1. Brilliance Auto

HK$12.22 - BUY

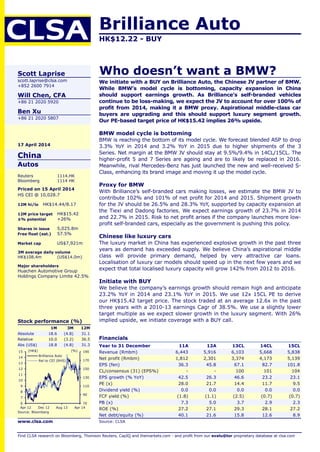

Financials

Year to 31 December 11A 12A 13CL 14CL 15CL

Revenue (Rmbm) 6,443 5,916 6,103 5,668 5,838

Net profit (Rmbm) 1,812 2,301 3,374 4,173 5,139

EPS (fen) 36.3 45.8 67.1 82.7 101.8

CL/consensus (31) (EPS%) - - 100 101 104

EPS growth (% YoY) 42.5 26.3 46.6 23.2 23.1

PE (x) 28.0 21.7 14.4 11.7 9.5

Dividend yield (%) 0.0 0.0 0.0 0.0 0.0

FCF yield (%) (1.8) (1.1) (2.5) (0.7) (0.7)

PB (x) 7.3 5.0 3.7 2.9 2.3

ROE (%) 27.2 27.1 29.3 28.1 27.2

Net debt/equity (%) 40.1 21.6 15.8 12.6 8.9

Source: CLSA

Find CLSA research on Bloomberg, Thomson Reuters, CapIQ and themarkets.com - and profit from our evalu@tor proprietary database at clsa.com

Scott Laprise

scott.laprise@clsa.com

+852 2600 7914

Will Chen, CFA

+86 21 2020 5920

Ben Xu

+86 21 2020 5807

17 April 2014

China

Autos

Reuters 1114.HK

Bloomberg 1114 HK

Priced on 15 April 2014

HS CEI @ 10,028.7

12M hi/lo HK$14.44/8.17

12M price target HK$15.42

±% potential +26%

Shares in issue 5,025.8m

Free float (est.) 57.5%

Market cap US$7,921m

3M average daily volume

HK$108.4m (US$14.0m)

Major shareholders

Huachen Automotive Group

Holdings Company Limite 42.5%

Stock performance (%)

1M 3M 12M

Absolute 18.6 (4.8) 31.1

Relative 10.0 (3.2) 36.5

Abs (US$) 18.8 (4.8) 31.3

Source: Bloomberg

www.clsa.com

70

90

110

130

150

170

190

6

7

8

9

10

11

12

13

14

15

Apr 12 Dec 12 Aug 13 Apr 14

Brilliance Auto

Rel to CEI (RHS)

(HK$) (%)

Who doesn’t want a BMW?

We initiate with a BUY on Brilliance Auto, the Chinese JV partner of BMW.

While BMW’s model cycle is bottoming, capacity expansion in China

should support earnings growth. As Brilliance’s self-branded vehicles

continue to be loss-making, we expect the JV to account for over 100% of

profit from 2014, making it a BMW proxy. Aspirational middle-class car

buyers are upgrading and this should support luxury segment growth.

Our PE-based target price of HK$15.42 implies 26% upside.

BMW model cycle is bottoming

BMW is reaching the bottom of its model cycle. We forecast blended ASP to drop

3.3% YoY in 2014 and 3.2% YoY in 2015 due to higher shipments of the 3

Series. Net margin at the BMW JV should stay at 9.5%/9.4% in 14CL/15CL. The

higher-profit 5 and 7 Series are ageing and are to likely be replaced in 2016.

Meanwhile, rival Mercedes-Benz has just launched the new and well-received S-

Class, enhancing its brand image and moving it up the model cycle.

Proxy for BMW

With Brilliance’s self-branded cars making losses, we estimate the BMW JV to

contribute 102% and 101% of net profit for 2014 and 2015. Shipment growth

for the JV should be 26.5% and 28.3% YoY, supported by capacity expansion at

the Tiexi and Dadong factories. We expect earnings growth of 23.7% in 2014

and 22.7% in 2015. Risk to net profit arises if the company launches more low-

profit self-branded cars, especially as the government is pushing this policy.

Chinese like luxury cars

The luxury market in China has experienced explosive growth in the past three

years as demand has exceeded supply. We believe China’s aspirational middle

class will provide primary demand, helped by very attractive car loans.

Localisation of luxury car models should speed up in the next few years and we

expect that total localised luxury capacity will grow 142% from 2012 to 2016.

Initiate with BUY

We believe the company’s earnings growth should remain high and anticipate

23.2% YoY in 2014 and 23.1% YoY in 2015. We use 12x 15CL PE to derive

our HK$15.42 target price. The stock traded at an average 12.6x in the past

three years with a 2010-13 earnings Cagr of 38.5%. We use a slightly lower

target multiple as we expect slower growth in the luxury segment. With 26%

implied upside, we initiate coverage with a BUY call.

2. Brilliance Auto - BUY

2 scott.laprise@clsa.com 17 April 2014

Brilliance Auto - HK$12.22 - BUY

The business Competition & market franchise

In 2003, Brilliance started its JV with BMW to produce localised

BMW models, including the 3 Series, 5 Series and X1. The JV is

the primary profit contributor, accounting for 102% of Brilliance’s

total profit in 2013. Sales of the company’s self-branded business,

Jinbei Minibus, remain weak and should be close to breakeven in

the next two years. We believe this is a reflection of Brilliance’s

car-making capability, which has to date not been very

successful. In the next three years, we don’t expect to see any

significant change from its self-brand minibus and forecast sales

of 77,000 and 79,000 units in 2014 and 2015.

Brilliance owns 51% of Shenyang Automotive (SYA), China's

largest minibus producer. The company has diverted it focus

from minibus as its core Hiase brand saw lower market share

in 2013. Its self-brand recorded an operating loss of Rmb24m

in 2012 and Rmb61m in 2013, due to slowing shipments. Its

JV business will benefit from BMW localisation. We forecast

shipment growth for BMW Brilliance at 26.5% YoY for 2014

and 28.3% YoY for 2015, mainly supported by capacity

expansion at its Tiexi and Dadong factories.

Valuation history

PE bands PB bands

Brilliance is trading at 11.5x 12-

month forward PE, below its

average of 12.6x in the past

three years and 13.9% higher

than the -1sd level. The

company is also trading at 2.9x

forward PB, which is lower than

its average of 3.1x in the past

three years and 13.7% higher

than the -1sd level.

Bands (from the top): max, +1sd, avg, -1sd, min

Target-price sensitivity

Our blue-sky value of HK$17.9

assumes BMW shipment

growth at 13.9% and 28.3%

YoY in 14CL and 15CL, with a

blended ASP rising 0.2% YoY

in 14CL and falling 3.2% YoY

in 15CL.

Our target price of HK$15.42

assumes 26.5% and 28.3%

BMW shipment growth in 14CL

and 15CL, with a blended ASP

YoY decline of 3.3% and 3.2%

over the two years.

Our rainy day value assumes

BMW shipment growth of

39.2% and 28.3% YoY in 14CL

and 15CL, with blended ASP

falling 7.6% and 3.2% YoY

over the two years.

Source: CLSA

2.1x

6.5x

10.9x

15.2x

19.5x

1

2

4

9

21

Apr 09 Apr 10 Apr 11 Apr 12 Apr 13 Apr 14

log (HK$)

0.4x

1.5x

2.6x

3.7x

4.7x

1

2

4

9

21

Apr 09 Apr 10 Apr 11 Apr 12 Apr 13 Apr 14

log (HK$)

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

Apr 11 Oct 11 Apr 12 Oct 12 Apr 13 Oct 13 Apr 14 Oct 14 Apr 15

Share price Target price

Blue sky Rainy day

(HK$)

10.2

17.9

15.4

3. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 3

BMW model cycle is bottoming

We forecast blended ASP for BMW to decline by 3.3% and 3.2% YoY in 2014

and 2015 due to higher shipments of the 3 Series. Net margin of the

Brilliance-BMW JV will stay at 9.5%/9.4% in 14CL/15CL. The higher-profit

5 and 7 Series are ageing and are likely to be replaced in 2016. Meanwhile,

rival Mercedes-Benz has just launched its new and well-received S-Class,

enhancing its overall brand image and moving it up the model cycle.

