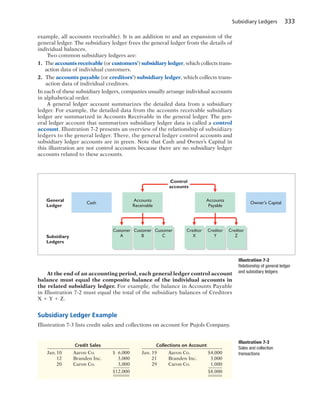

This document provides a summary of common account titles, their classification in financial statements, and their normal balance. It includes accounts like accounts payable, accounts receivable, accumulated depreciation, cash, common stock, and more. For each it lists whether it is a current asset, long-term asset, current liability, etc. and whether it has a normal debit or credit balance in accounts. This helps provide an overview of the basic accounts typically seen in financial statements.

![Learning Objectives

After studying this chapter, you should be able to:

[1] Explain what accounting is.

[2] Identify the users and uses of accounting.

[3] Understand why ethics is a fundamental business concept.

[4] Explain generally accepted accounting principles.

[5] Explain the monetary unit assumption and the economic

entity assumption.

[6] State the accounting equation, and define its components.

[7] Analyze the effects of business transactions on the

accounting equation.

[8] Understand the four financial statements and how they

are prepared.

Knowing the Numbers

Many students who take this course do not plan to be

accountants. If you are in that group, you might be thinking,

“If I’m not going to be an accountant, why do I need to

know accounting?” Well, consider this quote from Harold

Geneen, the former chairman of IT&T: “To be good at your

business, you have to know the numbers—cold.” In business,

accounting and financial statements are the means for

communicating the numbers. If you don’t know how to read

financial statements, you can’t really know your business.

Many businesses agree with this view. They see the value of

their employees being able to read financial statements and

understand how their actions affect the company’s financial

results. For example, consider Clif Bar & Company. The original

Clif Bar®

energy bar was created in 1990 after six months

of experimentation by Gary Erickson and his mother in her

kitchen. Today, the company has almost 300 employees and

is considered one of the leading Landor’s Breakaway Brands®

.

Clif Bar is guided by what it calls its Five Aspirations—

Sustaining Our Business, Our Brands, Our People, Our

Community, and the Planet. Its website documents its efforts

and accomplishments in these five areas. Just a few examples

include the company’s use of organic products to protect soil,

water, and biodiversity; the “smart” solar array (the largest in

North America), which provides nearly all the electrical needs

for its 115,000-square foot building; and the incentives Clif

Bar provides to employees to reduce their personal environ-

mental impact, such as $6,500 toward the purchase of an

efficient car or $1,000 per year for eco-friendly improvements

toward their homes.

One of the company’s proudest moments was the creation of

an employee stock ownership plan (ESOP) in 2010. This plan

gives its employees 20% ownership of the company (Gary

and his wife Kit own the other 80%). The ESOP also resulted

in Clif Bar enacting an open-book management program,

including the commitment to educate all employee-owners

about its finances. Armed with this basic financial knowledge,

employees are more aware of the financial impact of their

actions, which leads to better decisions.

Many other companies have adopted this open-book man-

agement approach. Even in companies that do not practice

1 Accounting in Action

Feature Story

✔ The Navigator

Learning Objectives give you a framework for learning the

specific concepts covered in the chapter.

The Navigator is a learning system designed to

prompt you to use the learning aids in the chapter

and set priorities as you study.

The Feature Story helps you picture how the chapter topic

relates to the real world of accounting and business. You

will find references to the story throughout the chapter.

Scan Learning Objectives

Read Feature Story

Read Preview

Read text and answer DO IT! p. 11

p. 14 p. 21 p. 25

Work Comprehensive DO IT! p. 26

Review Summary of Learning Objectives

Answer Self-Test Questions

Complete Assignments

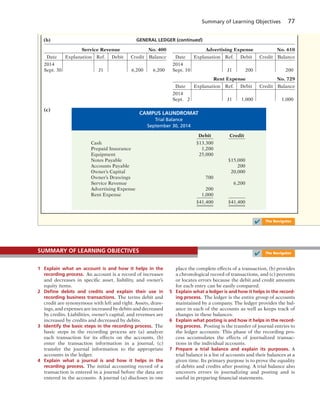

Go to WileyPLUS for practice and tutorials

Read A Look at IFRS p. 48

✔ The Navigator

✔ The Navigator

2](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-22-320.jpg)

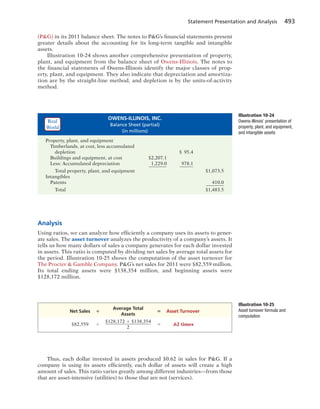

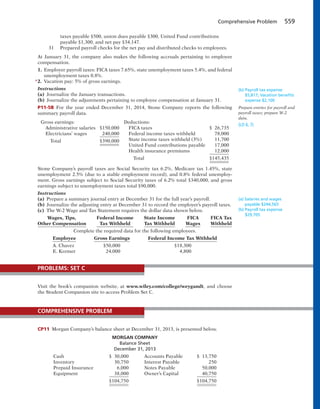

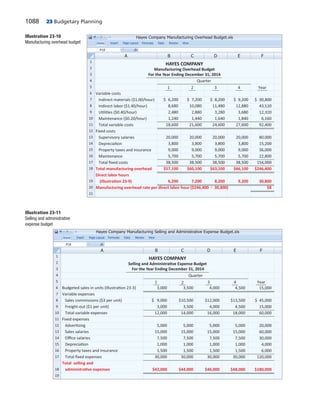

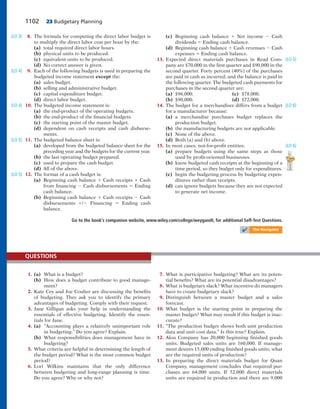

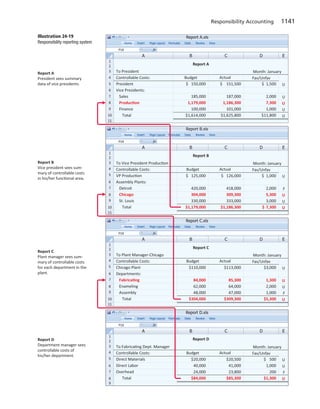

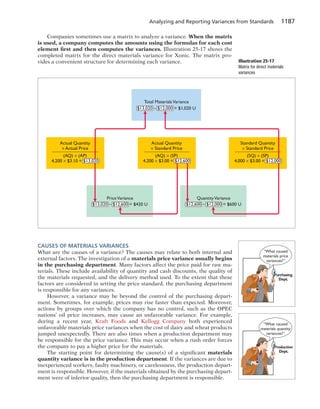

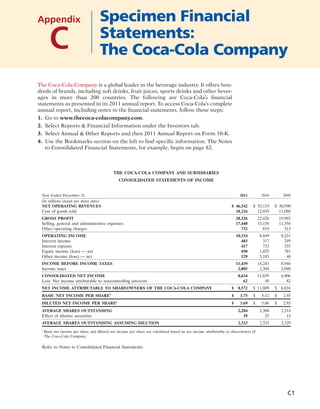

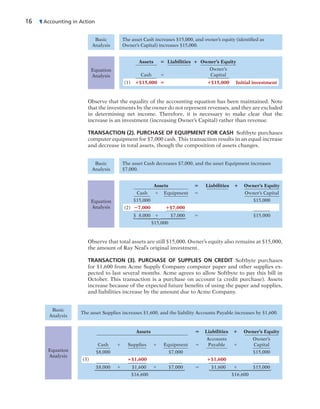

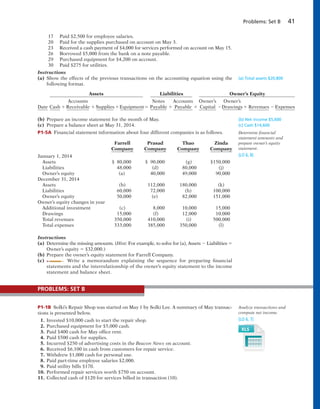

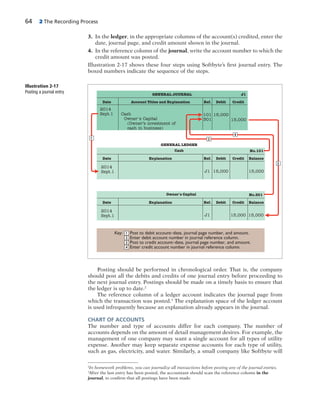

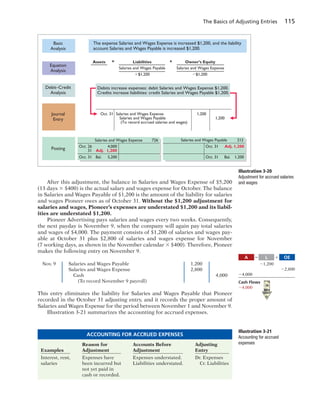

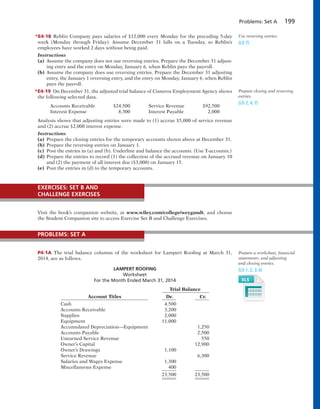

![18 1 Accounting in Action

time they are incurred. When Softbyte pays at a later date, the liability Accounts

Payable will decrease, and the asset Cash will decrease [see Transaction (8)]. The

cost of advertising is an expense (rather than an asset) because the company has

used the benefits. Advertising Expense is included in determining net income.

