Financial Markets

Role of Intermediaries in BFSI sector

History, growth, current position and

challenges for Banking, Financial services and

insurance sectors

Sub Topics to be covered

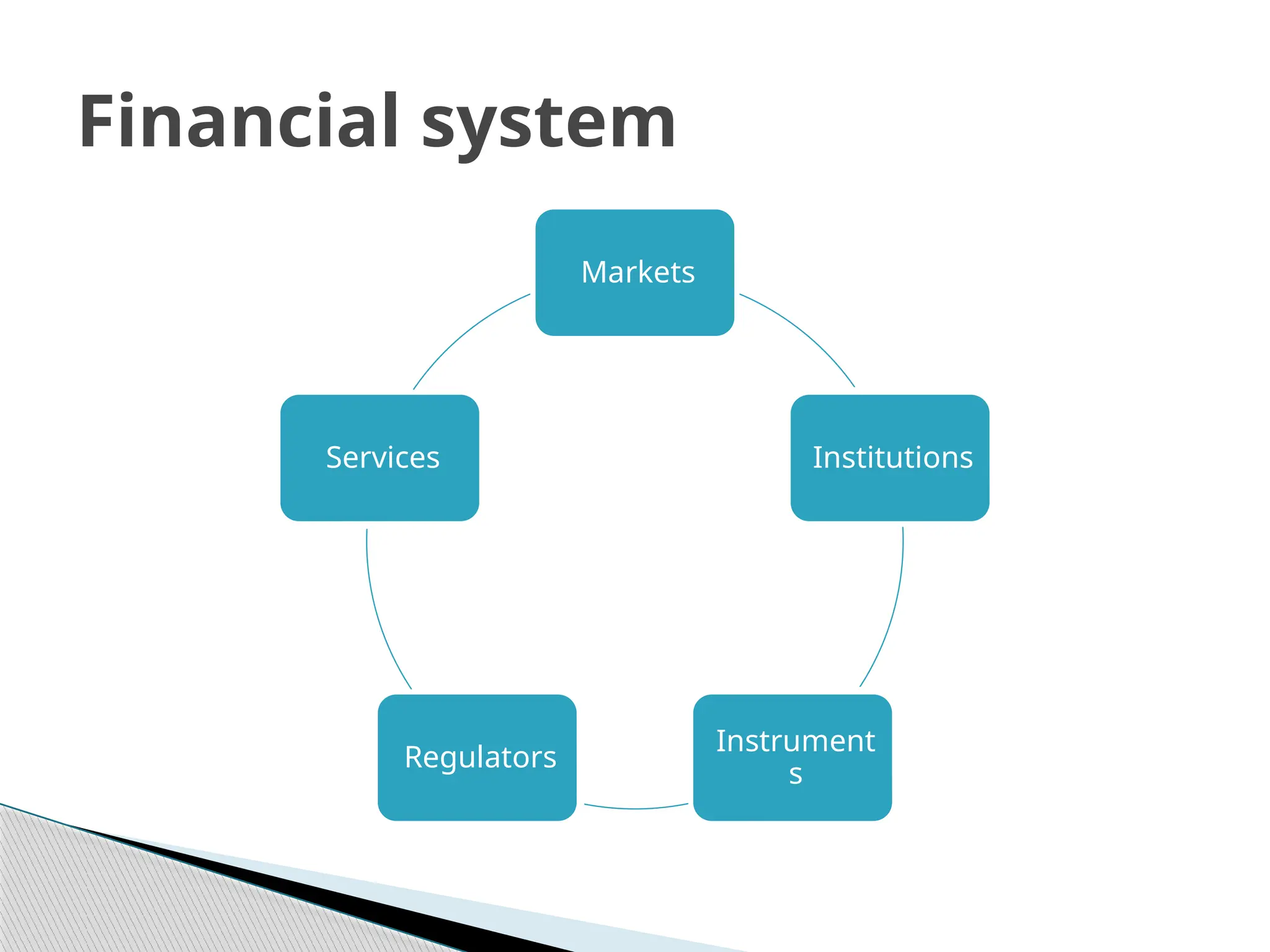

A financialsystem is the set of global, regional, or

firm-specific institutions and practices used to

facilitate the exchange of funds.

Financial markets refer to a centre that provides the

facilities of sale or purchase of financial claims and

services.

Individuals, financial institutions ,corporations and

government trade in this market either directly or

indirectly through brokers and dealers.