BMW-Brilliance joint venture

Brilliance China was established in 1992 and listed on the Hong Kong

exchange in 1999. In 2002, Brilliance started its joint venture with BMW

forming BMW Brilliance Automotive to produce localised BMW models. Models

include: the 3 Series, 5 Series and X1. One unfortunate issue for investors is

that BMW-related profit is added in at the JCE line, which means an equity

gain method of accounting. We therefore have very little data or insight into

the primary profit driver of the company, as it does not need to report any

financial details such as revenue, gross profit or cost items.

For 2013, Brilliance made net profit attributable to equity holders of

Rmb3,374m, or 46.6% YoY growth. Meanwhile, the JV income from BMW

Brilliance was Rmb3,829m, or 64% YoY growth. The JV is the primary profit

driver for the company. In 14CL, we expect income from the JV to be about

102% of total net income.

We have not factored in any exports of the 3 Series and 5 Series to other

markets, especially within Asia or the Middle East, as we expect the company

to focus its car sales within China. However, should sales slow dramatically,

the company may utilise this option as the longer version of these cars are in

high demand in some of these markets, particularly where consumers

commonly use a driver. There is little incentive to export as BMW would need

to share 50% of the profits with Brilliance, which it currently doesn’t have to

when it ships cars from Germany.

Figure 1 Figure 2 Figure 3

BMW Brilliance 3 Series BMW Brilliance 5 Series BMW Brilliance X1 SUV

Source: BMW China

Brilliance began to make vehicles in 1994. The company also had a pre-2010,

self-branded business that made losses. What we mean by self-branded is the

vehicles were 100% manufactured by Brilliance (Chinese-made domestic cars)

and not the cars in the JV with BMW. BMW Brilliance started to produce

localised BMW models from 2003, choosing what was thought to be a weaker

Chinese partner giving it the potential for more control of the JV. It was a

difficult decision for BMW to make cars in China as this had the potential to hurt

the brand image. A debate at BMW fuelled by worries that the government

might put in even higher import duties was the main reason to bring its high-

Brilliance has become

a proxy for BMW’s

China business

In 2009, the money-

losing self-brand

Zhonghua sedan was sold

back to the group

BMW details are reported

as an equity gain providing

few financial details

We have not factored in

any exports from China to

other markets

BMW decision to produce

in China driven by fears of

import taxes

Expect ASP decline on

higher shipments

JV income from BMW

Brilliance should make up

102% of total net income

4. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

4 scott.laprise@clsa.com 17 April 2014

volume cars to China. Audi had even earlier made this decision though that was

driven more by trying to sell cars to the government as officials could only buy

“Made in China” cars. We believe this was the wrong decision made by the

luxury carmakers as it would have been able to have higher profits from

imported cars and an even better brand image. We don’t believe that higher

taxes would have been imposed as the volume of cars was not so big and the

end user often is a government official. But the worry about long-term future

and the fact competitors were likely to produce locally drove their decision.

BMW has very few production facilities outside of Germany with an SUV plant in

the USA and small production of its 3 Series in South Africa.

Before 2009, Brilliance had two self-brands - Jinbei minibus and Zhonghua

sedans. At the end of 2009, Brilliance China changed the focus of the listed

company to an almost pure play on the BMW JV after it sold the money-losing

Zhonghua business back to the group company. This was an excellent solution

as BMW needed to plan a new factory but Brilliance did not have the money

and was worried BMW might want to start a new JV with another Chinese

partner. Selling the self-branded cars business to the parent gave it an

opportunity. At the same time, BMW started to look around at other JVs with

potential partners like SAIC. Other carmakers wanted to form a JV with BMW,

but with the high-volume 3 and 5 Series locked up with Brilliance, there was

not much left for a new JV.

Today, the self-branded business is Jinbei minibus, which saw weak sales in

1H13, shipping 34,000 buses with revenue of Rmb2,572m, a decline of 8.4%

YoY and a net loss of Rmb67m (excluding the Brilliance JV income), compared

to a Rmb22m profit and Rmb46m loss in 1H13 and 2H13. We believe this is a

reflection of the carmaking capability of Brilliance, which has to date not been

very successful.

Figure 4

BMW 2013 shipments and production in China compared with total passenger car sales

Brand Production Sales

Dec

2013

Jan-Dec

2013

Jan-Dec

2012

% Change Dec

2013

Jan-Dec

2013

Jan-Dec

2012

% Change

Prior

month

YTD Prior

month

YTD

Total PV 1,165,912 12,100,772 10,767,380 (0.79) 12.38 1,175,565 12,009,704 10,744,740 4.24 11.77

BMW 3 Series 8,053 62,598 25,354 13.9 146.9 5,368 61,213 20,794 3.43 194.38

BMW 5 Series 10,545 126,888 103,517 (9.71) 22.58 9,807 123,852 105,939 8.26 16.91

BMW M12 42 55 0 * * 0 0 0 * *

Total 18,640 189,541 128,871 (0.58) 47.08 15,175 185,065 126,733 6.5 46.03

Source: CAAM

Figure 5 Figure 6

Jinbei minibus Haishi Zhonghua sedan

Source: Company website

Brilliance had to sell its

self-branded car business

5. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 5

Brilliance China owns 51% of Shenyang Automotive (SYA), the country's

largest minibus producer. Its core Hiase minibus brand (known as Hiace

outside China) lost market share from 43,000 units in 2012 to 36,900 units in

2013. The vehicle is built with a quality Toyota engine but proved more costly

than cheaper Chinese competitors.

Figure 7

Company share structure

Source: Company disclosure. Xingyuandong makes auto parts. Jingbei Auto owns 49% of Shenyang Auto.

Huachen Automotive

Group Holdings

Individuals Liaoning Province

0.4% 99.6%

Brilliance China Automobile

Holdings Limited (1114 HK)

Public shareholders

42.5% 57.5%

Xingyuandong Shenyang Automotive Brilliance BMW

100% 51% 50%

Self-brand loses money

and we don’t expect this

to change anytime soon

50% share in JV with

BMW and 51% in

Shenyang Automotive

6. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

6 scott.laprise@clsa.com 17 April 2014

Company history: Over 64 years

Figure 8

Brilliance Auto history

Year Event

1949 Brilliance China Automotive Holdings Limited was founded.

1991 Shenyang Jinbei Car Maker was founded, one of the carmakers of Brilliance China Automotive Holdings Limited.

1992 Becomes first Chinese car company to be listed on a foreign stock exchange; it went public on the NYSE, in 1992. It was

incorporated in Bermuda. When it was first listed, it was one of the most active stocks on the exchange. Toyota sent

engineers to the company to train personnel.

1995 The first Chinese automotive company to pass the ISO 9000 quality assurance programme. At this time the Toyota

agreement expired, but the company was well on its way.

1996 The name was changed to Shenyang Brilliance Jinbei Automobile with a registered capital of US$444m. It launched a

mid-priced minibus which is their main product even today.

1998 The company bought a 51% indirect equity interest in Ningbo Yuming, which produces car windows, moulding and

stripping. It also bought a 50% indirect interest in Miayang Xinchen, which produces petrol engines for passenger

vehicles and light duty trucks. It also formed Xing Yuan Dong, a fully owned subsidiary, to consolidate the purchasing

and sourcing of spares parts.

1999 The company went public on the Hong Kong stock exchange. It also acquired a 16% equity stake in Shenyang

Aerospace, a joint venture company with Mitsubishi that manufactures Mitsubishi gasoline engines.

2000 Established Ningbo Brilliance Ruixing, a fully owned subsidiary to organise trading, and development of auto parts for Ningbo

Yuming. It also formed Mianyang Brilliance Ruian and a subsidiary company, also developing auto parts for Mianyang Xinchen.

It acquired a 50% equity interest in Shenyang Xinguang, making gasoline engines for passenger vehicles.

2001 Entered into an assistance agreement with BMW for technical support, and training to help them produce the Zhonghua

sedan. The company acquired a 100% equity interest in Dongxing, making automotive components.

2002 Entered into a joint venture with BMW. The Zhonghua sedan was launched.

2003 The company owns a research and design centre with 499 people. There were two doctors and 33 with a Master’s degree

and the rest technical personnel. The main purpose was to improve the company’s products, such as its cars, data

management system and testing. It also began producing BMW 3 and 5 Series, and launched the Jinbei minibus.

Today The company has 159 related companies, 14 of which are solely owned, 125 are ventures or holding companies, and 20

joint operating enterprises, with total assets of Rmb300bn. The company makes auto parts and components, including

window stripping. mouldings, seats, axles, safety and airbag systems, interior finishings, and engines for passenger cars,

minibuses, sport utility vehicles, and light duty trucks.

