Download to read offline

![May 2015

36

The Founder/Pioneer Member of the International Federation of Forensic Accountants & Auditors (The IFFAA) Newsletter

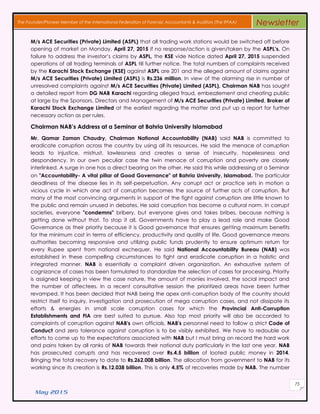

scrapped the project on April 18. The detailed judgement was issued on Wednesday following recent

directions from the Supreme Court of Pakistan. In the 110-page judgment, the bench headed by

Justice Mansoor Ali Shah observed that in proceeding with the project the LDA had caused

inconvenience to the residents of the city besides a loss of Rs.60 million to the public exchequer. “The

EPA failed to take action against the LDA and allowed construction work without the environmental

approval. We have been informed that Rs.60 million of taxpayers’ money has been spent on the

project so far,” it noted. The bench observed that local elections were scheduled in the province in

September 2015 and stated that until there was an elected government in the city the LDA should

restrict its activities to completion of projects launched before the election announcement. It also

expressed displeasure over the authority’s failure to submit in court a list of such projects. Besides, the

bench stated that the LDA could oversee day-to-day repair and maintenance work in areas that fall

under its jurisdiction. The bench struck down as unconstitutional initiation of the project by the LDA on

its own. It stated that work on the signal-free corridor was commenced in violation of Section 12 of the

Punjab Environment Protection Act and that any attempt to proceed with the project would be in

violation of Article 140 A of the Constitution (which requires elected authorities at the local level). It

observed that the LDA could propose establishment of the signal-free corridor at the site of the

elected local government. “It is up to the elected government to approve or disapprove the project,”

it said. The bench further stated that with the commencement of the project the LDA had

encroached upon the political, administrative and financial powers devolved on elected

governments under the Punjab Local Government Act. With the passage of the Punjab Local

Government Act, the LDA could no longer exercise powers vested in it under various sections (6, 13,

13A, 14, 15, 16, 18, 20, 23, 24, 28, 34A, 34B, 35, 38 and 46) of the Lahore Development Authority Act of

1975. It said such an attempt would be an encroachment on the jurisdiction of elected authorities.

The bench dismissed the prolonged absence of an elected government as a justification for

commencement of the project. It said the constitution had mandated the provincial government to

devolve powers to local governments. However, it said, the constitution or the PLGA had not specified

any timeline for the purpose. “The delay in announcement of local elections is a political affair and is

in violation of the law,” it ruled. “The failure to hold local elections is the sole responsibility of the

[provincial] executive. It has, thus far, failed to discharge this constitutional responsibility,” it said.

Assets reference: Zardari exempted from appearing in court

Former President Asif Ali Zardari appeared in an accountability court in Rawalpindi on Thursday. The

former president arrived in court today flanked by guards and amid tight security. Hearing the case,

Judge Khalid Ranjha gave Zardari complete exemption from appearing in court for future hearings of

the case. The hearing was subsequently adjourned until June 2, when the court has also summoned

the prosecution's witnesses to appear before the judge. This was the first time that the Pakistan

People’s Party (PPP) co-chairman appeared before the Rawalpindi accountability court judge since

the National Accountability Bureau (NAB) reopened the five-year-old reference in April. The PPP co-

chairman is accused of acquiring assets illegally and failing to submit correct details of his wealth. He

was previously excused from appearing in court due to ill health.

NAB committee gives recommendations on Haj

National Accountability Bureau (NAB) Chairman Qamar Zaman Chaurdry chaired a meeting in order

to review recommendations of Prevention Committee on Ministry of Religious Affairs here on Monday.

The representative of Ministry of Religious Affairs was also present in the meeting, says a press release.](https://image.slidesharecdn.com/d27bbfea-b9c1-49b3-a8f0-fc7a704ef557-160901155052/85/IFAP-Newsletter-May-2015-36-320.jpg)

This document summarizes the minutes from a meeting of the Institute of Forensic Accountants of Pakistan (IFAP). The meeting was held in Lahore and attended by IFAP members. Several members gave presentations on the role of forensic accountants and IFAP. They discussed how forensic accountants can help prevent fraud, uphold corporate governance and transparency. The members also discussed IFAP's syllabus and exemption policies for academic and professional qualifications. They agreed to keep the current syllabus and exemption policies in place for the next year.