Business combinationsare events or transactions in which

two or more business enterprises, or their net assets, are

brought under common control in a single accounting

entity.

Definition of BC

3.

A transaction orother event is a business combination if: The

assets acquired and liabilities assumed constitute a business.

If the asset acquired are not a business, it must be

accounted for as an asset acquisition.

Identification of BC

4.

IFRS 3defines a business as ‘an integrated set of

activities and assets that is capable of being conducted

and managed for the purpose of providing a return in

the form of dividends, lower costs or other economic

benefits directly to investors or other owners,

members or participants.

Business consists of Input, process and output

Business

5.

E&P CoA (an oil and gas exploration and production company)

acquires a mineral interest from E&P Co B, on which it intends

to perform exploration activities to determine if reserves exist.

The mineral interest is an unproven property and there have

been no exploration activities performed on the property.

It is not a BC.

Example

6.

• E&P CoA acquires a property similar to that in Example

above, except that oil and gas production activities are

in place. The target’s employees are not part of the

transferred set. E&P Co A will take over the operations

by using its own employees.

• It is a BC.

Cont…

7.

Combined Enterprise: Theaccounting entity that results from a

business combination.

Constituent Companies: The business enterprises that enter into a

combination.

Combinor : A constituent company entering into a combination whose

owners as a group ends up with control of the ownership interests in

the combined enterprise. The term acquirer, parent and combinor can

be used interchangeably.

Combinee: a constituent company other than the combinor in a

business combination. The term acquired, acquiree, subsidiary and

combinee can be used interchangeably.

Definition of terms under BC

8.

There are threetypes of business combinations: Horizontal Combination, Vertical Combination,

and Conglomerate Combination:

1. Horizontal Combination: is a combination involving enterprises in the same industry. E.g.

assume combination of Ethio flour and Sun flour.

2. Vertical Combination: A Combination involving an enterprise and its customers or

suppliers. It is a combination involving companies engaged in different stages of production

or distribution. It is classified into two: Backward Vertical Combination – combination with

supplier and Forward Vertical Combination – combination with customers.

E.g.: A Tannery Company acquiring a Shoes Company - Forward

3. Conglomerate (Mixed) Combination: is a combination involving companies that are neither

horizontally nor vertically integrated. It is a combination between enterprises in unrelated

industries or markets.

Types of Business Combinations

9.

The Threecommon methods for carrying out a business

combination are:

Statutory Merger

Statutory Consolidation, and

Acquisition of Common Stock

Methods of Business Combinations

10.

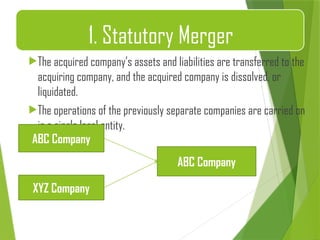

The acquired company’sassets and liabilities are transferred to the

acquiring company, and the acquired company is dissolved, or

liquidated.

The operations of the previously separate companies are carried on

in a single legal entity.

1. Statutory Merger

ABC Company

ABC Company

XYZ Company

11.

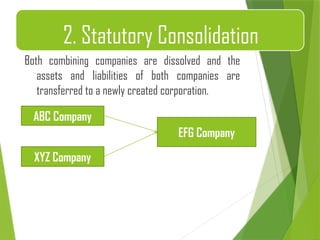

Both combining companiesare dissolved and the

assets and liabilities of both companies are

transferred to a newly created corporation.

2. Statutory Consolidation

ABC Company

EFG Company

XYZ Company

12.

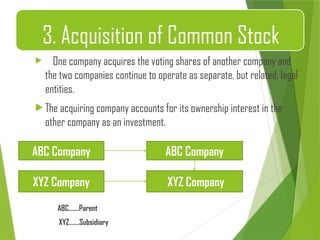

One companyacquires the voting shares of another company and

the two companies continue to operate as separate, but related, legal

entities.

The acquiring company accounts for its ownership interest in the

other company as an investment.

