DTI and FICO Flowchart

•Download as PPTX, PDF•

0 likes•20 views

This document outlines qualification requirements for FHA and conventional loans based on a borrower's FICO score. For FHA loans with a 620-639 score and a housing payment, the borrower must have 12 months of on-time payments documented, a DTI below 45% or an exception for up to 50%, and payment shock below 125%. For scores of 640+ some requirements are determined by the AUS. Conventional loans require a DTI of 50% or less or an AUS approval above that. Alternative qualification options exist that allow for higher DTIs if other criteria are met.

Recommended

More Related Content

What's hot

What's hot (17)

Similar to DTI and FICO Flowchart

Similar to DTI and FICO Flowchart (20)

More from Chenoa Fund

More from Chenoa Fund (20)

Recently uploaded

Recently uploaded (20)

DTI and FICO Flowchart

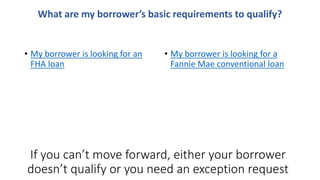

- 1. • My borrower is looking for an FHA loan • My borrower is looking for a Fannie Mae conventional loan What are my borrower’s basic requirements to qualify? If you can’t move forward, either your borrower doesn’t qualify or you need an exception request

- 2. • What is my borrower’s FICO range? • 620–639 • 640–659 • 660+ Go Back FHA DTI Ranges

- 3. • My borrower has… • A present housing payment (verifiable 12 months or more) • No present housing payment (or less than 12 months verifiable) Go Back FHA: 620–639 FICO (Housing Payment Options)

- 4. • Requirements: • Verification of twelve (12) months of current housing expense required; a traditional VOR is acceptable. If the borrower rents from a relative or individual (anyone other than an LLC or management company), then twelve (12) months of cancelled checks or bank statements are required to document payment history. See section 5.17 for more information • HBE required • Payment shock of 125% or less • DTI of 45% or less • But my borrower’s DTI is above 45% and is equal to or lower than 50%... • But my borrower exceeds those payment shock guidelines… FHA: 620—639 (With Housing Payment) Go Back

- 5. • Requirements: • VOR documenting no housing payment • HBE required • Maximum DTI 31% front-end and 45% backend; never to exceed 45% backend DTI • Three (3) months PITI reserves • Minimum two (2) years with present employer • Meet VA Residual Income requirements • There are no alternative qualification guidelines for this FICO band FHA: 620–639 (No Housing Payment) Go Back

- 6. • Requirements: • Verification of amount of current housing expense required (even if borrower has no housing payments); a payment history is not required • DTI of 50% or less • But my borrower exceeds those DTI requirements, and AUS approves above 50%... FHA: 640–659 FICO Go Back

- 7. • Requirements: • DTI ratio per AUS findings • Please note: a letter of explanation will be required if the borrower has no housing payment to report on the 1003 FHA: 660+ FICO Go Back • There are no alternative qualification guidelines for this FICO band

- 8. • What is my borrower’s FICO score range? • 640–659 • 660+ Go Back Conventional: DTI Ranges

- 9. • Requirements: • DTI 50% or less • But my borrower exceeds those DTI requirements, and AUS approves above 50%... Go Back Conventional: 640–659 FICO

- 10. • Requirements • DTI per AUS findings • There are no alternative qualification guidelines for this FICO band Go Back Conventional: 660+ FICO

- 11. Select one option from both categories • Two (2) years employed with the current employer OR • Two (2) months PITI reserves • A maximum DTI 31% frontend OR • Meets VA Residual Income Tests Go Back You do not need to make an exception request for these requirements. These requirements are in addition to the other requirements in your borrower’s FICO band, except for the specific DTI or payment shock requirement being excepted. Category 1 Category 2 Alternative Qualification Requirements