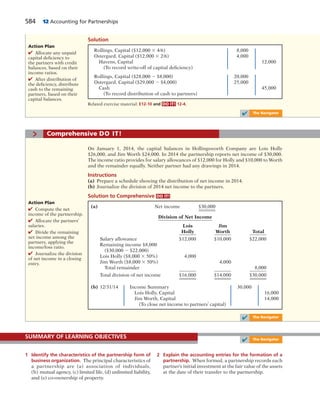

TRANSACTION (6). SERVICES PERFORMED FOR CASH AND CREDIT Softbyte

performs $3,500 of programming services for customers. The company receives

cash of $1,500 from customers, and it bills the balance of $2,000 on account. This

transaction results in an equal increase in assets and owner’s equity.

Softbyte recognizes $3,500 in revenue when it performs the service. In

exchange for this service, it received $1,500 in Cash and Accounts Receivable of

$2,000. This Accounts Receivable represents customers’ promises to pay $2,000

to Softbyte in the future. When it later receives collections on account, Softbyte

will increase Cash and will decrease Accounts Receivable [see Transaction (9)].

TRANSACTION (7). PAYMENT OF EXPENSES Softbyte pays the following ex-

penses in cash for September: store rent $600, salaries and wages of employees

$900, and utilities $200. These payments result in an equal decrease in assets and

owner’s equity.

Three specific items are affected: The asset Cash increases $1,500, the asset Accounts Receivable

increases $2,000, and owner’s equity increases $3,500 due to Service Revenue.

Basic

Analysis

Equation

Analysis

Assets 5 Liabilities 1 Owner’s Equity

Accounts Accounts Owner’s

Cash 1 Receivable 1 Supplies 1 Equipment 5 Payable 1 Capital 1 Revenues 2 Expenses

$9,200 $1,600 $7,000 $1,850 $15,000 $1,200 $250

(6) 11,500 1$2,000 13,500 Service

$10,700 1 $2,000 1 $1,600 1 $7,000 5 $1,850 1 $15,000 1 $4,700 2 $250 Revenue

$21,300 $21,300

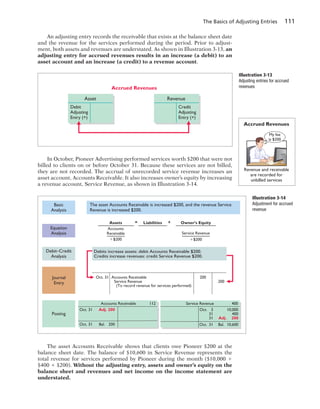

⎧

⎪

⎪

⎪

⎪

⎪

⎪

⎪

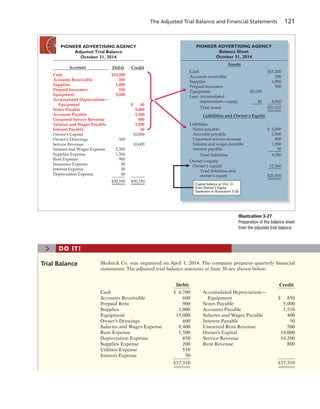

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎩

⎧

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎩

The asset Cash decreases $1,700, and owner’s equity decreases $1,700 due to the specific expense

categories (Rent Expense, Salaries and Wages Expense, and Utilities Expense).

Basic

Analysis

⎧

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎩

⎧

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎩

Assets 5 Liabilities 1 Owner’s Equity

Accounts Accounts Owner’s

Cash 1 Receivable 1 Supplies 1 Equipment 5 Payable 1 Capital 1 Revenues 2 Expenses

$10,700 $2,000 $1,600 $7,000 $1,850 $15,000 $4,700 $ 250

(7) 21,700 2600

2900

2200

$9,000 1 $2,000 1 $1,600 1 $7,000 5 $1,850 1 $15,000 1 $4,700 2 $1,950

$19,600 $19,600

Rent Expense

Sal. and Wages Exp.

Utilities Exp.

Equation

Analysis](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-38-320.jpg)

