Downloaded 22 times

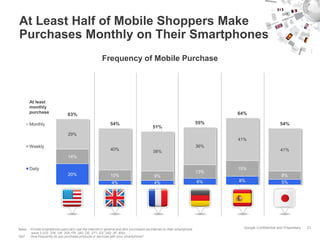

The document discusses global smartphone usage, finding that smartphone ownership and internet access via smartphones is rising worldwide. It also notes that smartphone users frequently look up local information and businesses near their location, with around 1 in 5 making a purchase after doing so. Finally, over half of mobile shoppers in most countries purchase something on their smartphone at least monthly.