ABC…….Parent

XYZ…….Subsidiary

3. Acquisition of Common Stock

ABC Company ABC Company

XYZ Company XYZ Company

13.

1. Growth: Inrecent years Growth has been main reason for

business enterprises to enter into a business combination. Firms

can achieve growth through external and internal methods. The

external (e.g. business combination) method of achieving growth

is more rapid than growth through internal methods, as per

advocates of external method.

2. Economies of scale: The economies of scale will occur

as a result of more intensive utilization of production facilities,

distribution network, research and development facilities, etc. The

economies of scale will lead to financial synergies.

Reasons of Business combination

14.

Cont.…

3. Better management:Combinations results in better

management. Combinations result running the large scale enterprises. A

large enterprise can offer to use the service of expertise. Various

managerial functions can be efficiently managed by those persons who

are qualified for such jobs.

4. Monopolistic ambition: One of the important reasons

behind business combination is monopolistic ambitions. The combined

enterprises try to control more and more enterprises in the same line

so that they may be able to detect their terms (E.g. set their price). But,

the antitrust law is against such type of business combination.

15.

Cont.…

5. Diversification: Whenone company involves business

combination, it can diversify risks of operations. A Company involving

business combination can minimize risks as the enterprise is

diversifying operation or line of their activity. Since different companies

are already dealing in their respective lines, there will be risk

diversification.

6. Tax advantage: When an enterprise with accumulated losses

merges with a profit making enterprise, it is able to utilize tax shields

(benefits). An enterprise having losses will not be able to set-off losses

against future profits, because it is not a profit earning unit.

16.

This standardrequires to use the acquisition method to account

for a business combination transaction.

It involves four steps:

Acquisition Method

17.

The guidance inIFRS 10 shall be used to identify the acquirer—the

entity that obtains control of another entity, i.e. the acquiree.

In an asset acquisition, the company transferring cash or other

assets and/or assuming liabilities is the acquiring company. In a

stock acquisition, the acquirer is, in most cases, the company

transferring cash or other assets for a controlling interest in

the voting common stock of the acquiree (company being

acquired).

Step 1: Identify the acquirer

18.

Cont.…

When anacquisition is accomplished through an exchange of equity

interests, the factors considered in determining the acquirer firm include

the following:

1. Voting rights—The entity with the largest share of voting rights is

typically the acquirer.

2. Large minority interest—Where the company purchases only a large

minority interest (under 50%), but no other owner or group has a

significant voting interest, the company acquiring the large minority

interest is likely the acquirer.

3. Governing body of combined entity—The entity that has the ability to

elect or appoint a majority of the combined entity is likely the acquirer.

19.

In the absenceof evidence to the contrary:

Example 1: Companies A and B combine businesses by forming C. C issues

30 million and 20 million shares to A’s & B’s shareholders in exchange for

A’s and B’s businesses.

Example 2: same as Example 1, except: 20 million shares are issued to each

of A’s & B’s shareholders. C had 9 board members, 5 appointed by A’s

shareholders and 4 by B’s.

Example 3: on 31 December 2014 A has 100 million shares in issue. On 1

January 2015 A issued 200 million new A shares to the owners of B in

exchange for all of B’s shares.

Cont….

20.

Entity A intendsto acquire the voting shares (and

therefore obtain control) of Target Entity. Entity A

incorporates Newco and uses this entity to effect the

business combination. Entity A provides a loan at

commercial interest rates to Newco. The loan funds are

used by Newco to acquire 100% of the voting shares of

Target Entity in an arm’s length transaction.

Cont…..

21.

The date onwhich the acquirer obtains control of the

acquiree is generally the date on which the acquirer

legally transfers the consideration, acquires the

assets and assumes the liabilities of the acquiree—

the closing date

Step 2: Determine the acquisition date: date

on which the acquirer obtains control.

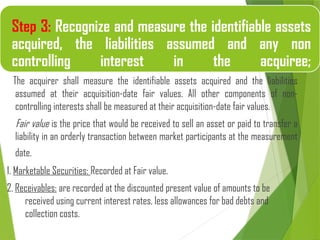

22.