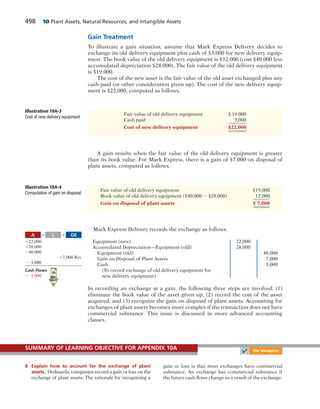

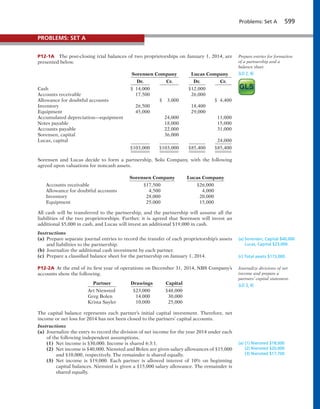

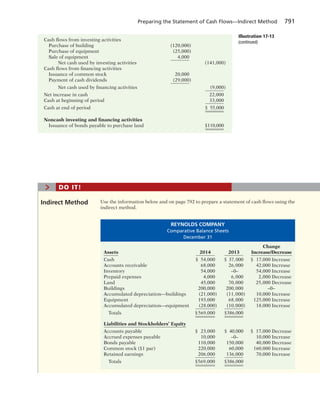

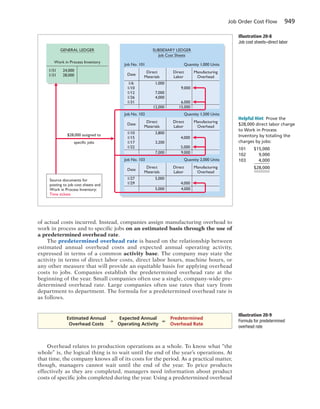

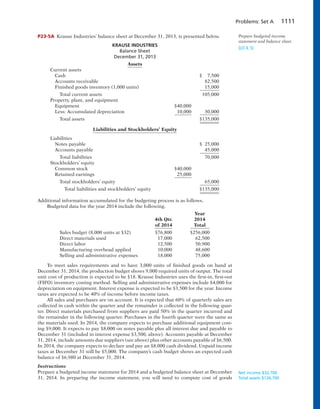

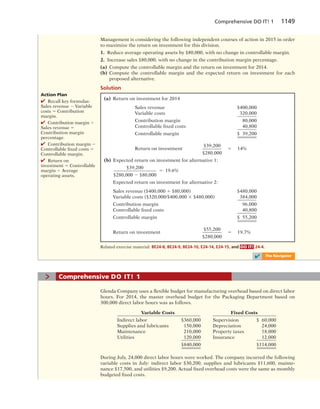

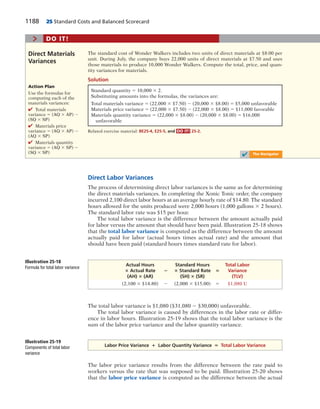

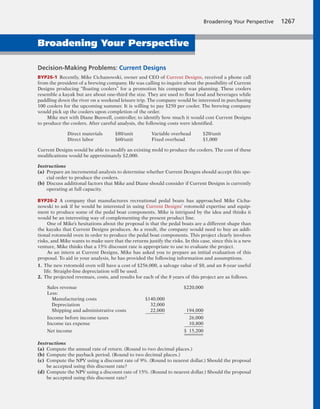

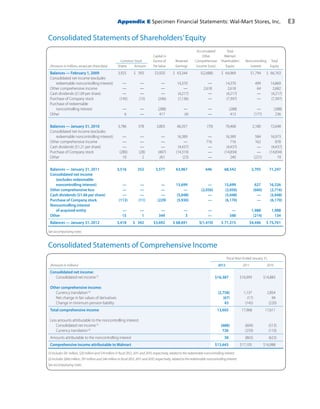

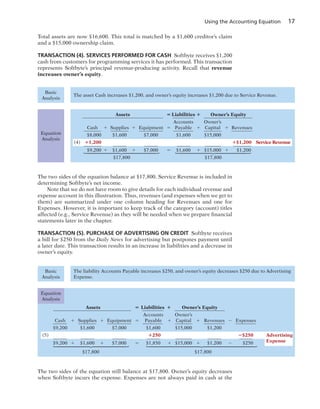

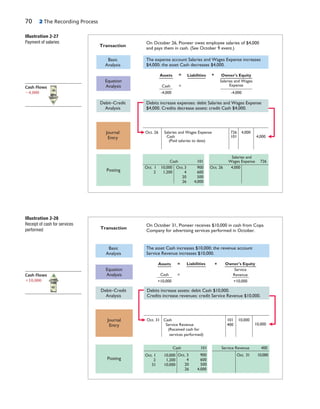

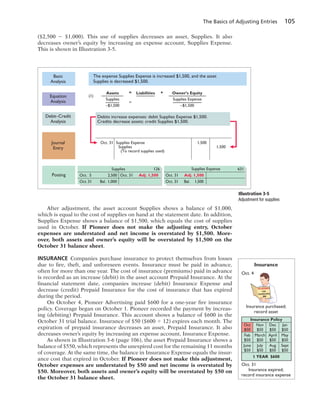

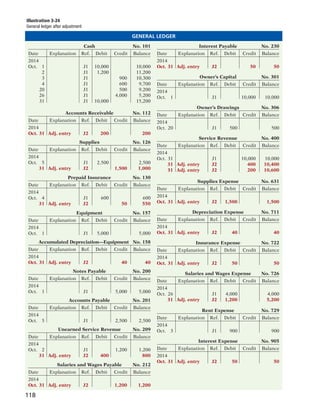

![Using the Accounting Equation 19

The two sides of the equation now balance at $19,600. Three lines in the analysis

indicate the different types of expenses that have been incurred.

TRANSACTION (8). PAYMENT OF ACCOUNTS PAYABLE Softbyte pays its $250

Daily News bill in cash. The company previously [in Transaction (5)] recorded the

bill as an increase in Accounts Payable and a decrease in owner’s equity.

Equation

Analysis

This cash payment “on account” decreases the asset Cash by $250 and also decreases the liability

Accounts Payable by $250.

Basic

Analysis

Assets 5 Liabilities 1 Owner’s Equity

Accounts Accounts Owner’s

Cash 1 Receivable 1 Supplies 1 Equipment 5 Payable 1 Capital 1 Revenues 2 Expenses

$9,000 $2,000 $1,600 $7,000 $1,850 $15,000 $4,700 $1,950

2250 2250

$8,750 1 $2,000 1 $1,600 1 $7,000 5 $1,600 1 $15,000 1 $4,700 2 $1,950

$19,350 $19,350

⎧

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎩

⎧

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎩

(8)

Observe that the payment of a liability related to an expense that has previously

been recorded does not affect owner’s equity. The company recorded this expense

in Transaction (5) and should not record it again.

TRANSACTION (9). RECEIPT OF CASH ON ACCOUNT Softbyte receives $600

in cash from customers who had been billed for services [in Transaction (6)].

Transaction (9) does not change total assets, but it changes the composition of

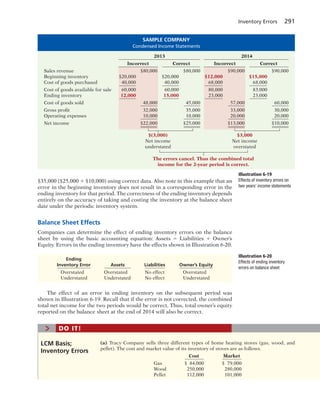

those assets.

The asset Cash increases $600, and the asset Accounts Receivable decreases $600.

Basic

Analysis

Assets 5 Liabilities 1 Owner’s Equity

Accounts Accounts Owner’s

Cash 1 Receivable 1 Supplies 1 Equipment 5 Payable 1 Capital 1 Revenues 2 Expenses

$8,750 $2,000 $1,600 $7,000 $1,600 $15,000 $4,700 $1,950

1600 2600

$9,350 1 $1,400 1 $1,600 1 $7,000 5 $1,600 1 $15,000 1 $4,700 2 $1,950

$19,350 $19,350

⎧

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎩

⎧

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎪

⎪

⎪

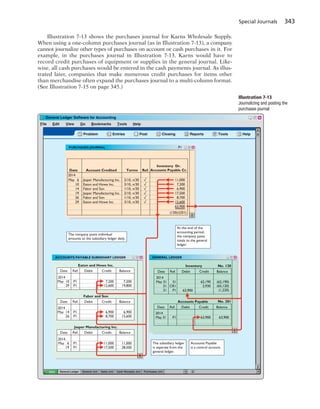

⎪

⎪

⎩

(9)

Equation

Analysis

Note that the collection of an account receivable for services previously billed

and recorded does not affect owner’s equity. Softbyte already recorded this reve-

nue in Transaction (6) and should not record it again.

TRANSACTION (10). WITHDRAWAL OF CASH BY OWNER Ray Neal withdraws

$1,300 in cash from the business for his personal use. This transaction results in

an equal decrease in assets and owner’s equity.](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-39-320.jpg)