Source: Company

Figure 9

Brilliance historical price

Source: Winds

0

2

4

6

8

10

12

14

16

Oct 99 Mar 02 Aug 04 Dec 06 May 09 Oct 11 Feb 14

(HK$)

Brilliance share price

jumped after the sale of

the self-branded cars

back to parent

7. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 7

Brilliance and the BMW JV contract

Foreign auto companies coming into China are required to set up joint

ventures if they want to manufacture vehicles in China. While in many other

sectors a JV is preferable to help get through red tape and establish

relationships or “guanxi”, the main purpose of an auto JV is to try and help

Chinese partners learn how to build quality cars. The auto sector system of

JVs is to give the Chinese partner relatively easy access to profits to fund

their own car production as well as learn how to make cars.

Profit, loss, and risk are shared to the contribution of registered capital of the

JV partners. The contract is set up in both English and Chinese equally, being

valid in accordance with the Law of the People’s Republic of China on Sino-

Foreign Equity Joint Ventures. Interestingly, almost all the business contracts

we have ever encountered are only valid using the Chinese version and the

English version is only provided as an aid.

The JV contract with BMW Brilliance Automotive Limited (BBA) was formed on

27 March, 2003. The JV partners are BMW Holding, a 100% subsidiary of

BMW AG, which is located in the Netherlands, and the Shenyang JinBei

Automotive Industry Holdings Company (Brilliance) located in China, with

both holding a 50% stake.

The Brilliance stake is with Brilliance China Automotive Holdings Limited

holding a 40.5% stake and the Shenyang municipal government holding a

9.5% stake. The Chinese-German 50:50 partners both agreed to initially

invest €450m by 2005 with registered capital of €150m, which was later

increased.

The partner’s general terms and business activities are defined in the first

paragraphs of the JV contract, with initially six engine-variants of the 3 Series

and five engine-variants of the 5 Series and at the start 30,000 passenger

cars in total. Of course the contract has some flexibility built in, such as being

able to add new products down the road. The company planned in the

contract to possibly export cars abroad and to establish international

branches and a distribution and sales branch in Beijing was already regulated.

Figure 10

BMW Brilliance car models

Car line Body variance Model Engine code Engine capacity Cyl. Gearbox Designation

E46 4 door limousine 318i N42B20 2.0 L 4 Automatic 318i limousine

E90 4 door limousine 318i N46B20 2.0 L 4 Automatic 318i limousine

E46 4 door limousine 320i M54B22 2.2 L 6 Automatic 320i limousine

E90 4 door limousine 320i N52B22 2.2 L 6 Automatic 320i limousine

E46 4 door limousine 325i M54B25 2.5 L 6 Automatic 325i limousine

E90 4 door limousine 325i N52B25 2.5 L 6 Automatic 325i limousine

E60 4 door limousine 520i M54B22 2.2 L 6 Automatic 520i limousine

E60 4 door limousine 520i N52B22 2.2 L 6 Automatic 520i limousine

E60 4 door limousine 525i M54B25 2.5 L 6 Automatic 525i limousine

E60 4 door limousine 525i N52B25 2.5 L 6 Automatic 525i limousine

E60 4 door limousine 530i M54B30 3.0 L 6 Automatic 530i limousine

E60 4 door limousine 530i N52B30 3.0 L 6 Automatic 530i limousine

Source: BMW Brilliance

Must have a JV for all

foreign auto companies

BMW ownership is held

out of the Netherlands

The contract does allow

exporting of cars out of

China though we have not

forecast any exports

8. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

8 scott.laprise@clsa.com 17 April 2014

The business scope is the production of BMW passenger cars, engines, parts

and components, and accessories. The company can sell products produced

and provide after-sales services, including spare parts. From the contract:

4.2 Business Scope

4.2.1 The business scope of the JV Company shall be to produce BMW

passenger cars, engines, parts and components, and accessories

therefore; to sell the products produced by itself; and to provide after-

sales services (including spare parts) in connection with its products.

4.2.2 The JV Company also will conduct all business activities necessary for or

ancillary to the activities listed in Article 4.2.1 including, but not limited to,

industrial, engineering, commercial, financial, marketing, financial

services, and training activities.

The contract was set up for the years 2003 to 2010, with the business plan to

be renewed for a six-year period. A management by deviation approach is

followed with benchmark figures set for the budget and an accepted

difference of 15% and for return on sales of 5%.

Board of directors composition

The board of directors of BBA was initially composed of 13 directors, six

appointed by the two parties and one independent director, first nominated by

BMW and then mutually appointed by the parties. After three years, the board

of directors in the JV contract agreed to be reduced to seven directors, each

party appointing three and one independent, not employed by BMW. If the

ownership structure changes then the allocation will change as well.

Staff appointments

The JV’s general manager reports to the board of directors bi-annually and as

needed. The GM needs to report on finances, major dealings and transactions,

problems and important matters materially affecting the business, and the

budget. Typically for a JV, also in the case of BBA, the chairman of the board is

appointed by Brilliance, whereas the vice-chairman is appointed by BMW. Both

are appointed for three years and can be reappointed.

The general manager as well as the deputy general managers for the

departments’ sales and manufacturing are nominated by BMW and then

appointed by the board, as is common in Sino-Foreign JVs.

Brilliance nominates the deputy general manager for the finance department. For

human resources the nomination is done by both. Qualifications for all appointed

persons include professional qualifications, substantial experience in their field,

and ability to speak English, as this is the working language of the JV at least at

a senior corporate level. This is a common issue in a JV, communication. Day-to-

day activities are conducted in Chinese, but it seems like they must have a lot of

translating to do at the senior level as it is unlikely they can all speak English.

Roles of both parties in the JV

Brilliance

Apply for loans

Helps to localise the product

Procure fiscal, administrative, customs, and tax-related services

Recruitment, and transportation of imported equipment

Provide the site and infrastructure

The company can produce

cars, components, sell

and provide service

The contract is renewable

every six years

Board of directors has

seven members

Chairman appointed by

Brilliance, whereas the

vice-chairman is

appointed by BMW

Surprisingly English is the

working language of the

JV at least at a senior

corporate level

Roles of the parties

clearly defined

9. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 9

BMW

Assists with the purchasing of material and equipment

Training of employees

Localised parts and components development

Set up of the production site and existing buildings and equipment

Technology transfer, licensing certain technology, management and

operational know-how required for the JV over a time of 15 years

Further agreements in the JV

Brilliance assures to not use any of the technology or process knowledge

transferred. This seems to me to be contrary to the purpose of a Chinese

automotive JV. Brilliance products are not to be marketed in competition with

the JV products. While improvements are allowed, the appearance of the

Brilliance cars is not allowed to be adapted from BMW cars. Definitely

previous models of the Zhonghua cars (those models sold back to the parent

in late 2009) looked like BMWs. One of the first times we went to the factory

and walked through the parking lot and saw the cars from the rear, we had

difficulty distinguishing Zhonghua sedans from the BMWs.

The quality of the JV products is agreed to meet BMW standards and when we

talked with the company it said the quality level is exactly the same as cars

made in Germany. We also spoken to Daimler on this issue and management

there told us that this was one of the biggest mistakes the company had

made. The company wishes it spent more time explaining to consumers that

the product made in China is exactly the same as the one made in Germany.

While the model and options may vary, product quality is the same.

Consumers in China still believe the best cars are imported cars and that a

car made in China is inferior, but this is slowly changing. It is also agreed to

not vary retail prices by more than 5%. Importing products also made in the

JV is only allowed up to 5% of the produced volume of the JV in case of

competition of the similar products.

How does the contract renewal occur

In the past, when contracts were renewed, the Chinese partners still had

limited bargaining power and were also worried about adding more terms in

the contract when talking with the OEM. Making profit from the JV is more

important for the Chinese partner. But we should expect to see more

additions in future contracts, which benefit the Chinese partner when we have

future renewals. This is due to:

1) Poor overseas markets and more reliance on China.

2) More bargaining power from the Chinese side. We are seeing this now in

the negotiations between PSA and Dongfeng.

Interestingly, Brilliance’s CEO Qi Yuming was quoted with an interesting idea

last year, wanting the government to set a price ceiling of Rmb150,000 for

any car a foreign JV partner wanted to sell in China. We might see the

Chinese partner adding this term into the contract.

How could the contract terminate

The best example of a termination is the Nanjing Fiat case. The main reasons

for the Fiat JV contract termination was due to weak sales of the JV models

and Fiat was not happy. So the company started to look for other JV partners

and has since hooked up with Guangzhou Auto Group Company (GAC).

