Download as XLS, PPTX

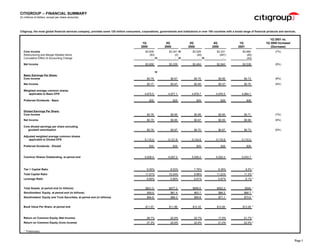

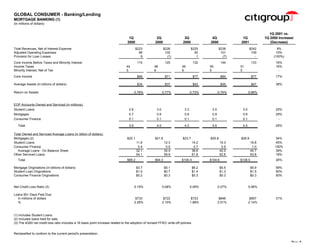

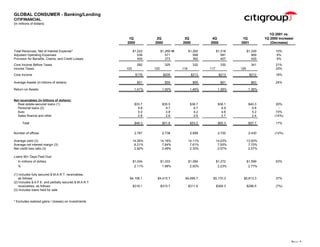

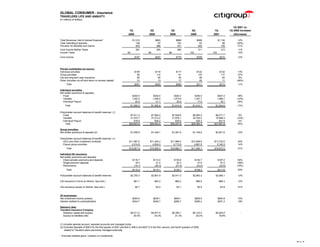

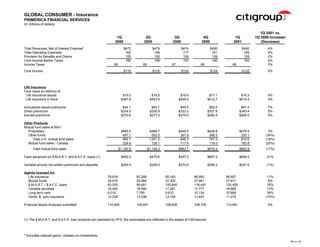

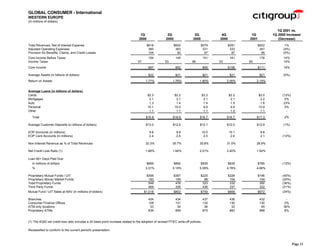

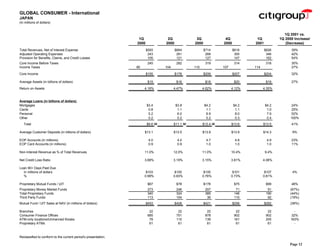

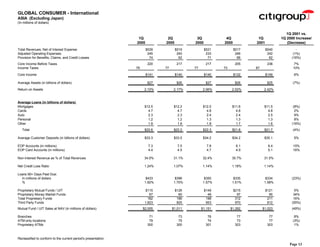

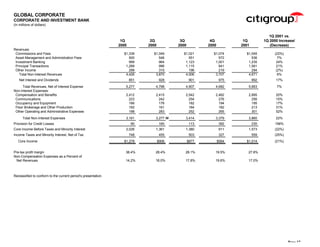

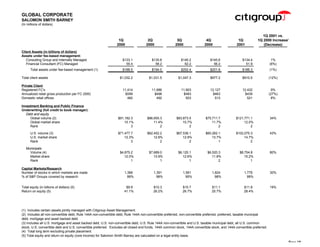

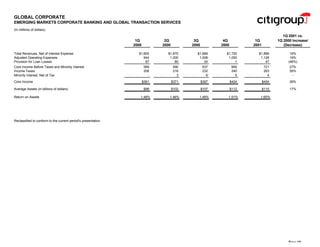

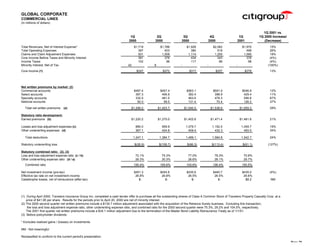

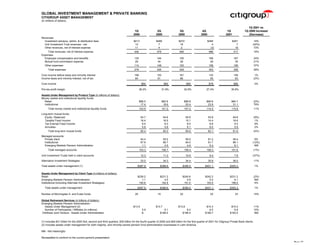

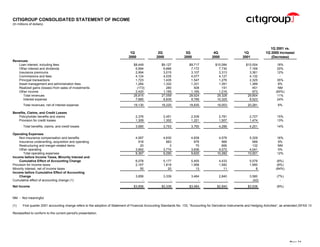

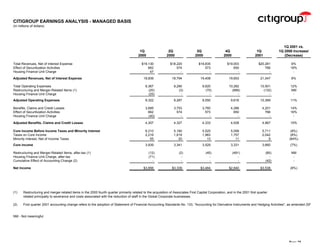

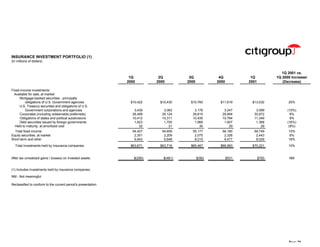

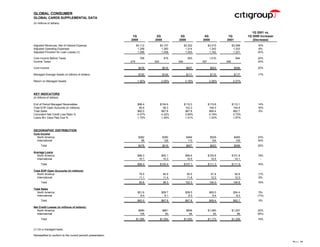

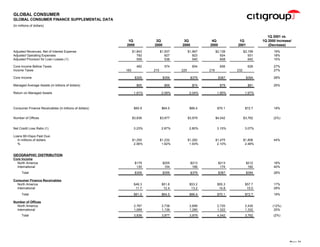

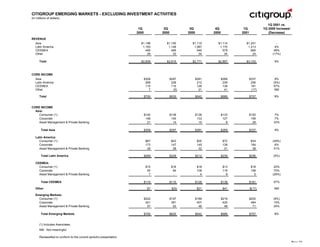

Citigroup, the largest global financial services company, reported quarterly financial results. Core income decreased 7% year-over-year to $3.66 billion, while net income decreased 8% to $3.54 billion. Revenues increased 6% to $21.05 billion driven by strong growth in North America Cards, Corporate Finance, and emerging markets. Citibanking North America revenues increased 6% to $613 million with core income before taxes up 24% to $271 million.

![Professional Power Point[1]](https://cdn.slidesharecdn.com/ss_thumbnails/professionalpowerpoint1-1232554329238199-3-thumbnail.jpg?width=640&height=640&fit=bounds)