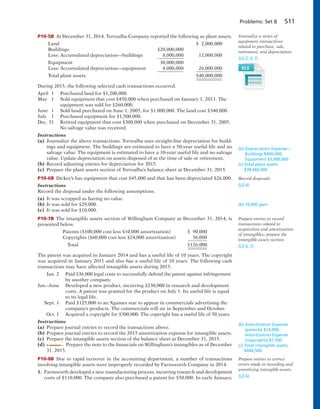

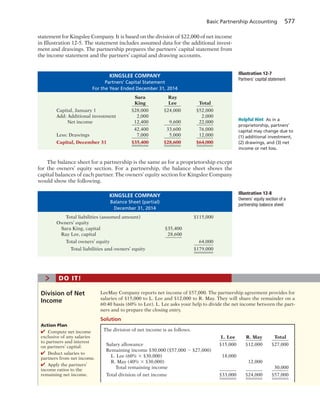

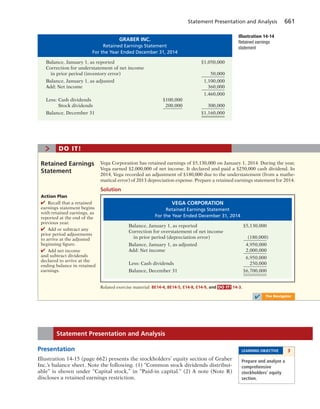

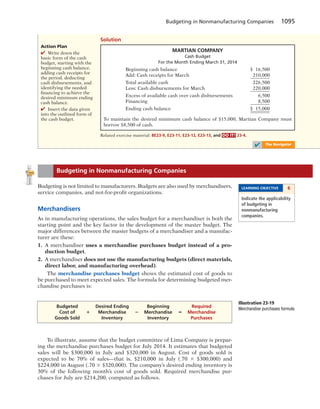

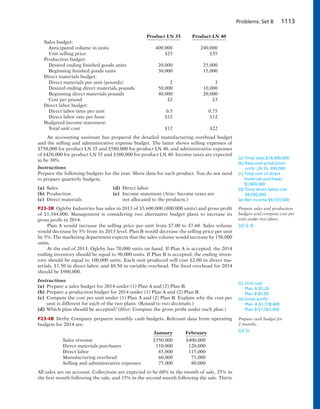

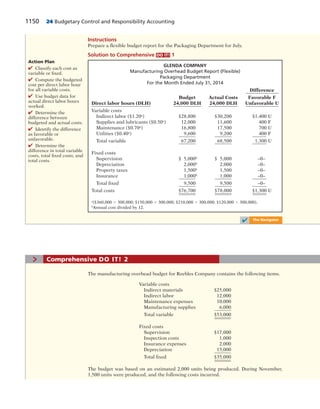

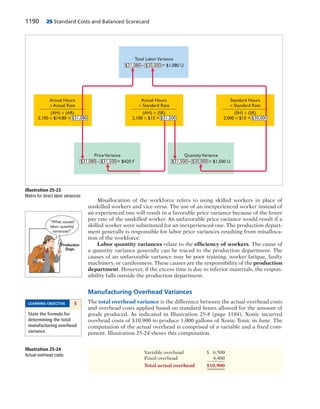

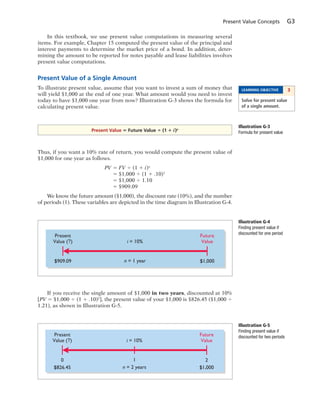

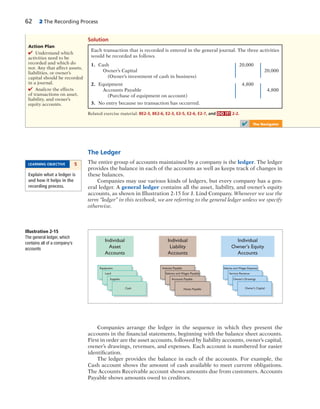

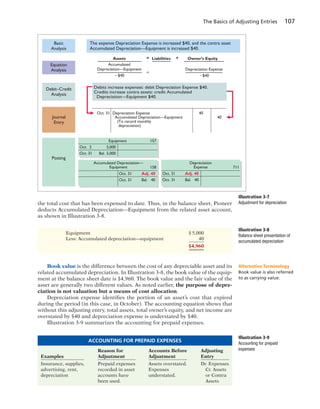

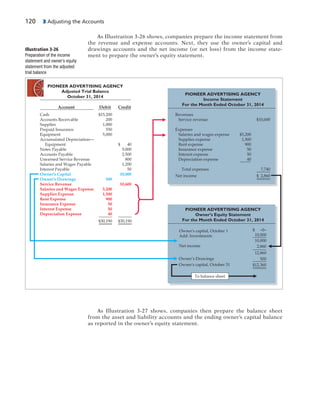

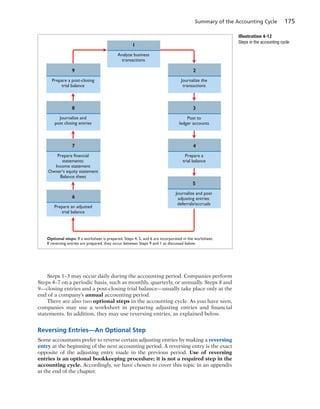

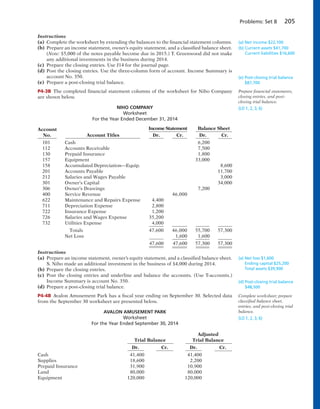

![26 1 Accounting in Action

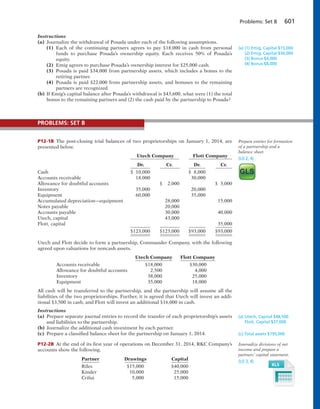

Joan Robinson opens her own law office on July 1, 2014. During the first month of opera-

tions, the following transactions occurred.

1. Joan invested $11,000 in cash in the law practice.

2. Paid $800 for July rent on office space.

3. Purchased office equipment on account $3,000.

4. Performed legal services to clients for cash $1,500.

5. Borrowed $700 cash from a bank on a note payable.

6. Performed legal services for client on account $2,000.

7. Paid monthly expenses: salaries and wages $500, utilities $300, and advertising $100.

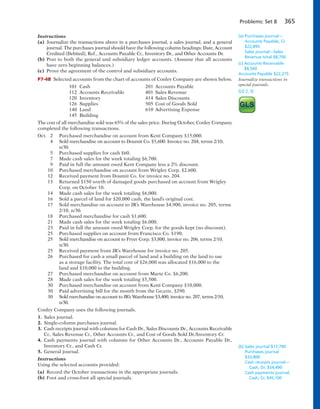

8. Joan withdraws $1,000 cash for personal use.

Instructions

(a) Prepare a tabular summary of the transactions.

(b) Prepare the income statement, owner’s equity statement, and balance sheet at July 31

for Joan Robinson, Attorney.

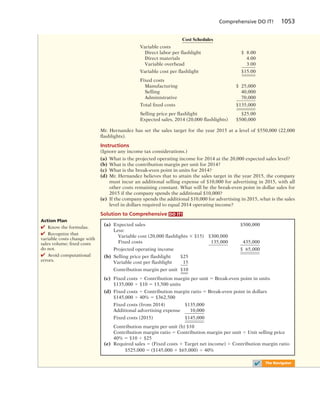

Solution to Comprehensive DO IT!

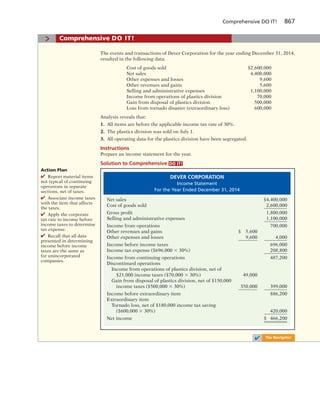

> Comprehensive DO IT!

The Comprehensive

DO IT! is a final review

of the chapter. The

Action Plan gives tips

about how to approach

the problem, and the

Solution demonstrates

both the form and

content of complete

answers.

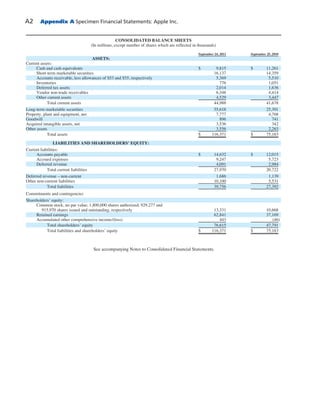

Assets 5 Liabilities 1 Owner’s Equity

Trans- Accounts Notes Accounts Owner’s Owner’s

action Cash 1 Receivable 1 Equipment 5 Payable 1 Payable 1 Capital 2 Drawings 1 Revenues 2 Expenses

(1) 1$11,000 5 1$11,000

(2) 2800 2$800

(3) 1$3,000 5 1$3,000

(4) 11,500 1$1,500

(5) 1700 1$700

(6) 1$2,000 12,000

(7) 2500 2500

2300 2300

2100 2100

(8) 21,000 2$1,000

$10,500 1 $2,000 1 $3,000 5 $700 1 $3,000 1 $11,000 2 $1,000 1 $3,500 2 $1,700

$15,500 $15,500

⎧

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎩

⎧

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎪

⎩

(a)

(c) The ending owner’s equity of Flanagan Company is $8,500. By rewriting the

accounting equation, we can compute owner’s equity as assets minus liabilities, as

follows.

Total assets [as computed in (a)] $27,000

Less: Liabilities

Notes payable $16,500

Accounts payable 2,000 18,500

Owner’s equity $ 8,500

Note that it is not possible to determine the company’s owner’s equity in any

other way because the beginning total for owner’s equity is not provided.

Related exercise material: BE1-10, BE1-11, E1-9, E1-12, E1-13, E1-14, E1-15, E1-16, and DO IT! 1-4.

✔ The Navigator](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-46-320.jpg)

![Learning Objectives

After studying this chapter, you should be able to:

[1] Explain what an account is and how it helps in the

recording process.

[2] Define debits and credits and explain their use in recording

business transactions.

[3] Identify the basic steps in the recording process.

[4] Explain what a journal is and how it helps in the recording

process.

[5] Explain what a ledger is and how it helps in the recording

process.

[6] Explain what posting is and how it helps in the recording

process.

[7] Prepare a trial balance and explain its purposes.

Accidents Happen

How organized are you financially? Take a short quiz. Answer

yes or no to each question:

• Does your wallet contain so many cash machine receipts

that you’ve been declared a walking fire hazard?

• Do you wait until you debit card is denied before

checking the status of your funds?

• Was Aaron Rodgers (the quarterback for the Green Bay

Packers) playing high school football the last time you

verified the accuracy of your bank account?

If you think it is hard to keep track of the many transactions

that make up your life, imagine how difficult it is for a big

corporation to do so. Not only that, but now consider how

important it is for a large company to have good accounting

records, especially if it has control of your life savings. MF

Global Holdings Ltd is such a company. As a big investment

broker, it held billions of dollars of investments for clients.

If you had your life savings invested at MF Global, you might

be slightly displeased if you heard this from one of its

representatives: “You know, I kind of remember an account

for someone with a name like yours—now what did we do

with that?”

Unfortunately, that is almost exactly what happened to MF

Global’s clients shortly before it recently filed for bankruptcy.

During the days immediately following the bankruptcy filing,

regulators and auditors struggled to piece things together. In

the words of one regulator, “Their books are a disaster . . .

we’re trying to figure out what numbers are real numbers.”

