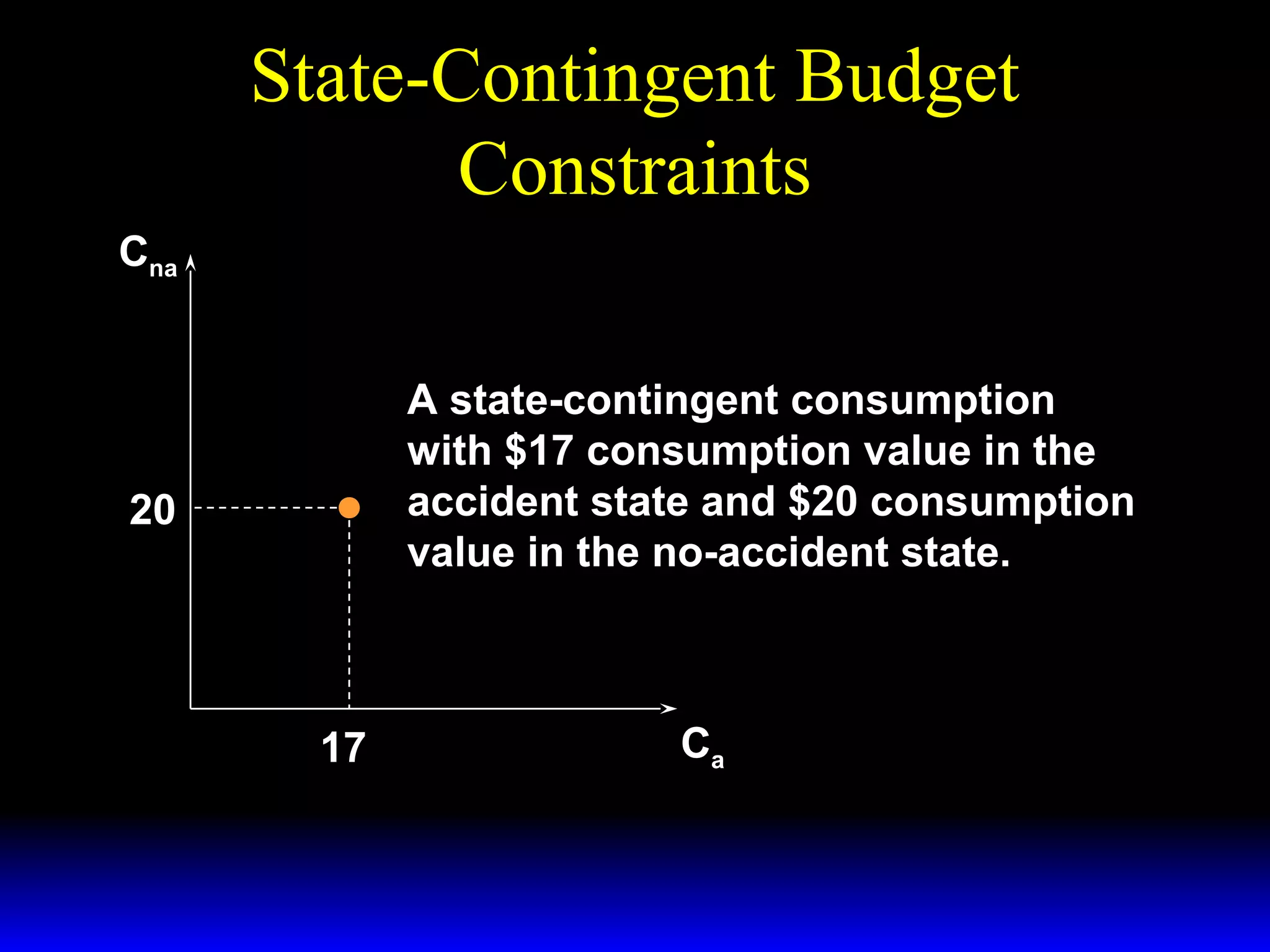

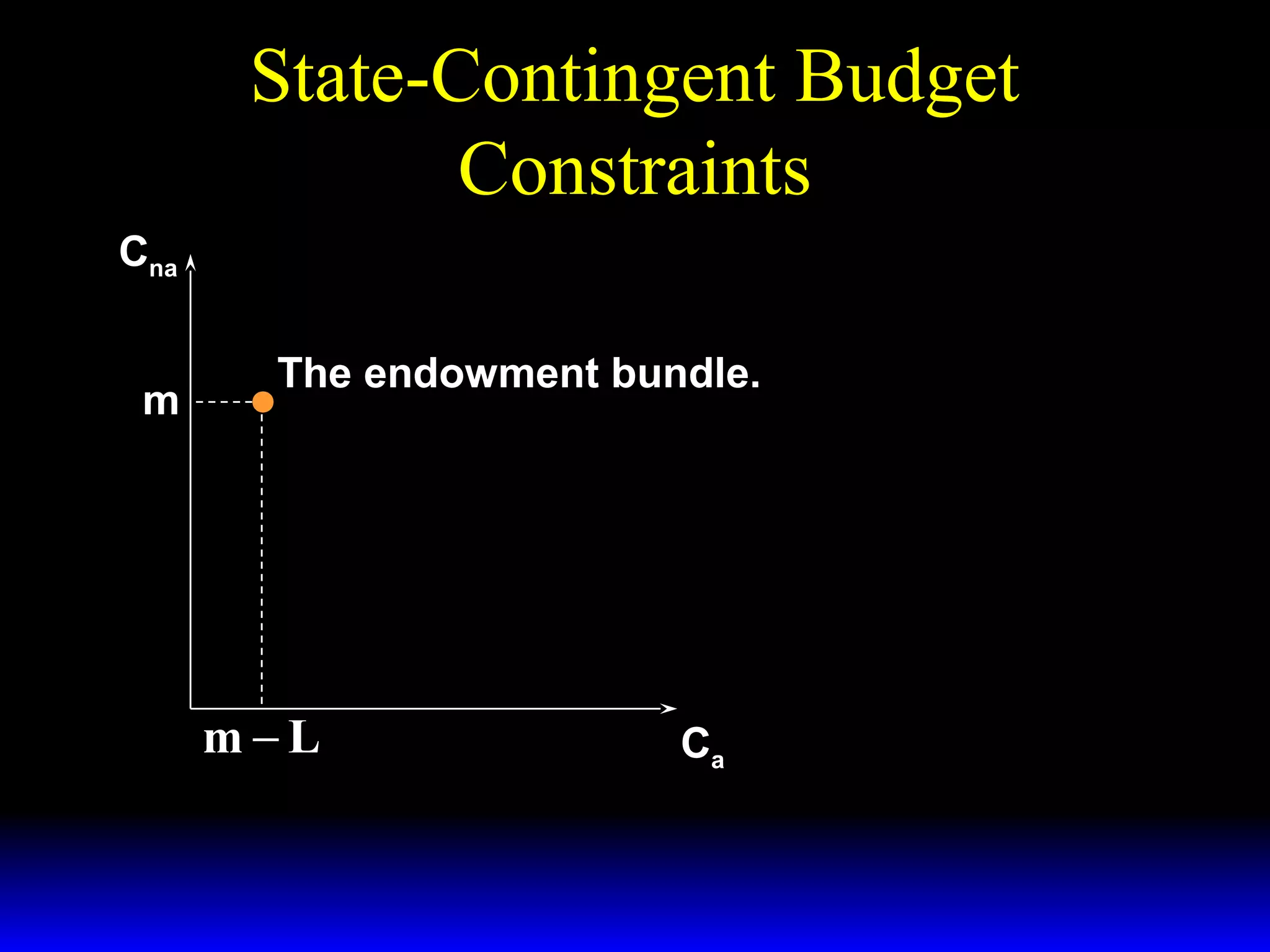

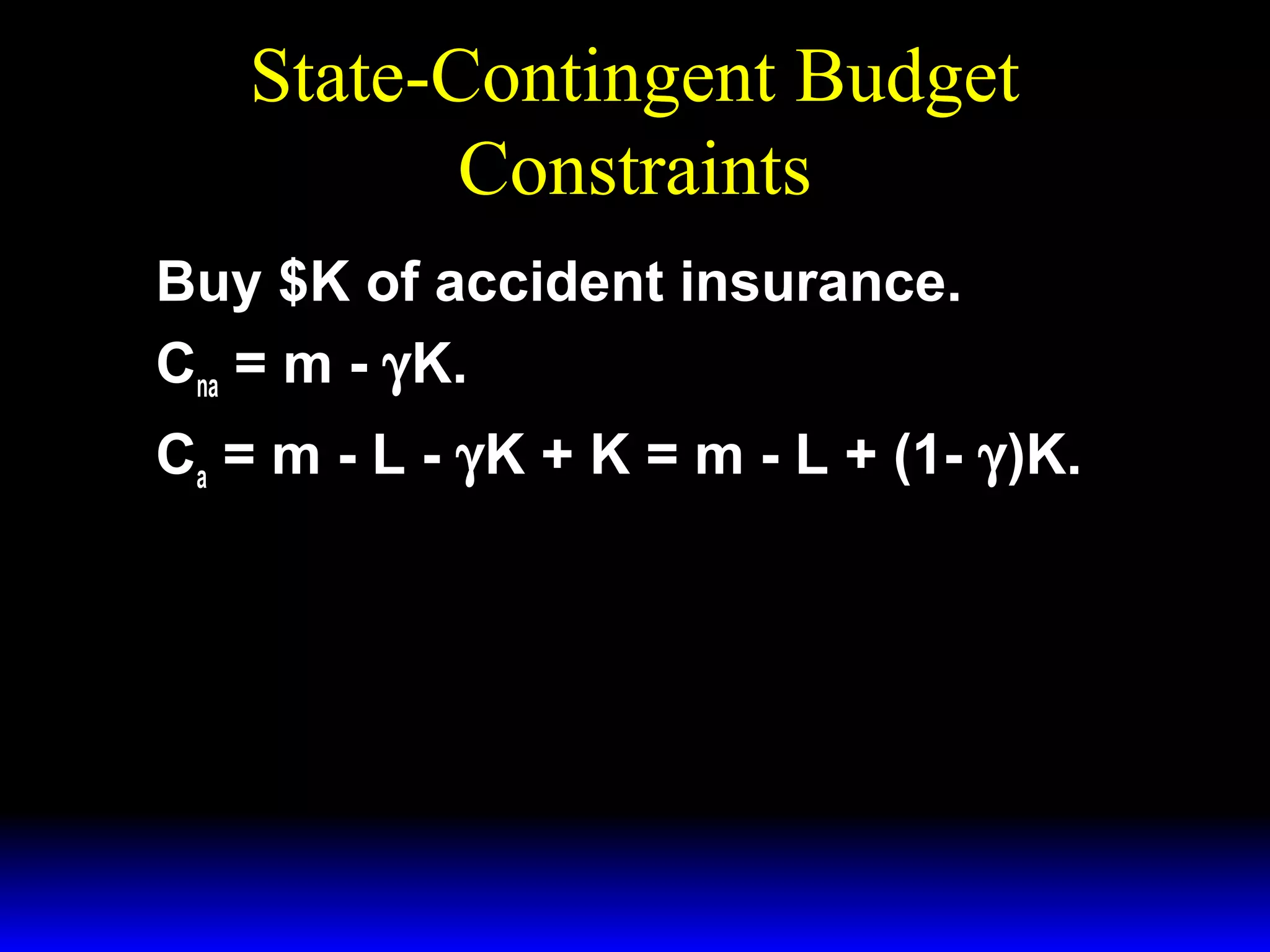

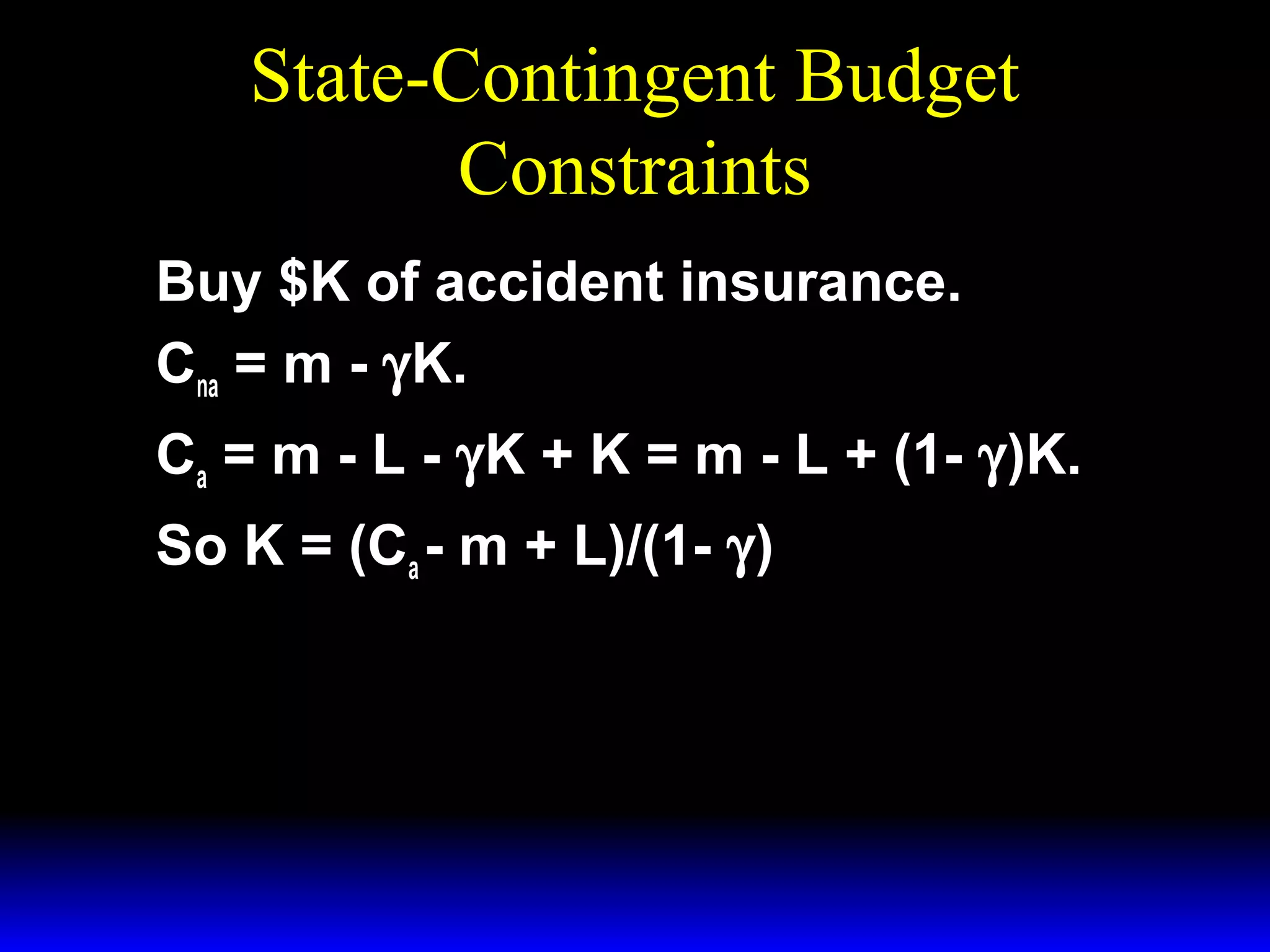

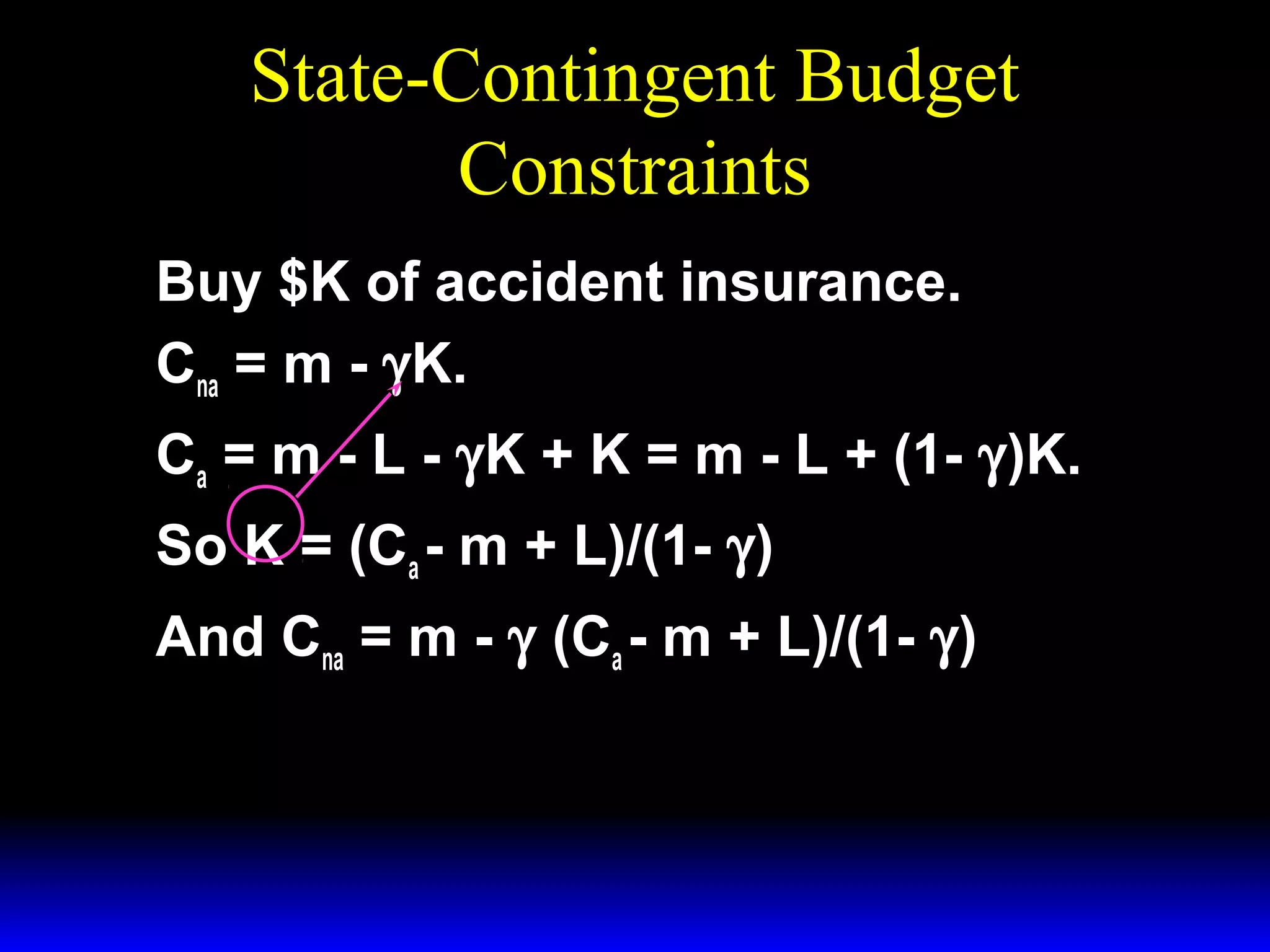

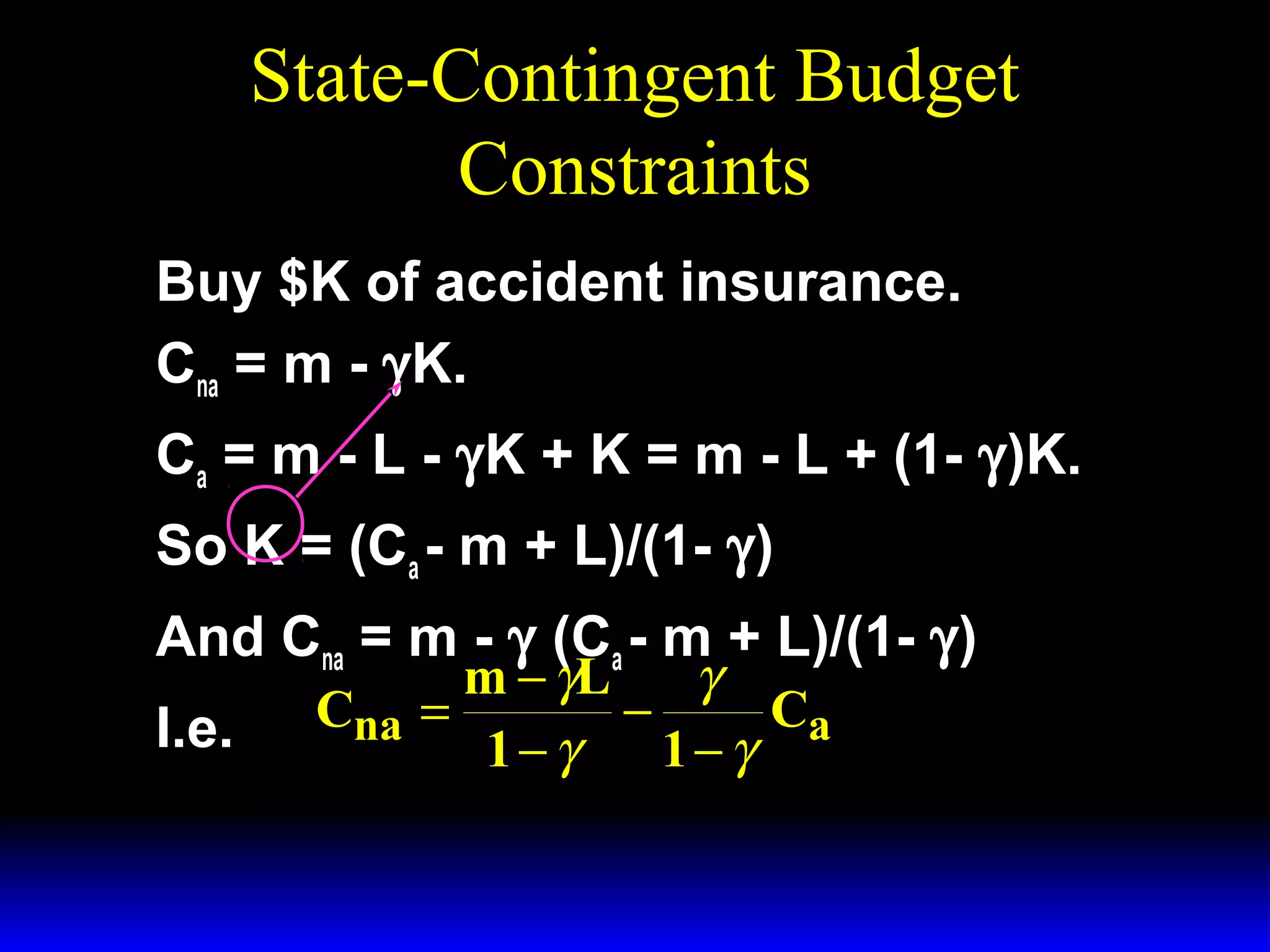