Another termination was PSA, previously the JV partner with GAC but that

Appearance of BMW

cars is not allowed

to be copied

Contract renewals could

change in the future

Proposal to limit car

ASP from JVs

There have been

contract terminations

in the past in China

We believe the quality

of a BMW made in

China vs Germany

are almost identical

10. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

10 scott.laprise@clsa.com 17 April 2014

venture ended in 1996 and PSA signed a new venture with Dongfeng Auto.

The company was with GAC for about 11 years, made only about 100,000

cars but the French company did not want to localise car-part production in

China. Also the French had the view of only introducing old models with old

technologies and in the end GAC wanted to end the relationship.

Termination can occur when: sales are not good; either party is unhappy

about cooperation; or leaves the Chinese market (low possibility).

Brilliance is all about BMW

While most Chinese carmakers are trying to introduce their own self-branded

cars within the structure of their JVs, Brilliance changed back in 2009 and is

using the old SOE structure. Domestic cars are made mainly in the group

company and BMWs in the listed company. The government initially set up

JVs to make the self-branded cars within the JVs so it is interesting to see the

company continue to be allowed to work this way. We don’t believe this

structure will last unless the central government changes its view on the auto

JV policy. But by keeping some small minibus production and investing in

electric vehicles, the company seems to be doing enough to keep Beijing

satisfied, at least for the time being.

Figure 11

Major BMW, Benz and Audi product cycle

Source: CLSA

2005 2006 2007 2008 2009 2010 2011 2012 2013 14CL 15CL 16CL

Benz

C-Class New version New version

E-Class New version New version

S-Class New version New version

GLK First launch New version

BMW

3 Series New version New version

5 Series New version New version

New

version

7 Series New version New version

X1 First launch New version

I3

I3 EV

launch

I8 EV

launch

Zinoro First launch

Audi

A4 New version

A6 New version New version

A8 New version

Q3 New version

Q5 First launch

Brilliance removed most

self-brands from their JV

11. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 11

Financial details cover self-branded business

We need to highlight that the financial details from the company are very

limited as the JV profits are accounted for by equity gain, a structure

becoming more common and providing little insight into the company. When

we look at financial highlights for the company in the chart below, the detail is

derived from the self-branded car business and not the BMW JV.

Even though the purpose of the company is to make its own self-branded

cars, it has not been able to successfully make any new cars in the JV. Its

self-brand recorded an operating loss of Rmb57m in 2012 and a loss of

Rmb178m in 2013 due to slowing shipments this year. We only forecast mini-

bus shipments of 75,000 units in 13CL, or a decline of 9% YoY.

In the next three years, we don’t expect to see any significant change from

its self-brand minibus and we forecast 77,309 units and 79,628 units, in 2014

and 2015, considering no significant new models, no competitive advantage

in technology or features.

Figure 12

Key financial highlights only represent self-branded cars and not BMW JV

(Rmbm) 1H13 2H13 2013 1H14CL 2H14CL 14CL 1H15CL 2H15CL 15CL

Revenue 2,572 3,531 6,103 2,649 3,019 5,668 2,728 3,110 5,838

Cost of sales (2,296) (3,121) (5,417) (2,365) (2,726) (5,090) (2,435) (2,807) (5,243)

Gross profit 276 411 687 284 294 578 293 303 595

Other net income 11 85 96 12 30 42 12 31 43

Interest income 24 23 47 25 30 55 25 31 56

Selling & distribution expenses (246) (362) (608) (189) (329) (518) (195) (339) (534)

Administrative expenses (195) (204) (399) (160) (165) (324) (164) (170) (334)

Ebitda (61) 25 (36) 89 (22) 67 98 (17) 81

Operating profit (130) (48) (178) (28) (139) (168) (29) (144) (173)

Finance costs (70) (68) (139) (87) (87) (175) (94) (94) (188)

Share of associates 97 96 193 97 97 193 97 97 193

Share of JCEs 2,105 1,343 3,448 2,081 2,209 4,290 2,534 2,740 5,274

Impairment losses on assets 0 0 0 0 0 0 0 0 0

PBT 2,002 1,323 3,325 2,062 2,079 4,140 2,507 2,600 5,107

Income tax (expense) credit (2) (6) (8) 0 (2) (2) 0 (2) (2)

PAT 2,000 1,317 3,316 2,062 2,076 4,138 2,507 2,597 5,105

Loss for the year from

discontinued operations

0 0 0 0 0 0 0 0 0

Minority interest 30 28 58 (0) 35 35 (1) 35 34

Net profit 2,030 1,344 3,374 2,062 2,111 4,173 2,506 2,632 5,139

Depreciation & amortization 69 73 143 117 117 235 127 127 254

Share base - Basic (m) 5,026 5,026 5,026 5,046 5,046 5,046 5,046 5,046 5,046

Share base - Diluted (m) 5,046 5,046 5,046 5,046 5,046 5,046 5,046 5,046 5,046

Basic EPS (Rmb) 0.404 0.267 0.671 0.409 0.418 0.827 0.497 0.522 1.018

Margins (%)

Gross margin 10.7 11.6 11.2 10.7 9.7 10.2 10.7 9.7 10.2

Other net income 0.1 0.1 1.6 0.1 0.1 0.7 0.1 0.1 0.7

Interest income 0.0 0.0 0.8 0.0 0.0 1.0 0.0 0.0 1.0

Selling & distribution expenses (9.6) (10.3) (10.0) (2.0) (2.5) (9.1) (2.0) (2.5) (9.1)

Administrative expenses (2.0) (2.4) (6.5) (2.0) (2.4) (5.7) (2.0) (2.4) (5.7)

Ebitda margin (2.4) 0.7 (0.6) 3.4 (0.7) 1.2 3.6 (0.5) 1.4

Operating margin (5.1) (1.4) (2.9) (1.1) (4.6) (3.0) (1.1) (4.6) (3.0)

PBT margin 77.8 37.5 54.5 77.8 68.8 73.0 91.9 83.6 87.5

Effective Tax rate 25.0 25.0 0.3 25.0 25.0 0.1 25.0 25.0 0.0

PAT margin 77.7 37.3 54.3 77.8 68.8 73.0 91.9 83.5 87.4

Net margin 78.9 38.1 55.3 77.8 69.9 73.6 91.9 84.7 88.0

Source: Company, CLSA (JCE - Joint controlled entities, BMW makes 99% of this income)

Self-brand mini-bus

business is shrinking and

loss-making . . .

. . . and we are bearish

on its minibus business in

the next three years

12. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

12 scott.laprise@clsa.com 17 April 2014

We highlight that the above financials table is not helpful to investor since the

key profit driver, BMW income, is treated as an equity gain. In addition, there

is limited information about the JV business provided by Brilliance China,

which means there is low visibility within the company to BMW. The BMW JV

profits are reported under the share of joint controlled entities (JCEs).

Figure 13 Figure 14

Self-brand net profit likely a small loss in next few years No significant change expected for self-branded cars

Figure 15

Self-brands should still make a loss in the next three years

Source: Company, CLSA

Forced into electric vehicles

We don’t expect to see any short-term catalyst for Brilliance self-brands, noting

that even the company gives very bearish guidance since the BMW JV is so

profitable, which leaves little desire to develop own brands. In the meantime,

BMW has agreed to help with the JV co-branded electric vehicle (EV) model

called the Zinoro 1E (Zhi Nuo, 之诺, in Chinese). It was on display at the

Guangzhou Auto Show in November 2013. A co-brand is a vehicle that will be

branded under the Chinese partner’s name but made together by both

companies and both share in the profits. It is sort of the opposite of a normal JV

that is made by a Chinese and foreign company using the foreign brand’s name.

According to BMW Brilliance, it will have a range of about 150 kilometers, (93

miles using a lithium battery from Ningde Times New Energy Technology),

rear-wheel drive using a 125kW electric motor (165hp) with peak torque of

about 250 Nm (184 lb-ft). The specifications don’t seem to be very exciting

(100)

(50)

0

50

100

150

200

250

300

350

400

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2010 2011 2012 2013 14CL 15CL

(Rmbm)

Revenue

Net profit (RHS)

(Rmbm)

(20)

(15)

(10)

(5)

0

5

10

15

20

25

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2009 2010 2011 2012 2013 14CL 15CL

(units) Mid-priced minibus

Deluxe minibuses

YoY (RHS)

(%)

(2,000)

(1,000)

0

1,000

2,000

3,000

4,000

5,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2010 2011 2012 2013 14CL 15CL

(Rmb)

Blended ASP

Profit per car (RHS)

(Rmb)

No intention to make

significant change for its

self-brand in the short-

term if they don’t have to

Poor visibility into the

BMW business as the

company uses equity

gain accounting

The potential turnaround

opportunity for them is

entering into MPV from its

minibus business

Self-brand ASP should

be Rmb73k and loss

per car of Rmb996 in

14CL and 15CL

13. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 13

as the car can go from 0-50 kilometres (31 miles per hour) in 5.5 seconds, a

bit slow for an electric car. The acceleration tops out at 130kph (81mph),

which is pretty fast for an electric car. Charging seems reasonable at about

eight hours from empty to fully charged using the 220v standard in China.