One company that considered buying an interest in MF

Global walked away from the deal because it “couldn’t get a

sense of what was on the balance sheet.” That company said

the information that should have been instantly available

instead took days to produce.

It now appears that MF Global did not properly segregate

customer accounts from company accounts. And, because of

its sloppy recordkeeping, customers were not protected

when the company had financial troubles. Total customer

losses were approximately $1 billion. As you can see,

accounting matters!

Source: S. Patterson and A. Lucchetti, “Inside the Hunt for MF Global Cash,”

Wall Street Journal Online (November 11, 2011).

2 The Recording Process

Feature Story

✔ The Navigator

Scan Learning Objectives

Read Feature Story

Read Preview

Read text and answer DO IT! p. 58

p. 61 p. 71 p. 75

Work Comprehensive DO IT! p. 75

Review Summary of Learning Objectives

Answer Self-Test Questions

Complete Assignments

Go to WileyPLUS for practice and tutorials

Read A Look at IFRS p. 96

✔ The Navigator

✔ The Navigator

52](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-72-320.jpg)

![Learning Objectives

After studying this chapter, you should be able to:

[1] Explain the time period assumption.

[2] Explain the accrual basis of accounting.

[3] Explain the reasons for adjusting entries and identify the

major types of adjusting entries.

[4] Prepare adjusting entries for deferrals.

[5] Prepare adjusting entries for accruals.

[6] Describe the nature and purpose of an adjusted

trial balance.

Keeping Track of Groupons

Who doesn’t like buying things at a discount? That’s why it’s

not surprising that three years after it started as a company,

Groupon was estimated to be worth $16 billion. This trans-

lates into an average increase in value of almost $15 million

per day.

Now consider that Groupon had previously been estimated

to be worth even more than that. What happened? Well,

accounting regulators and investors began to question the

way that Groupon had accounted for some of its transactions.

But if Groupon sells only coupons (“groupons”), you’re

probably wondering how hard can it be to accurately account

for that? It turns out that accounting for coupons is not as

easy as you might think.

First, consider what happens when Groupon makes a

sale. Suppose it sells a groupon for $30 for Highrise

Hamburgers. When it receives the $30 from the customer,

it must turn over half of that amount ($15) to Highrise

Hamburgers. So should Groupon record revenue for the full

$30 or just $15? Until recently, Groupon recorded the full

$30. But, in response to an SEC ruling on the issue, Groupon

now records revenue of $15 instead.

A second issue is a matter of timing. When should Groupon

record this $15 revenue? Should it record the revenue when it

sells the groupon, or must it wait until the customer uses the

groupon at Highrise Hamburgers? You can find the answer to

this question in the notes to Groupon’s financial statements.

It recognizes the revenue once “the number of customers

who purchase the daily deal exceeds the predetermined

threshold, the Groupon has been electronically delivered to

the purchaser and a listing of Groupons sold has been made

available to the merchant.”

The accounting becomes even more complicated when you

consider the company’s loyalty programs. Groupon offers free

or discounted groupons to its subscribers for doing things

such as referring new customers or participating in promotions.

These groupons are to be used for future purchases, yet the

company must record the expense at the time the customer

receives the groupon. The cost of these programs is huge for

Groupon, so the timing of this expense can definitely affect its

reported income.

The final kicker is that Groupon, like all other companies,

must rely on many estimates in its financial reporting.

For example, Groupon reports that “estimates are utilized

3 Adjusting the Accounts

Feature Story

✔ The Navigator

Scan Learning Objectives

Read Feature Story

Read Preview

Read text and answer DO IT! p. 102

p. 110 p. 116 p. 121

Work Comprehensive DO IT! p. 122

Review Summary of Learning Objectives

Answer Self-Test Questions

Complete Assignments

Go to WileyPLUS for practice and tutorials

Read A Look at IFRS p. 157

98

✔ The Navigator

✔ The Navigator](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-118-320.jpg)

![142 3 Adjusting the Accounts

facilities. The 2014 income statement for the club showed that service revenue of $161,000

was earned during the year.

Instructions

(Hint: You will probably find it helpful to use T-accounts to analyze these data.)

(a) Prepare journal entries for each of the following events that took place during 2014.

(1) Accounts receivable from 2013 were all collected.

(2) Gift certificates outstanding at the end of 2013 were all redeemed.

(3) An additional $38,000 worth of gift certificates were sold during 2014. A portion

of these was used by the recipients during the year; the remainder was still out-

standing at the end of 2014.

(4) Services performed for members for 2014 were billed to members.

(5) Accounts receivable for 2014 (i.e., those billed in item [4] above) were partially

collected.

(b) Determine the amount of cash received by the club, with respect to member services,

during 2014.

*E3-16 Aaron Lynch Company has the following balances in selected accounts on

December 31, 2014.

Service Revenue $40,000

Insurance Expense 2,700

Supplies Expense 2,450

All the accounts have normal balances. Aaron Lynch Company debits prepayments to

expense accounts when paid, and credits unearned revenues to revenue accounts when

received. The following information below has been gathered at December 31, 2014.

1. Aaron Lynch Company paid $2,700 for 12 months of insurance coverage on June 1,

2014.

2. On December 1, 2014, Aaron Lynch Company collected $40,000 for consulting services

to be performed from December 1, 2014, through March 31, 2015.

3. A count of supplies on December 31, 2014, indicates that supplies of $900 are on hand.

Instructions

Prepare the adjusting entries needed at December 31, 2014.

*E3-17 At Cambridge Company, prepayments are debited to expense when paid, and

unearned revenues are credited to revenue when cash is received. During January of the

current year, the following transactions occurred.

Jan. 2 Paid $1,920 for fire insurance protection for the year.

10 Paid $1,700 for supplies.

15 Received $6,100 for services to be performed in the future.

On January 31, it is determined that $2,500 of the services were performed and that there

are $650 of supplies on hand.

Instructions

(a) Journalize and post the January transactions. (Use T-accounts.)

(b) Journalize and post the adjusting entries at January 31.

(c) Determine the ending balance in each of the accounts.

*E3-18 Presented below are the assumptions and principles discussed in this chapter.

1. Full disclosure principle. 4. Time period assumption.

2. Going concern assumption. 5. Historical cost principle.

3. Monetary unit assumption. 6. Economic entity assumption.

Instructions

Identify by number the accounting assumption or principle that is described below. Do

not use a number more than once.

_______ (a) Is the rationale for why plant assets are not reported at liquidation value.

(Note: Do not use the historical cost principle.)

_______ (b) Indicates that personal and business record-keeping should be separately

maintained.

_______ (c) Assumes that the monetary unit is the “measuring stick” used to report on

financial performance.

_______ (d) Separates financial information into time periods for reporting purposes.

Journalize transactions and

adjusting entries.

(LO 7)

Identify accounting assump-

tions and principles.

(LO 8)

Journalize adjusting entries.

(LO 7)](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-162-320.jpg)

![Learning Objectives

After studying this chapter, you should be able to:

[1] Prepare a worksheet.

[2] Explain the process of closing the books.

[3] Describe the content and purpose of a post-closing

trial balance.

[4] State the required steps in the accounting cycle.

[5] Explain the approaches to preparing correcting entries.

[6] Identify the sections of a classified balance sheet.

Everyone Likes to Win

When Ted Castle was a hockey coach at the University of

Vermont, his players were self-motivated by their desire to

win. Hockey was a game you usually either won or lost. But

at Rhino Foods, Inc., a bakery-foods company he founded in

Burlington, Vermont, he discovered that manufacturing-line

workers were not so self-motivated. Ted thought, what if he

turned the food-making business into a game, with rules,

strategies, and trophies?

In a game, knowing the score is all-important. Ted felt that

only if the employees know the score—know exactly how

the business is doing daily, weekly, monthly—could he turn

food-making into a game. But Rhino is a closely held, family-

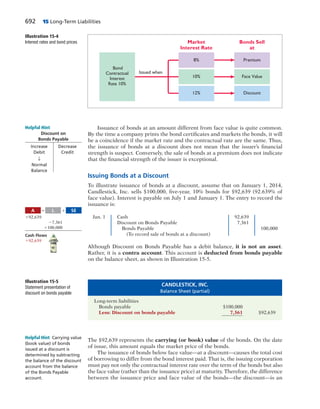

owned business, and its financial statements and profits were

confidential. Ted wondered, should he open Rhino’s books to

the employees?

A consultant put Ted’s concerns in perspective when he said,

“Imagine you’re playing touch football. You play for an hour

or two, and the whole time I’m sitting there with a book,

keeping score. All of a sudden I blow the whistle, and I say,

‘OK, that’s it. Everybody go home.’ I close my book and walk

away. How would you feel?” Ted opened his books and

revealed the financial statements to his employees.