Step 3: Recognizeand measure the identifiable assets

acquired, the liabilities assumed and any non

controlling interest in the acquiree;

The acquirer shall measure the identifiable assets acquired and the liabilities

assumed at their acquisition-date fair values. All other components of non-

controlling interests shall be measured at their acquisition-date fair values.

Fair value is the price that would be received to sell an asset or paid to transfer a

liability in an orderly transaction between market participants at the measurement

date.

1. Marketable Securities: Recorded at Fair value.

2. Receivables: are recorded at the discounted present value of amounts to be

received using current interest rates, less allowances for bad debts and

collection costs.

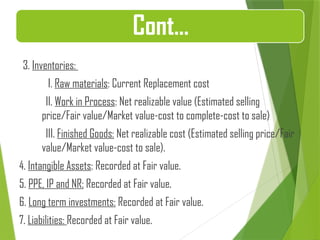

23.

3. Inventories:

I. Rawmaterials: Current Replacement cost

II. Work in Process: Net realizable value (Estimated selling

price/Fair value/Market value-cost to complete-cost to sale)

III. Finished Goods: Net realizable cost (Estimated selling price/Fair

value/Market value-cost to sale).

4. Intangible Assets: Recorded at Fair value.

5. PPE, IP and NR: Recorded at Fair value.

6. Long term investments: Recorded at Fair value.

7. Liabilities: Recorded at Fair value.

Cont…

24.

Cont.…

8. Research anddevelopment assets: The fair values of both tangible

and intangible research and development assets are recorded even

where the assets do not have alternative future uses (the usual criteria

for capitalization of R&D assets).

25.

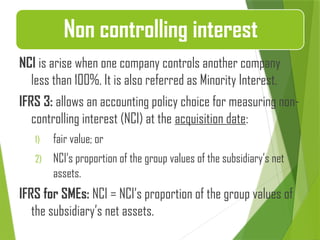

NCI is arisewhen one company controls another company

less than 100%. It is also referred as Minority Interest.

IFRS 3: allows an accounting policy choice for measuring non-

controlling interest (NCI) at the acquisition date:

1) fair value; or

2) NCI’s proportion of the group values of the subsidiary’s net

assets.

IFRS for SMEs: NCI = NCI’s proportion of the group values of

the subsidiary’s net assets.

Non controlling interest

26.

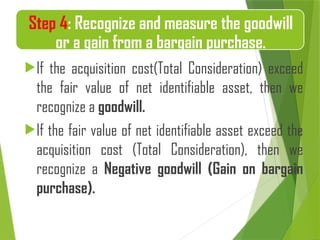

If the acquisitioncost(Total Consideration) exceed

the fair value of net identifiable asset, then we

recognize a goodwill.

If the fair value of net identifiable asset exceed the

acquisition cost (Total Consideration), then we

recognize a Negative goodwill (Gain on bargain

purchase).

Step 4: Recognize and measure the goodwill

or a gain from a bargain purchase.

27.

Cont…

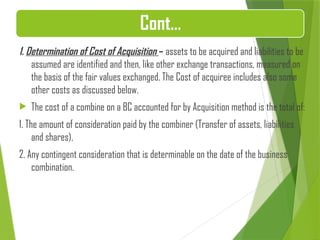

1. Determination ofCost of Acquisition – assets to be acquired and liabilities to be

assumed are identified and then, like other exchange transactions, measured on

the basis of the fair values exchanged. The Cost of acquiree includes also some

other costs as discussed below.

The cost of a combine on a BC accounted for by Acquisition method is the total of:

1. The amount of consideration paid by the combiner (Transfer of assets, liabilities

and shares),

2. Any contingent consideration that is determinable on the date of the business

combination.

28.

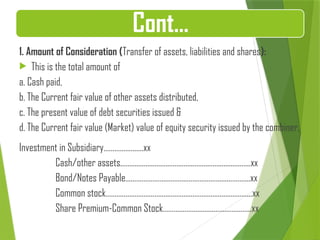

1. Amount ofConsideration (Transfer of assets, liabilities and shares):

This is the total amount of

a. Cash paid,

b. The Current fair value of other assets distributed,

c. The present value of debt securities issued &

d. The Current fair value (Market) value of equity security issued by the combiner.