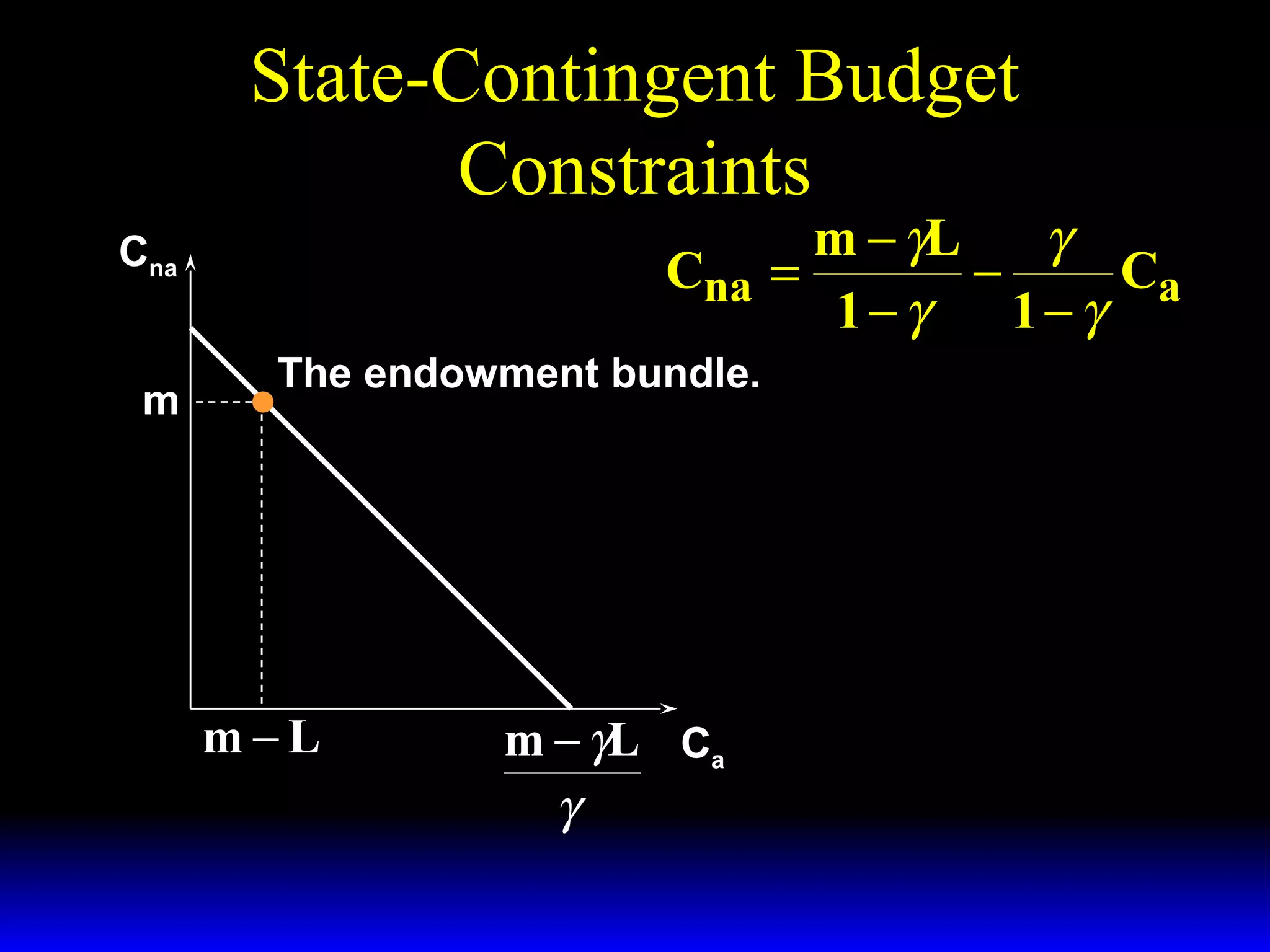

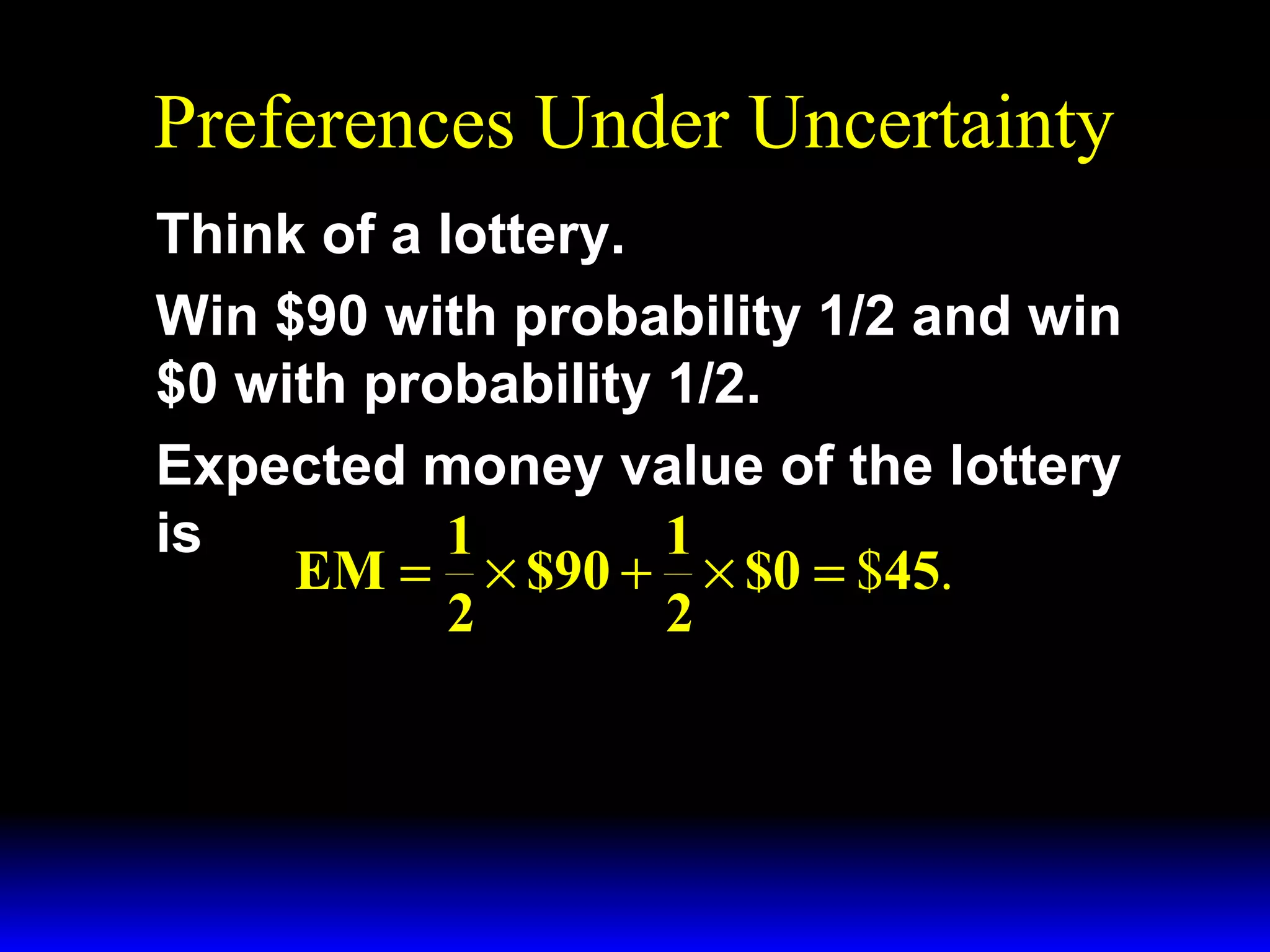

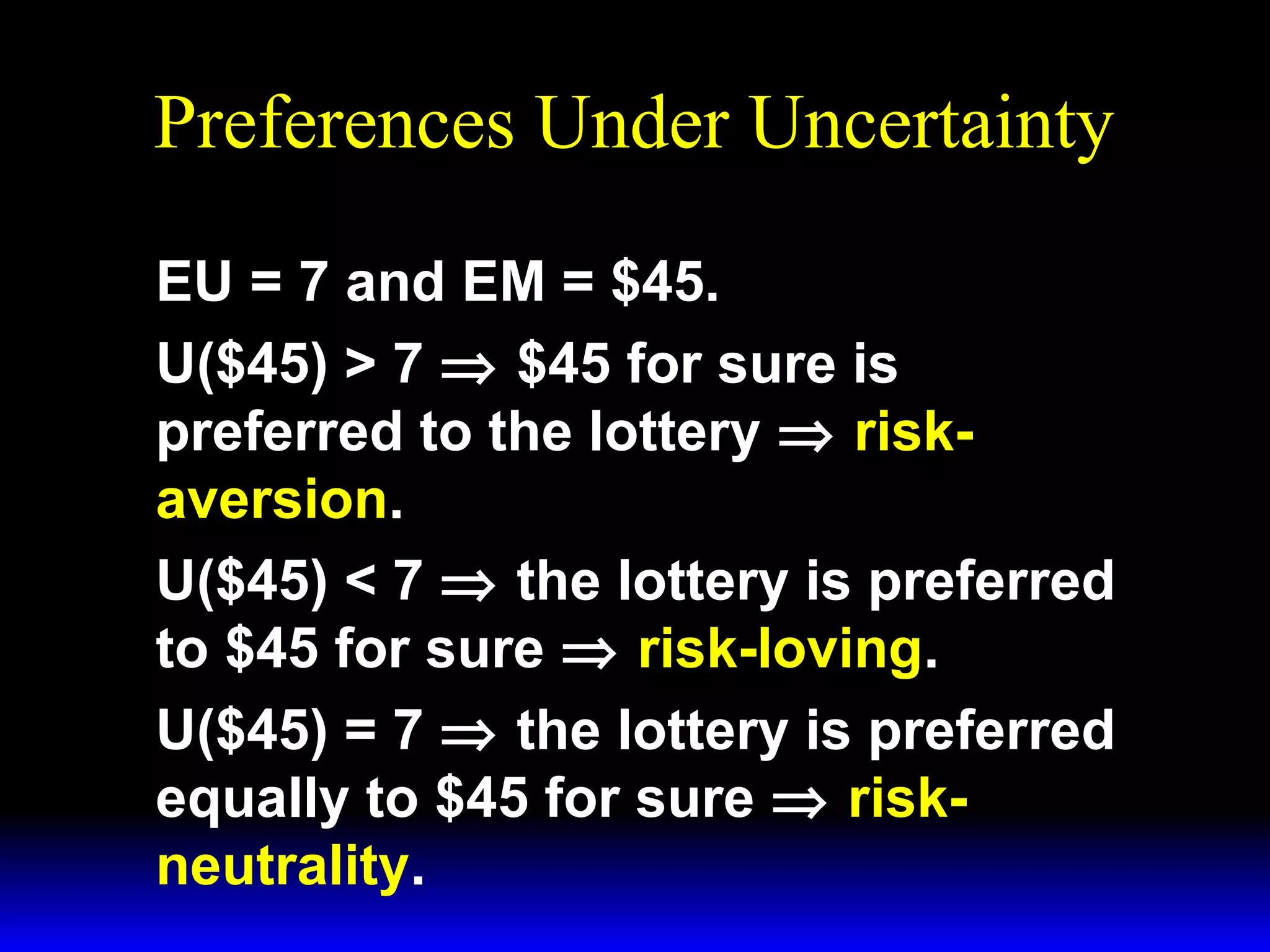

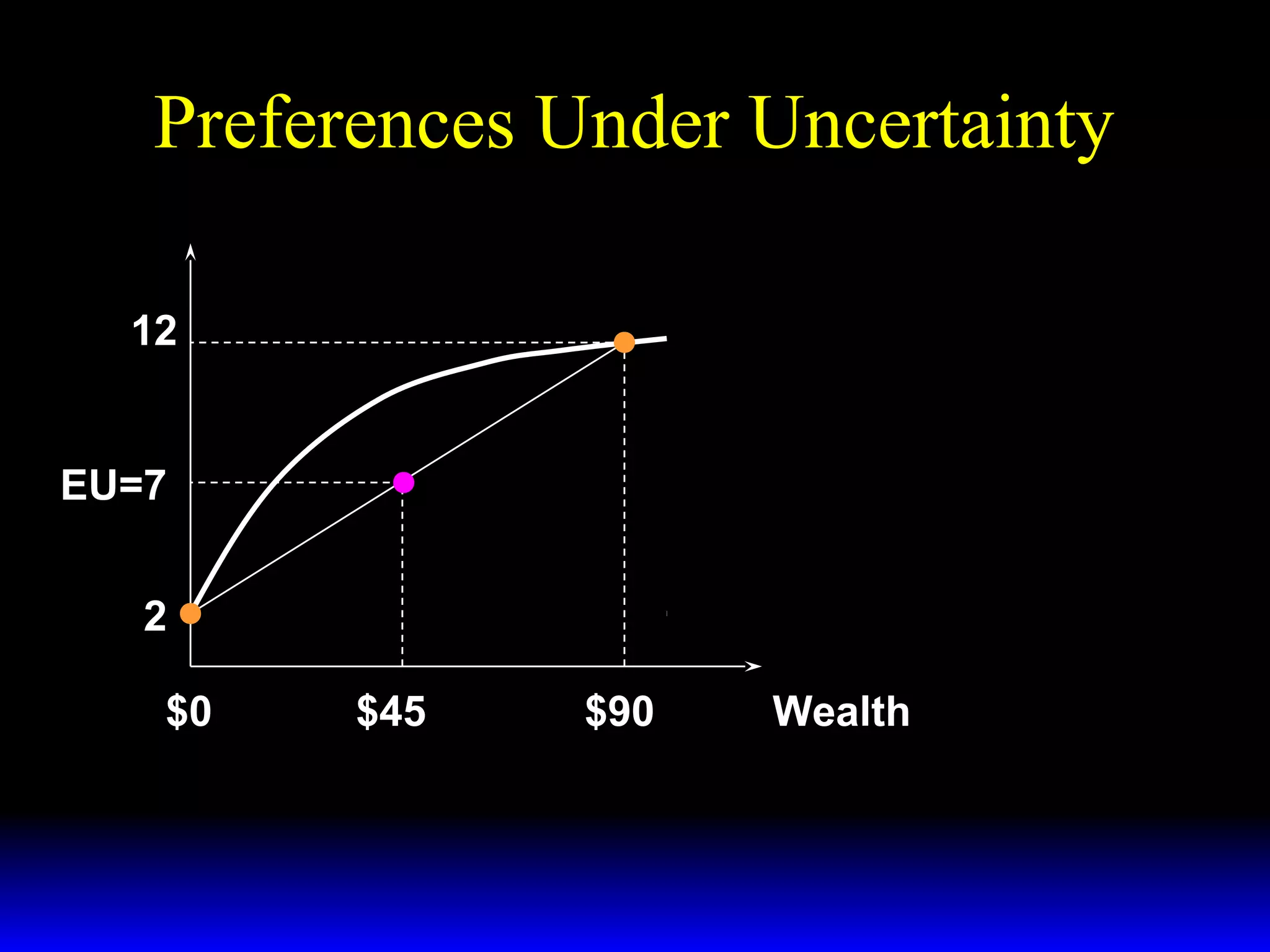

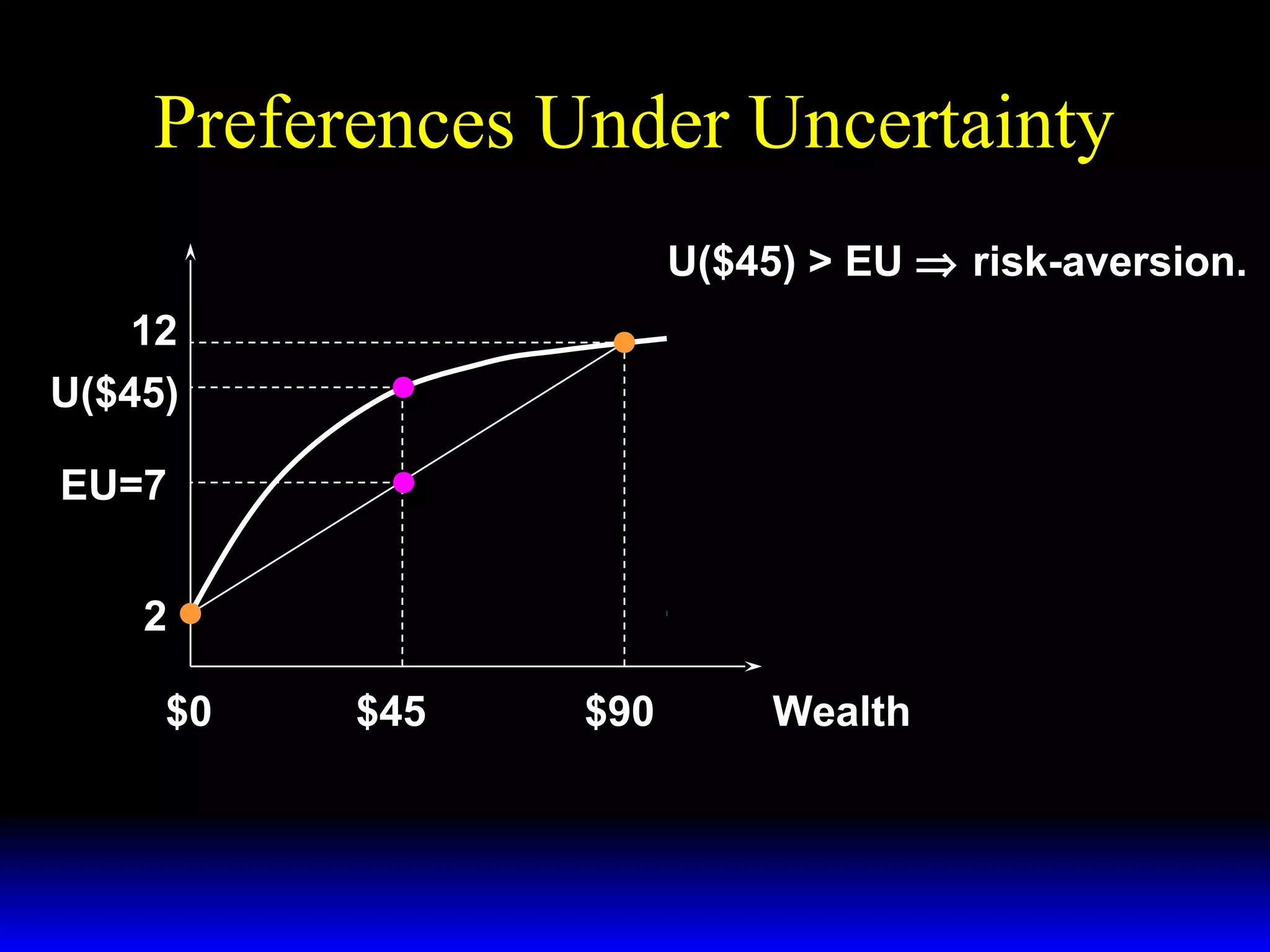

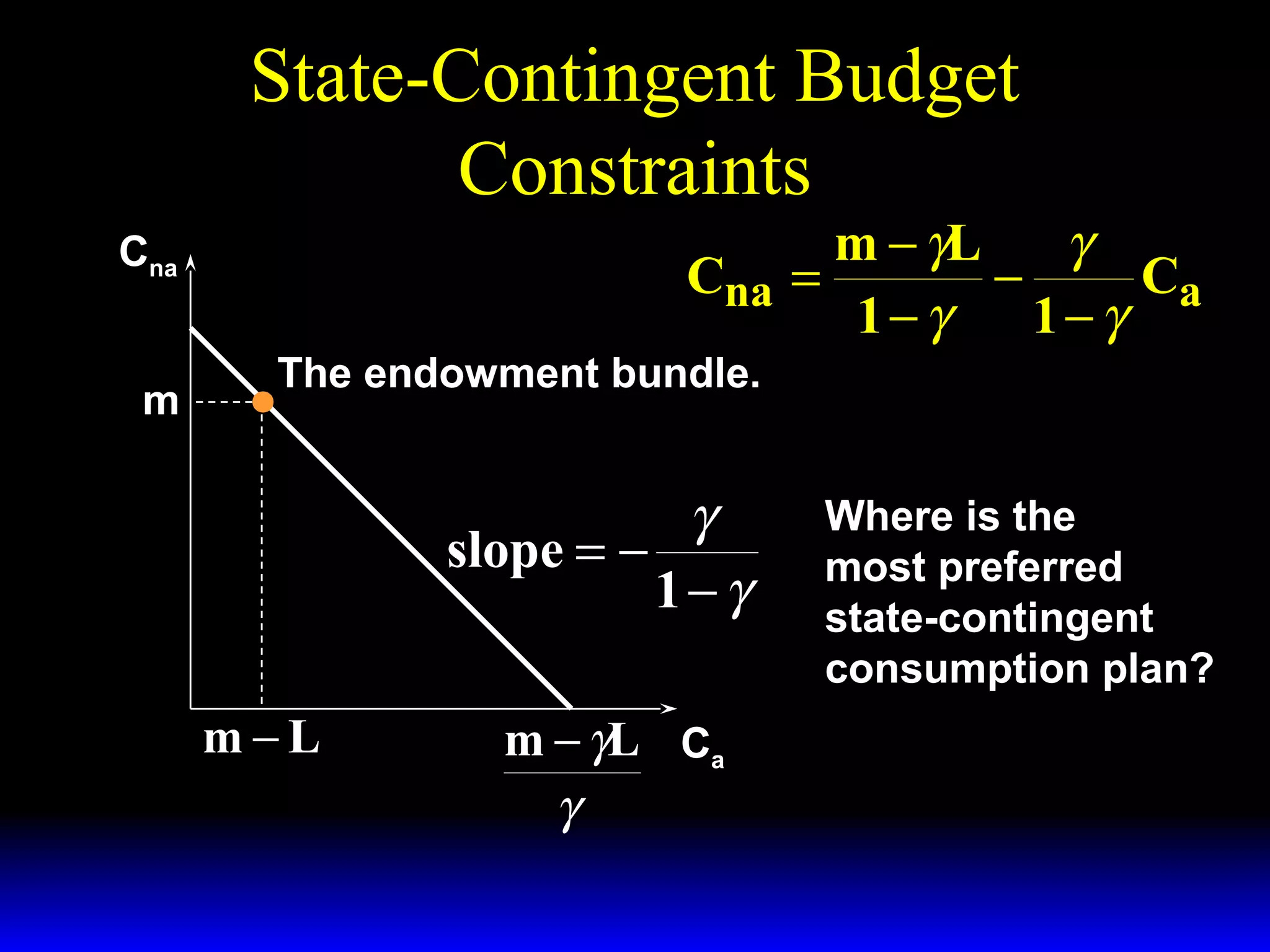

