Downloaded 14 times

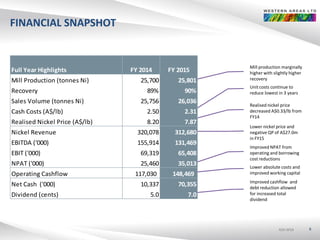

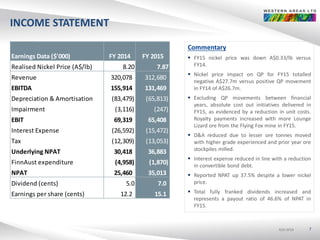

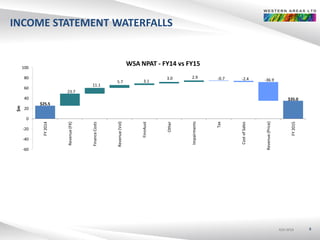

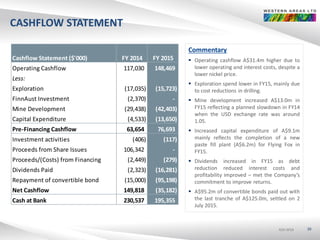

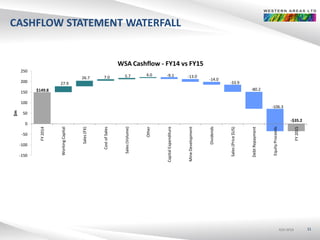

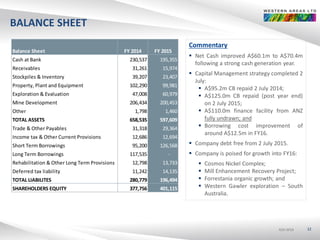

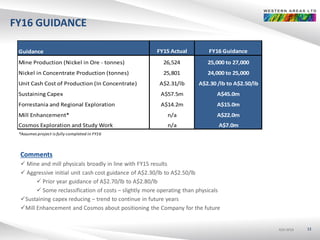

Western Areas Ltd presented its full year results for the period ending 30 June 2015. Key highlights included record low lost time injury frequency rate, nickel production of 26,524 tonnes at an average grade of 4.9% and cash costs of $2.31/lb. Net profit after tax was $35 million, up from $25.4 million in the previous year due to lower costs despite a $0.33/lb lower nickel price. Operating cashflow increased 27% to $148.5 million while net cash position improved to $70.4 million.