The next step was to teach employees the rules and strategies

of how to “win” at making food. The first lesson: “Your

opponent at Rhino is expenses. You must cut and control

expenses.” Ted and his staff distilled those lessons into daily

scorecards—production reports and income statements—that

keep Rhino’s employees up-to-date on the game. At noon

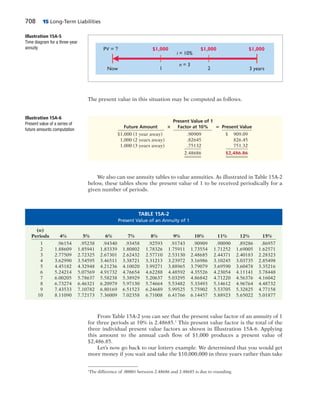

each day, Ted posts the previous day’s results at the entrance

to the production room. Everyone checks whether they made

or lost money on what they produced the day before. And it’s

not just an academic exercise: There’s a bonus check for each

employee at the end of every four-week “game” that meets

profitability guidelines.

Rhino has flourished since the first game. Employment has

increased from 20 to 130 people, while both revenues and

profits have grown dramatically.

4 Completing the

Accounting Cycle

Feature Story

✔ The Navigator

Scan Learning Objectives

Read Feature Story

Read Preview

Read text and answer DO IT! p. 167

p. 172 p. 181 p. 183

Work Comprehensive DO IT! p. 184

Review Summary of Learning Objectives

Answer Self-Test Questions

Complete Assignments

Go to WileyPLUS for practice and tutorials

Read A Look at IFRS p. 212

160

✔ The Navigator

✔ The Navigator

160](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-180-320.jpg)

![Learning Objectives

After studying this chapter, you should be able to:

[1] Identify the differences between service and merchandising

companies.

[2] Explain the recording of purchases under a perpetual

inventory system.

[3] Explain the recording of sales revenues under a perpetual

inventory system.

[4] Explain the steps in the accounting cycle for a merchandising

company.

[5] Distinguish between a multiple-step and a single-step

income statement.

✔ The Navigator

Scan Learning Objectives

Read Feature Story

Read Preview

Read text and answer DO IT! p. 225

p. 229 p. 232 p. 237

Work Comprehensive DO IT! p. 238

Review Summary of Learning Objectives

Answer Self-Test Questions

Complete Assignments

Go to WileyPLUS for practice and tutorials

Read A Look at IFRS p. 271

216

Buy Now, Vote Later

Have you ever shopped for outdoor gear at an REI (Recreational

Equipment Incorporated) store? If so, you might have been

surprised if a salesclerk asked if you were a member. A

member? What do you mean a member? You soon realize

that REI might not be your typical store. In fact, there’s a lot

about REI that makes it different.

REI is a consumer cooperative, or “co-op” for short. To figure

out what that means, consider this quote from the company’s

annual report:

As a cooperative, the Company is owned by its members. Each

member is entitled to one vote in the election of the Company’s

Board of Directors. Since January 1, 2008, the nonrefundable,

nontransferable, one-time membership fee has been $20

dollars. As of December 31, 2010, there were approximately

10.8 million members.

Voting rights? Now that’s something you don’t get from

shopping at Wal-Mart. REI members get other benefits as

well, including sharing in the company’s profits through a

dividend at the end of the year, which can be used for

purchases at REI stores during the next two years. The more

you spend, the bigger your dividend.

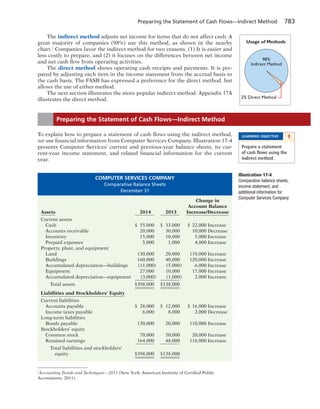

Since REI is a co-op, you might wonder whether manage-

ment’s incentives might be a little different. For example, is

management still concerned about making a profit? The

answer is yes, as it ensures the long-term viability of the

company. At the same time, REI’s members want the com-

pany to be run efficiently, so that prices remain low. In order

for its members to evaluate just how well management is

doing, REI publishes an audited annual report, just like

publicly traded companies do. So, while profit maximization

might not be the ultimate goal for REI, the accounting and

reporting issues are similar to those of a typical corporation.

How well is this business model working for REI? Well, it has

consistently been rated as one of the best places to work in

the United States. It was ranked 8th on Fortune’s 2012 list.

Also, REI had sustainable business practices long before social

responsibility became popular at other companies. The CEO’s

Stewardship Report states “we reduced the absolute amount

of energy we use despite opening four new stores and

growing our business; we grew the amount of FSC-certified

✔ The Navigator

5

Accounting for

Merchandising

Operations

Feature Story ✔ The Navigator](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-240-320.jpg)

![Learning Objectives

After studying this chapter, you should be able to:

[1] Determine how to classify inventory and inventory quantities.

[2] Explain the accounting for inventories and apply the

inventory cost flow methods.

[3] Explain the financial effects of the inventory cost flow

assumptions.

[4] Explain the lower-of-cost-or-market basis of accounting

for inventories.

[5] Indicate the effects of inventory errors on the financial

statements.

[6] Compute and interpret the inventory turnover.

“Where Is That Spare

Bulldozer Blade?”

Let’s talk inventory—big, bulldozer-size inventory. Caterpillar

Inc. is the world’s largest manufacturer of construction and

mining equipment, diesel and natural gas engines, and

industrial gas turbines. It sells its products in over 200 countries,

making it one of the most successful U.S. exporters. More

than 70% of its productive assets are located domestically,

and nearly 50% of its sales are foreign.

In the past, Caterpillar’s profitability suffered, but today

it is very successful. A big part of this turnaround can be

attributed to effective management of its inventory. Imagine

what it costs Caterpillar to have too many bulldozers sitting

around in inventory—a situation the company definitely

wants to avoid. Conversely, Caterpillar must make sure it

has enough inventory to meet demand.

At one time during a 7-year period, Caterpillar’s sales increased

by 100%, while its inventory increased by only 50%. To

achieve this dramatic reduction in the amount of resources

tied up in inventory, while continuing to meet customers’

needs, Caterpillar used a two-pronged approach. First, it

completed a factory modernization program, which greatly

increased its production efficiency. The program reduced by

60% the amount of inventory the company processed at any

one time. It also reduced by an incredible 75% the time

it takes to manufacture a part.

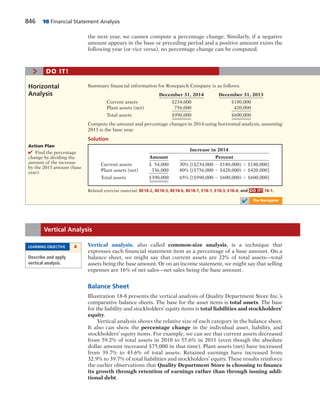

Second, Caterpillar dramatically improved its parts distribution

system. It ships more than 100,000 items daily from its 23

distribution centers strategically located around the world

(10 million square feet of warehouse space—remember, we’re

talking bulldozers). The company can virtually guarantee that

it can get any part to anywhere in the world within 24 hours.

After these changes, Caterpillar had record exports, profits,

and revenues. It would seem that things couldn’t be better.

But industry analysts, as well as the company’s managers,

thought otherwise. In order to maintain Caterpillar’s position

as the industry leader, management began another major

6 Inventories

Feature Story

✔ The Navigator

274

Scan Learning Objectives

Read Feature Story

Read Preview

Read text and answer DO IT! p. 280

p. 286 p. 291 p. 294

Work Comprehensive DO IT! 1 p. 294

2 p. 299

Review Summary of Learning Objectives

Answer Self-Test Questions

Complete Assignments

Go to WileyPLUS for practice and tutorials

Read A Look at IFRS p. 324

✔ The Navigator

✔ The Navigator](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-298-320.jpg)

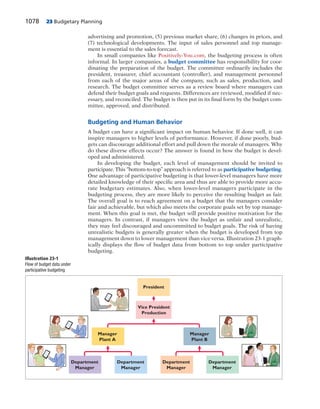

![286 6 Inventories

We can verify the cost of goods sold under this method by multiplying the

units sold times the weighted-average unit cost (550 3 $12 5 $6,600). Note that

this method does not use the average of the unit costs. That average is $11.50

($10 1 $11 1 $12 1 $13 5 $46; $46 4 4). The average-cost method instead uses

the average weighted by the quantities purchased at each unit cost.

