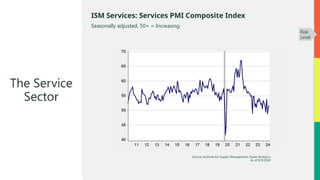

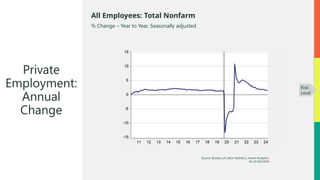

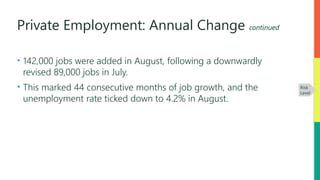

In September 2024, the service sector saw a slight improvement in confidence, with the PMI index rising to 51.5, although it has trended downwards over the year. Private employment continued to grow with 142,000 jobs added in August, leading to a decrease in the unemployment rate to 4.2%. Despite these positive signs, consumer confidence remains weak on a year-over-year basis, indicating potential economic challenges ahead.

![Economic Risk Factor Update: August 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateaugust2024am-240815171155-2612b755-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: June 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatejune2024am-240612135955-62fda29d-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: October 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateoctober2024am-241009015353-d2831b2a-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: July 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatejuly2024am-240712130225-147b17c8-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: May 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatemay2024am-240515130440-74d66100-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: March 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatemarch2024am-240313133142-2574fc7f-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: April 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateapril2024am-240417130922-b8ca38a5-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: February 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatefebruary2024am-240207153630-0724fa23-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: January 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatejanuary2024am-240110150920-3ad906d7-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: September 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateseptember2023am-230906173934-b5fa365e-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: November 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatenovember2023am-231108133417-ef934499-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: December 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatedecember2023am-231213134840-5e762269-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: October 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateoctober2023am-231011151056-66e85714-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: August 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateaugust2023am-230816184852-13dbaeea-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: September 2022 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateseptember2022-220908190947-72948a4f-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: April 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateapril2023-230412142206-19aefbed-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: May 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatemay2023-230510134611-1a672de5-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: October 2022 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdateoctober2022rlkfam-221012174700-98da4480-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: March 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatemarch2023-230314161429-1d4fab6a-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: July 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatejuly2023-230712140125-f973b1c9-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: February 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatefeburary2023rlam-230208172904-cd6e86be-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: June 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatejune2023-230607164130-edf07dd5-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: January 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatejanuary2023-230111180647-387605c3-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: November 2022 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatenovember2022amkf-221115155738-ea360603-thumbnail.jpg?width=640&height=640&fit=bounds)

![Economic Risk Factor Update: December 2022 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/economicriskfactorupdatedecember2022-221215184601-a4c55ce0-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: August 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateaugust2024am-240821135054-bcf05ed7-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: September 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatesept2024am-240918134147-6b6cc9a3-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: September 2022 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateseptember2022-220915194606-6c06e262-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: October 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateoct2024am-241016133219-d645282f-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: July 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatejuly2024am-240717142310-0da22cfe-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: June 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatejune2024am-pf2ka417-240618125718-421c825a-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: May 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatemay2024am-240522122148-e521348e-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: April 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateapril2024am-240424140359-342f2410-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: March 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatefebruary2024am-240320140945-833de20e-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: February 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatefebruary2024-240214182605-2944667c-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: January 2024 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatejanuary2024-240117184430-04ccf529-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: December 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatedecember2023-231220143729-32260328-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: November 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatenovember2023-231115143226-35f33125-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: October 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateoctober2023-231018170735-6202cf20-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: September 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateseptember2023-230912213959-e48e736b-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: August 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdateaugust2023-230823125440-082a056b-thumbnail.jpg?width=640&height=640&fit=bounds)

![Monthly Market Risk Update: July 2023 [SlideShare]](https://cdn.slidesharecdn.com/ss_thumbnails/monthlymarketriskupdatejuly2023-230719123124-43dfed09-thumbnail.jpg?width=640&height=640&fit=bounds)