Activities in financial markets lead to direct effects

on behaviour of individual, business and consumers

Financial Markets

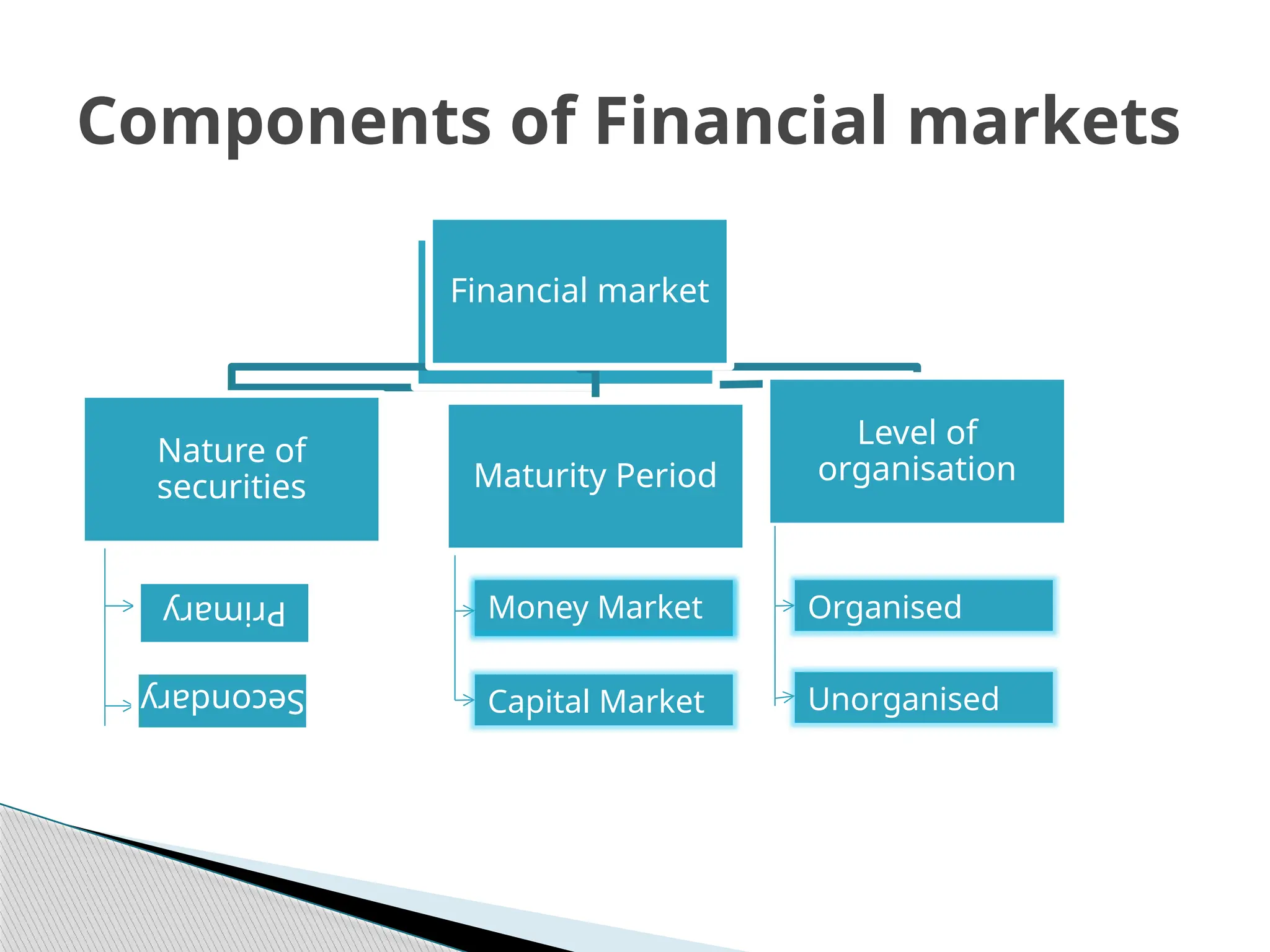

5.

