Call Girls Jp Nagar Just Call 👗 7737669865 👗 Top Class Call Girl Service Bang...

ICCR taxes.state.mn.us

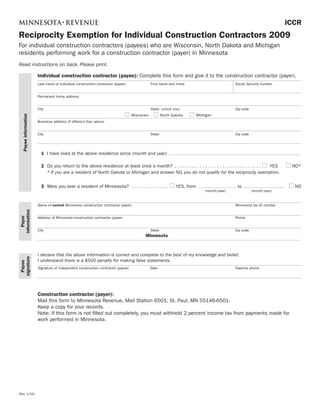

1. ICCR

Reciprocity Exemption for Individual Construction Contractors 2009

For individual construction contractors (payees) who are Wisconsin, North Dakota and Michigan

residents performing work for a construction contractor (payer) in Minnesota

Read instructions on back. Please print.

Individual construction contractor (payee): Complete this form and give it to the construction contractor (payer).

Last name of individual construction contractor (payee) First name and initial Social Security number

Permanent home address

City State (check one) Zip code

Wisconsin North Dakota Michigan

Payee information

Business address (if different than above)

City State Zip code

1 I have lived at the above residence since (month and year) .

2 Do you return to the above residence at least once a month? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . YES NO*

* If you are a resident of North Dakota or Michigan and answer NO, you do not qualify for the reciprocity exemption.

3 Were you ever a resident of Minnesota? . . . . . . . . . . . . . YES, from to . NO

(month/year) (month/year)

Name of current Minnesota construction contractor (payer) Minnesota tax ID number

information

Payer

Address of Minnesota construction contractor (payer) Phone

City State Zip code

Minnesota

I declare that the above information is correct and complete to the best of my knowledge and belief.

signature

I understand there is a $500 penalty for making false statements.

Payee

Signature of independent construction contractor (payee) Date Daytime phone

Construction contractor (payer):

Mail this form to Minnesota Revenue, Mail Station 6501, St. Paul, MN 55146-6501.

Keep a copy for your records.

Note: If this form is not filled out completely, you must withhold 2 percent income tax from payments made for

work performed in Minnesota.

(Rev. 1/09)

2. Instructions for Form ICCR

Individual construction Penalties

The law

If you knowingly make any statements on

contractors (payees) this form you know are incorrect, you may Beginning January 1, 2009, construction

be assessed a $500 penalty.

Qualifying information regarding contractors are required to deduct and

residency withhold 2 percent Minnesota income

Use of Information tax from payments made to individual

Minnesota has income tax reciprocity

All information on Form ICCR is private by construction contractors for work

agreements with Wisconsin, North Da-

state law. It may only be given to your state performed in Minnesota. Payments

kota and Michigan. If you are a resident of

of residence, the Internal Revenue Service are subject to 2 percent withholding if

one of these states, income from personal

and to other state tax agencies as provided the work was performed in Minnesota

services is exempt from Minnesota income

by law. The information may be compared and the total payments during the year

tax and payments for personal services

with other information you furnished to exceed $600. [M.S. 290.92, subd. 4a(3)]

you receive as an individual construction

the Department of Revenue. Your name,

contractor are not subject to the 2 percent

Definitions

address and Social Security number are

Minnesota withholding. (Note: If you are a

A construction contractor (payer) is

required for identification. Your address

resident of North Dakota or Michigan, you

any individual or business entity car-

is also required to verify your state of resi-

must return to your state of residence at

rying on a trade or business described

dence. The construction contractor’s name,

least once a month. Wisconsin residents are

in industry code numbers 23 through

Minnesota tax ID number, address and

not required to meet this requirement.)

238990 of the North American Industry

phone number are required in case we have

Classification System (NAICS). For a de-

to contact them regarding the tax withheld

Qualifying information regarding

scription of the NAICS industry codes,

from your pay. The only information not

personal service income and

go to www.census.gov/eos/www/naics/.

required is your phone number. However,

business income

we ask that you provide it so we can contact

Personal service income (payments for Examples of construction trades covered

you quickly if we have questions.

professional services personally provided by by this law include, but are not limited

you) qualifies for reciprocity. to, residential and commercial building

Construction contractors construction, residential remodeling,

Business income generated by your

(payers) framing and finish carpentry, masonry,

employees or resulting from the sale of

roofing and siding, electrical contract-

goods does not qualify for reciprocity if If you are making payment to an individual ing, plumbing and HVAC, drywall,

that income is more than incidental. The construction contractor (payee) who is a painting, and flooring.

services performed by employees or sales resident of a reciprocity state and they have

of goods are incidental if they are a minor An individual construction contractor

not given you a properly completed Form

contribution to the income of the business. (payee) is any individual carrying on a

ICCR, you must withhold 2 percent income

The salary you pay all employees, together trade or business as a sole proprietorship

tax from their pay for work performed in

with the gross profit from the sales of goods, described in industry code numbers 23

Minnesota.

is presumed incidental if it is less than the through 238990 of the NAICS. A single

In addition, individual construction con-

greater of either $20,000 or 10 percent of member Limited Liability Company

tractors (payees) are required to give you

the gross profit of the business. (LLC) is not a sole proprietorship for

a new Form ICCR each calendar year by purposes of this law.

If you qualify for reciprocity and February 28.

