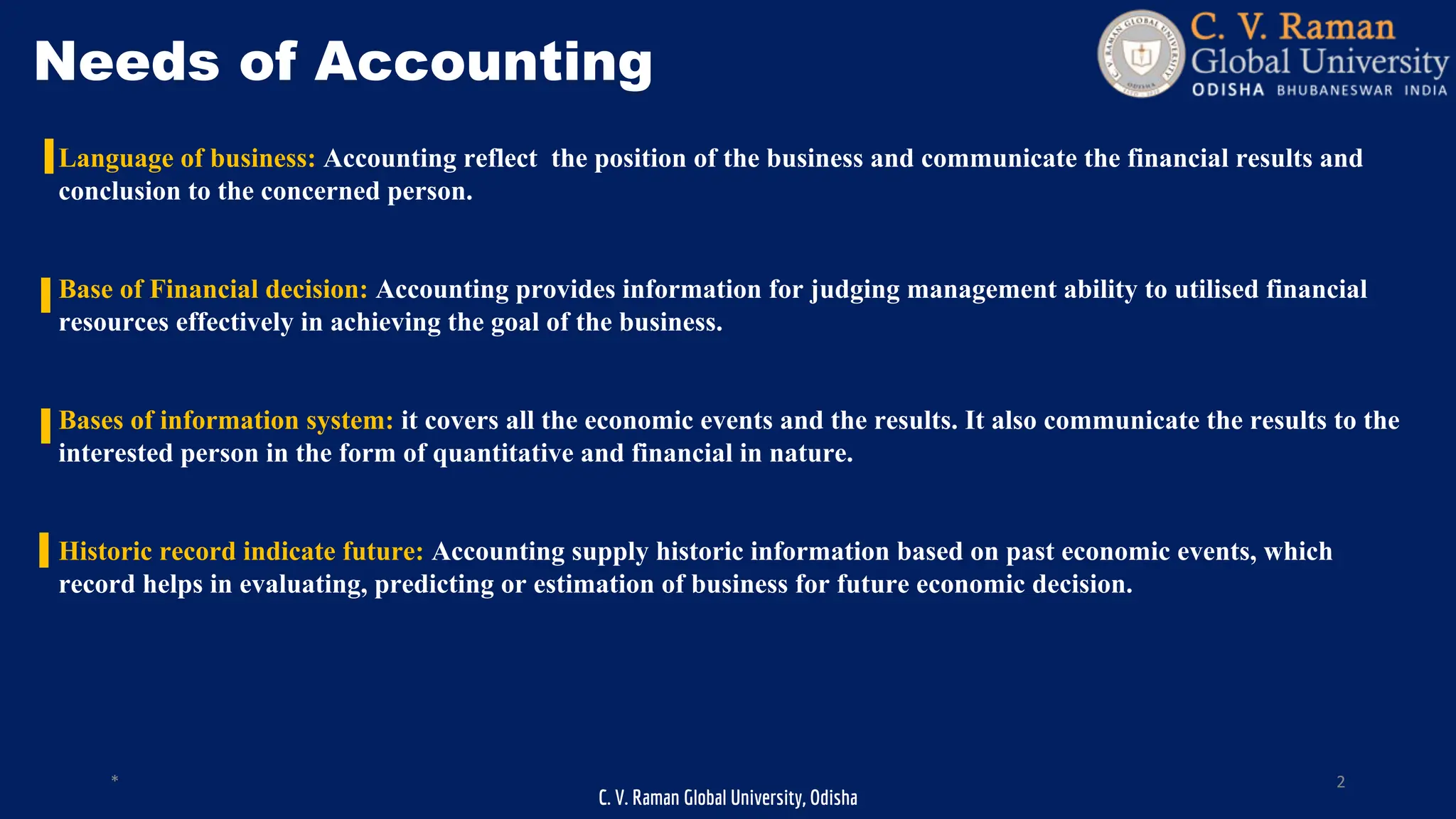

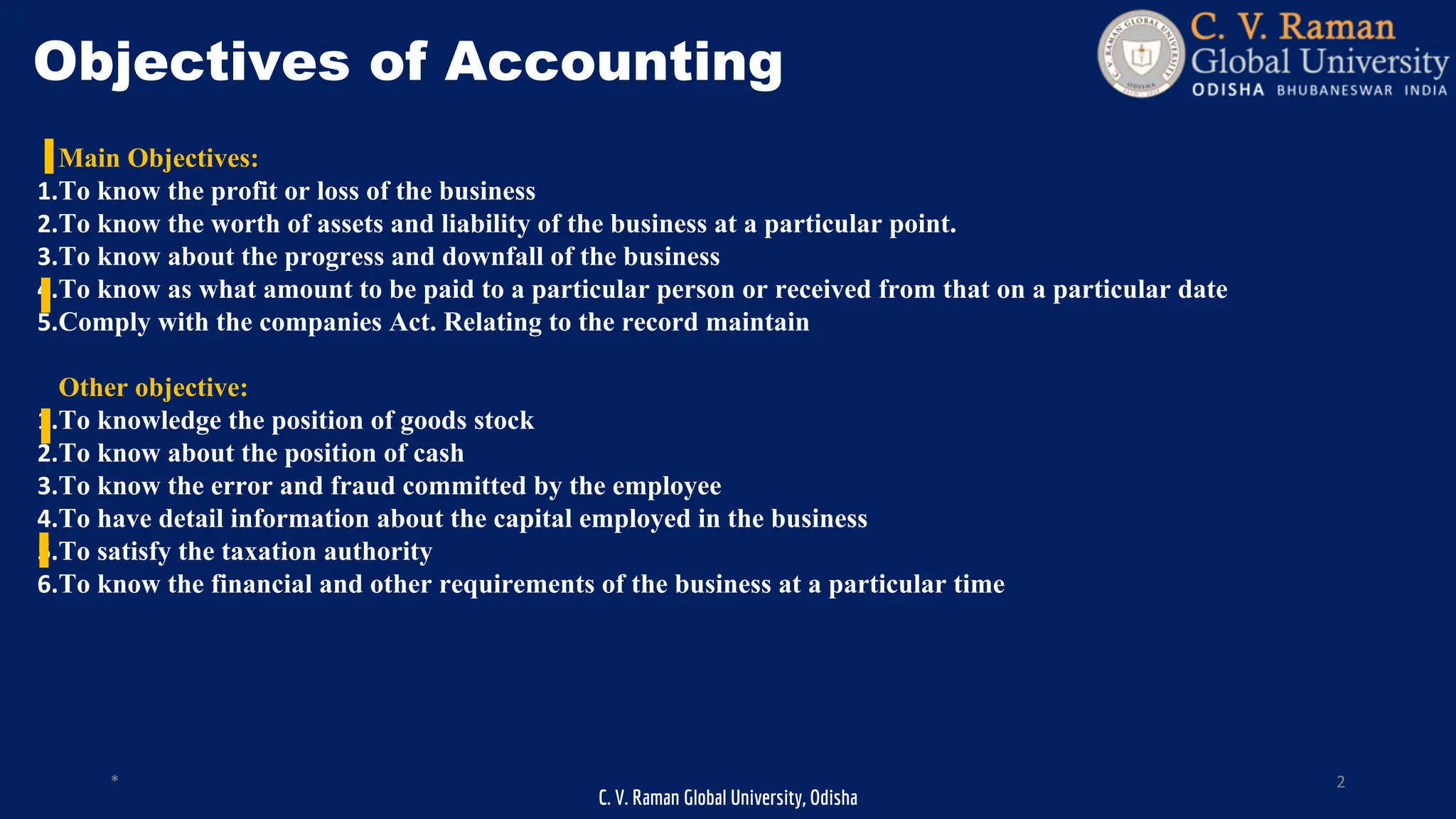

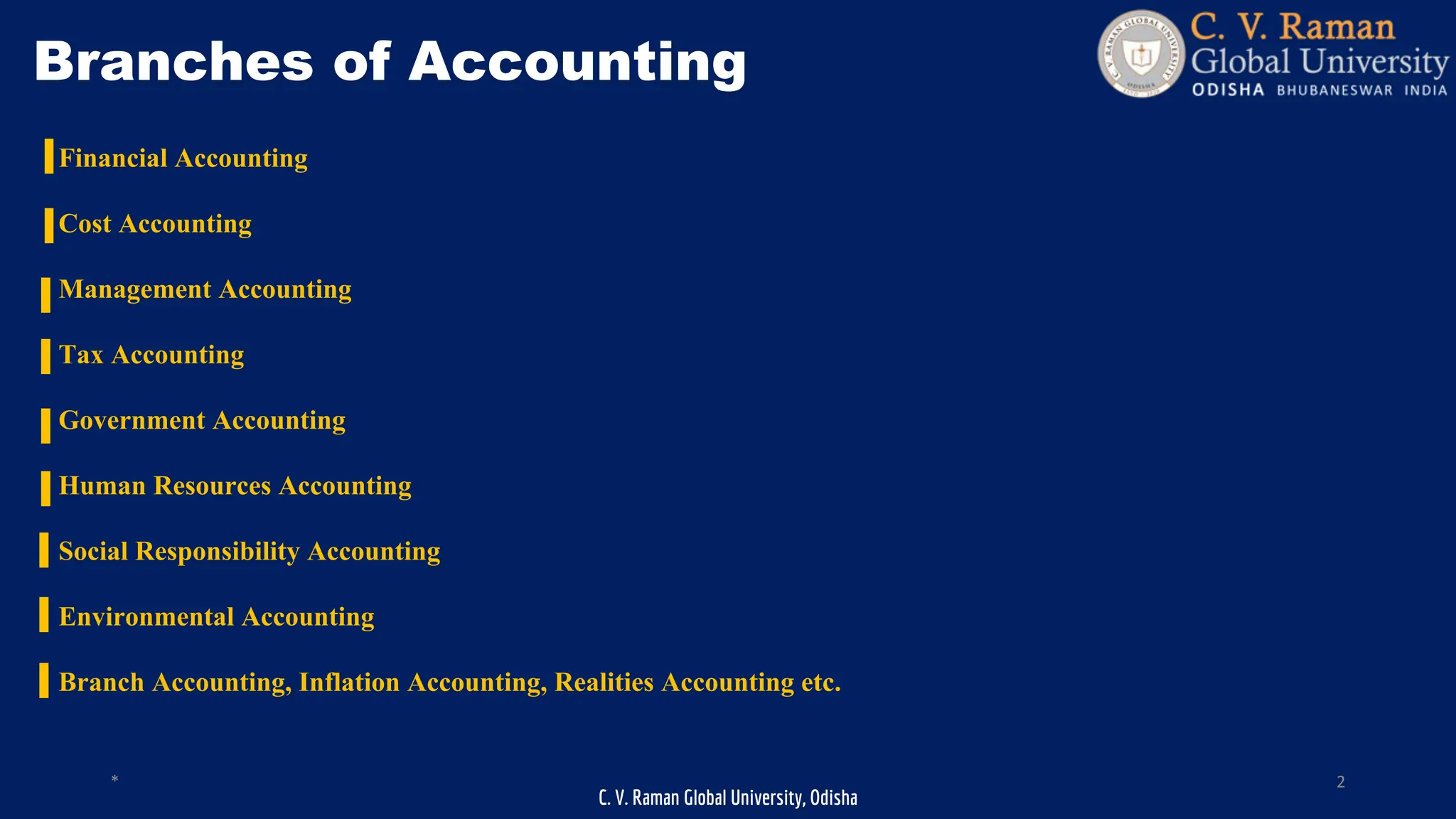

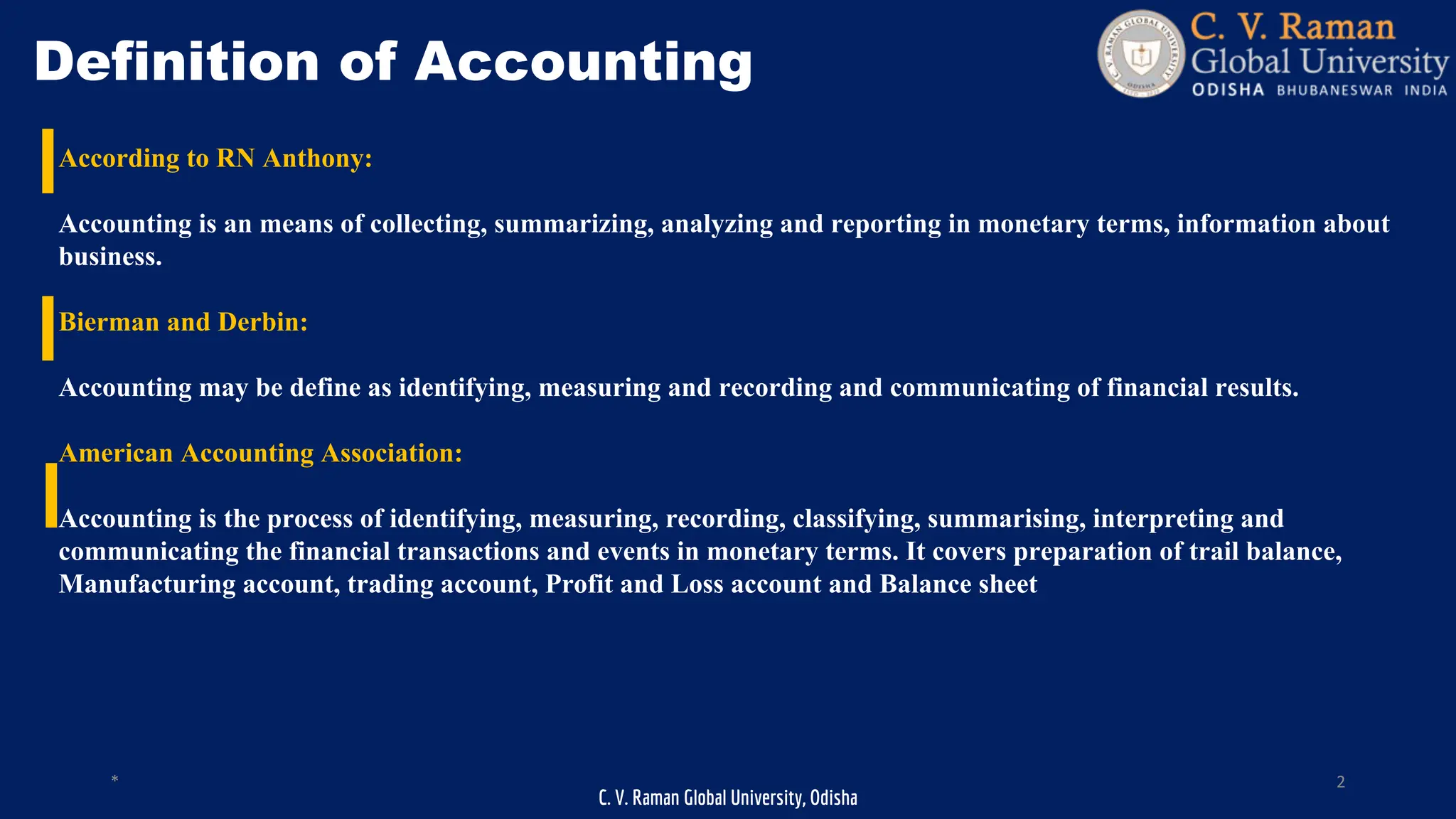

This document provides an introduction to accounting. It defines accounting according to several sources and outlines its key characteristics such as recording economic activities monetarily and presenting information in a summarized format. The document also discusses the nature and scope of accounting, including preparing financial statements from bookkeeping entries. It notes the needs and objectives of accounting such as providing a language for business and a basis for financial decision making. Finally, it lists some of the main branches of accounting such as financial, cost, management, and tax accounting.