Financial market

Nature MaturityPeriod

Level of

organisation

Primary

Secondary

Components of Financial markets

Money Market

Capital Market

Financial market

Nature of

securities Maturity Period

Level of

organisation

Primary

Secondary

Money Market Organised

Unorganised

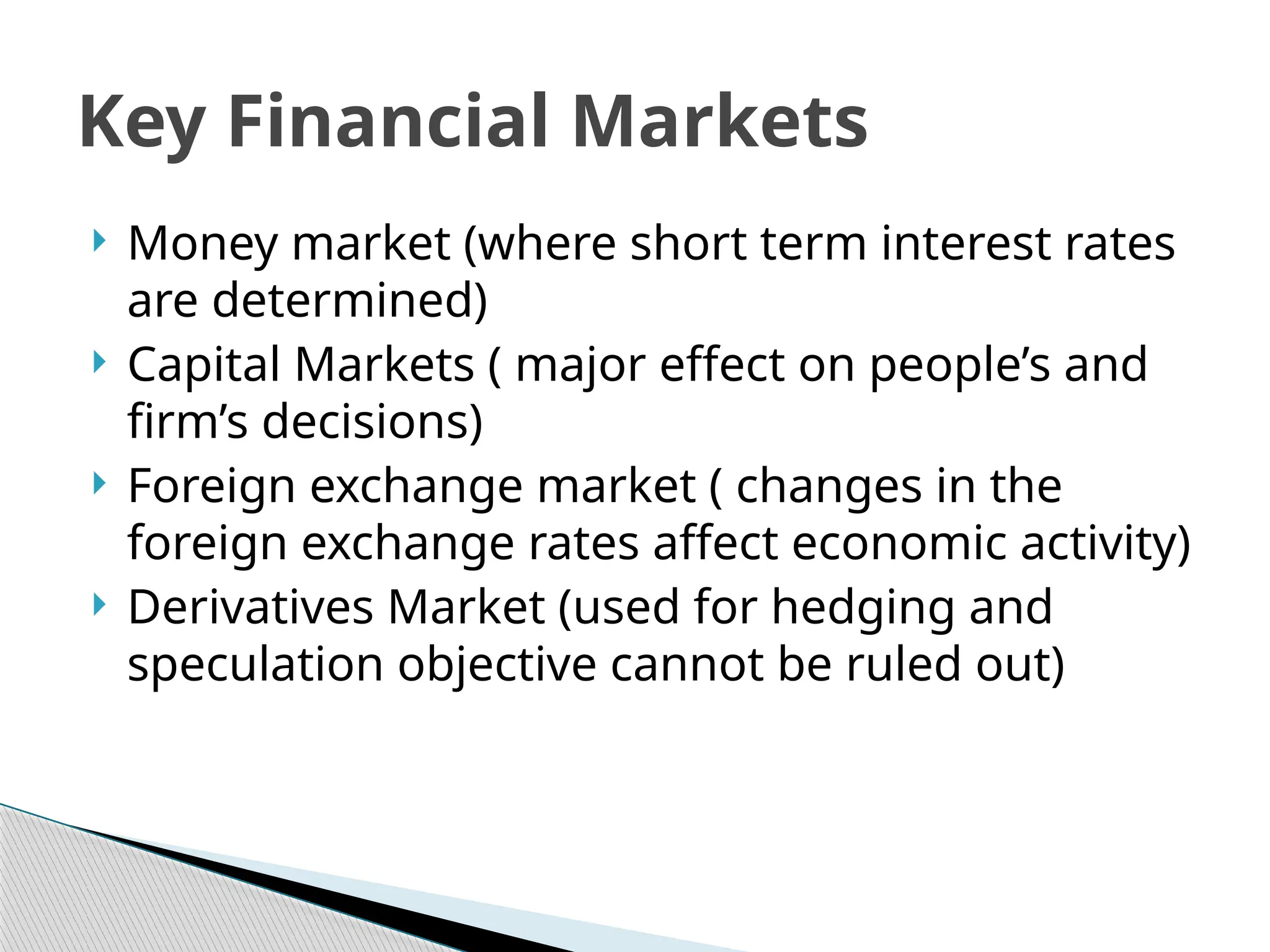

6.

Money market(where short term interest rates

are determined)

Capital Markets ( major effect on people’s and

firm’s decisions)

Foreign exchange market ( changes in the

foreign exchange rates affect economic activity)

Derivatives Market (used for hedging and

speculation objective cannot be ruled out)

Key Financial Markets

7.

Organised &unorganised

Low per capita leading to inadequate

participation

Regulatory bodies like RBI,SEBI,IRDA,MOF,NCLT

Paucity of financial instruments

Issues of corporate governance and scams

Financial Markets in India

8.

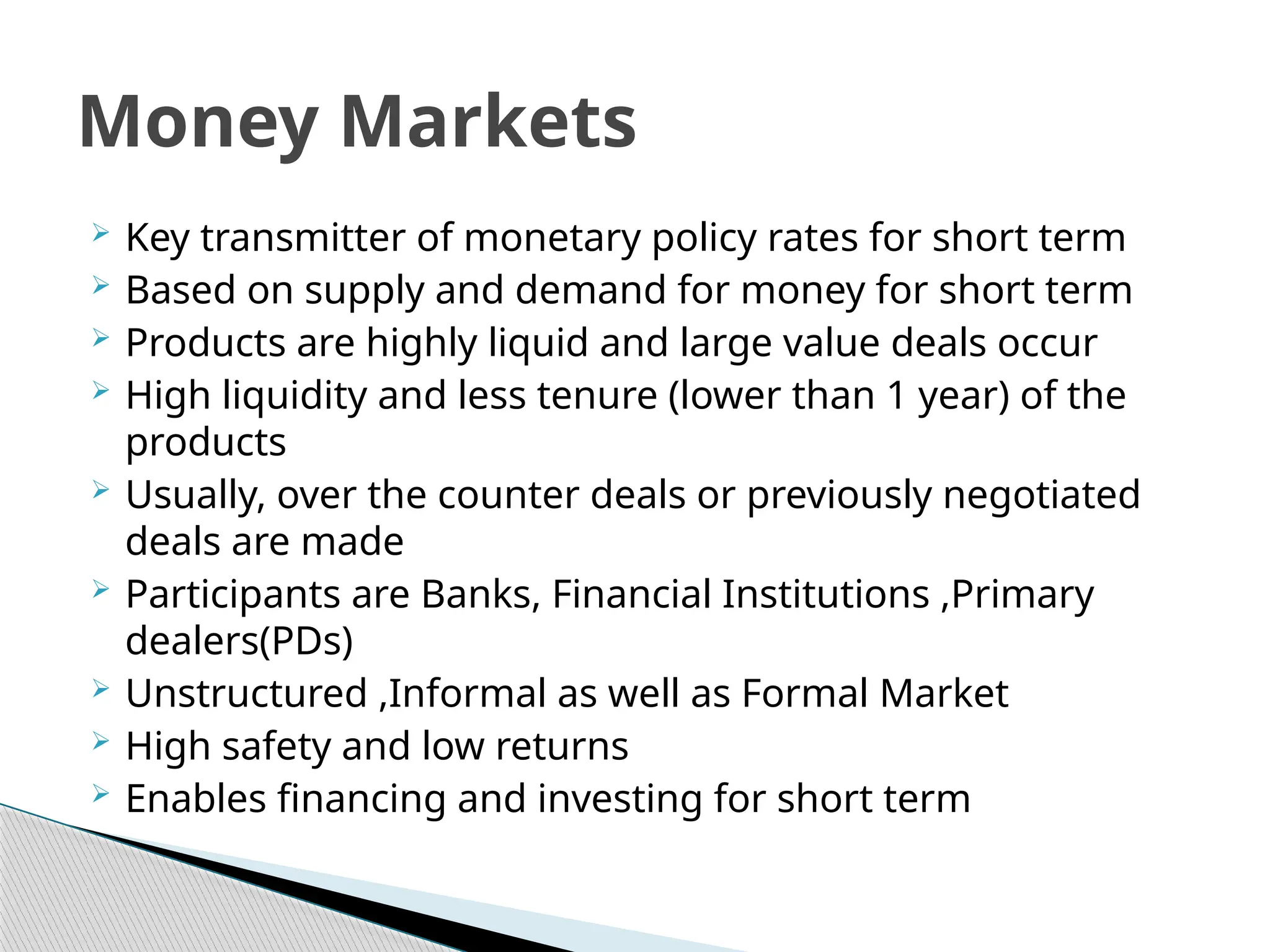

Key transmitterof monetary policy rates for short term

Based on supply and demand for money for short term

Products are highly liquid and large value deals occur

High liquidity and less tenure (lower than 1 year) of the

products

Usually, over the counter deals or previously negotiated

deals are made

Participants are Banks, Financial Institutions ,Primary

dealers(PDs)

Unstructured ,Informal as well as Formal Market

High safety and low returns

Enables financing and investing for short term

Money Markets

Long tenureassets with higher risk involved

Enables capital formation & economic

development

Can be categorised into stock Markets and

Bond Markets OR primary market and

secondary market

Capital Markets

11.