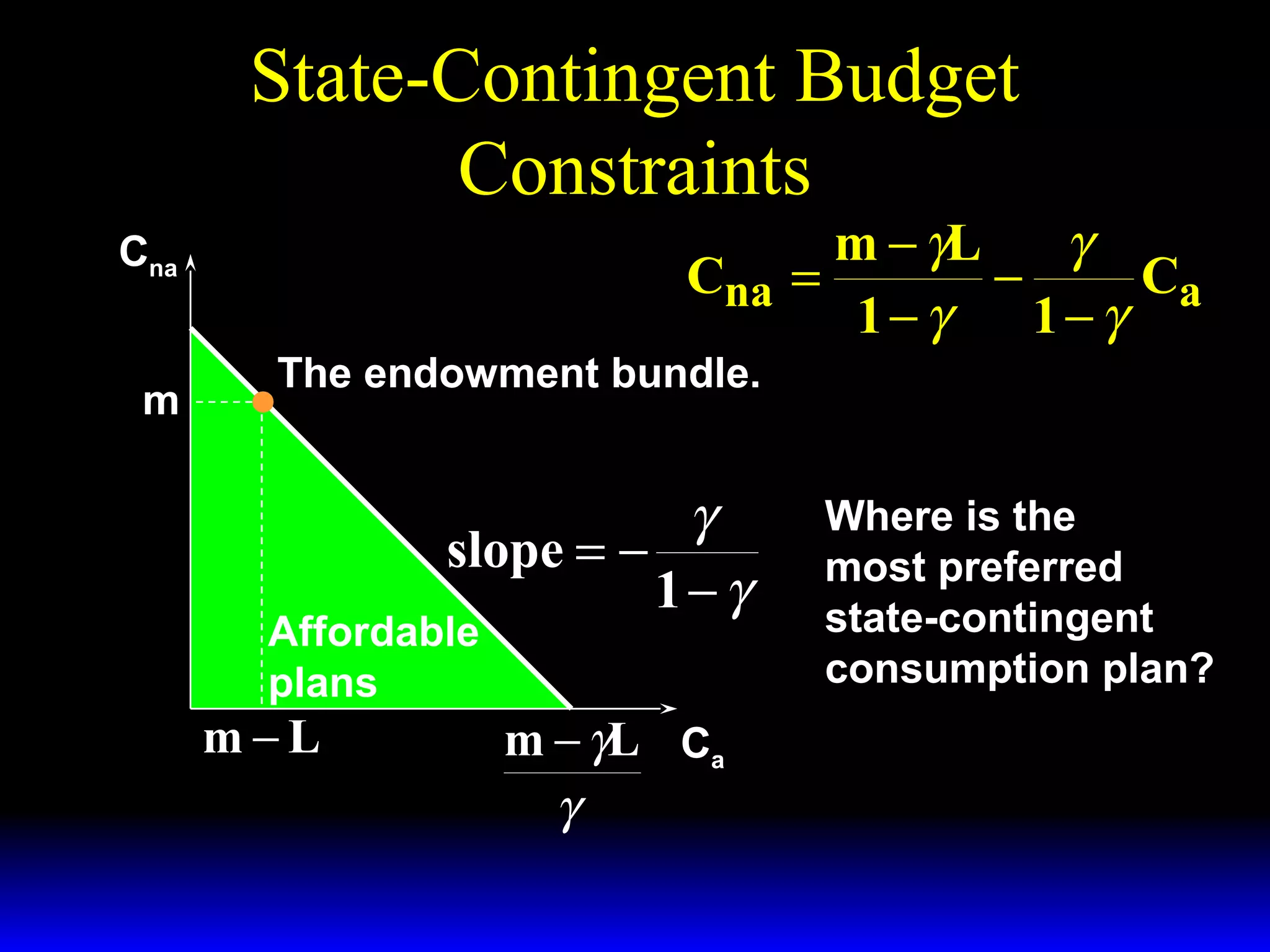

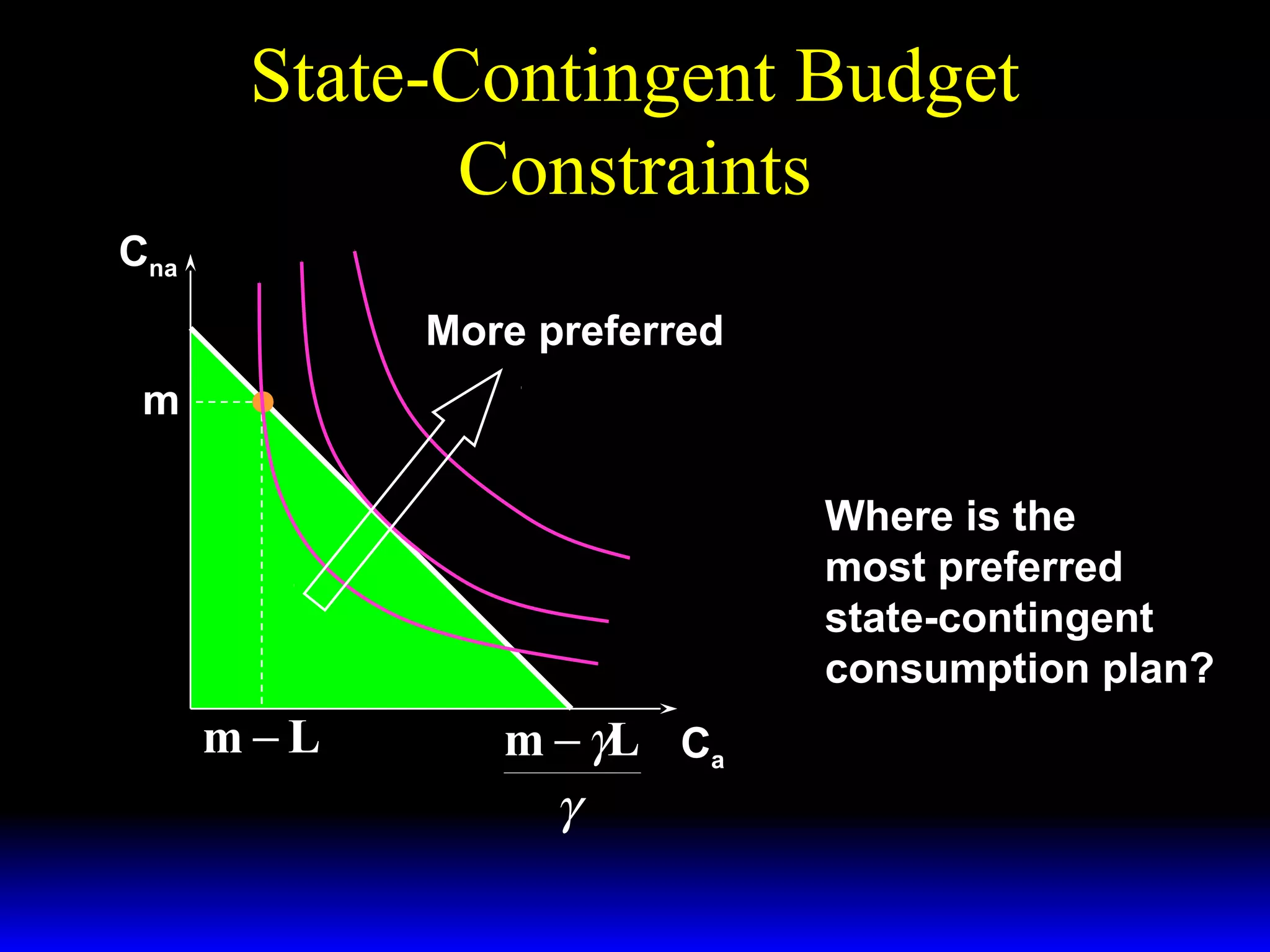

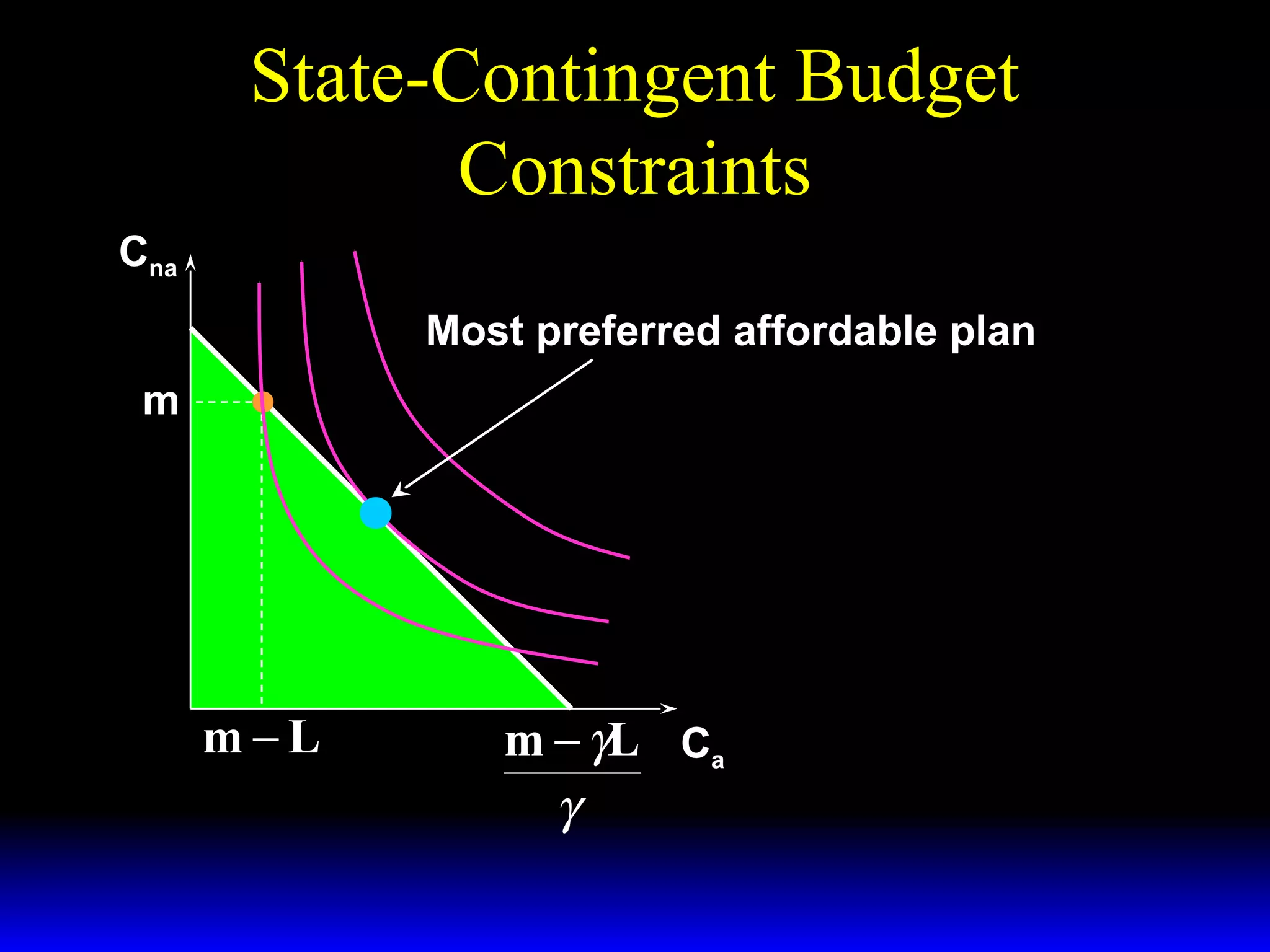

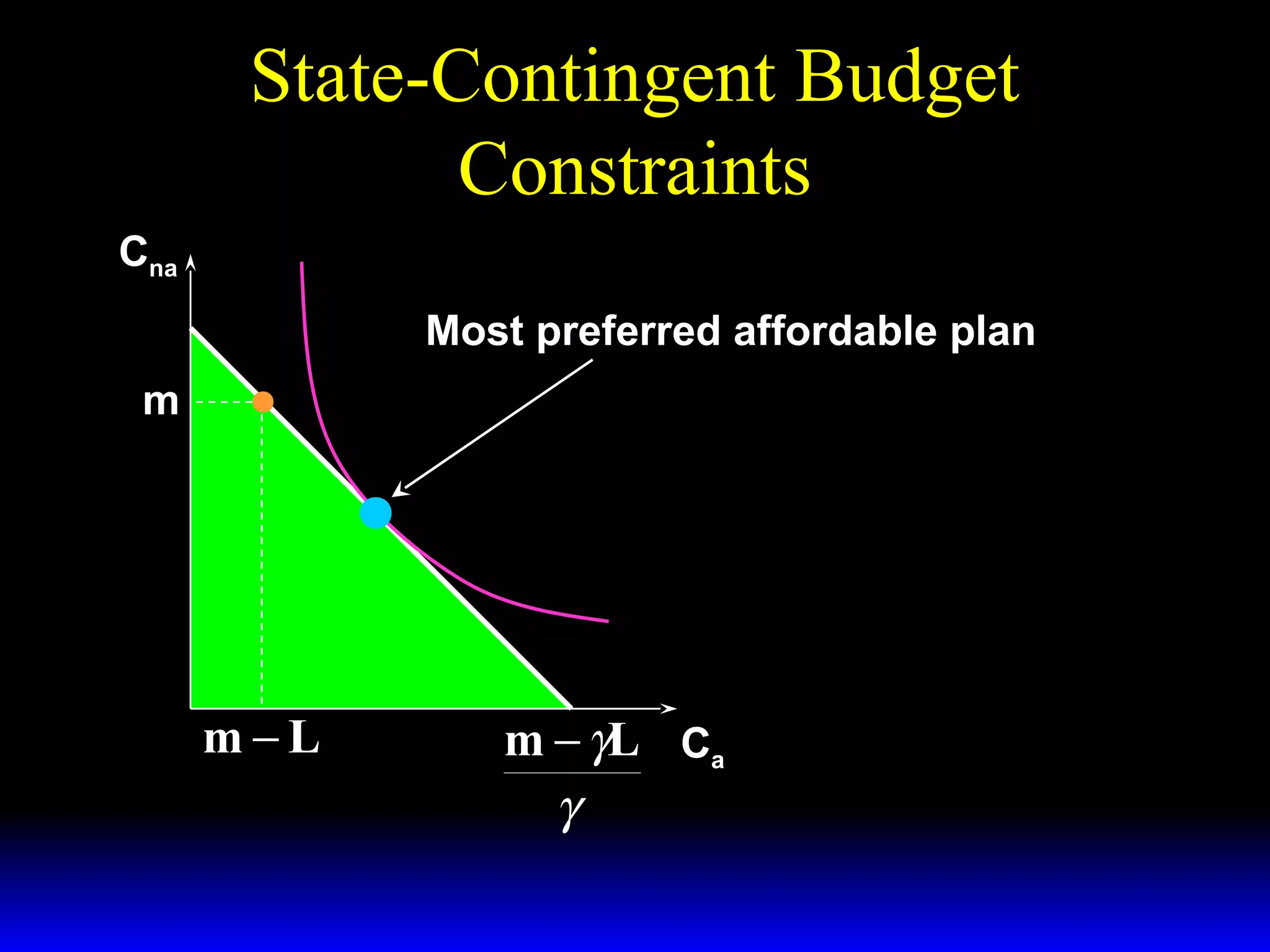

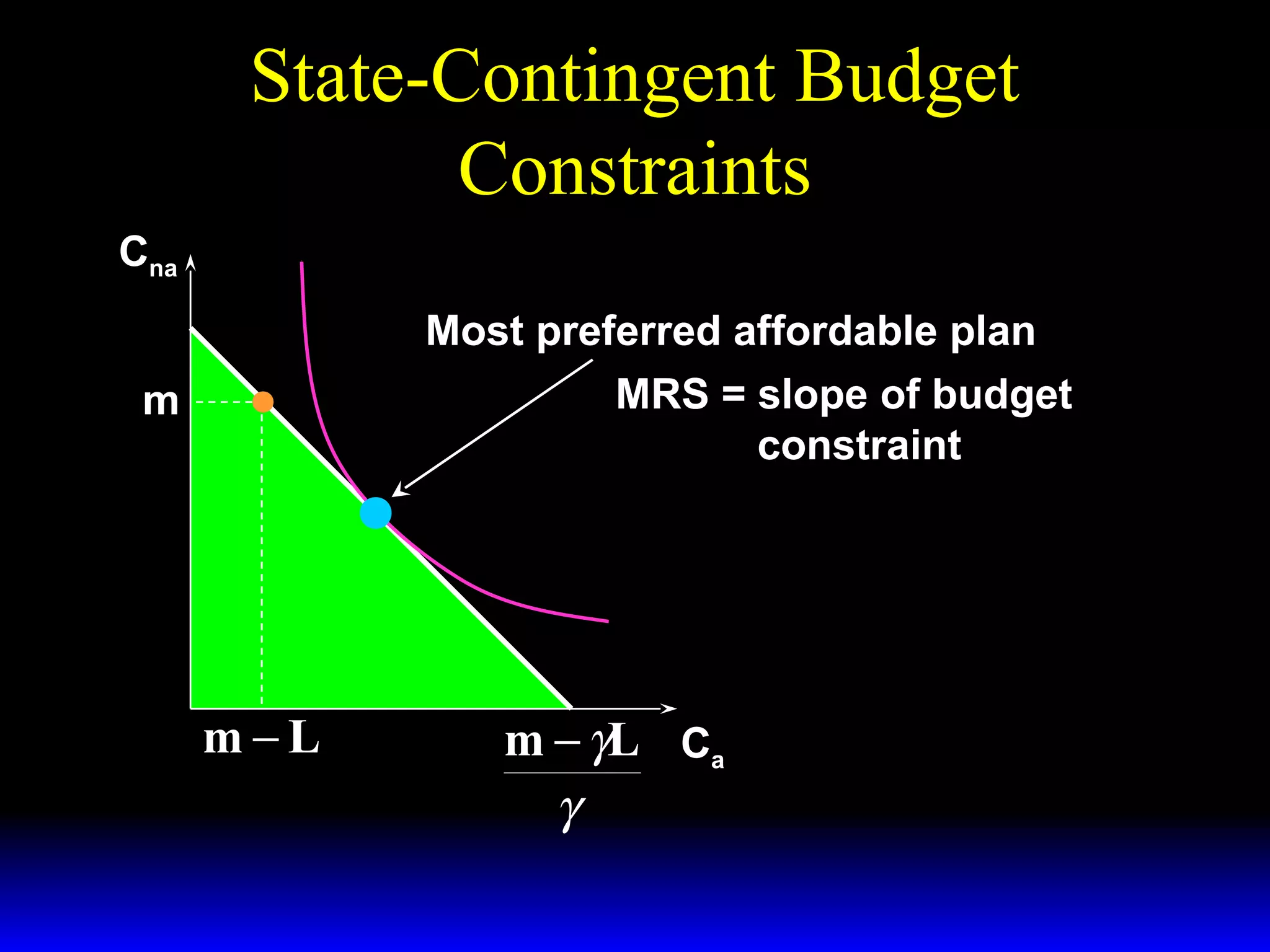

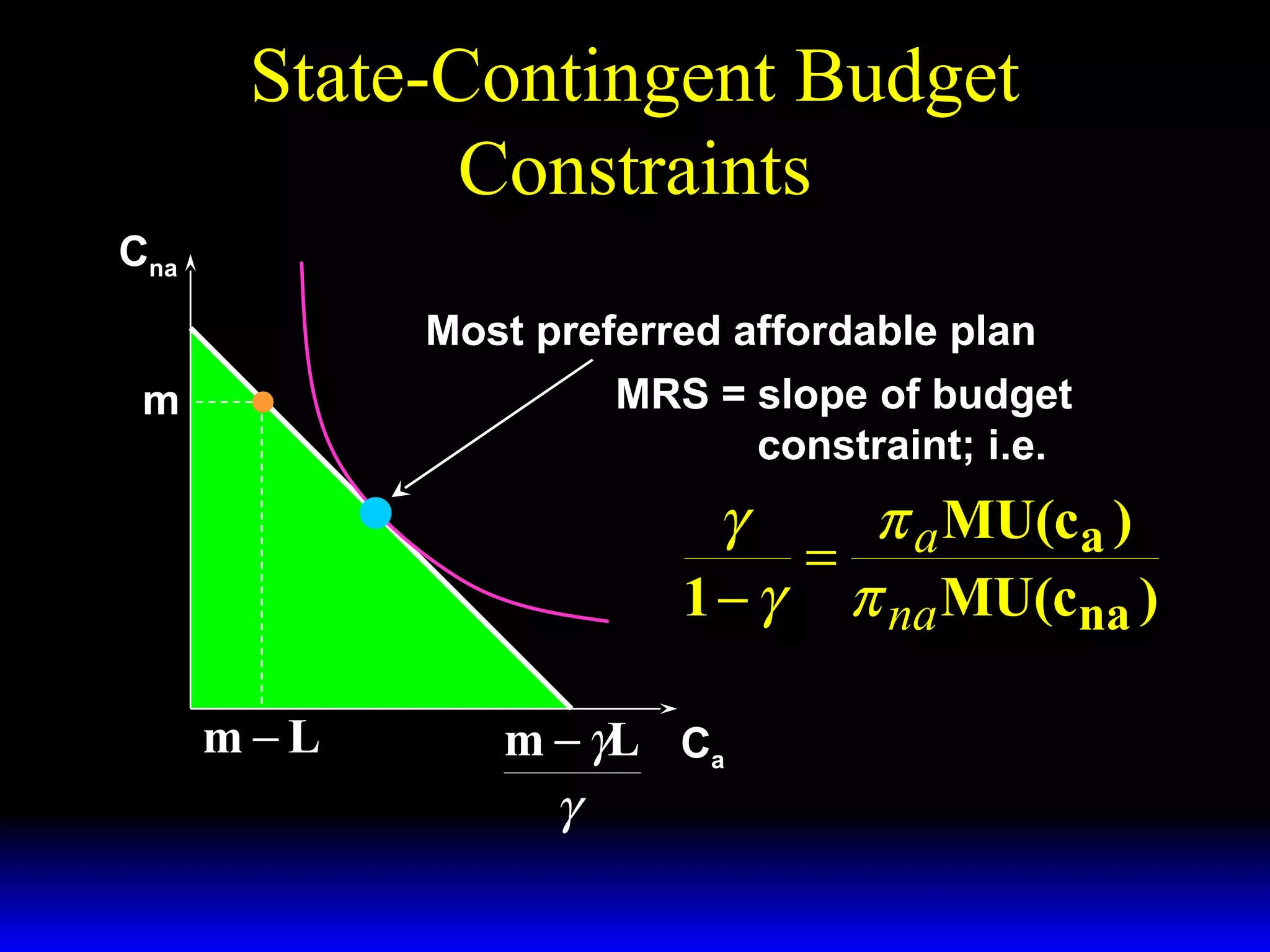