Investment in Subsidiary………………….xx

Cash/other assets………………………………………………………………xx

Bond/Notes Payable….………………………………………………………..xx

Common stock……………………………………………………………………...xx

Share Premium-Common Stock……………………….…………………xx

Cont…

29.

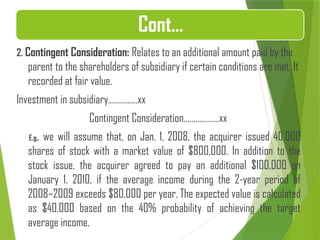

2. Contingent Consideration:Relates to an additional amount paid by the

parent to the shareholders of subsidiary if certain conditions are met. It

recorded at fair value.

Investment in subsidiary……………xx

Contingent Consideration………………xx

E.g. we will assume that, on Jan. 1, 2008, the acquirer issued 40,000

shares of stock with a market value of $800,000. In addition to the

stock issue, the acquirer agreed to pay an additional $100,000 on

January 1, 2010, if the average income during the 2-year period of

2008–2009 exceeds $80,000 per year. The expected value is calculated

as $40,000 based on the 40% probability of achieving the target

average income.

Cont…

30.

Cont.…

Summary

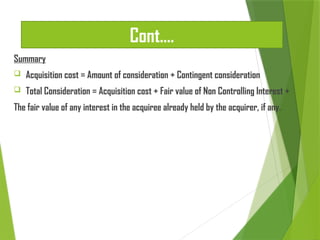

Acquisition cost= Amount of consideration + Contingent consideration

Total Consideration = Acquisition cost + Fair value of Non Controlling Interest +

The fair value of any interest in the acquiree already held by the acquirer, if any.

31.

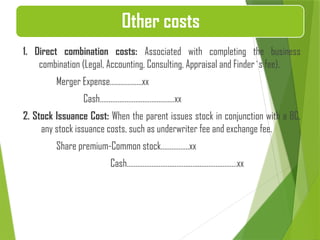

1. Direct combinationcosts: Associated with completing the business

combination (Legal, Accounting, Consulting, Appraisal and Finder`s fee).

Merger Expense………………xx

Cash……………………………………xx

2. Stock Issuance Cost: When the parent issues stock in conjunction with a BC,

any stock issuance costs, such as underwriter fee and exchange fee.

Share premium-Common stock…………….xx

Cash…………………………………..…………………xx

Other costs

32.

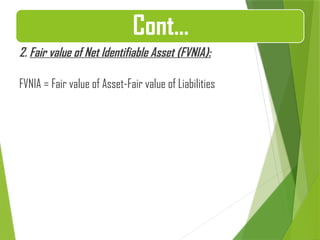

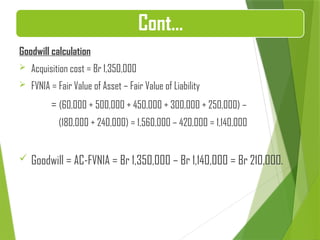

2. Fair valueof Net Identifiable Asset (FVNIA):

FVNIA = Fair value of Asset-Fair value of Liabilities

Cont…

33.

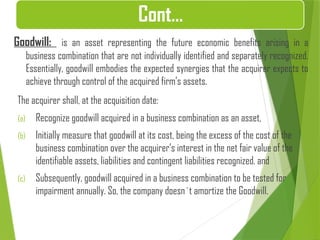

Goodwill: is anasset representing the future economic benefits arising in a

business combination that are not individually identified and separately recognized.

Essentially, goodwill embodies the expected synergies that the acquirer expects to

achieve through control of the acquired firm’s assets.