Products areEquities, Mutual Funds, ETFs,

Securities borrowing and lending schemes,

Debts-Corporate debts and securitised assets

In bond market, long term trading of

government securities, Bonds issued by PSU

Undertakings/Corporates/Banks like floating

rate bonds, Zero coupon Bonds, Corporate

debentures, state government loans,

securitised assets of banks, FIs , corporates and

others

Capital Markets

12.

Largest Financialmarket with players all over

the world

Global network working 24 hours a day

Facilitates determination of foreign exchange

rates between currency pairs

Participants include Banks, forex dealers,

Central bankers, hedge funds, investors

Foreign Exchange Markets

13.

Derivatives arefinancial securities and are financial

contracts that obtain value from something else,

known as underlying securities. Underlying

securities may be stocks, currency, commodities or

bonds, etc.

Formal derivative trading started in year 2001 after

electronic trading mechanisms were introduced in

India

Examples: Forwards, Futures, Options, Swaps

https://rmoneyindia.com/research-blog-traders/

indian-derivatives-market-investing/

Derivatives Market

14.

Direct Finance:Savers invest their funds

directly without any intervention of the

financial intermediary For example: issue of

equity shares and /or corporate bonds by

companies to public

Indirect Finance: Involves role of financial

intermediaries to facilitate movement of funds

from surplus units to deficit units For eg:

Banks, Mutual Funds etc

Types of Finance

Fund basedfinancial services

◦ Provide finance

◦ Reduce risk

◦ Examples: Lease financing, Factoring , Hire purchase, venture

capital, House financing, discounting

◦ Entities: Insurance companies, Banks, Housing finance

institutions

Fee based financial services

◦ Specialised services

◦ Professional fees charged to clients

◦ Examples: Portfolio consultancy, Merchant banking, Capital

restructuring

◦ Entities: Merchant bankers, Portfolio consultants, Issue managers

Types of Financial services

18.

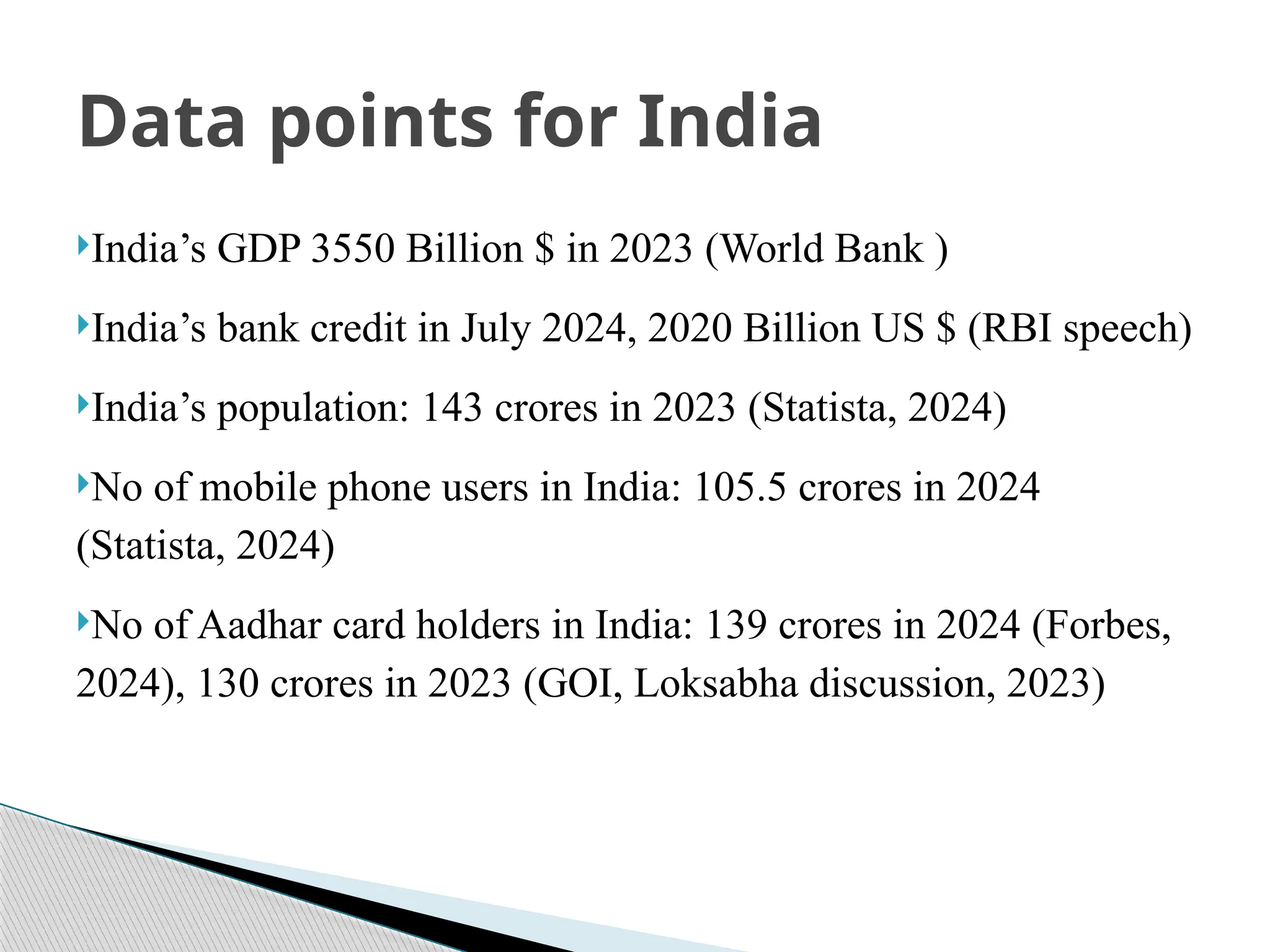

India’s GDP 3550Billion $ in 2023 (World Bank )

