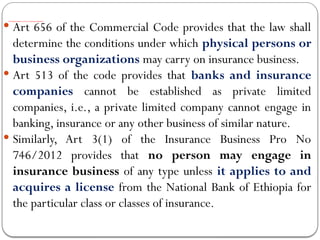

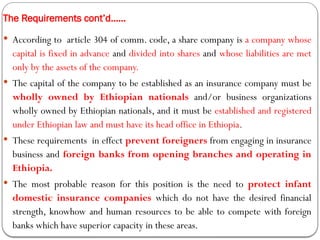

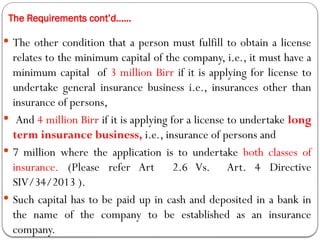

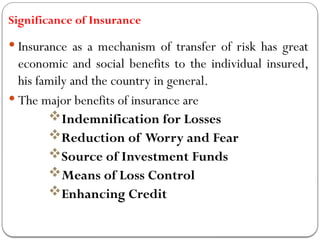

The document provides a comprehensive overview of the law of insurance, highlighting its definition, types, and importance within financial law. It discusses the development of insurance practices from ancient societies to modern systems, emphasizing the contractual nature of insurance agreements and the roles of the insurer and insured. Additionally, it details the evolution of the insurance industry in Ethiopia, outlining historical events that shaped its regulation and operation.