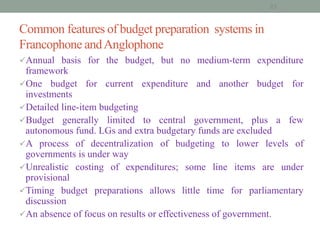

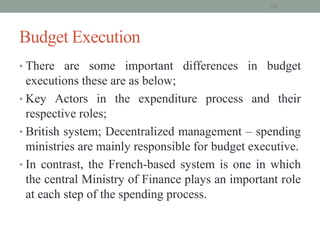

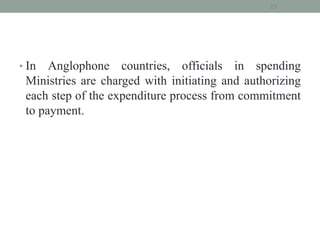

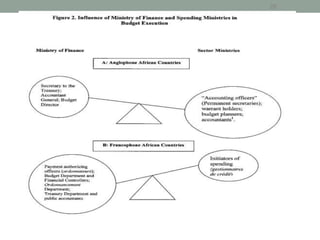

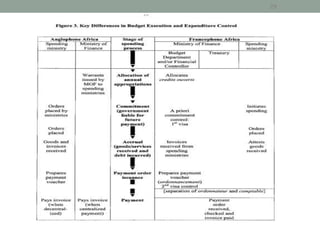

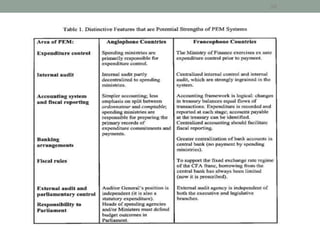

The document discusses public expenditure management (PEM) systems, highlighting the importance of aligning government spending with revenues and achieving desired social outcomes. It contrasts the French-based and British-based PEM systems, detailing their budget preparation and execution processes, as well as the respective roles of finance ministries. Key differences include governance structures, delegation of responsibilities, and the emphasis on prepayment controls in French systems versus the reliance on external audits in British systems.