Cost of goods available for sale 5 (4,000 3 $3) 1 (6,000 3 $4) 5 $36,000

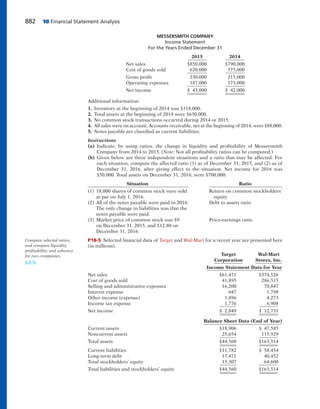

Ending inventory 5 10,000 2 7,000 5 3,000 units

(a) FIFO: $36,000 2 (3,000 3 $4) 5 $24,000

(b) LIFO: $36,000 2 (3,000 3 $3) 5 $27,000

(c) Average cost per unit: [(4,000 @ $3) 1 (6,000 @ $4)] 4 10,000 5 $3.60

Average-cost: $36,000 2 (3,000 3 $3.60) 5 $25,200

The accounting records of Shumway Ag Implements show the following data.

Beginning inventory 4,000 units at $ 3

Purchases 6,000 units at $ 4

Sales 7,000 units at $12

Determine the cost of goods sold during the period under a periodic inventory system

using (a) the FIFO method, (b) the LIFO method, and (c) the average-cost method.

Solution

Cost Flow

Methods

Action Plan

✔ Understand the

periodic inventory system.

✔ Allocate costs between

goods sold and goods on

hand (ending inventory)

for each cost flow method.

✔ Compute cost of

goods sold for each

method. Related exercise material: BE6-3, BE6-4, BE6-5, E6-3, E6-4, E6-5, E6-6, E6-7, E6-8, and DO IT! 6-2.

> DO IT!

✔ The Navigator

Financial Statement and Tax Effects of Cost Flow Methods

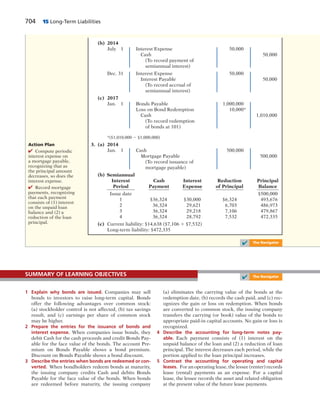

Each of the three assumed cost flow methods is acceptable for use. For example,

Reebok International Ltd. and Wendy’s International currently use the FIFO

method of inventory costing. Campbell Soup Company, Krogers, and Walgreen

Drugs use LIFO for part or all of their inventory. Bristol-Myers Squibb, Starbucks,

and Motorola use the average-cost method. In fact, a company may also use more

than one cost flow method at the same time. Stanley Black & Decker Manufacturing

Company, for example, uses LIFO for domestic inventories and FIFO for foreign

inventories. Illustration 6-12 (in the margin) shows the use of the three cost flow

methods in 500 large U.S. companies.

The reasons companies adopt different inventory cost flow methods are varied,

but they usually involve one of three factors: (1) income statement effects, (2)

balance sheet effects, or (3) tax effects.

INCOME STATEMENT EFFECTS

To understand why companies might choose a particular cost flow method, let’s

examine the effects of the different cost flow assumptions on the financial statements

of Houston Electronics. The condensed income statements in Illustration 6-13

assume that Houston sold its 550 units for $18,500, had operating expenses of $9,000,

and is subject to an income tax rate of 30%.

LEARNING OBJECTIVE 3

Explain the financial

effects of the inventory

cost flow assumptions.

24%

LIFO

45%

FIFO

16%

Average-

Cost

15%

Other

Illustration 6-12

Use of cost flow methods in

major U.S. companies](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-310-320.jpg)

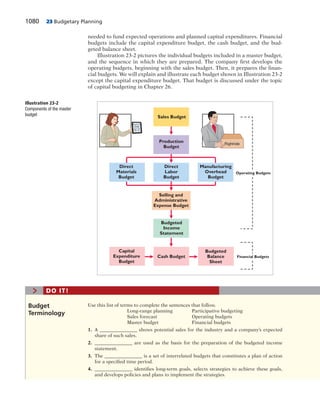

![Appendix 6A: Inventory Cost Flow Methods in Perpetual Inventory Systems 297

What inventory cost flow methods do companies employ if they use a perpetual

inventory system? Simple—they can use any of the inventory cost flow methods

described in the chapter. To illustrate the application of the three assumed cost

flow methods (FIFO, LIFO, and average-cost), we will use the data shown in Illus-

tration 6A-1 and in this chapter for Houston Electronics’ Astro condensers.

APPENDIX 6A Inventory Cost Flow Methods in Perpetual

Inventory Systems

LEARNING OBJECTIVE 7

Apply the inventory

cost flow methods to

perpetual inventory

records.

HOUSTON ELECTRONICS

Astro Condensers

Units Total Balance

Date Explanation Units Cost Cost in Units

1/1 Beginning inventory 100 $10 $ 1,000 100

4/15 Purchases 200 11 2,200 300

8/24 Purchases 300 12 3,600 600

9/10 Sale 550 50

11/27 Purchases 400 13 5,200 450

$12,000

First-In, First-Out (FIFO)

Under perpetual FIFO, the company charges to cost of goods sold the cost of the

earliest goods on hand prior to each sale. Therefore, the cost of goods sold on

September 10 consists of the units on hand January 1 and the units purchased

April 15 and August 24. Illustration 6A-2 shows the inventory under a FIFO

method perpetual system.

The ending inventory in this situation is $5,800, and the cost of goods sold is

$6,200 [(100 @ $10) 1 (200 @ $11) 1 (250 @ $12)].

Compare Illustrations 6-6 (page 283) and 6A-2. You can see that the results

under FIFO in a perpetual system are the same as in a periodic system. In both

cases, the ending inventory is $5,800 and cost of goods sold is $6,200. Regardless

of the system, the first costs in are the costs assigned to cost of goods sold.

Illustration 6A-1

Inventoriable units and costs

Balance

Date Purchases Cost of Goods Sold (in units and cost)

January 1 (100 @ $10) $ 1,000

April 15 (200 @ $11) $2,200 (100 @ $10)

(200 @ $11) $ 3,200

August 24 (300 @ $12) $3,600 (100 @ $10)

(200 @ $11) $ 6,800

(300 @ $12)

September 10 (100 @ $10)

(200 @ $11)

(250 @ $12) ( 50 @ $12) $ 600

$6,200

November 27 (400 @ $13) $5,200 ( 50 @ $12)

$5,800

(400 @ $13) Ending inventory

Cost of goods sold

⎧

⎪

⎪

⎨

⎪

⎪

⎩

⎧

⎨

⎩

⎧

⎨

⎩

⎧

⎪

⎨

⎪

⎩

Illustration 6A-2

Perpetual system—FIFO](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-321-320.jpg)

![Exercises 311

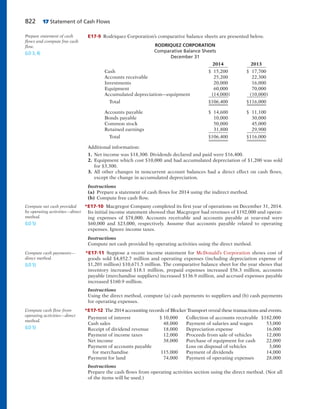

E6-13 This information is available for Quick’s Photo Corporation for 2012, 2013, and 2014.

2012 2013 2014

Beginning inventory $ 100,000 $ 300,000 $ 400,000

Ending inventory 300,000 400,000 480,000

Cost of goods sold 900,000 1,120,000 1,300,000

Sales revenue 1,200,000 1,600,000 1,900,000

Instructions

Calculate inventory turnover, days in inventory, and gross profit rate (from Chapter 5) for

Quick’s Photo Corporation for 2012, 2013, and 2014. Comment on any trends.

E6-14 The cost of goods sold computations for Alpha Company and Omega Company are

shown below.

Alpha Company Omega Company

Beginning inventory $ 45,000 $ 71,000

Cost of goods purchased 200,000 290,000

Cost of goods available for sale 245,000 361,000

Ending inventory 55,000 69,000

Cost of goods sold $190,000 $292,000

Instructions

(a) Compute inventory turnover and days in inventory for each company.

(b) Which company moves its inventory more quickly?

*E6-15 Bufford Appliance uses a perpetual inventory system. For its flat-screen television

sets, the January 1 inventory was 3 sets at $600 each. On January 10, Bufford purchased

6 units at $660 each. The company sold 2 units on January 8 and 4 units on January 15.

Instructions

Compute the ending inventory under (1) FIFO, (2) LIFO, and (3) moving-average cost.

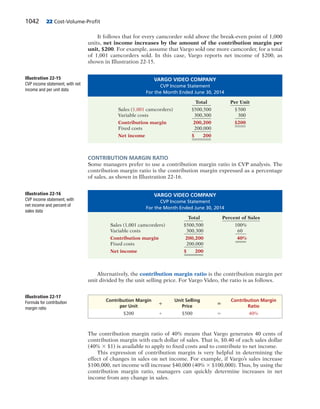

*E6-16 Kaleta Company reports the following for the month of June.