The company does not seem to be planning to make many of these cars and

we hear it will probably lease them. The plan so far is to open a store in

Shanghai and Beijing.

Figure 16 Figure 17

Zinoro - using the same platform as the BMW X1 Denza - Co-branded version from Daimler and BYD JV

Source: Company

The competitor from Daimler, the Denza, is based on a first-generation

Mercedes-Benz B Class designed to accept batteries within the floor. It was

developed in China by a team of engineers from both Daimler and BYD Auto.

The companies put together this deal back in March 2010.

It is interesting to note the two different styles these carmakers are following.

BMW is making this car for the Chinese partner and does not want to have

any association with the Chinese brand. It seems the approach BMW is taking

is to get the car companies to push the EV concept in order to try and get

more acceptances in the market. Daimler, on the other hand, is using its own

brand to market the car.

The reason these companies are specifically helping the Chinese partners on

EV cars is that they don’t expect a lot to be sold. But more importantly, there

is a perception that unless they share some technology for helping the

Chinese government with the new energy vehicle policy, they may not get

approval for more new factories. We find this difficult to believe and this is

what a Chinese partner is supposed to manage - future expansion. But some

of the carmakers are taking this very seriously and worry they could be

penalised down the road, so the fear factor is driving this programme.

BMW is clearly moving “big time” into electrification and it seems it is

providing technology to the Chinese partner that will be at the low end of

their product portfolio. So the company should not have a big impact on the

more important segments of higher-end that they really care about. But for

Daimler, we are a little bit confused as to why it wants to keep its own logo on

the car and branding with BYD. It might be due to the fact that Daimler is

further behind on the electrification strategy and maybe this strategy buys

them more time.

Denza - JV with

Daimler and BYD

At the start the plan is to

lease rather than sell

these cars

We do not expect to see a

lot of units sold for Zinoro

BMW at the corporate

level is making a big bet

into electrification

14. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

14 scott.laprise@clsa.com 17 April 2014

Opportunities for Brilliance self-brand

We do not have a clear view of the self-brand strategy of Brilliance other than

the company seems to want to keep self-branded cars out of the listed

company and put them in the parent group. Brilliance clearly would like to

keep the listed company as much of a pure play on BMW as possible, though

we don’t believe this is doable in the long run. We would expect the

government at some point to come in and question the whole JV structure,

which is counter to the system. Therefore, the move into new energy vehicles

seems to be a good compromise strategy. We have seen little so far in results

in terms of a self-branded car, but at least the company can argue that it is

working hard and spending money.

We do see a potential opportunity to enter the multi-purpose vehicle (MPV)

segment as an extension to its minibus business. We expect MPVs to possibly

experience similar explosive growth to that of SUVs in the next few years. So

far, we have not heard the company making any MPVs but we simply highlight

where we see an opportunity.

MPVs are the fastest-growing segment in the China auto market. It is a bit of

a surprise to see the segment growing so well but this is likely some of the

fallout from the growth in SUVs plus a low-base effect. Traditionally in China,

MPVs are bought by companies to move around management personnel. This

tradition exists from the old days of the SOEs whereby transportation is

always provided. Consumers have not wanted to buy an MPV for personal use

as they don’t want other people to think they are driving a company car. But

this is changing as consumers realise the convenience of having a big SUV for

use with the family. We also see more MPV choices in the market and

consumers are slowly looking at an MPV as an option. We expect to see good

growth going forward as these cars slowly gain acceptance with the

consumer.

Figure 18

Monthly PV shipment YoY growth breakdown

Source: Wind

Back in 2000, almost no MPVs were sold. Historically, most MPVs have been

the kind of multiuse vehicle or something called a mianbao che (translated as

bread loaf vehicle). They historically have not sold well for family use as they

give the Chinese consumer the feeling of a company car for use in

transporting people or cargo. This segment is currently dominated by low

pricing at around Rmb50,000 and offers minimal features.

(100)

(50)

0

50

100

150

200

250

300

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Jan 12 Apr 12 Jul 12 Oct 12 Jan 13 Apr 13 Jul 13 Oct 13 Jan 14

('000 units) PV Basic Car

MPV SUV

Cross over PV YoY (RHS)

Basic car YoY (RHS) MPV YoY (RHS)

SUV YoY (RHS) Crossover YoY (RHS)

(%)

MPV’s up 141% YTD

albeit from a low base

MPVs a good

opportunity

to expand

Brilliance seems to want

to keep self-branded cars

out of the listed company

MPVs are the fastest-

growing segment in the

China auto market

15. Section 1: BMW model cycle is bottoming Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 15

We see the segment overall as the least oversupplied and the best

opportunity for carmakers going forward from a low base. In the MPV

segment, we see the low, mid and high models all undersupplied compared to

other segments. SUVs over the past two years have been undersupplied, but

almost all carmakers are targeting the segment with new products. While it

will still take some marketing to overcome the company car stigma, we

believe the recent growth in the SUV market will help pave the way for bigger

and similar cars like MPVs.

Figure 19

Segment share of passenger cars in China

Source: CAAM

0

20

40

60

80

100

2008 2009 2010 2011 2012 2013

(%)

MPV

SUV

A class: up to 1.6L

B class: 1.6-2.5L

C class: 2.5-3.0L

D class: over 3.0L

MPV segment - least

oversupplied and

best opportunity

16. Section 2: Proxy for BMW Brilliance Auto - BUY

16 scott.laprise@clsa.com 17 April 2014

Proxy for BMW

We saw 102% of net profit for 2013 coming from the BMW JV. We estimate

shipment growth for BMW Brilliance to maintain at 26.5% and 28.3% YoY in

2014 and 2015, respectively, mainly supported by capacity expansion at the

Tiexi and Dadong factories, which results in earnings growth of 23.7% and

22.7% YoY. Risk to net profit arises if the company launches more low-profit

self-branded cars, especially as the government is pushing this policy.

Figure 20

Profit contribution breakdown

(Rmbm) 2009 2010 2011 2012 2013 14CL 15CL

JV income from Brilliance-BMW 355 896 1,720 2,325 3,435 4,250 5,214

Profit from self-brand business (1,995) 375 92 (24) (61) (77) (76)

Total net profit (1,640) 1,271 1,812 2,301 3,374 4,173 5,139

Profit contribution from

BMW Brilliance (%)

70.5 94.9 101.1 102 102 101

Figure 21

Key financial highlights for BMW Brilliance

(Rmbm) 2009 2010 2011 2012 2013 14CL 15CL

Revenue 14,674 21,485 37,532 56,151 73,173 89,170 110,705

Cost of goods sold (12,606) (17,602) (31,059) (44,577) (57,330) (70,684) (88,138)

Gross profit 2,069 3,883 6,473 11,573 15,842 18,487 22,566

SG&A (1,317) (1,834) (3,194) (4,500) (6,139) (7,153) (8,661)

Operating profit 751 2,049 3,278 7,073 9,704 11,333 13,905

Tax (41) (257) 162 (2,423) (2,833) (2,833) (3,476)

Net profit 711 1,792 3,441 4,650 6,871 8,500 10,429

Net profit attributable to

Brilliance

355 896 1,720 2,325 3,435 4,250 5,214

Ratio analysis (%)

Ebit margin 5.1 9.5 8.7 12.6 13.3 12.7 12.6

Net profit margin 4.8 8.3 9.2 8.3 9.4 9.5 9.4

SG&A as % of revenue (9.0) (8.5) (8.5) (8.0) (8.4) (8.0) (7.8)

Gross margin 14.1 18.1 17.2 20.6 21.7 20.7 20.4

Figure 22

Key financial highlights for self-brand segments

Minibus (Rmbm) 2009 2010 2011 2012 2013 14CL 15CL

Revenues 6,149 8,949 6,443 5,916 6,103 5,668 5,838

Cost of sales (5,294) (7,725) (5,587) (5,220) (5,417) (5,090) (5,243)

