Download to read offline

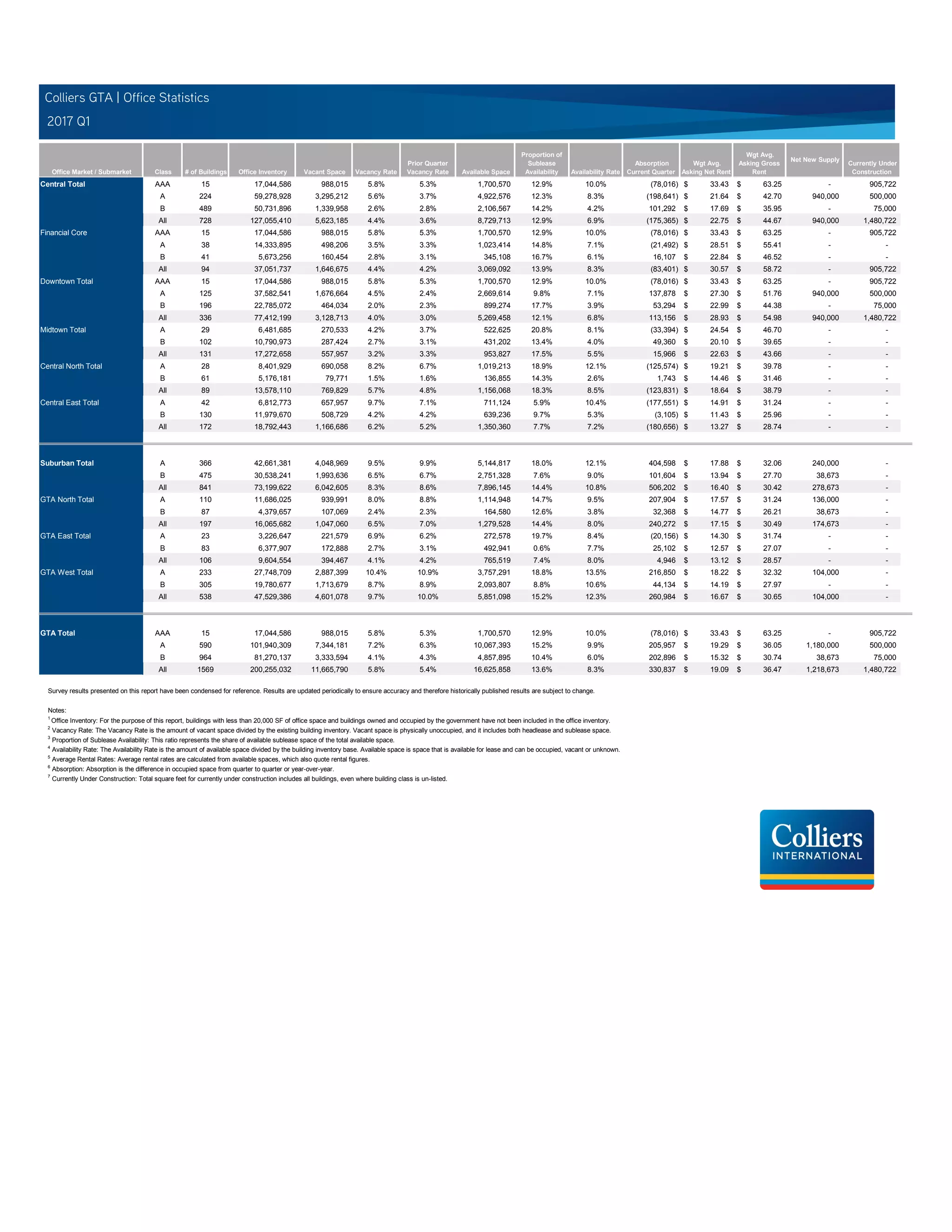

This document provides an overview of office market statistics for various submarkets in the Greater Toronto Area (GTA) for the first quarter of 2017. Key metrics reported include number of buildings, total office inventory, vacant space, vacancy rates, available space, absorption rates, and average asking rental rates. The Financial Core submarket had 94 buildings totaling 37 million square feet of office inventory, with a vacancy rate of 4.4% and average asking gross rent of $58.72 per square foot.