Date Explanation Units Unit Cost Total Cost

June 1 Inventory 200 $5 $1,000

12 Purchase 400 6 2,400

23 Purchase 300 7 2,100

30 Inventory 100

Instructions

(a) Calculate the cost of the ending inventory and the cost of goods sold for each cost flow

assumption, using a perpetual inventory system. Assume a sale of 440 units occurred

on June 15 for a selling price of $8 and a sale of 360 units on June 27 for $9.

(b) How do the results differ from E6-6 and E6-8?

(c) Why is the average unit cost not $6 [($5 1 $6 1 $7) 4 3 5 $6]?

*E6-17 Information about Linda’s Boards is presented in E6-4. Additional data regarding

Linda’s sales of Xpert snowboards are provided below. Assume that Linda’s uses a perpetual

inventory system.

Date Units Unit Price Total Revenue

Sept. 5 Sale 12 $199 $ 2,388

Sept. 16 Sale 50 199 9,950

Sept. 29 Sale 59 209 12,331

Totals 121 $24,669

Instructions

(a) Compute ending inventory at September 30 using FIFO, LIFO, and moving-average cost.

(b) Compare ending inventory using a perpetual inventory system to ending inventory

using a periodic inventory system (from E6-4).

(c) Which inventory cost flow method (FIFO, LIFO) gives the same ending inventory

value under both periodic and perpetual? Which method gives different ending inven-

tory values?

Compute inventory turnover,

days in inventory, and gross

profit rate.

(LO 6)

Apply cost flow methods to

perpetual records.

(LO 7)

Calculate inventory and cost

of goods sold using three cost

flow methods in a perpetual

inventory system.

(LO 7)

Apply cost flow methods to

perpetual records.

(LO 7)

Compute inventory turnover

and days in inventory.

(LO 6)](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-335-320.jpg)

![The major IFRS requirements related to accounting and reporting for inventories are the same as

GAAP. The major differences are that IFRS prohibits the use of the LIFO cost flow assumption and

determines market in the lower-of-cost-or-market inventory valuation differently.

Key Points

• The requirements for accounting for and reporting inventories are more principles-based under

IFRS. That is, GAAP provides more detailed guidelines in inventory accounting.

A Look at IFRS

324 6 Inventories

FASB Codification Activity

BYP6-9 If your school has a subscription to the FASB Codification, go to http://aaahq.org/

ascLogin.cfm to log in and prepare responses to the following.

Instructions

(a) The primary basis for accounting for inventories is cost. How is cost defined in the Codification?

(b) What does the Codification state regarding the use of consistency in the selection or employ-

ment of a basis for inventory?

(c) What does the Codification indicate is a justification for the use of the lower-of-cost-or-market

for inventory valuation?

Answers to Chapter Questions

Answers to Insight and Accounting Across the Organization Questions

p. 277 A Big Hiccup Q: What steps might the companies take to avoid such a serious disruption

in the future? A: The manufacturer of the piston rings should spread its manufacturing facilities

across a few locations that are far enough apart that they would not all be at risk at once. In addi-

tion, the automakers might consider becoming less dependent on a single supplier as well as hav-

ing weather contingency plans.

p. 278 Falsifying Inventory to Boost Income Q: What effect does an overstatement of inventory

have on a company’s financial statements? A: The balance sheet looks stronger because inventory

and retained earnings are overstated. The income statement looks better because cost of goods sold

is understated and income is overstated.

p. 289 Is LIFO Fair? Q: What are the arguments for and against the use of LIFO? A: Proponents

of LIFO argue that it is conceptually superior because it matches the most recent cost with the

most recent selling price. Critics contend that it artificially understates the company’s net income

and consequently reduces tax payments. Also, because most foreign companies are not allowed to

use LIFO, its use by U.S. companies reduces the ability of investors to compare U.S. companies

with foreign companies.

p. 293 Too Many TVs or Too Few? Q: For Sony, what are the advantages and disadvantages of

having a low days in inventory measure? A: If Sony has a low days in inventory, it reduces the

amount of cash it has tied up in inventory. It also minimizes the risk it will be stuck with excess

inventory that could force it to provide big discounts, resulting in punishing losses. Sony also faces

the risk that the TVs will become obsolete before they are sold. However, Sony increases the risk that

it will encounter “stock-outs,” that is, it will not have adequate inventory to meet customer demand.

Answers to Self-Test Questions

1. a 2. b ($180,000 1 $35,000) 3. b 4. c [(5,000 3 $13) 1 (4,000 3 $12)] 5. d [(8,000 3 $11) 1

(1,000 3 $12)] 6. d ((5,000 3 $8) 1 (15,000 3 $10) 1 (20,000 3 $12)) 4 40,000 5 $10.75; $10.75 3

7,000 7. c 8. d 9. d (200 3 $80) 10. b 11. b 12. b $285,000 4 [($80,000 1 $110,000) 4 2] 5 3;

365 4 3 13. d *14. d *15. b [$150,000 2 (30% 3 $150,000)] 5 $105,000; $135,000 2 $105,000

LEARNING OBJECTIVE 9

Compare the accounting

procedures for inventories

under GAAP and IFRS.](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-348-320.jpg)

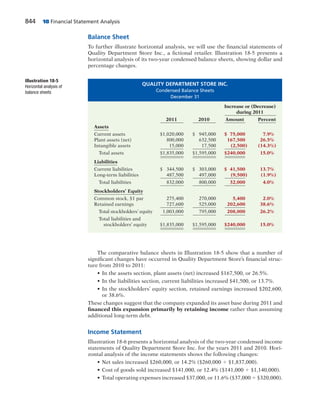

![Learning Objectives

After studying this chapter, you should be able to:

[1] Identify the basic concepts of an accounting

information system.

[2] Describe the nature and purpose of a subsidiary

ledger.

[3] Explain how companies use special journals in

journalizing.

QuickBooks®

Helps This

Retailer Sell Guitars

Starting a small business requires many decisions. For example,

you have to decide where to locate, how much space you

need, how much inventory to have, how many employees to

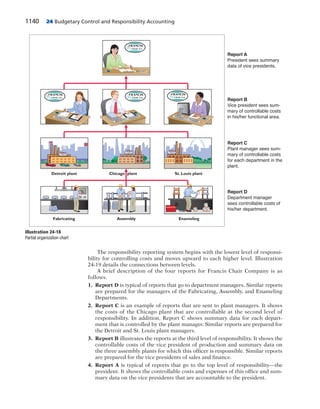

hire, and where to advertise. Small business owners are

typically so concerned about the product and sales side of

their business that they often do not give enough thought to

something that is critical to their success—how to keep track

of financial results.

Small business owners today can choose either manual or

computerized accounting systems. For example, Paul and

Laura West are the owners of the first independent dealership

of Carvin guitars and professional audio equipment. When

they founded their company, in Sacramento, California, they

decided to purchase a computerized accounting system that

would integrate many aspects of their retail operations. They

wanted to use their accounting software to manage their

inventory of guitars and amplifiers, enter sales, record and

report financial data, and process credit card and debit card

transactions. They evaluated a number of options and chose

QuickBooks®

by Intuit Inc.

QuickBooks®

, like most other popular software packages, has

programs designed for the needs of a specific business, which

in this case is retailing. This QuickBooks®

retailing package

automatically collects sales information from its point-of-sale

scanning devices. It also keeps track of inventory levels and

automatically generates purchase orders for popular items

when re-order points are reached. It even supports sales

efforts by compiling a customer database from which the

Wests send out targeted direct mailings to potential customers.

The computerized system enables data files to be emailed to

the company’s accountant. This keeps costs down and

makes it easier and more efficient to generate financial

reports as needed. The Wests believe that the investment in

the computerized system has saved them time and money,

and allowed them to spend more time on other aspects of

their business.

Source: Intuit Inc., “QuickBooks®

and ProAdvisor®

Help Make Guitar Store a

Hit,” Journal of Accountancy (May 2006), p. 101.

7 Accounting Information

Systems

Feature Story

✔ The Navigator

Scan Learning Objectives

Read Feature Story

Read Preview

Read text and answer DO IT! p. 335

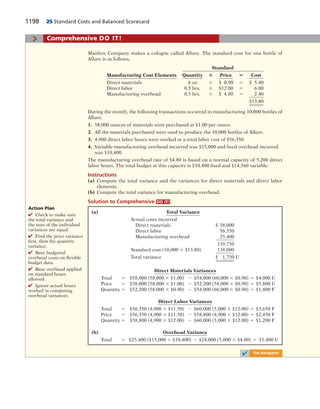

p. 348

Work Comprehensive DO IT! p. 349

Review Summary of Learning Objectives

Answer Self-Test Questions

Complete Assignments

Go to WileyPLUS for practice and tutorials

Read A Look at IFRS p. 371

✔ The Navigator

✔ The Navigator

328](https://image.slidesharecdn.com/ebookaccountingprinciples11ebyweygandtkieso-161028113436/85/E-book-accounting_principles_11_e_by_weygandt_kieso-352-320.jpg)