Download as PDF, PPTX

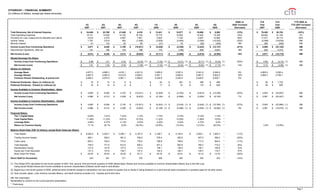

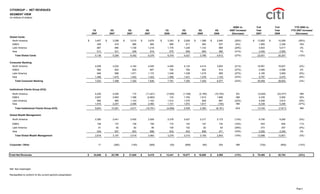

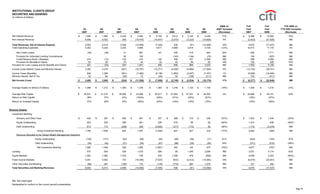

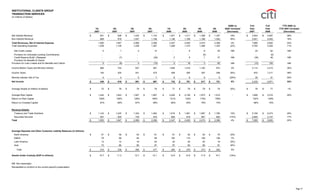

Citigroup reported financial results for the 4th quarter of 2008. Net income decreased 16% to a loss of $8.3 billion compared to a loss of $9.8 billion in 4th quarter 2007. Total revenues declined 13% to $5.6 billion. The provision for loan losses increased 66% to $12.7 billion due to higher credit costs. Total assets decreased 11% to $1.9 trillion and book value per share declined 35% to $14.70.