Download to read offline

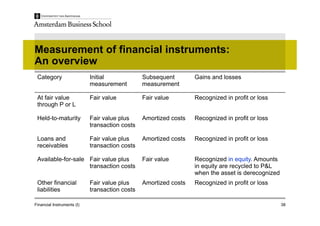

This document outlines the initial and subsequent measurement and treatment of gains and losses for five categories of financial instruments: instruments at fair value through profit or loss are measured at fair value both initially and subsequently with changes recognized in profit or loss; held-to-maturity and loans and receivables instruments are measured at amortized cost using the effective interest method with gains and losses recognized in profit or loss; available-for-sale instruments are measured at fair value with changes recognized in other comprehensive income and recycled to profit or loss on derecognition; other financial liabilities are also measured at amortized cost using the effective interest method with gains and losses recognized in profit or loss.

![What Is Blockchain Technology A Simple Beginner’s Guide [2026]](https://cdn.slidesharecdn.com/ss_thumbnails/whatisblockchaintechnologyasimplebeginnersguide2026-260101112141-cf432b44-thumbnail.jpg?width=640&height=640&fit=bounds)