Download to read offline

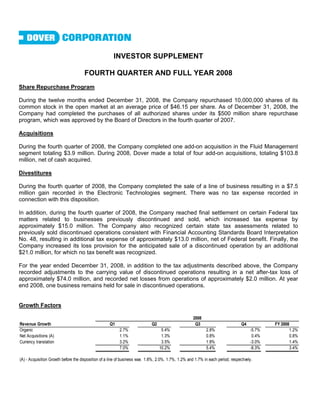

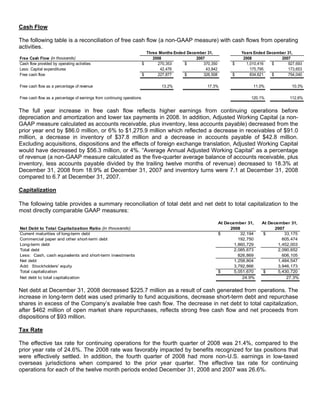

During the fourth quarter of 2008: - The company repurchased 10 million shares at an average price of $46.15 per share, completing its $500 million share repurchase program. - It acquired one company for $3.9 million to boost its Fluid Management segment. - It sold a line of business for a $7.5 million gain in its Electronic Technologies segment. - It incurred tax expenses of $28 million related to prior tax matters and discontinued operations.