An actionable definition of systemic risk in financial services validated using data from the Icelandic financial system failure

•

1 like•1,439 views

Illin T, Varga L (2014) An actionable definition of systemic risk in financial services validated using data from the Icelandic financial system failure.

Recommended

Recommended

More Related Content

Viewers also liked

Viewers also liked (11)

More from Cranfield University

More from Cranfield University (20)

Recently uploaded

Recently uploaded (20)

An actionable definition of systemic risk in financial services validated using data from the Icelandic financial system failure

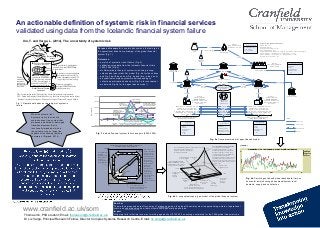

- 1. Ilin, T. and Varga, L. (2014), The uncertainty of systemic risk Thomas Ilin, PhD student, Email: thomas.ilin@cranfield.ac.uk, Dr Liz Varga, Principal Research Fellow, Director Complex Systems Research Centre, Email: liz.varga@cranfield.ac.uk www.cranfield.ac.uk/som An actionable definition of systemic risk in financial services validated using data from the Icelandic financial system failure $ PARTICIPANT (regulated) $ PARTICIPANT (unregulated) $ CENTRAL AUTHORITY FINANCIAL SERVICE PRODUCTS LOAN DEPOSIT DEBT SETTLEMENT SECURITY FUND $$ SOVEREIGN GDP % Treasury Budget LENDING (LL) / BORROWING (LB) TAKING (DT) / PLACING (DP) ISSUING (DI) / HOLDING (DH) RETIRING (DR) / DISCHARGING (DD) TENDERING (ST) / ACQUIRING (SA) RECEIVING (FR) Activities Regulated Participant Data Profit Assets Liquid-Assets Liabilities Fines … etc LENDING (LL) / BORROWING (LB) TAKING (DT) / PLACING (DP) ISSUING (DI) / HOLDING (DH) RETIRING (DR) / DISCHARGING (DD) TENDERING (ST) / ACQUIRING (SA) RECEIVING (FR) Activities Unregulated Participant Data Profit Assets Liquid-Assets Liabilities … etc PROVIDING (FP) Activities LL / LB, DT / DP Fine Policy % of Assets Central Authority Data Fine Rate Ratios Interest Rates Liquid-Assets … etc FP / FR FP / FR RATING AGENCY Strategy: MAX-REGULATION MIN-REGULATION Strategy: GROW-PROFITS GROW-ASSETS REDUCE-LIABILITIES MAINTAIN-LIQUIDITY BALANCE Strategy: GROW-PROFITS GROW-ASSETS REDUCE-LIABILITIES MAINTAIN-LIQUIDITY BALANCE Fine Policy Strategy: PROVIDE-LIQUIDITY DO-NOTHING Product Data Function Holdings Total Bids Open Total Offers Open Total … etc Fine SIMULATION MODEL CONTENTS: COUNTRY (x1) SOVEREIGN (x1) CENTRAL AUTHORITY (x1) RATING AGENCY (x1) FOREIGN PARTICIPANT (x1, sized as a multiple of native participants) PARTICIPANT - regulated (x1 < configurable <= x100) PARTICIPANT - unregulated (x1 < configurable <= x100) SIFS (2 per 6 functions = 12) % GDP Sovereign Data Treasury Budget Fine Policy Country-GDP .. etc $ FOREIGN PARTICIPANT Acquisition DI / DH DR / DD ST / SA INTERNATIONAL MARKET DI / DH DR / DD ST / SA KEY: Reference Value flow Participation Detail $ FOREIGN PARTICIPANT Acquisition Regulatory Budget Financial service activity-types (SIFS Supply / Demand) Financial service activity-types (SIFS Supply / Demand) Macroeconomic events Distress is created by exogenous causes, and operationalized in the system. Systemic behaviour is manifested as external effects, sometimes causing further distress. SIPs – Systemically important Participants (e.g. banks, intermediaries, counterparties). SIFS – Systemically important Financial Services (e.g. short-term funding from money-markets). * Behaviour can also be: Contagious, Dispersive, Convergent, Expansive, Divergent, Optimal. Global Financial System operations In response to increasing distress, local operational efforts of SIPs become focused on certain SIFS (e.g. getting short-term funding).A B effects causes F Distress is propagated system-wide as problems in the execution-level activities of SIPs in overall supply vs demand for certain SIFS. (e.g. lack of short-term funding). Failed* D E Which becomes emergent operational behaviour. C Distress is increased by endogenous causes within the system’s operations. stability instability effects of instability Purpose of research: to explain phenomena that emerge in the operational behaviour paradigm of the global financial system (Fig 1). Outcomes: • a metric of systemic risk of failure (Fig. 2) • validation using data from the Icelandic financial crisis 2000-2009 (Fig. 3) • multidisciplinary theory of systemic risk using a cusp- catastrophe type (static 3d) model (Fig. 4a for the surface and Fig. 4b with base from Fig. 4a and time in the z axis) • a dynamical complex system model responding to collective participation behaviour (Fig. 5a for conceptual model and Fig. 5b for the agent based model ) Fig. 1 Operational behaviour paradigm of systemic failure Source: Extracted from the reported accounts of all 51 financial institutions in the Iceland database of Bankscope. 