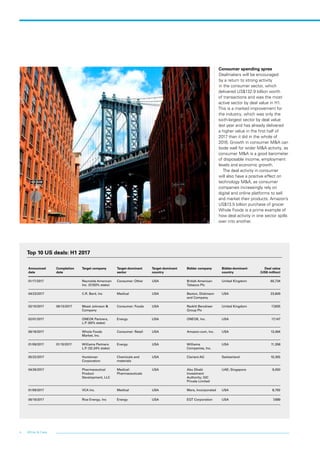

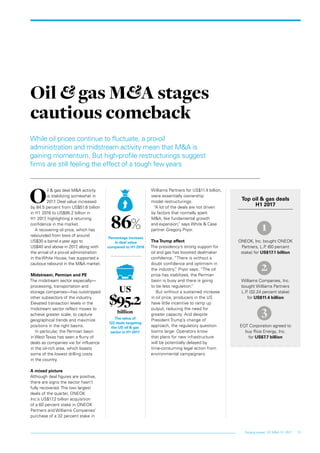

Download to read offline

In the first half of 2017, U.S. M&A activity remained strong with 2,413 deals totaling $588.5 billion, a slight increase in value from the previous year despite a drop in volume. The consumer sector led the market, driven by technology disruptions and steady economic fundamentals, although concerns remain due to incoming regulations and geopolitical tensions, especially regarding Chinese investments. The success of M&A in the U.S. will largely depend on how President Trump's proposed tax reforms and other policies are implemented, amid uncertainties surrounding their effectiveness.