India’s bank credit in July 2024, 2020 Billion US $ (RBI speech)

India’s population: 143 crores in 2023 (Statista, 2024)

No of mobile phone users in India: 105.5 crores in 2024

(Statista, 2024)

No of Aadhar card holders in India: 139 crores in 2024 (Forbes,

2024), 130 crores in 2023 (GOI, Loksabha discussion, 2023)

Data points for India

19.

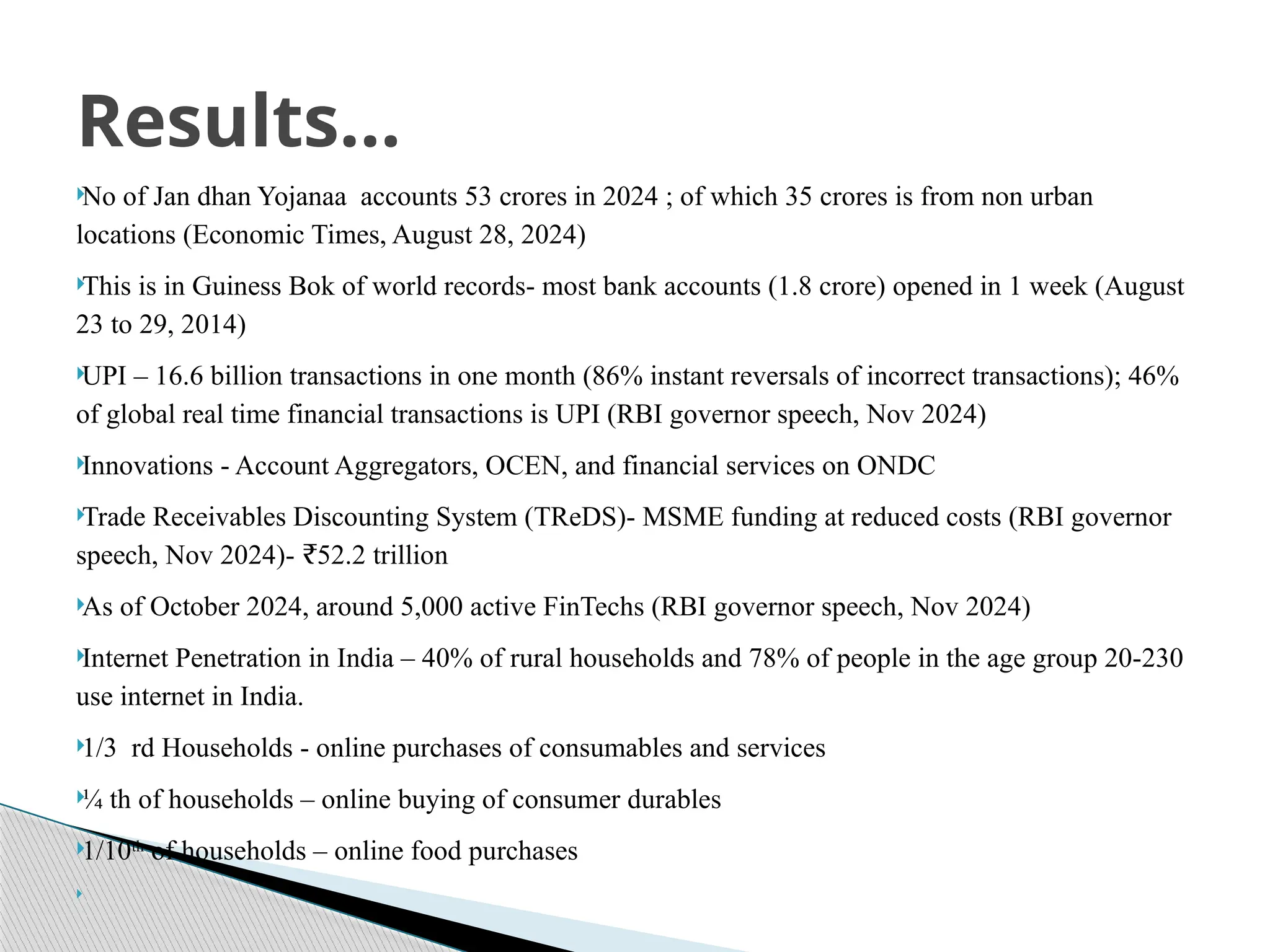

No of Jandhan Yojanaa accounts 53 crores in 2024 ; of which 35 crores is from non urban

locations (Economic Times, August 28, 2024)

This is in Guiness Bok of world records- most bank accounts (1.8 crore) opened in 1 week (August

23 to 29, 2014)

UPI – 16.6 billion transactions in one month (86% instant reversals of incorrect transactions); 46%

of global real time financial transactions is UPI (RBI governor speech, Nov 2024)

Innovations - Account Aggregators, OCEN, and financial services on ONDC

Trade Receivables Discounting System (TReDS)- MSME funding at reduced costs (RBI governor

speech, Nov 2024)- 52.2 trillion

₹

As of October 2024, around 5,000 active FinTechs (RBI governor speech, Nov 2024)

Internet Penetration in India – 40% of rural households and 78% of people in the age group 20-230

use internet in India.