Gross profit 855 1,224 856 696 687 578 595

Other net income 112 92 48 50 96 42 43

Interest income 31 79 76 74 47 55 56

Selling & distribution expenses (310) (462) (388) (539) (608) (518) (534)

Administrative expenses (331) (363) (361) (339) (399) (324) (334)

Ebitda 818 709 369 83 (36) 67 81

Operating profit 357 569 231 (57) (178) (168) (173)

Finance costs (94) (171) (194) (174) (139) (175) (188)

Share of associates 22 92 69 92 193 193 193

Share of JCEs (1) 78 122 109 13 40 60

PBT (360) 569 229 (31) (111) (110) (107)

Income tax (expense) credit (41) 54 (58) (58) (8) (2) (2)

PAT (401) 623 171 (88) (119) (112) (110)

Loss for the year from

discontinued operations

(2,698) 0 0 0 0 0 0

Minority interest 1,104 (248) (79) 64 58 35 34

Net profit (1,995) 375 92 (24) (-61) (77) (76)

Source: CLSA, Company report

We expect that the JV income of BMW Brilliance to make up 102% of

Brilliance’s total net profit in 2014 and the ratio kept at around 100% in the

next two years.

Proxy for BMW

China business

Since 2012 BMW

provides around 100%

of profit for Brilliance

BMW Brilliance Ebit

margin should be stable

over the next three years

Self-brand should

continue to make loss in

the next few years

17. Section 2: Proxy for BMW Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 17

Figure 23

JV income of BMW Brilliance is 99% of Brilliance net profit in 2013

Source: Company, CLSA

BMW’s China business outlook is a function of the JV with Brilliance in the

next few years, which is reflected in the high sensitivity of BMW Brilliance’s

shipment volume and ASP to Brilliance’s earnings.

Below we show how much Brilliance represents of BMW’s worldwide profit. We

do not have any further breakdown in China for parts, or any other profit

made at the JV. China as part of BMW globally also makes profit from parts

sent to the JV, imported cars like the 7 Series and X Series SUVs.

Figure 24

BMW Brilliance profit contribution to BMW

(Rmbm) 2009 2010 2011 2012 2013 14CL 15CL

Brilliance-BMW 355 896 1,720 2,325 3,435 4,250 5,214

BMW 1,943 28,972 43,930 41,343 43,058 44,227 46,408

% contribution 18.3 3.1 3.9 5.6 8.0 9.6 11.2

Source: CLSA, Bloomberg

Figure 25

Sensitivity analysis - most sensitive to ASP change

(%) Net profit Ebitda

2013 2014 2015 2013 2014 2015

1% change in Brilliance-BMW blended ASP 8.0 8.1 8.2 0.0 0.0 0.0

1% change in Brilliance-BMW sales volume 1.7 1.7 1.7 0.0 0.0 0.0

1% change in Jinbei minibus blended ASP 1.6 1.4 1.2 na na na

1% change in Jinbei minibus sales volume 0.2 0.1 0.1 na na na

Source: CLSA

Great 1H13 result supported by the new 3 Series

In 4Q12, BMW Brilliance launched a long-wheeled version of the 3 Series and

the regular version was launched in 1Q13. Monthly 3 Series shipments have

reached 5,000 per month. According to CAAM, in 2013, total 3 Series

shipments were up by 194% YoY with the 5 Series up 17% YoY. This strong

sales performance helped the company to make a total net profit of

Rmb3,374m, up 46.6% YoY. JV income from BMW Brilliance was Rmb3,448m,

or 47.7% YoY growth.

0

20

40

60

80

100

120

(2,000)

(1,000)

0

1,000

2,000

3,000

4,000

5,000

6,000

2009 2010 2011 2012 2013 14CL 15CL

(Rmbm) JV income from Brilliance-BMW (LHS)

Total net profit (LHS)

Net profit

(%)

BMW Brilliance is the sole

profit source for Brilliance

and will likely be in the

next three years

JV shipments and ASP has

high sensitivity to the

Brilliance’s earnings

BMW Brilliance

contributed c.8% of total

profit for BMW Group

and the ratio should

trend up to 11.2% in

15CL, with expanding

localisation capacity

1% ASP change of BMW

Brilliance blended will

cause over 8% Brilliance

net profit change

18. Section 2: Proxy for BMW Brilliance Auto - BUY

18 scott.laprise@clsa.com 17 April 2014

Figure 26

BMW Brilliance monthly shipments breakdown by products

Source: Company

The CAAM data is the only official source for vehicle shipments to car dealers

in China. This official source will only tell us sales to dealers and not to end

users and is therefore the reason we always refer to car shipments. There is

unfortunately no source for end user sales in China. This can therefore lead to

some errors or strange numbers coming out of CAAM.

The CAAM data shows BMW Brilliance 3 Series shipments in 2012 were only

20,794 units (monthly average 17,000 units). In 2Q12, there were no 3

Series shipments. This was due to a local capacity constraint, so BMW China

launched the imported model 3 Series first and in 4Q12, the long-wheel

version of the new 3 Series was sold. The new Tiexi factory has annual

capacity for 100,000 units and since it has come online, there are no more

imports of these models into China.

Shipment growth supported by capacity additions

We forecast shipment growth for BMW Brilliance to maintain at 26.5% and

28.3% YoY in 2014 and 2015, mainly supported by capacity expansion at the

Tiexi and Dadong factories. The 5 Series should still make up the largest

shipment volume and we forecast 138,714 units (116,000 units per month)

and 149,000 units (124,000 units per month) in 2014 and 2015. However, we

expect 5 Series shipments as a percentage of total shipments to decrease to

44.3% in 2015 from 65.7% in 2012 while on the other hand the 3 Series is

expected to increase to 36.6% in 2015 from only 21.5% in 2012 with the new

3 Series launched in 4Q12 (long-wheel) and 1Q13 (regular version).

0

5,000

10,000

15,000

20,000

25,000

Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12 Jan 13 Jul 13

Brilliance BMW X1

Brilliance BMW 5 Series

Brilliance BMW 3 Series

(units)

New 3 Series monthly

shipments around 5k

units on average

There is no data source

for car sales to

consumers in China

Unit volume growth will

come more and more

from the less-profitable

3 Series

19. Section 2: Proxy for BMW Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 19

Figure 27

BMW Brilliance shipment forecast breakdown by model

Source: Company, CLSA

Figure 28

5 Series had a facelift in 3Q13, though with no major upgrades

Source: BMW China

The key upgrades of the new face lifted 5 Series are:

Small change to the exterior: including the shape of headlights, rear-view

mirror and taillights.

Change in the interior: offering one more colour option for the seat

Upgrade of the main console with an LED panel

Upgrade of the iDrive system

Upgrade in the driving assistance system

Installed a surveillance camera on the top of the car

0

10

20

30

40

50

60

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2009 2010 2011 2012 2013 14CL 15CL

(units)

3 Series

5 Series

X1 SUV

Zinoro

1 Series

YoY chg (RHS)

(%)

5 Series discount offered

is less than 5% due to

strong consumer demand

Shipment growth should

maintain at 26.5 % in

14CL and 28.3% in 15CL

20. Section 2: Proxy for BMW Brilliance Auto - BUY

20 scott.laprise@clsa.com 17 April 2014

We believe the 3 Series will be the primary growth engine for BMW Brilliance

shipments, supported by both long-wheel and regular versions as highlighted

with the recent launch of the entry-level model 316i. We expect 3 Series

annual shipments could reach 94,880 units (7900 units per month) in 2014

and 123,344 units (10,278 units per month) in 2015. We expect that new

entry-level model, the 316i, will sell well due to the very competitive ASP

(MSRP starting from Rmb283,000), which is at the upper end of pricing for

mid-class sedans, such as GAC Honda Accord, GAC Toyota Camry, DFM Nissan

Tienna and the Buick Regal.

The normal 3 Series is very similar to the 3 Series sold throughout the world.

The long version is designed to target consumers who have a driver and

compete with the Audi A4L. The long version has premium pricing while the

regular version is more aggressively priced.

Figure 29

Entry-level luxury models will put pressure on middle-to-high end segment

Car model MSRP (Rmb’000)

Brilliance BMW 316i 283.0

GAC Honda Accord 2.4L 235.8

GAC Toyota Camry 2.5L CVT 259.8

Buick Lacross 2.0T 259.9

Source: CLSA, Autohome.com

The entry-level luxury models are grabbing market share from the mid-to-

high-end segment, especially the Japanese, due to brand premium. Our talk

with dealers showed the average age of car buyers is between 25 and 40,

though they are getting younger. Those car buyers care more about the car

branding and consider buying a car as a way to raise their social status. In

addition, those buyers are more willing to accept using credit as opposed to

their parents who saved money, making those low-rate loans very attractive.