The acquirer shall, at the acquisition date:

(a) Recognize goodwill acquired in a business combination as an asset,

(b) Initially measure that goodwill at its cost, being the excess of the cost of the

business combination over the acquirer’s interest in the net fair value of the

identifiable assets, liabilities and contingent liabilities recognized. and

(c) Subsequently, goodwill acquired in a business combination to be tested for

impairment annually. So, the company doesn`t amortize the Goodwill.

Cont…

34.

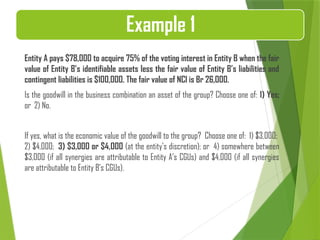

Entity A pays$78,000 to acquire 75% of the voting interest in Entity B when the fair

value of Entity B’s identifiable assets less the fair value of Entity B’s liabilities and

contingent liabilities is $100,000. The fair value of NCI is Br 26,000.

Is the goodwill in the business combination an asset of the group? Choose one of: 1) Yes;

or 2) No.

If yes, what is the economic value of the goodwill to the group? Choose one of: 1) $3,000;

2) $4,000; 3) $3,000 or $4,000 (at the entity’s discretion); or 4) somewhere between

$3,000 (if all synergies are attributable to Entity A’s CGUs) and $4,000 (if all synergies

are attributable to Entity B’s CGUs).

Example 1

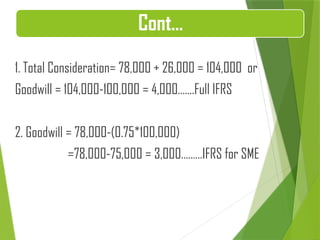

35.

1. Total Consideration=78,000 + 26,000 = 104,000 or

Goodwill = 104,000-100,000 = 4,000…….Full IFRS

2. Goodwill = 78,000-(0.75*100,000)

=78,000-75,000 = 3,000………IFRS for SME

Cont…

36.

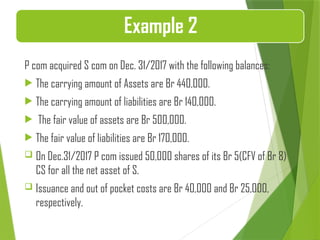

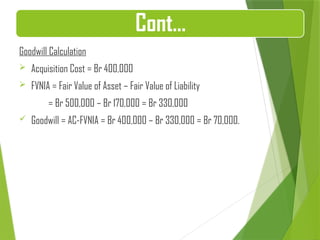

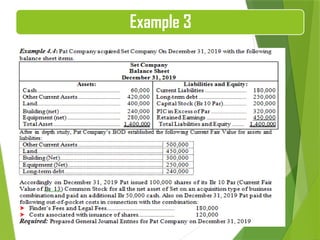

P com acquiredS com on Dec. 31/2017 with the following balances:

The carrying amount of Assets are Br 440,000.

The carrying amount of liabilities are Br 140,000.

The fair value of assets are Br 500,000.

The fair value of liabilities are Br 170,000.

On Dec.31/2017 P com issued 50,000 shares of its Br 5(CFV of Br 8)

CS for all the net asset of S.

Issuance and out of pocket costs are Br 40,000 and Br 25,000,

respectively.

Example 2

37.

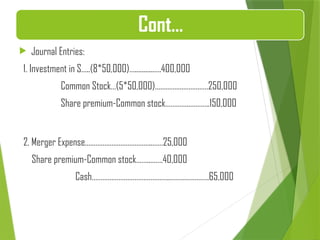

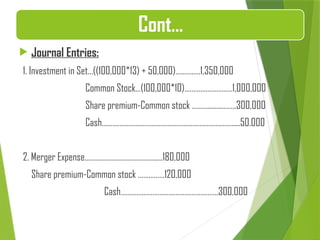

Journal Entries:

1.Investment in S…..(8*50,000)…...........….400,000

Common Stock…(5*50,000)…………………………250,000

Share premium-Common stock…………..………..150,000

2. Merger Expense………………………………..……25,000

Share premium-Common stock……..…….40,000

Cash……………………………………..………………….65,000

Cont…