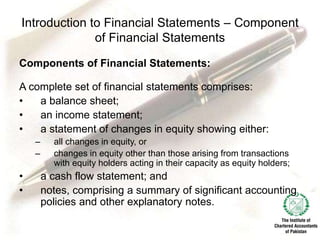

The document provides an introduction to financial statements, why they are audited, and basic accounting principles. It discusses that financial statements are a structured representation of a company's financial position and performance that provide useful information to decision makers. It also notes that audits are required by regulations to independently evaluate the fairness of financial statements. Finally, it outlines some key accounting principles like fair presentation, going concern assumption, and accrual basis of accounting.