Taking BMW and Audi as examples, BMW is offering a 1.99%-2.99% loan rate

and Audi even offers 0%.

As luxury car sales continue to slow down, BMW and the car dealers are

focusing on a new strategy. For example, in our talk with one dealership

group, they put big advertising boards close to the Toyota Camry dealer. They

use the slogan translated from Chinese “just add a little bit more and you

could be driving away in a BMW”. We believe this targeted advertising will

work very well as most consumers go to a dealership with a budget in mind.

But the BMW dealers think they can change the mind of these consumers by

using car loans and explaining that their car payment will be just a little bit

more. We thought this would mean more 3 Series sales as consumers move

up. But to our surprise, talking to the dealer, they actually try to get the

buyer to go from looking at a Camry into buying a BMW 5 Series. The dealer

explained to us that car buying is such an emotional experience that once you

can convince a buyer they can afford a 5 Series, many will go for this option.

So the car dealers are becoming much more sophisticated in their selling

approach and moving aspirational car buyers from lower products into their

entry-level or premium luxury cars.

3 Series will be the

primary growth engine

for shipments

BMW dealers moving

aspirational buyers

up the value chain

Car loans at some BMW

dealers going from 15%

in 2012 to +40% in 2013

21. Section 2: Proxy for BMW Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 21

Figure 30

BMW suggests Rmb283k for the 316i with market price around Rmb250k

Source: BMW China

Three positive catalysts for the 3 Series

We outline below why we see the BMW 3 Series as a big growth driver over

the next few years.

1. Capacity is not a problem with the new Tiexi factory completed

In 2013, BMW Brilliance’s total annual capacity hit 300,000 units with the new

Tiexi factory phase I completed. In 2014, we expect 50,000 units of

additional capacity will be added at the Dadong factory with total annual

capacity reaching 350,000 units. Now this can also be a negative if we see

consumers slow down and then capacity utilisation ratio fall, which would

leads to a less efficient factory impacting margins.

Figure 31

BMW Brilliance capacity breakdown

Source: Company, CLSA

0

20

40

60

80

100

120

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2009 2010 2011 2012 2013 14CL 15CL

(units) Tiexi

Dadong

Utilisation (RHS)

(%)

Total annual capacity

should reach 350k units

in 14CL (Tiexi 200k and

Dadong 150k units)

316i launched in 4Q13

with two versions and

MSRP at Rmb283k

Total annual capacity can

reach 500k in 2016CL

22. Section 2: Proxy for BMW Brilliance Auto - BUY

22 scott.laprise@clsa.com 17 April 2014

Figure 32

Tiexi factory total capacity should reach 350k units per annum in 14CL

2009 2010 2011 2012 2013 14CL 15CL 16CL

Tiexi 100,000 200,000 200,000 250,000 350,000

Dadong 50,000 100,000 100,000 100,000 100,000 150,000 150,000 150,000

Total 50,000 100,000 100,000 200,000 300,000 350,000 400,000 500,000

Brilliance BMW 44,997 53,963 95,451 147,374 207,427 259,433 318,120 381,649

Utilisation (%) 90.0 72.0 95.5 98.2 83.0 79.8 84.8 84.8

Source: Company, CLSA, Capacity utilisation is calculated from an average capacity over 2 years as all the capacity will not be in place for the whole year

2. Entry-level luxury models will provide the growth

We expect 3 Series shipment volume to increase from 29% of total shipments

in 13CL to over 36% in 14CL and the 5 Series to drop from 60% to 53% in

14CL. We expect 3 Series annual shipment volumes to increase from 61,000

units in 13CL (5,000 units per month) to 123,000 units in 15CL (127,000

units per month). Entry-level luxury models such as the 316i which retail at

Rmb260,000 will grab market share from middle-to-high-end cars, especially

Japanese brands. They will appeal to younger car buyers where branding

becomes more important in the emotional car buying decision. The younger

buyers, the target market for the 3 Series, are also less concerned about

going into debt so car loans are a viable option.

Figure 33

Shipment breakdown

Shipment (units) 2009 2010 2011 2012 2013 14CL 15CL

3 Series 17,899 29,605 42,843 34,766 61,213 94,880 123,344

5 Series 27,623 41,019 65,494 105,939 123,852 138,714 149,118

X1 SUV 0 0 5 20,641 22,362 28,400 33,228

Zinoro 0 0 0 0 0 500 1,000

2 Series 0 0 0 0 0 0 30,000

Total 45,522 70,624 108,342 161,346 207,427 262,494 336,690

Total shipment growth YoY (%) 55 53 49 29 26.5 28.3

Shipments by product (%)

3 Series 39.3 41.9 39.5 21.5 29.5 36.1 36.3

5 Series 60.7 58.1 60.5 65.7 59.7 52.8 44.3

X1 SUV 0.0 0.0 0.0 12.8 10.8 10.8 9.9

Zinoro 0.0 0.0 0.0 0.0 0.0 0.2 0.3

1 Series 0.0 0.0 0.0 0.0 0.0 0.0 8.9

Total 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Source: Company, CLSA

As we move to a greater portion of sales coming from the 3 Series, this will

impact negatively on ASP and profit per car. We see 2013 as the peak for ASP

and profit per car. But as BMW moves down the luxury market, the company

will be able to sell more volume.

Figure 34 Figure 35

Profit per car and blended ASP BMW Brilliance margins almost flat in next 3 years

Source: Company, CLSA

270

280

290

300

310

320

330

340

350

360

370

0

5

10

15

20

25

30

35

40

2009 2010 2011 2012 2013 14CL 15CL

(Rmb'000) Profit per car

Blended ASP (RHS)

(Rmb'000)

0

2

4

6

8

10

12

14

2009 2010 2011 2012 2013 14CL 15CL

Net profit margin

Ebit margin

(%)

3 Series production is

increasing rapidly

In 2013 we saw the peak

in ASP and profit per car

23. Section 2: Proxy for BMW Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 23

We forecast blended ASP to drop by 3.3% YoY in 2014 and 3.2% YoY in 2015

due to a higher portion of 3 Series shipped. In addition, net margin of the

BMW Brilliance JV will stay at 9.5% and 9.4%, in 14CL and 15CL.

When we compared YoY growth rates for both shipment and profit, we found,

except in 2012, that profit growth outpaced shipment growth, which we

believe is mainly due to a high production utilisation ratio and high-margin

products like the 5 Series. This means the efficiency from expansion is

dropping. Presently our sensitivity shows that a 1% change in shipment

growth is not enough to give 1% profit growth.

Figure 36

Shipment growth faster than profit growth in most years

Source: Company, CLSA

3. BMW is the top luxury brand in Chinese consumers’ mind

Among the three German luxury brands, during the past three years, BMW

and Audi outperformed Mercedes Benz. Audi’s ‘government sales changing

into individual market’ strategy has proved a big success and compared with

the other two, Audi has the highest localisation level with more JV models and

fewer imports. The advantage of this strategy has been government officials,

who are more inclined to buy a car made in China as an imported car

symbolises excess. Also, Audi maintains a strong market among companies

that are almost SOEs and service providers to SOEs. If a government official

is driving an Audi, it is very difficult for a service provider to be driving

around in a car much better as this might cause a loss of face.

Digital Luxury Group’s 2013 luxury survey has Audi and BMW ranked No.1

and No.2 of the most sought-after luxury brands in China while Mercedes

Benz ranks No.7. Now, the Benz brand is very well known, and we believe it

will increase as it introduces new models. Its old model lineup has hurt its

image in the past few years. The new S Class, we believe, is already

impacting favourably on the brand and we should see a pickup in the

desirability for the brand in the next few years.