1/3 rd Households - online purchases of consumables and services

¼ th of households – online buying of consumer durables

1/10th

of households – online food purchases

Results…

20.

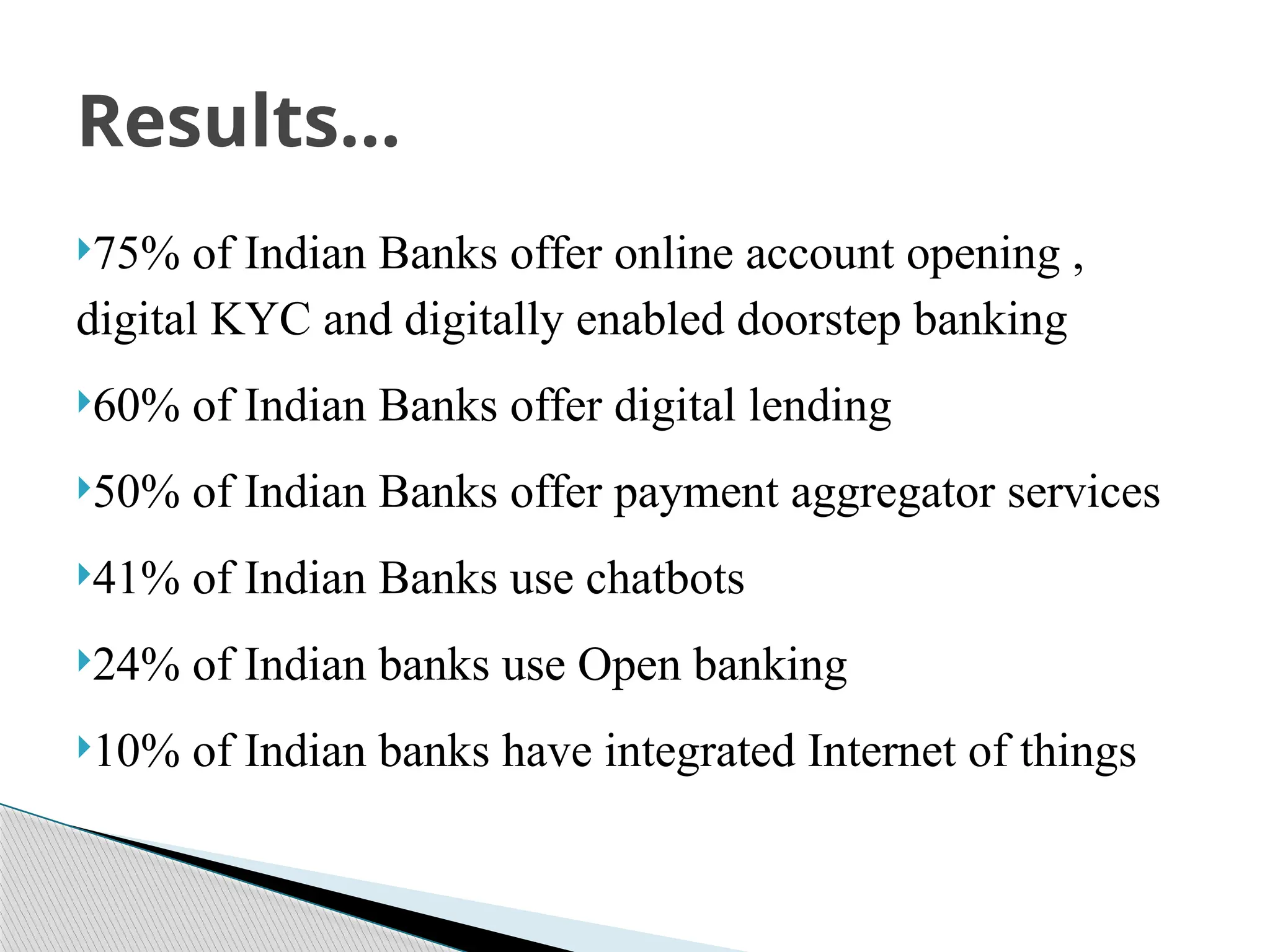

75% of IndianBanks offer online account opening ,

digital KYC and digitally enabled doorstep banking

60% of Indian Banks offer digital lending

50% of Indian Banks offer payment aggregator services

41% of Indian Banks use chatbots

24% of Indian banks use Open banking

10% of Indian banks have integrated Internet of things

Results…

21.