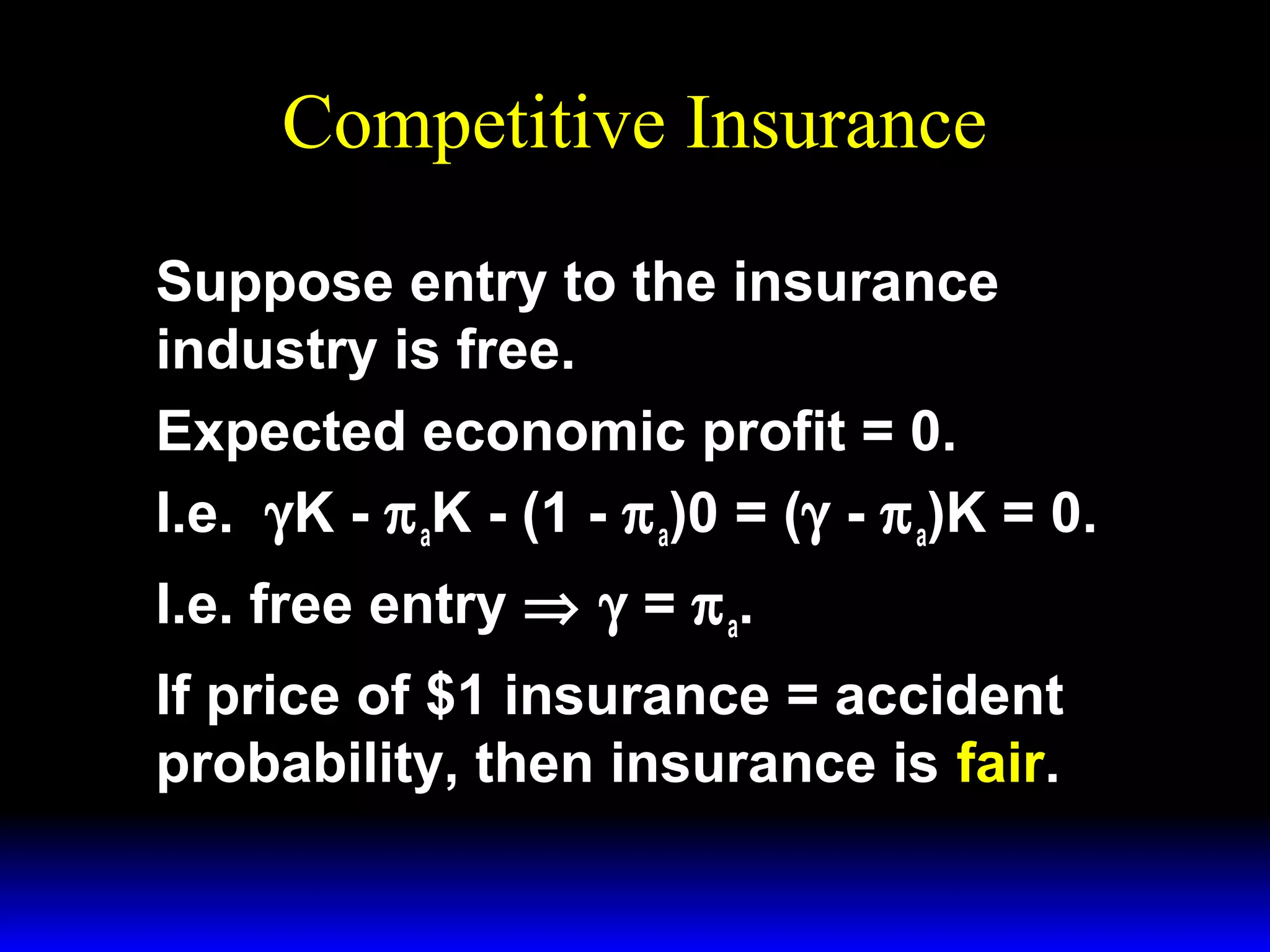

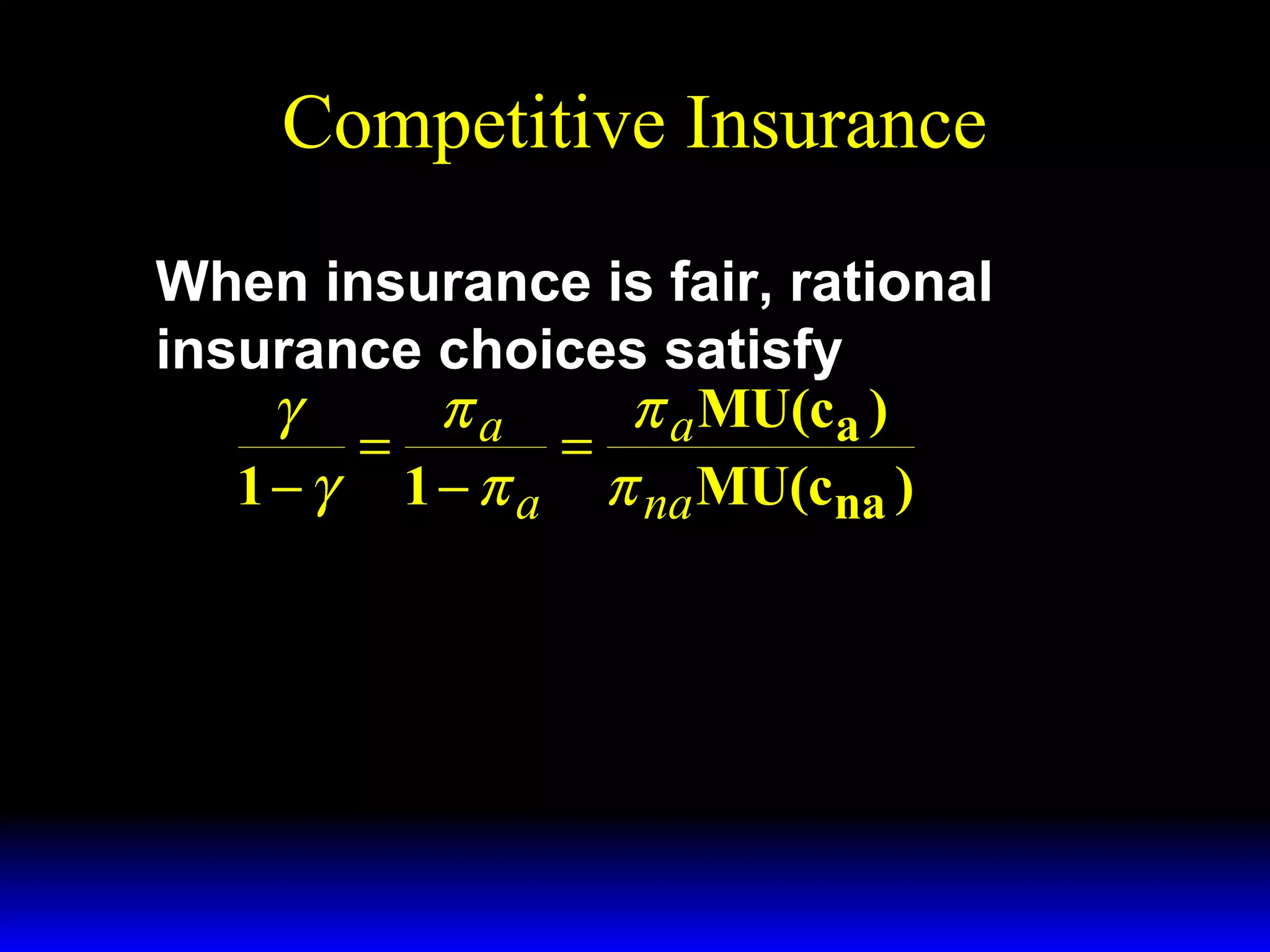

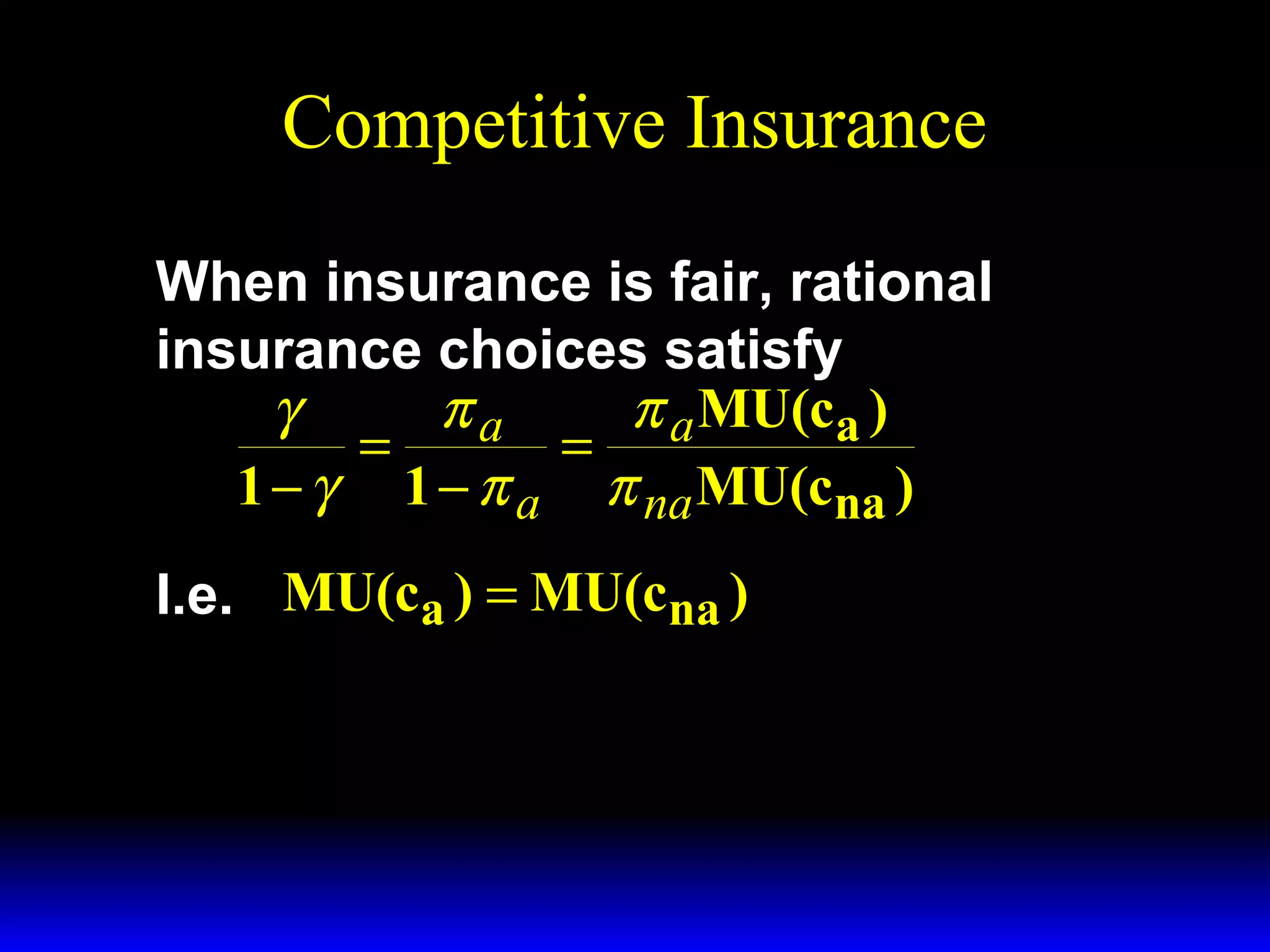

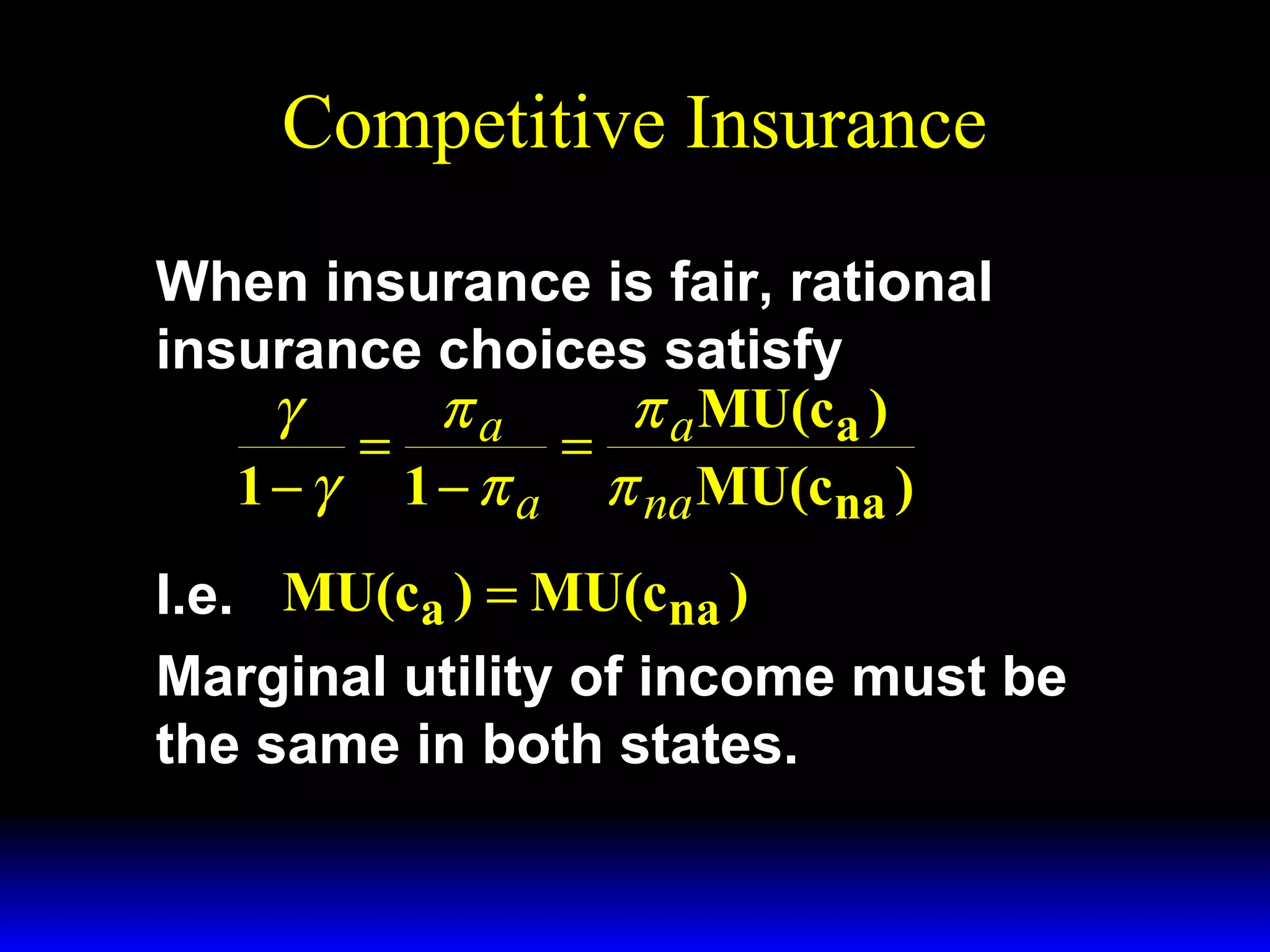

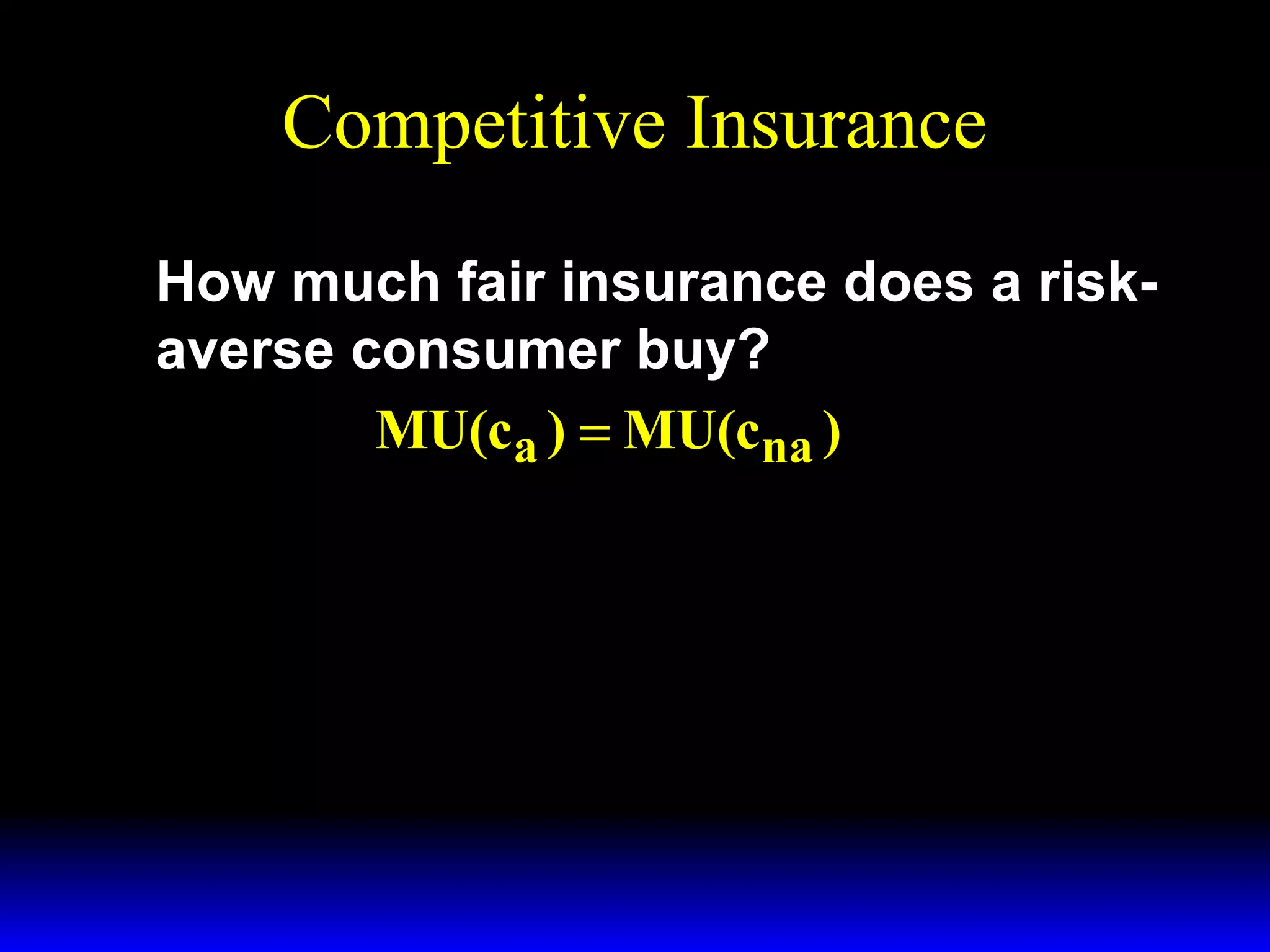

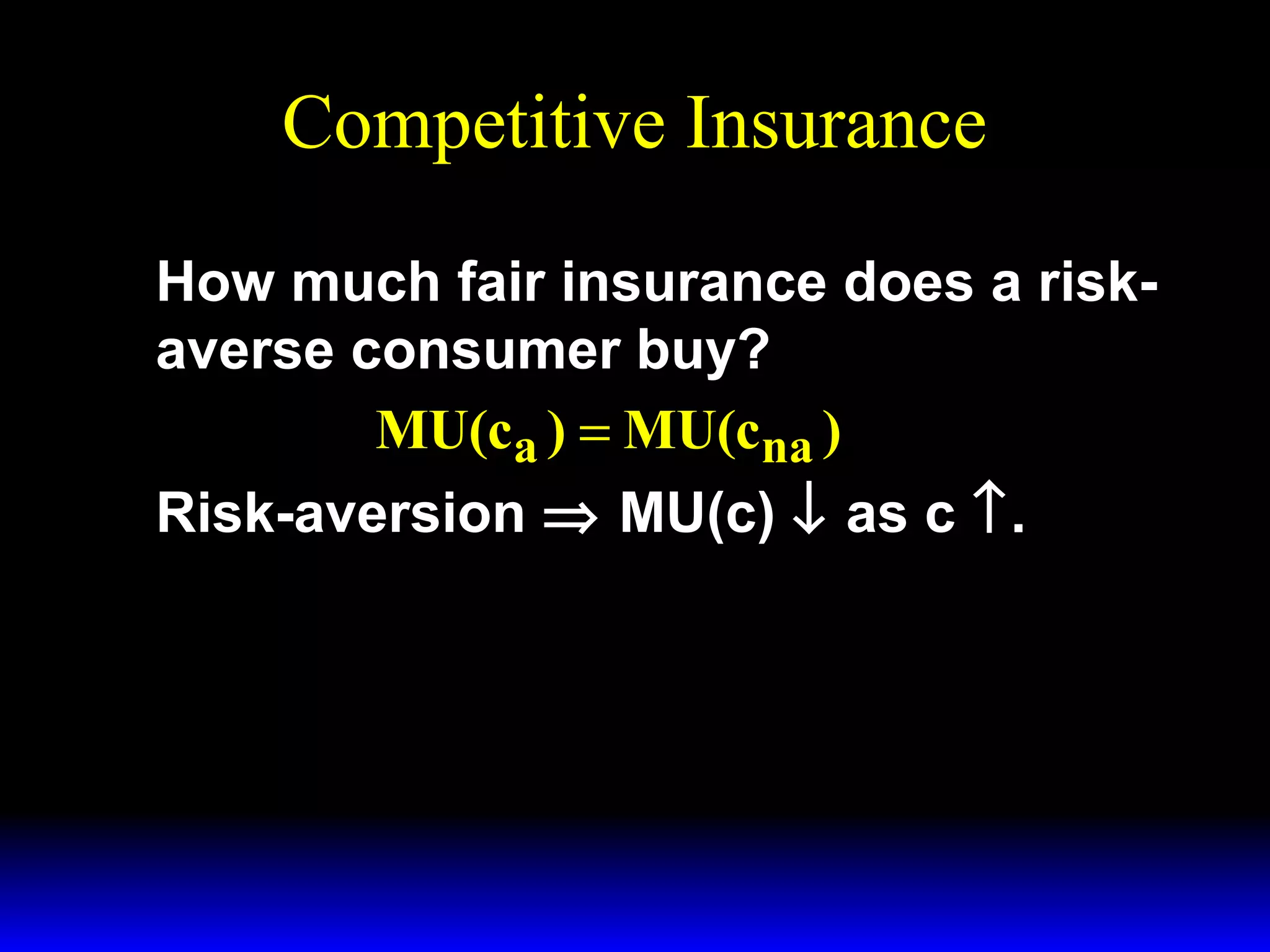

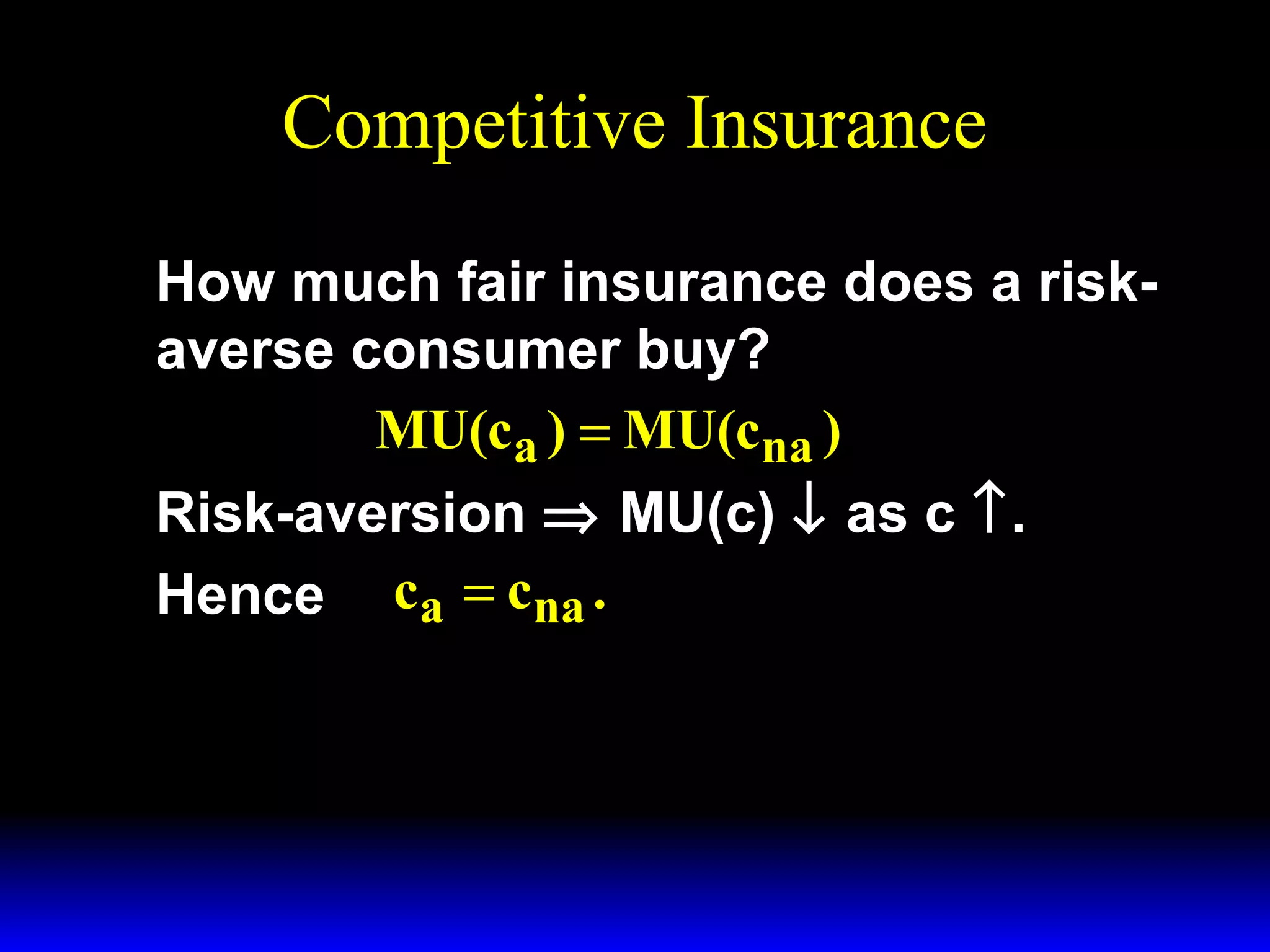