0

20

40

60

80

100

120

140

160

2010 2011 2012 2013 14CL 15CL

BMW Brilliance shipment growth

BMW Brilliance profit growth

(%)

Shipment growth outpaced

the profit growth, which

we think is mainly due to

the margin erosion

Higher portion of 3

Series production should

bring down net margins

Benz becoming

more popular

During the past three

years, BMW and Audi

outperformed

Mercedes Benz

24. Section 2: Proxy for BMW Brilliance Auto - BUY

24 scott.laprise@clsa.com 17 April 2014

Figure 37

BMW ranks No.2 of the most sought-after luxury brands in China

1 Audi 11 Lancome

2 BMW 12 Gucci

3 Chanel 13 Hermes

4 Estee Lauder 14 Volvo

5 Louis Vuitton 15 Land Rover

6 Mercedes Benz 16 Infiniti

7 Lexus 17 Chow Tai Fook

8 Dior 18 Cadillac

9 Porsche 19 Cartier

10 Lamborghini 20 Clinique

Source: Digital Luxury Group

In the Chinese consumers’ mind, Mercedes Benz and BMW are better than

Audi. This is also reflected in the price with Audi being the cheapest among

the three German marques. Car owners who want to show their social status

is reflected in a Chinese saying: “开宝马,坐奔驰” -“drive a BMW and be driven

in a Mercedes Benz”. Audi has carved out a niche as being a modest luxury

brand mostly used by government or government-like companies in China.

For BMW Group, China has become the most important market, accounting

for 18% of its total worldwide shipments. In total, China has more than one

million BMW cars on the road. In addition, the 5 Series, X5 and X6 SUV and 7

Series China shipments all outpaced ex-China shipments, which is a reflection

of the Chinese consumer’s strong demand for ultra-luxury imported autos.

Figure 38

BMW Brilliance profit contribution to BMW

(Rmbm) 2009 2010 2011 2012 13CL 14CL 15CL

Brilliance-BMW 355 896 1,720 2,325 3,435 4,250 5,214

BMW 1,943 28,972 43,930 41,343 43,058 44,227 46,408

% contribution 18.3 3.1 3.9 5.6 8.0 9.6 11.2

Source: CLSA, Bloomberg

Figure 39

BMW China shipments vs ex-China breakdown by product

Source: CLSA, BMW Group

0

5

10

15

20

25

30

35

40

1

Series

X1 3

Series

X3 Z4 5

Series

X5 X6 6

Series

7

Series

MINI Rolls

(%)

China

Ex-China

BMW has a sportier image

and thought to be the

better choice for those who

personally drive their car

China is BMW’s largest

market in the world

BMW ranks No.2 of

the most sought-after

luxury brands in

China, second to Audi

China market represents

over 18% of total BMW

global shipments

25. Section 2: Proxy for BMW Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 25

BMW Brilliance will benefit from capacity additions and we expect localised

BMW models to increase from 55% in 13CL to 68% in 15CL of BMW’s total

unit sales in China.

Figure 40

BMW’s localisation ratio should reach 68% in 15CL from 55% now

Source: BMW Group, CLSA

Five negative catalysts for the stock

After reviewing the three potential catalysts for Brilliance, we now look at five

negatives we see developing for the company.

Negative 1: Priced to perfection with limited upside

BMW management has done a great job managing the brand in China, and

indeed we consider it the best of the luxury carmakers. It has outperformed

in almost every area, including dealer network expansion, dealership

management, brand building, product localisation and even JV partner

selection (Brilliance is a weaker partner than BAIC/Mercedes and FAW/Audi).

Discussion with BMW dealers reveals active management and proactive policies

from the employees here in China. Compared to Benz, they have had a lot of

management issues in the past such as having price wars among dealer groups

for the old S Class. We see this now fixed at Benz and it will improve a lot in

the next two years with better management and better models.

Figure 41 Figure 42

Ranks No.2 in car segment, second to Audi in branding BMW did best in dealership expansion in past few years

Ranks Cars Fashion Beauty

1 Audi Chanel Estee Lauder

2 BMW LV Lancome

3 Lexus Gucci Dior

Ranks Hospitality Watches Jewelry

1 Sheraton Omega Chow Tai Fook

2 Hilton Rolex Cartier

3 Intercontinental Longines Swarovski

Source: Digital Luxury Group Source: CLSA, internet news

40

45

50

55

60

65

70

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2009 2010 2011 2012 13CL 14CL 15CL

Imported (LHS)

Brilliance BMW (LHS)

JV model of total BMW China shipment

(units) (%)

0

100

200

300

400

500

600

2012 13CL 14CL 15CL

Audi Mercedes Benz BMW Porsche JLR

(stores)

BMW will continue to sell

more domestic made

BMWs as a % of their

total shipments to China

We view BMW as the

best-managed luxury

carmaker in China

26. Section 2: Proxy for BMW Brilliance Auto - BUY

26 scott.laprise@clsa.com 17 April 2014

But the competition has also been watching and is starting to emulate BMW.

Audi and Mercedes Benz have already started to copy BMW’s dealership

management style, which is a reflection of its success. The question now is

what can BMW do next? What’s the future upside? We believe the company

has peaked and is entering a poor part of the model cycle, especially when

compared with Mercedes.

In Figure 43, we describe the different dealership styles for the big three

German brands. While we describe the current situation, we don’t expect this

to continue forever. We see a lot of changes ahead for Mercedes Benz and

expect the company could move away from such a concentration at a few

dealership groups to a more balanced approach, similar to BMW. Audi’s

dealership strategy seems to be working, but if the company does move in any

direction, we expect it will be more towards the BMW model. For BMW, we fail

to see what the company can do to improve from here. It has already cut back

on costs as this year’s dealership meeting was held in China and we think the

company could be preparing for a tougher, more competitive year ahead.

Figure 43

Dealership style comparison between the German Big 3 in China

Source: CLSA

Major brand differences in China

BMW is regarded as a good quality auto, with strong power and a sporty

image in China, or a “driver’s car.” This is related to the company’s history.

BMW stands for Bayerische Motoren Werke, which produced engines for

airplanes back in 1916. BMW’s commercials always use light colours (usually

white and blue from its logo) to demonstrate sportiness, which makes BMW

appeal to a younger Chinese generation. This is also reflected from a Chinese

saying: ‘开宝马,坐奔驰’ - “drive a BMW, be driven in a Mercedes Benz.”

Balance style

Build up relationship with several large dealers, but each

market share should below 10%

Dealers has incentive to build up their own brand in dealership

Can ensure service quality and maintain competition between

dealers

Still have control and strong bargaining power over dealers

Scatter style

All dealer partners are very small ones with no concentration

Pros: Fully control those dealer partners

Cons: Can't ensure the service of the quality and dealers have

no strong incentive to further develop business

Concentration style

Primary partner is Lei Shing Hong

Pros: Can ensure service quality

Cons: Low bargaining power with dealers; Expansion speed will

be limited

BMW’s dealership

management style

has proved to be

the most successful

Competition copying

BMW’s successful dealer

management approach

BMW brand image

is about being

sporty and young

27. Section 2: Proxy for BMW Brilliance Auto - BUY

17 April 2014 scott.laprise@clsa.com 27

Figure 44 Figure 45

Blue and white are the main colours in BMW’s ads Brilliance BMW 3 Series commercial

Source: BMW China

Audi was essentially a government car in China in the past and always put

the emphasis on new technology. The company is perceived as being more

about a value-for-money luxury car choice. Compared to the other two

brands, Audi does not often use celebrities in commercials and focuses more

on the car itself. Audi has a lower profile, or considered more of middle-of-

the-road luxury brand and widely treated as the best car for doing business.

The typical colour for an Audi sedan is black, which gives people a feeling of

calm, tradition and steadiness.

Figure 46 Figure 47

FAW Audi A4L commercial FAW Audi A6L most widely used in business

Source: Audi China

Mercedes Benz has tried to deliver a brand to consumers that is luxurious,

noble and successful. Along with BMW, a Mercedes Benz sedan is a car for the

elite and successful. It is not used for government as it is thought to be too

luxurious and overstated. Mercedes uses more celebrities in its commercials.

Audi brand image is

more conservative

Mercedes brand

image is for the

elite and successful

28. Section 2: Proxy for BMW Brilliance Auto - BUY

28 scott.laprise@clsa.com 17 April 2014

Figure 48 Figure 49

Movie start Ziyi Zhang is the spokeswoman for Benz Luxurious, noble and successful is the image for Benz

Source: Mercedes Benz

What is interesting is how Lexus has been able to have such a high ranking

as the third most sought-after luxury car and sixth overall in terms of luxury

brand in China. This ranking even beats Mercedes Benz, which has a

manufacturing presence, far more dealerships and more cars overall sold per

year. Lexus has decided not to manufacture in China yet as the company

prefers to focus on controlling product quality coming out of one factory in

Japan. While it sells fewer cars, it can make more profit per car as it does not

have to share with a Chinese JV partner. But what is most surprising is how

this brand has done so well despite all the political issues between Japan and