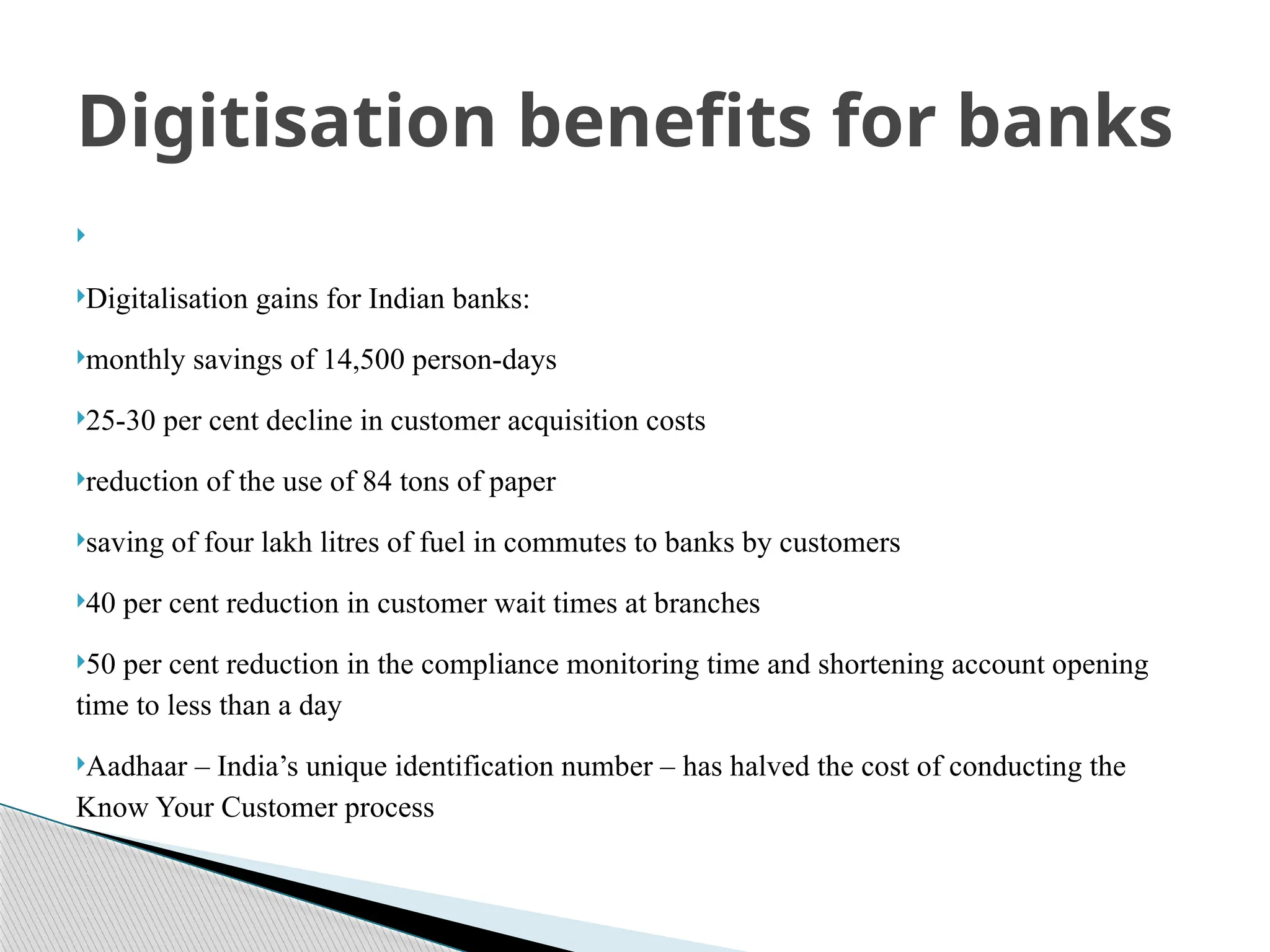

Digitalisation gains forIndian banks:

monthly savings of 14,500 person-days

25-30 per cent decline in customer acquisition costs

reduction of the use of 84 tons of paper

saving of four lakh litres of fuel in commutes to banks by customers

40 per cent reduction in customer wait times at branches

50 per cent reduction in the compliance monitoring time and shortening account opening

time to less than a day

Aadhaar – India’s unique identification number – has halved the cost of conducting the

