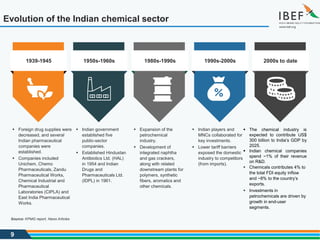

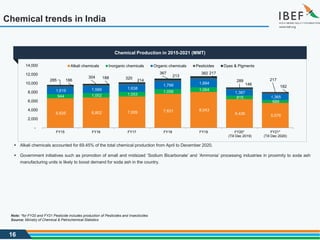

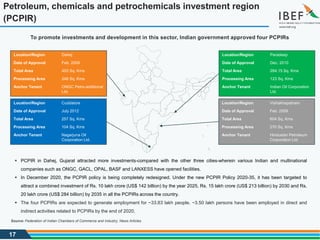

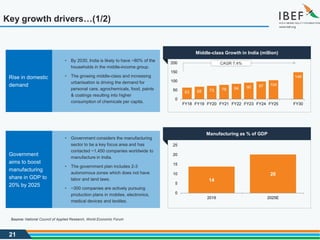

The document discusses recent trends and strategies in India's chemical sector. It notes that production of chemicals and petrochemicals declined in February 2021 compared to January. Exports of chemicals increased 68.5% in April 2021 while imports rose 72.9%. The agrochemical market is expected to grow 8% annually. The government has established four Petroleum, Chemicals and Petrochemicals Investment Regions to promote investment in the sector and attract over $284 billion by 2035.