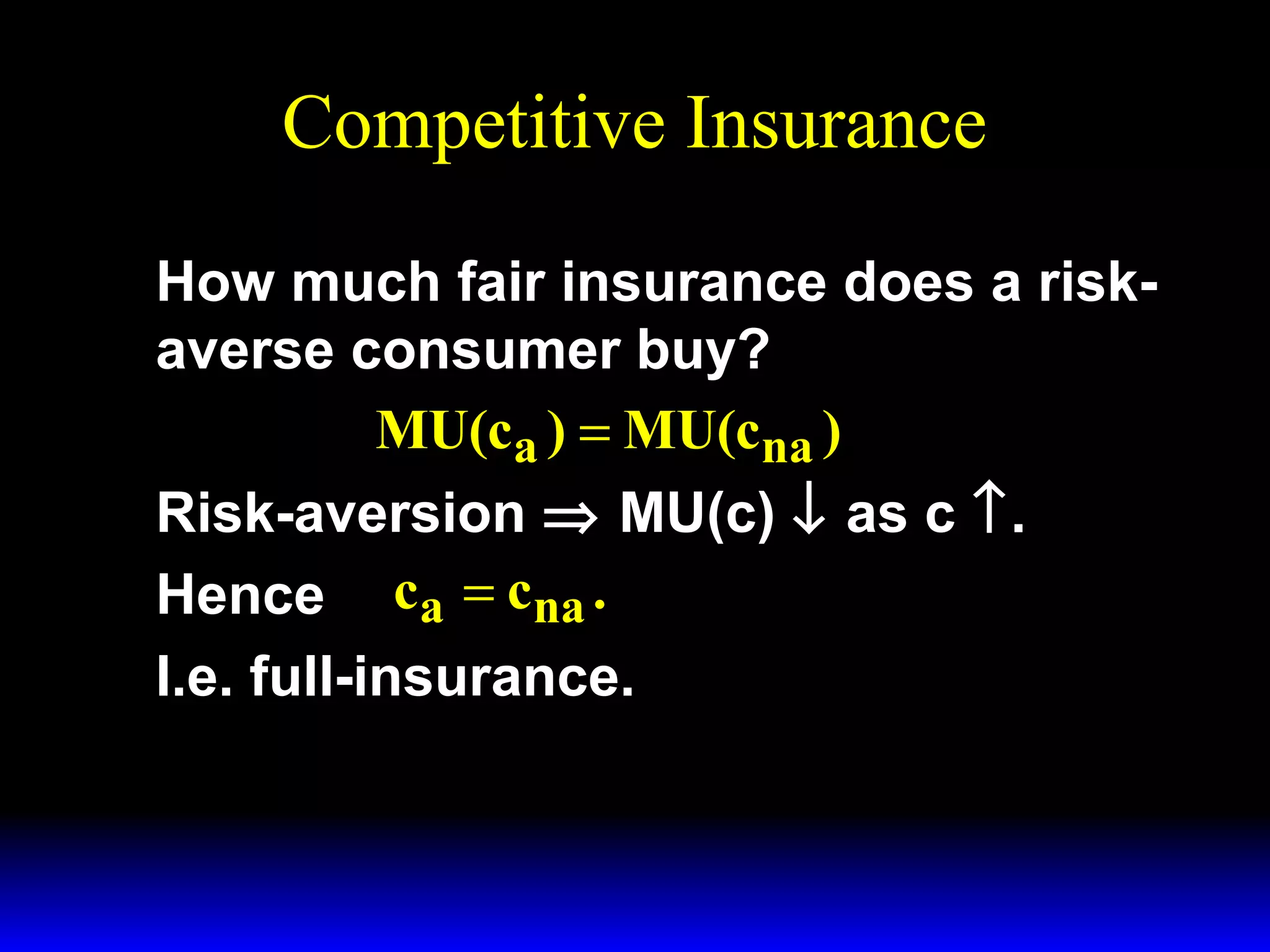

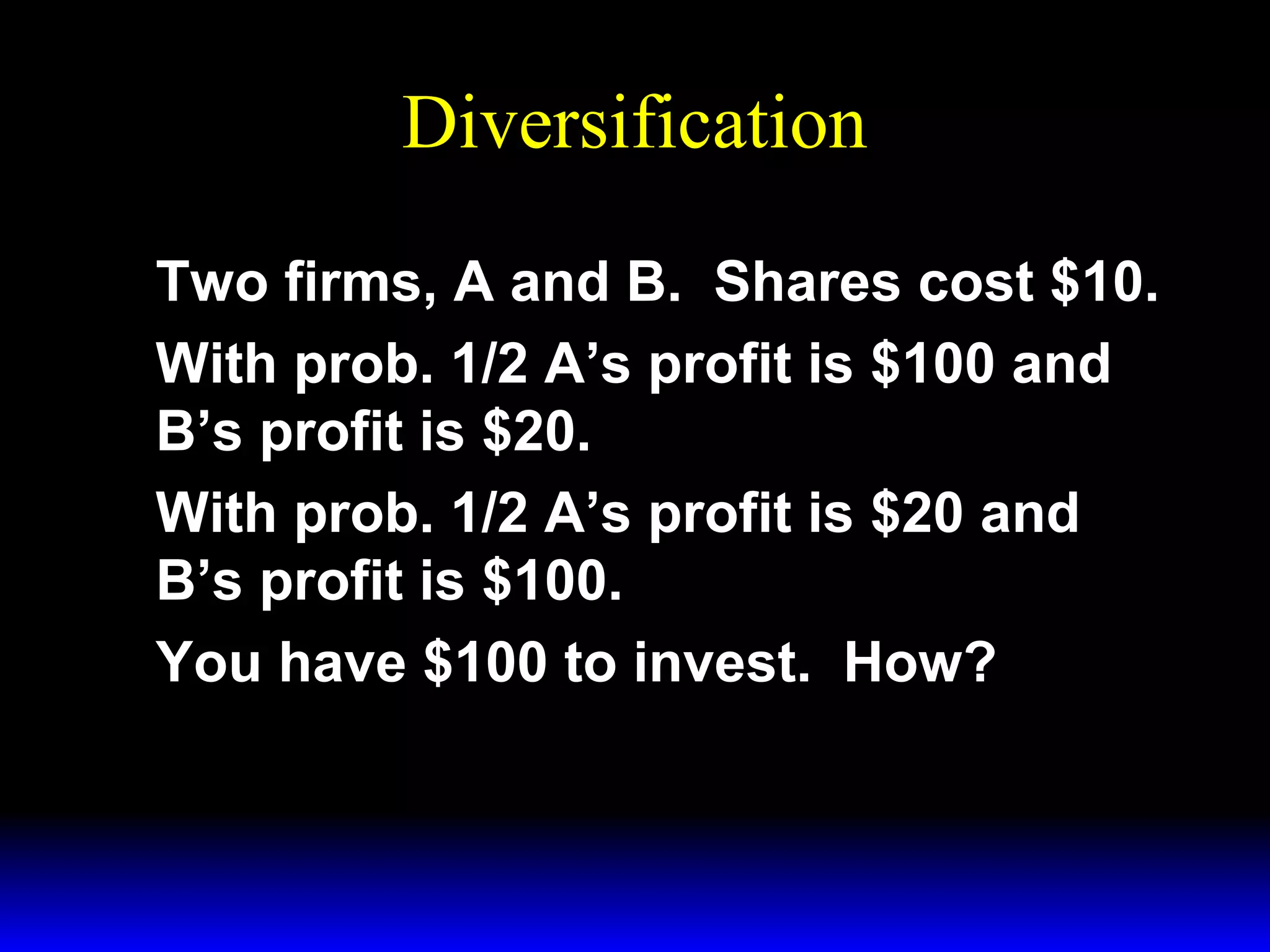

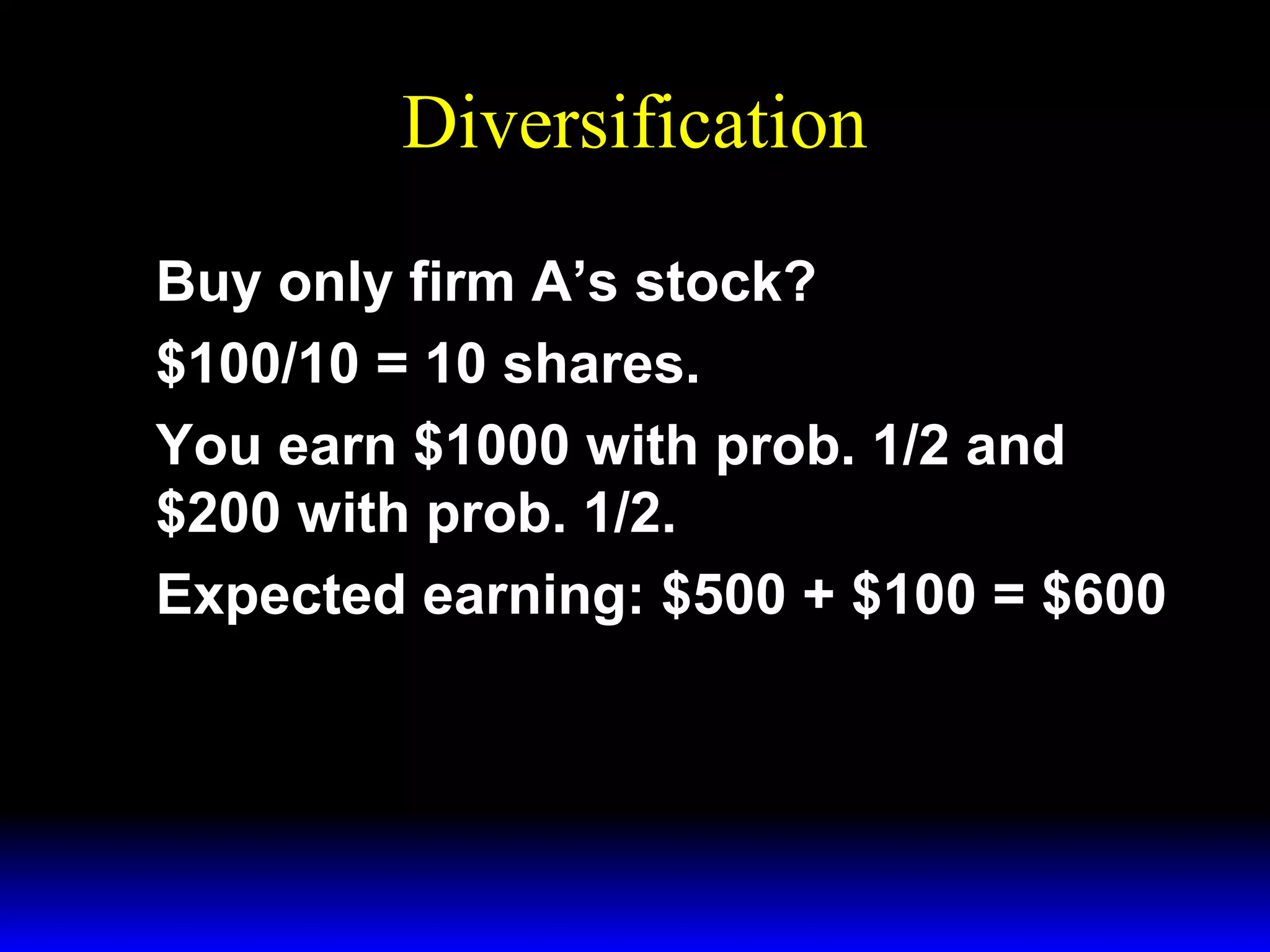

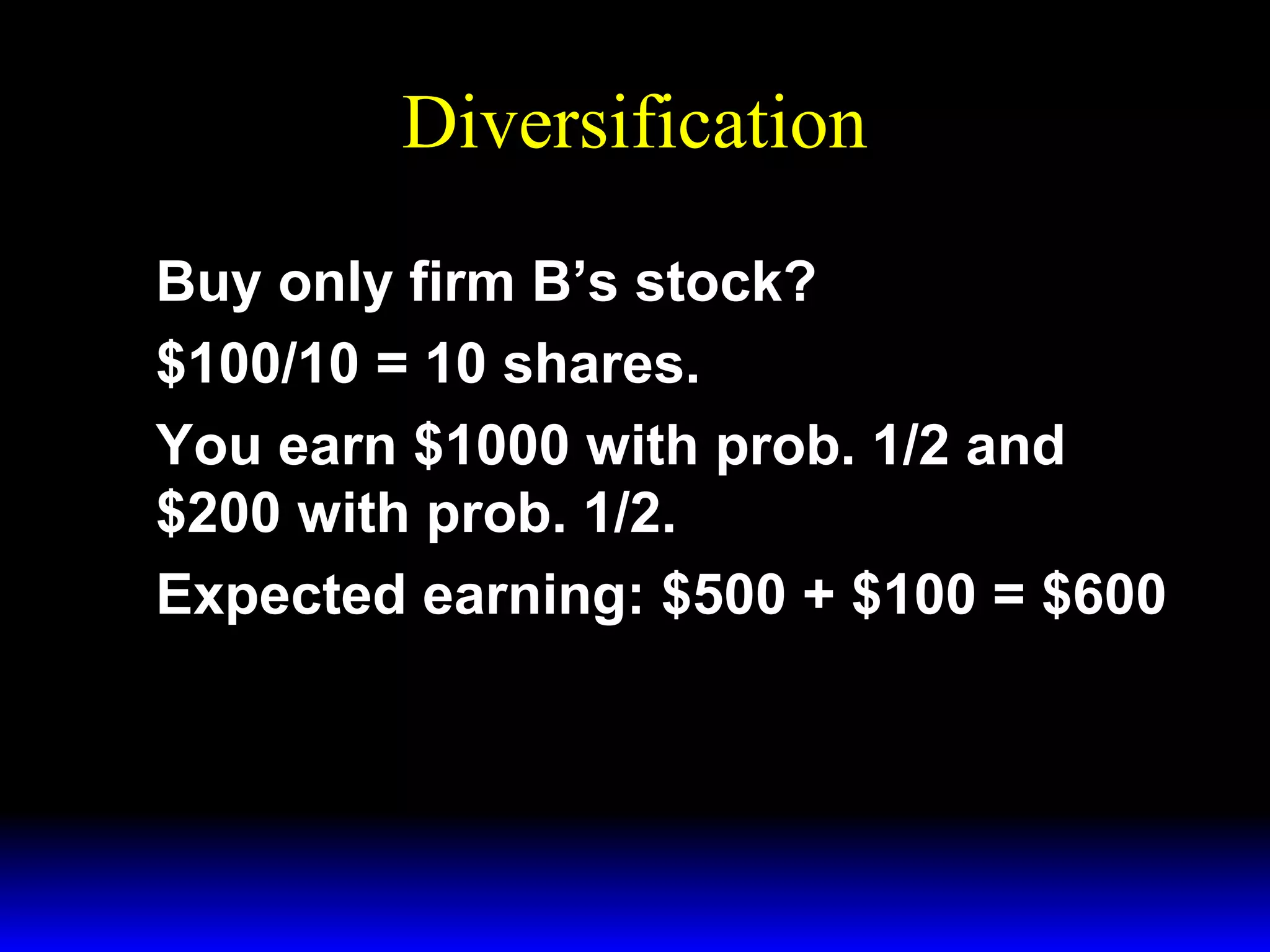

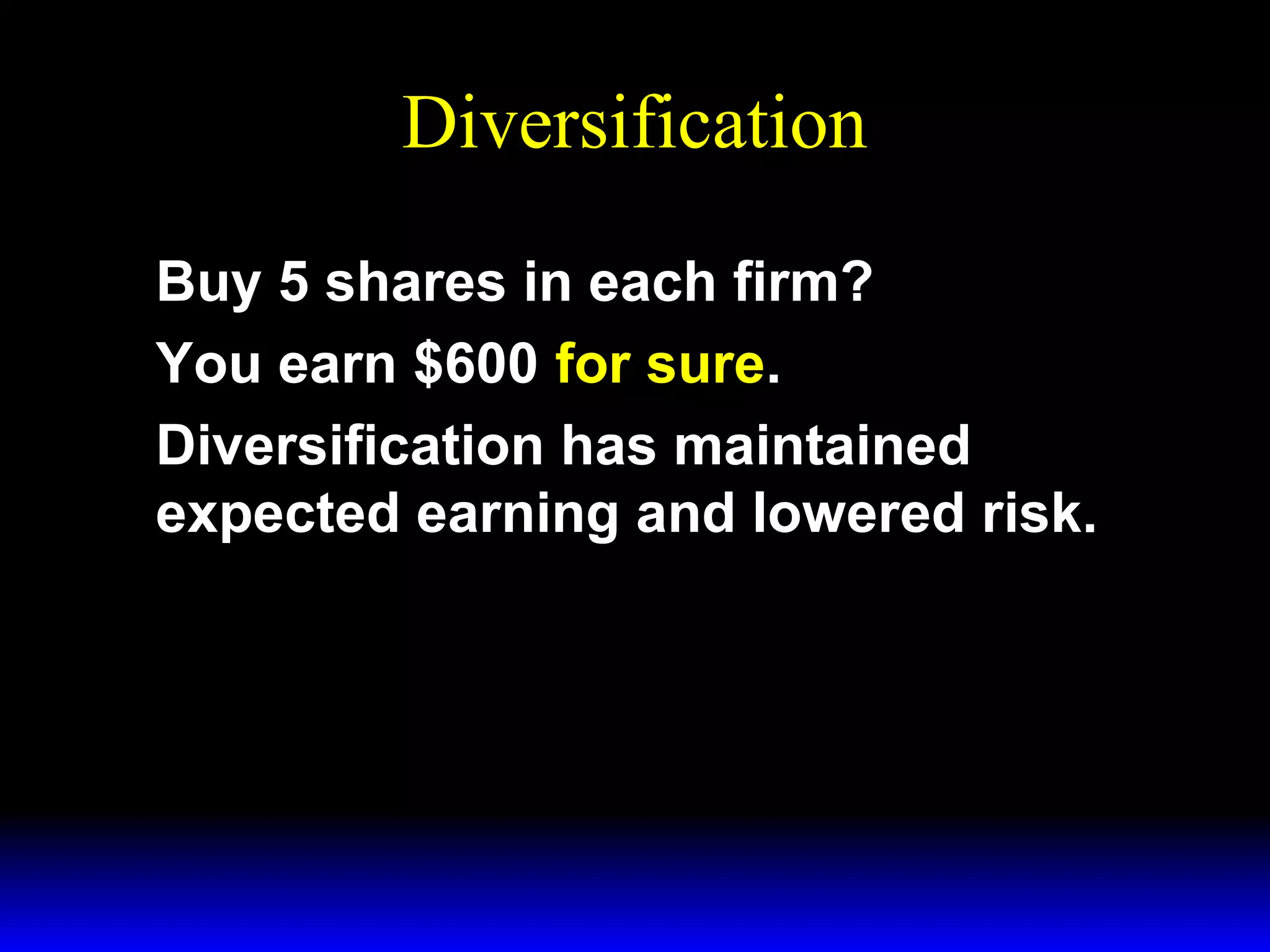

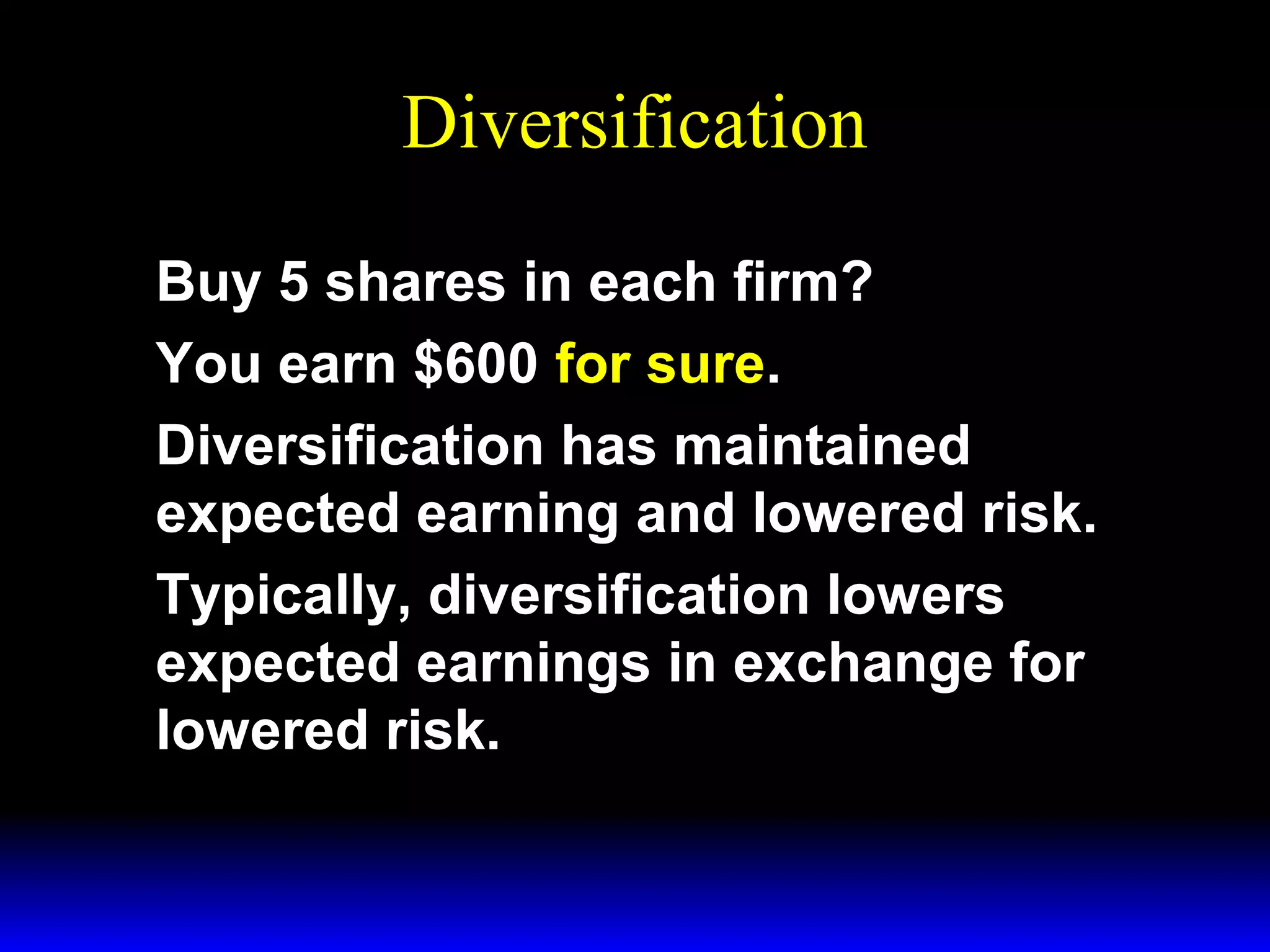