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 tot_profit_act 1,656,700 4,312,100 8,403,100 2,276,100 6,020,600 3,549,845,139 239,599,662 206,412,248 -1,953,841,290 -607,881,900 tot_assets_act 451,393,500 924,935,100 981,676,800 565,522,000 2,939,201,500 15,999,713,336 7,811,197,543 10,435,219,325 4,996,139,748 3,887,703,500 tot_liabilities_act 468,318,500 939,790,100 995,786,700 570,690,500 3,044,863,900 16,654,898,860 8,383,680,300 11,465,867,885 5,574,049,530 4,318,728,400 tot_liquid_act 231,931,800 330,242,100 363,716,300 103,713,500 691,861,200 1,525,669,113 2,581,366,364 4,860,068,189 2,374,534,591 1,734,561,200 tot_securities_act 53,084,900 74,062,800 67,007,000 17,630,800 407,113,000 12,681,175,749 1,712,223,256 2,715,050,572 1,093,228,923 774,386,700 tot_debt_act 202,975,600 557,257,400 572,129,000 437,710,500 1,951,623,900 7,215,230,684 4,429,202,641 4,835,106,317 3,480,337,873 3,811,485,100 tot_loans_act 0 0 0 0 250,700,200 354,177,740 934,168,278 999,915,622 332,978,327 323,283,500 tot_deposits_act 92,725,900 138,312,400 136,906,900 5,807,700 136,177,400 342,577,782 511,286,489 1,081,272,784 688,948,932 362,818,900 -5,000,000,000 0 5,000,000,000 10,000,000,000 15,000,000,000 20,000,000,000 ISKthousands National Systemic Failure Summary - Iceland Actual Financials (total levels among all operational participants in each year) Foreign acquisitions. High ratio and level of assets in traded international securities. Relief Euphoria Frustration Euphoria Relief Prolific new issuance of long- term debt securities on foreign markets. Banking system collapsed. State restructured remaining banks and allowed them to default on their external debt. Liberalisation of the Icelandic financial sector and privatisation of domestic banks completed. Negative reports by rating agencies limited access to international securities markets. Fear Datapoints: Sentiment: 1 2 3 4 5 6 Fig. 3 Iceland financial system failure analysis (2000-2009) What is systemic risk? Systemic risk is the risk of a systemic event in a system that produces an altered or damaged transitional system that is functionally impeded, which in the extreme may no longer be capable of functioning (authors’ summary of Zigrand, 2014). Fig. 4b A cusp catastrophe-type model of the global financial system Fig. 5a Conceptual model of agent-based model So what The method proposed here offers a way of diagnosing when the global financial system is approaching a state of operational crisis, and understanding how that outcome could generally be avoided. Impact Mitigating falls in lifetime income of working age adults of $150,000 on average estimated for the 2008 global financial crisis Potentially Catastrophic Systemic Fidelity Systemic Failure set Divergent Contagious Optimal Contagious Dispersive Dispersive DivergentOptimal 0% When shifts in the system’s operational state over time are projected from the three-dimensional surface of behaviour Bt onto this two- dimension control surface of focus F, and then are described by extensions to the concepts of divergence and hysteresis from catastrophe theory, they provide a categorisation of operational behaviour. Hysteresis y 100% % of systemically important financial services (SIFS) that are the focus of concentrations in supply intentions x 100% % of systemically important financial services (SIFS) that are the focus of concentrations in demand intentions ( )fail F ( )F The two-dimensional control surface F of overall focus on intended supply relative to demand Fig. 5b Part of agent-based model dashboard (time on horizontal axis) showing phenomena/system level demand, supply and satisfaction 100% 0% y x 100% z The two-dimensional control surface Ft of overall operational focus on intended supply relative to demand The three-dimensional surface Bt of all previous and predicted operational states at time t. This surface represents the operational behaviour topology, in which each coordinate point (x, y, z) =bt∈Bt is a potential overall operational effectiveness at time t. Then a current operational state at t is defined by a single point on this surface and a state category derived from its placement in a region of Bt. Bifurcation set (shadow of the fold on the control surface), which is also a catastrophic contagion set Systemic Failure set Singularity Cusp (can fold either way) Progressive contagion set for y (supply) Cross-sectional cut in surface Bt Catastrophic failure of the system Systemic risk mitigation effect Progressive contagion set for x (demand) 100% % of all available systemically important financial services that achieve a minimum level of overall supply satisfaction of demand