECTRONIC PRODUCTS AND SYSTEMS FOR THE ARMY, NAVY AND THE AIR FORCE. BEL HAS ALSO DIVERSIFIED INTO VARIOUS AREAS LIKE HOMELAND SECURITY SOLUTIONS, SMART CITIES, E-GOVERNANCE SOLUTIONS, SPACE ELECTRONICS INCLUDING SATELLITE INTEGRATION, ENERGY STORAGE PRODUCTS INCLUDING E-VEHICLE CHARGING STATIONS, SOLAR, NETWORK & CYBER SECURITY, RAILWAYS & METRO SOLUTIONS, AIRPORT SOLUTIONS, ELECTRONIC VOTING MACHINES, TELECOM PRODUCTS, PASSIVE NIGHT VISION DEVICES, MEDICAL ELECTRONICS, COMPOSITES AND SOFTWARE SOLUTIONS.

#48 P

In the next five years, India’s defense sector is likely to experience significant transformation and growth in the following ways:

1. : A substantial rise in locally manufactured defense equipment, driven by the "Make in India" initiative, reducing dependency on imports.

2. Greater integration of cutting-edge technologies such as AI, drones, and cybersecurity measures in military operations and defense systems.

3. Strengthened partnerships with global defense manufacturers and allies, resulting in joint ventures and technology transfers that enhance operational capabilities.

4. Streamlined logistics and supply chain management will lead to faster maintenance and deployment of defense assets.

5. Significant upgrades to air and naval capabilities, including new aircraft, submarines, and advanced weaponry, improving overall readiness and strategic deterrence.

F6Development of robust cyber defense mechanisms and space-based capabilities to secure communication and intelligence operations.

7. Enhanced training and skill development programs will create a more capable and technologically adept defense personnel pool.

Overall, India’s defense sector is poised for modernization, self-reliance, and increased operational effectiveness, positioning the country as a key player in regional and global defense dynamics.