The term “carrying on a trade or

do not want Minnesota income Send the completed form within 30 days of business” generally includes any

tax withheld from your pay receipt to Minnesota Revenue, Mail Station

activity conducted for the produc-

To avoid having Minnesota income tax 6501, St. Paul, MN 55146-6501. You must

tion of income from selling goods or

withheld from your pay, you must complete keep a copy of all Forms ICCR for five

performing services. Carrying on a

Form ICCR and give it to the construction years from the date received. You may be

trade or business includes all business

contractor (payer) before they make pay- assessed a $50 penalty for each form you are

ment to you. You must provide a new form activities (primary, secondary, etc.).

required to send us but do not.

by February 28 of each calendar year you

work for the construction contractor and

Additional information

qualify for this reciprocity exemption. If you

do not complete this form and give it to the Additional forms and information, includ-

construction contractor, they are required ing fact sheets and frequently asked ques-

to withhold 2 percent of Minnesota income tions, are available on our website at www.

tax from payments made to you. taxes.state.mn.us.

Email: withholding.tax@state.mn.us

Fill out the form completely

If you do not complete every item on this Phone: 651-282 9999 or 1-800-657-3594.

form, the construction contractor (payer) is TTY: Call 711 for Minnesota Relay.

required to withhold 2 percent Minnesota

income tax from your pay.

![Instructions for Form ICCR

Individual construction Penalties

The law

If you knowingly make any statements on

contractors (payees) this form you know are incorrect, you may Beginning January 1, 2009, construction

be assessed a $500 penalty.

Qualifying information regarding contractors are required to deduct and

residency withhold 2 percent Minnesota income

Use of Information tax from payments made to individual

Minnesota has income tax reciprocity

All information on Form ICCR is private by construction contractors for work

agreements with Wisconsin, North Da-

state law. It may only be given to your state performed in Minnesota. Payments

kota and Michigan. If you are a resident of

of residence, the Internal Revenue Service are subject to 2 percent withholding if

one of these states, income from personal

and to other state tax agencies as provided the work was performed in Minnesota

services is exempt from Minnesota income

by law. The information may be compared and the total payments during the year

tax and payments for personal services

with other information you furnished to exceed $600. [M.S. 290.92, subd. 4a(3)]

you receive as an individual construction

the Department of Revenue. Your name,

contractor are not subject to the 2 percent

Definitions

address and Social Security number are

Minnesota withholding. (Note: If you are a

A construction contractor (payer) is

required for identification. Your address

resident of North Dakota or Michigan, you

any individual or business entity car-

is also required to verify your state of resi-

must return to your state of residence at

rying on a trade or business described

dence. The construction contractor’s name,

least once a month. Wisconsin residents are

in industry code numbers 23 through

Minnesota tax ID number, address and

not required to meet this requirement.)

238990 of the North American Industry

phone number are required in case we have

Classification System (NAICS). For a de-

to contact them regarding the tax withheld

Qualifying information regarding

scription of the NAICS industry codes,

from your pay. The only information not

personal service income and

go to www.census.gov/eos/www/naics/.

required is your phone number. However,

business income

we ask that you provide it so we can contact

Personal service income (payments for Examples of construction trades covered

you quickly if we have questions.

professional services personally provided by by this law include, but are not limited

you) qualifies for reciprocity. to, residential and commercial building

Construction contractors construction, residential remodeling,

Business income generated by your

(payers) framing and finish carpentry, masonry,

employees or resulting from the sale of

roofing and siding, electrical contract-

goods does not qualify for reciprocity if If you are making payment to an individual ing, plumbing and HVAC, drywall,

that income is more than incidental. The construction contractor (payee) who is a painting, and flooring.

services performed by employees or sales resident of a reciprocity state and they have

of goods are incidental if they are a minor An individual construction contractor

not given you a properly completed Form

contribution to the income of the business. (payee) is any individual carrying on a

ICCR, you must withhold 2 percent income

The salary you pay all employees, together trade or business as a sole proprietorship

tax from their pay for work performed in

with the gross profit from the sales of goods, described in industry code numbers 23

Minnesota.

is presumed incidental if it is less than the through 238990 of the NAICS. A single

In addition, individual construction con-

greater of either $20,000 or 10 percent of member Limited Liability Company

tractors (payees) are required to give you

the gross profit of the business. (LLC) is not a sole proprietorship for

a new Form ICCR each calendar year by purposes of this law.

If you qualify for reciprocity and February 28.

The term “carrying on a trade or

do not want Minnesota income Send the completed form within 30 days of business” generally includes any

tax withheld from your pay receipt to Minnesota Revenue, Mail Station

activity conducted for the produc-

To avoid having Minnesota income tax 6501, St. Paul, MN 55146-6501. You must

tion of income from selling goods or

withheld from your pay, you must complete keep a copy of all Forms ICCR for five

performing services. Carrying on a

Form ICCR and give it to the construction years from the date received. You may be

trade or business includes all business

contractor (payer) before they make pay- assessed a $50 penalty for each form you are

ment to you. You must provide a new form activities (primary, secondary, etc.).

required to send us but do not.

by February 28 of each calendar year you

work for the construction contractor and

Additional information

qualify for this reciprocity exemption. If you

do not complete this form and give it to the Additional forms and information, includ-

construction contractor, they are required ing fact sheets and frequently asked ques-

to withhold 2 percent of Minnesota income tions, are available on our website at www.

tax from payments made to you. taxes.state.mn.us.

Email: withholding.tax@state.mn.us

Fill out the form completely

If you do not complete every item on this Phone: 651-282 9999 or 1-800-657-3594.

form, the construction contractor (payer) is TTY: Call 711 for Minnesota Relay.

required to withhold 2 percent Minnesota

income tax from your pay.](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)