Download to read offline

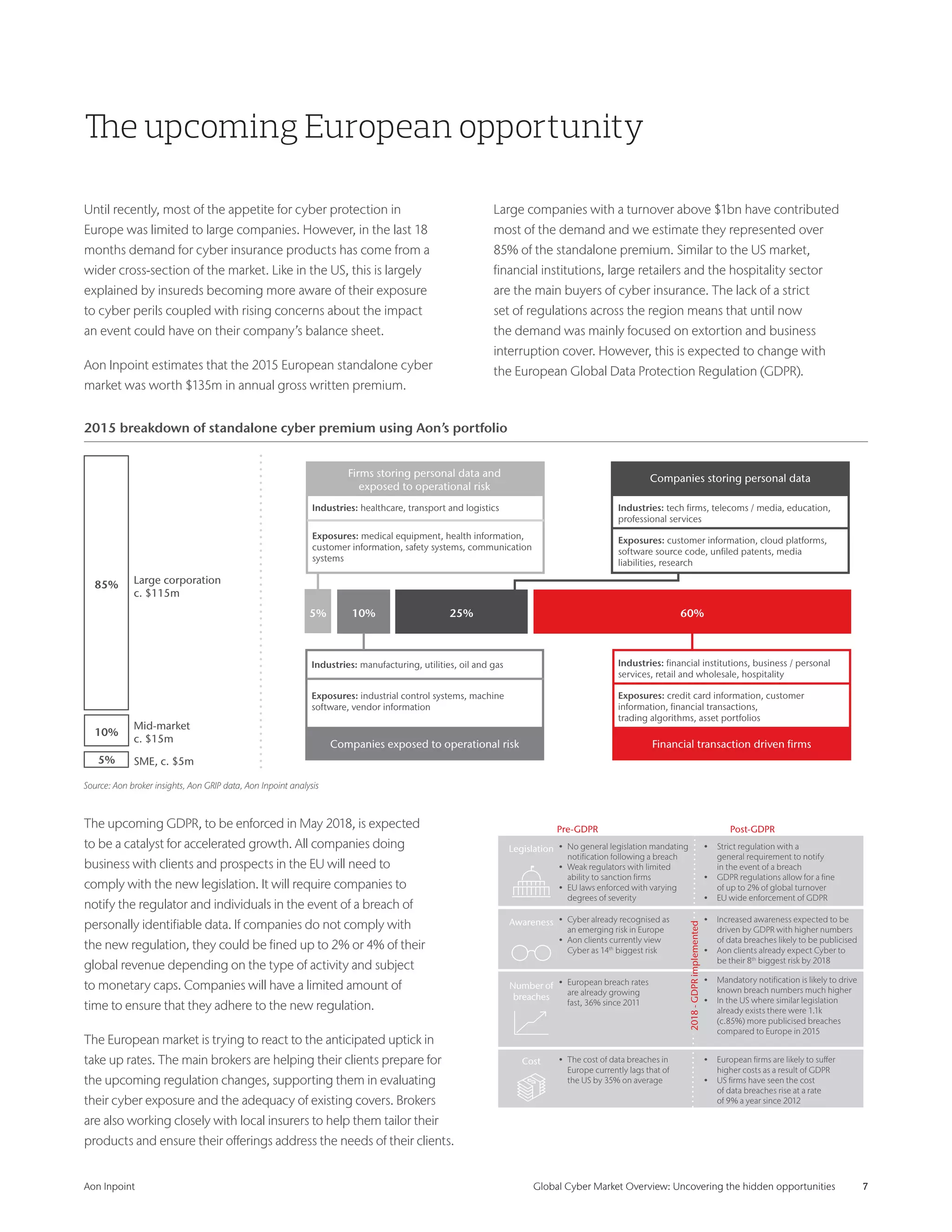

The document provides an overview of the global cyber insurance market, including: - The cyber insurance market is still in its infancy globally but has grown significantly in recent years, especially in the US where it is estimated to be worth $1.5 billion in 2015. - The largest market is the US, driven by data breach legislation, high-profile cyber attacks increasing awareness, and demand from companies storing personal data. - The upcoming European GDPR regulation coming into effect in 2018 is expected to be a major driver for the growing but still relatively nascent European cyber insurance market. - Various industries like retail, healthcare, and financial institutions are among the largest buyers of cyber insurance.

![Coded Agents – with UiPath SDK + LangGraph [Virtual Hands-on Workshop]](https://cdn.slidesharecdn.com/ss_thumbnails/codedagentsdeck-251215155422-5497c599-thumbnail.jpg?width=640&height=640&fit=bounds)