![C. V. Raman Global University, Odisha

* 2

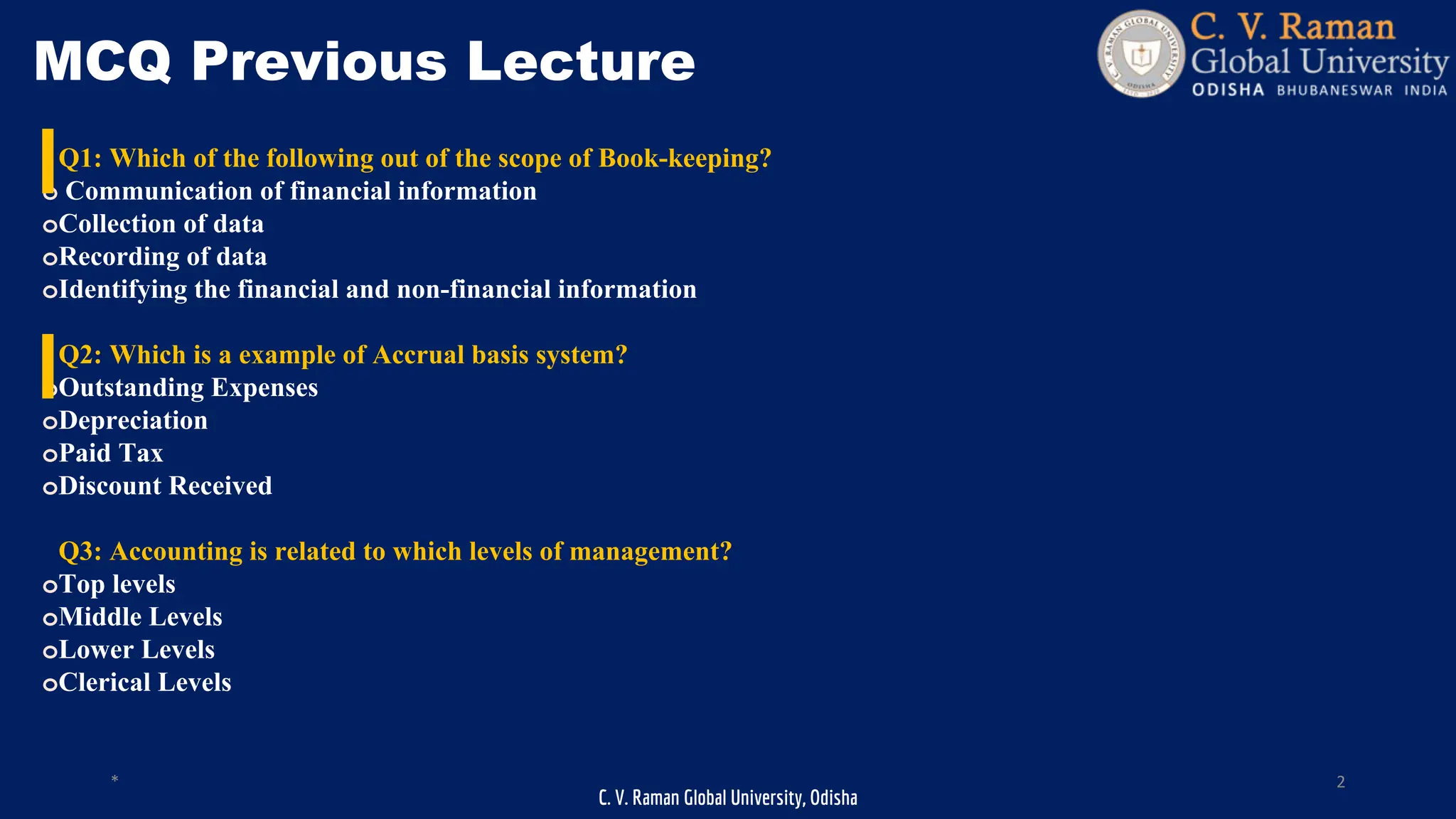

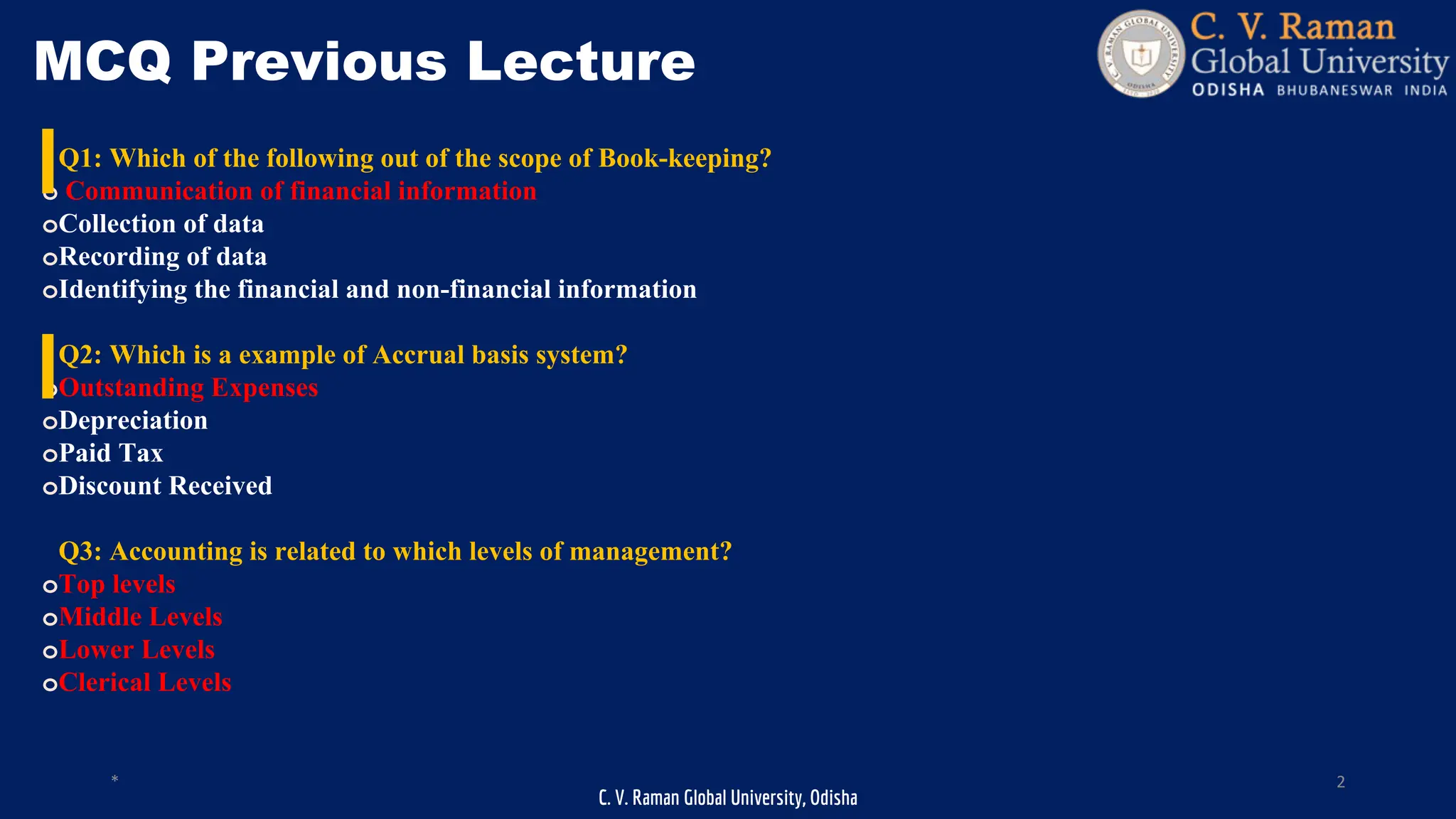

Scope of Accounting

To test and verify the entries in Book-keeping

To test the total and balance of ledger

To prepare Trail Balance from Ledger

To disclose adjustments

To Prepare the Final Account [Trading, P&L, BS]

To rectify error

To find out conclusion on the basis of analysis of financial statements](https://image.slidesharecdn.com/unit1accounts3p-240408085203-a944ecf4/75/Fundamentals-of-Financial-Accounting-PPT-7-2048.jpg)