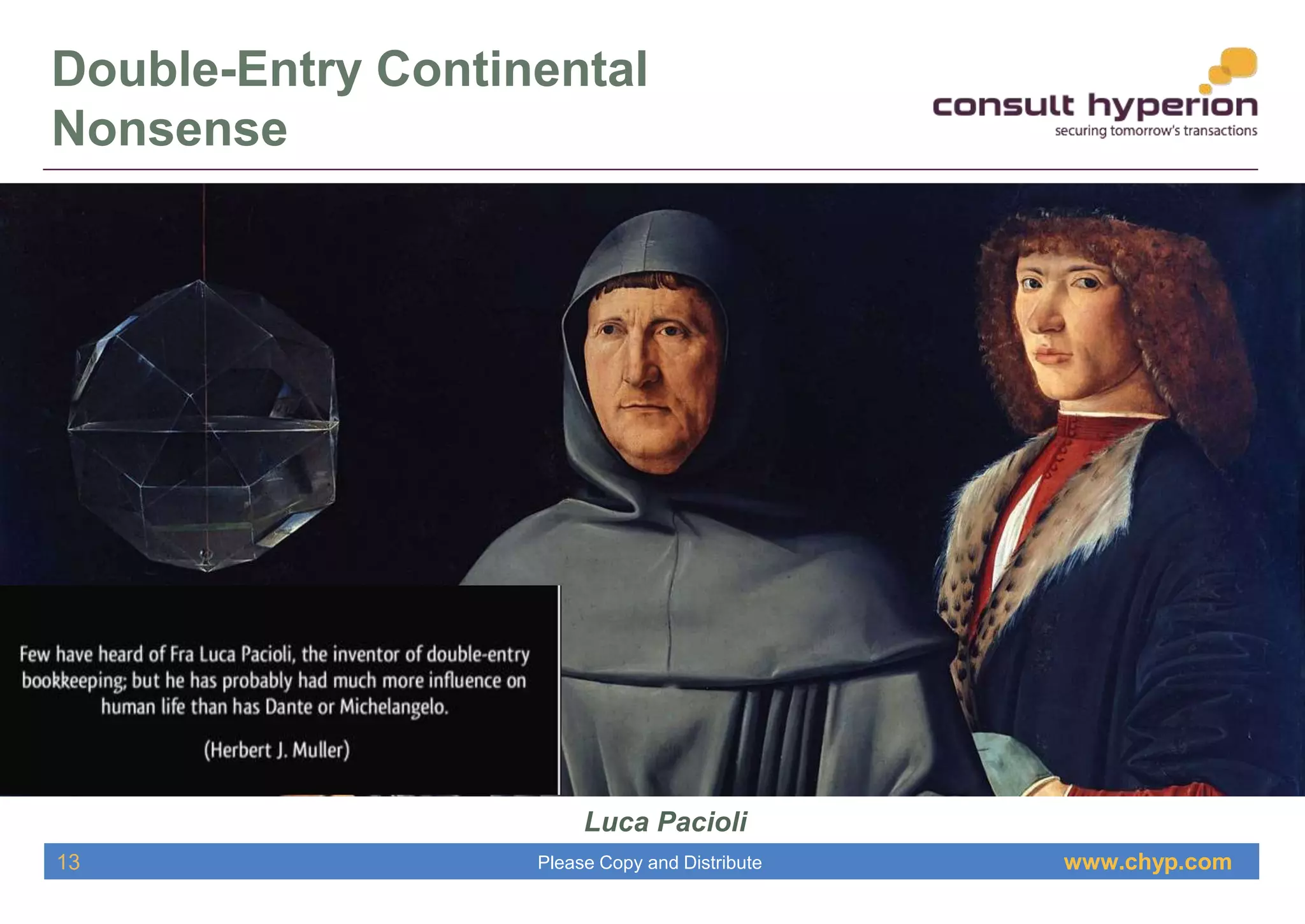

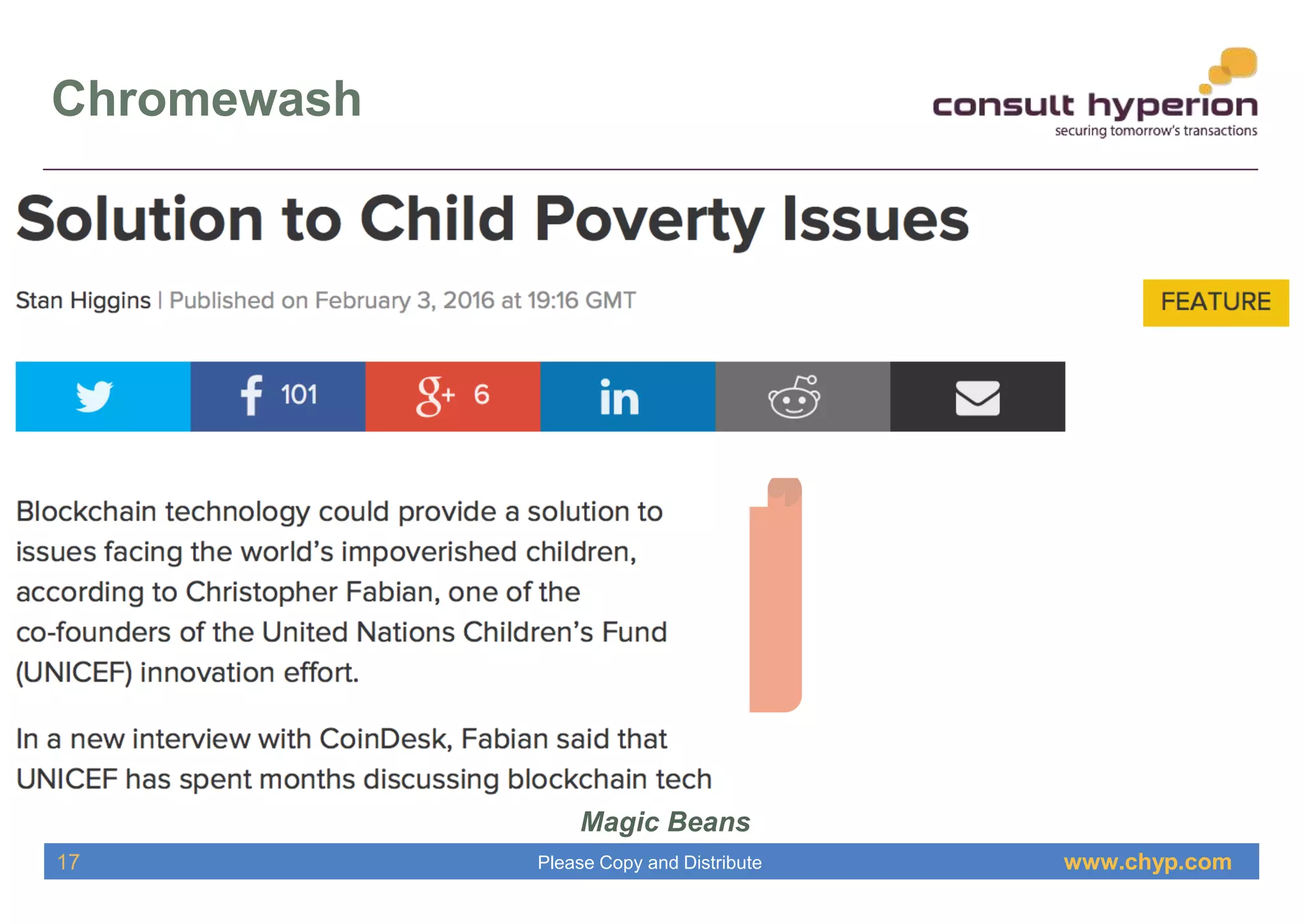

The document discusses the significance of fintech, highlighting influential figures like David G.W. Birch and referencing historical context for financial systems. It introduces concepts such as the need for immutable and accessible tax records, and presents ideas around blockchain technology. Furthermore, it emphasizes the conservative nature of finance and the evolving relationship between technology and debt monetization.