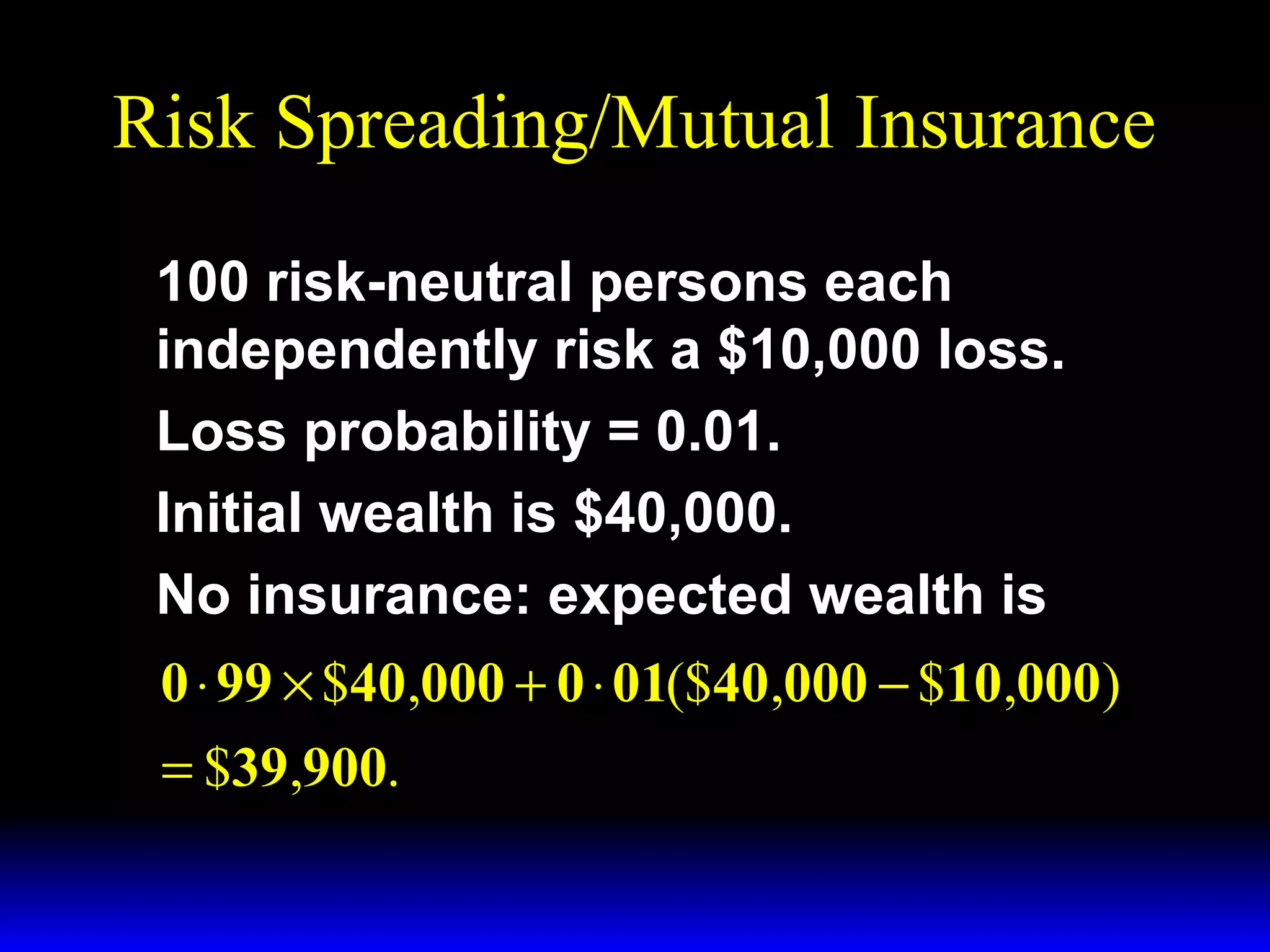

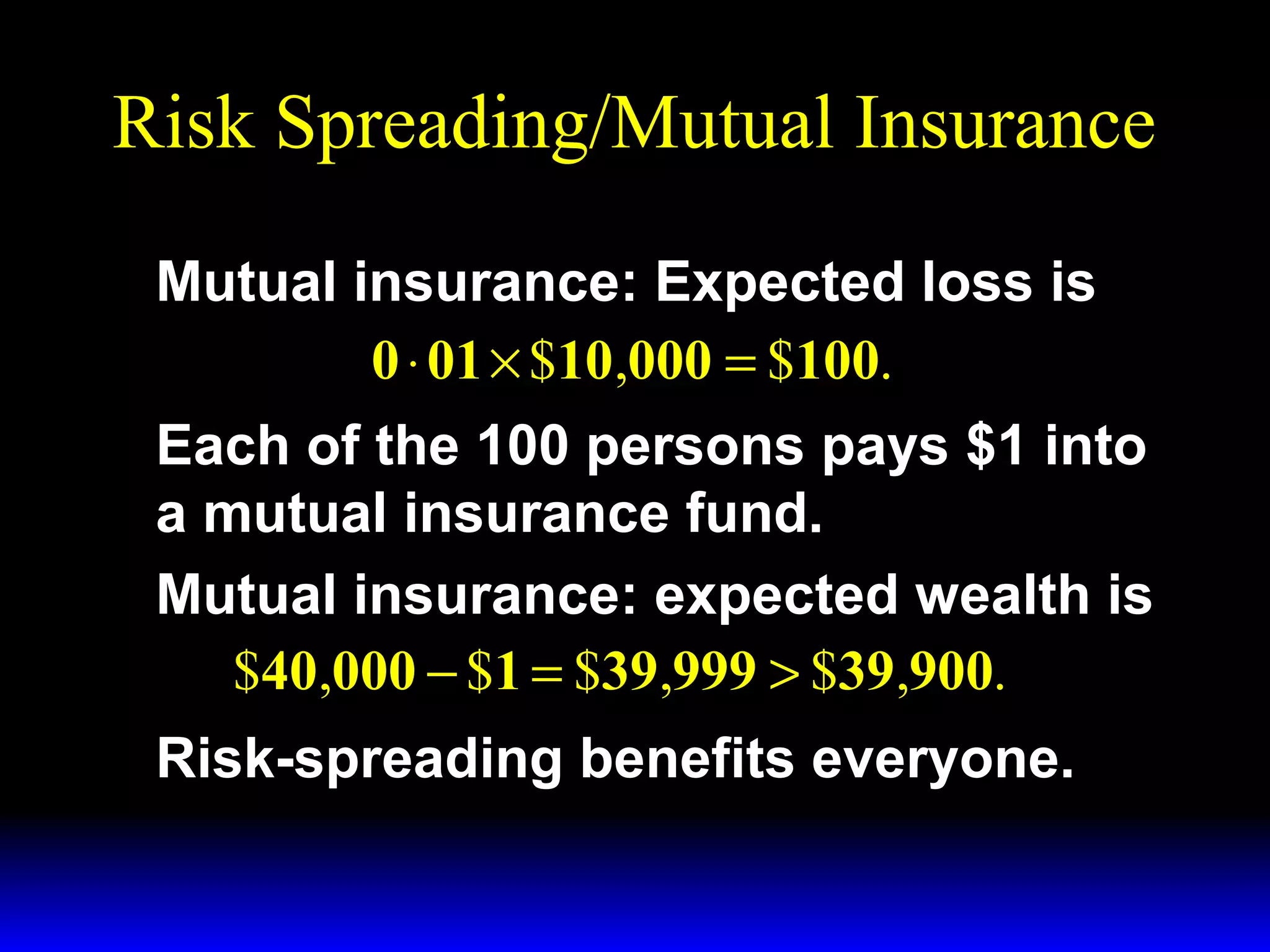

This chapter discusses uncertainty and rational responses to it. It introduces key concepts like states of nature, contingent contracts and consumption plans, and state-contingent budget constraints. Rational agents will choose the most preferred affordable consumption plan from their budget set. Insurance is a common response to reduce the costs of uncertainty. Competitive insurance leads to "fair" prices where risk-averse agents buy full insurance. Diversification and mutual insurance are other ways to manage risk.

![[Economics] Perfectly Competitive Market](https://cdn.slidesharecdn.com/ss_thumbnails/mic-131224022237-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)