Know Your Customer process

Digitisation benefits for banks

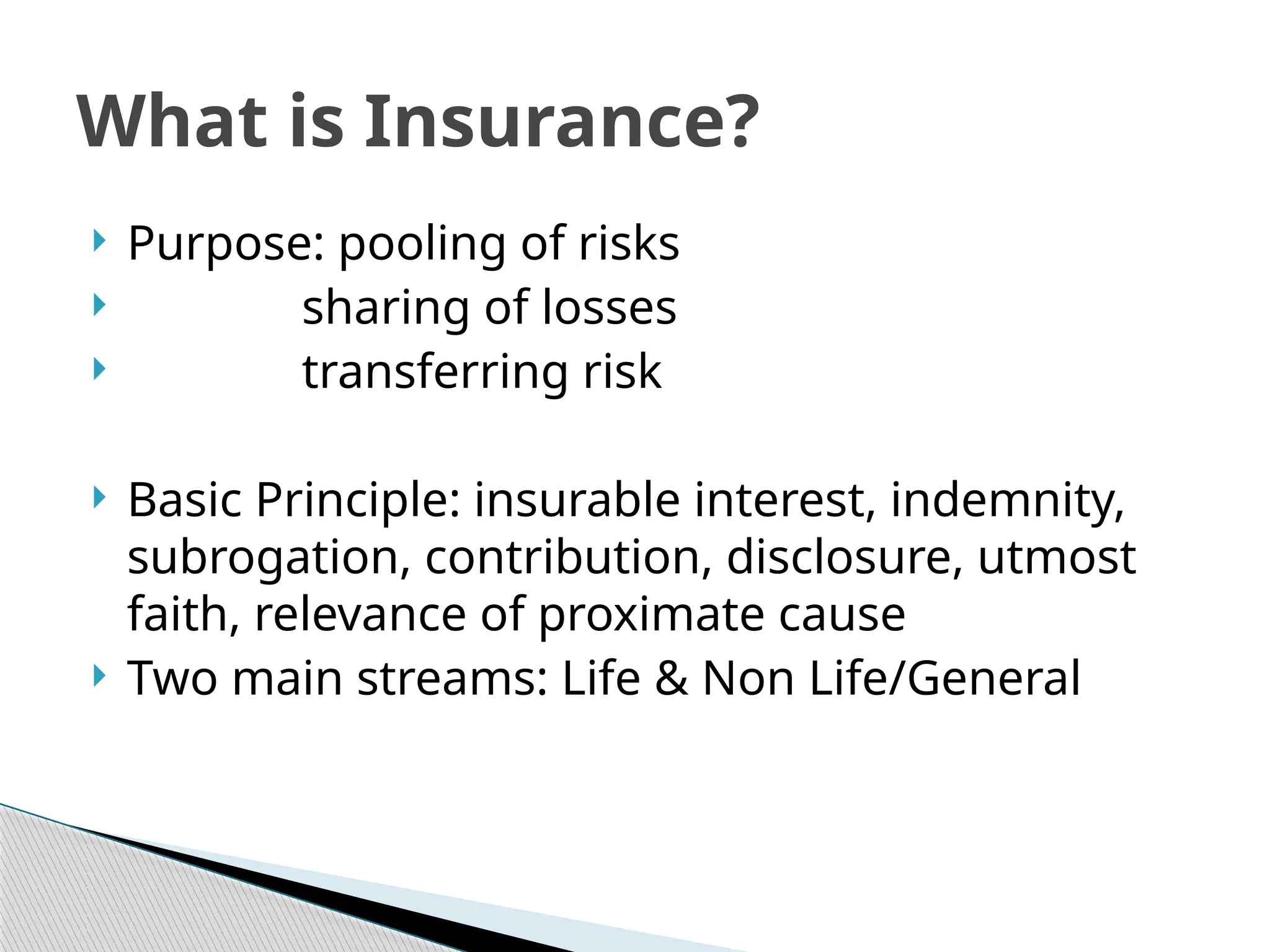

Purpose: poolingof risks

sharing of losses

transferring risk

Basic Principle: insurable interest, indemnity,

subrogation, contribution, disclosure, utmost

faith, relevance of proximate cause

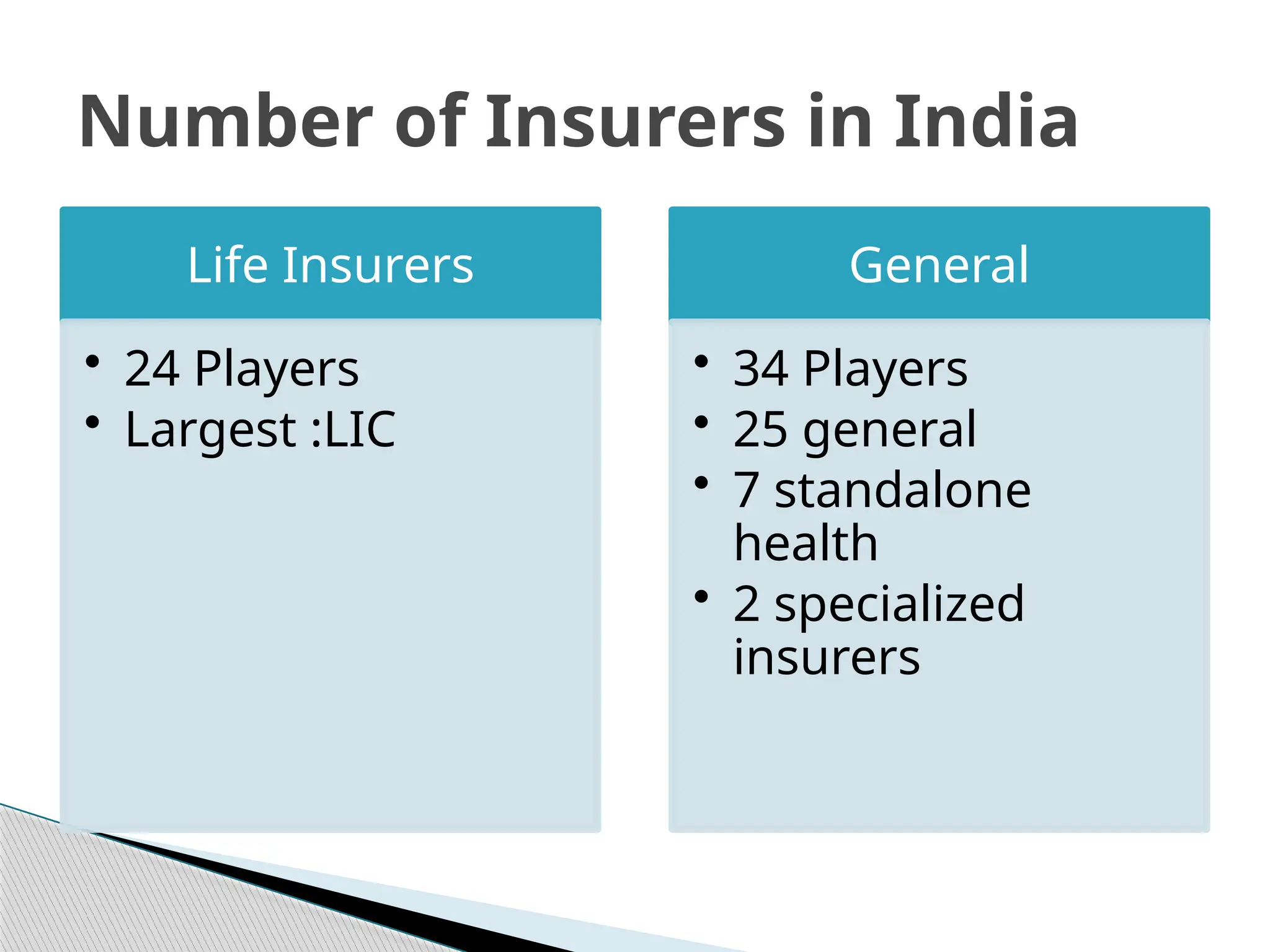

Two main streams: Life & Non Life/General

What is Insurance?

25.

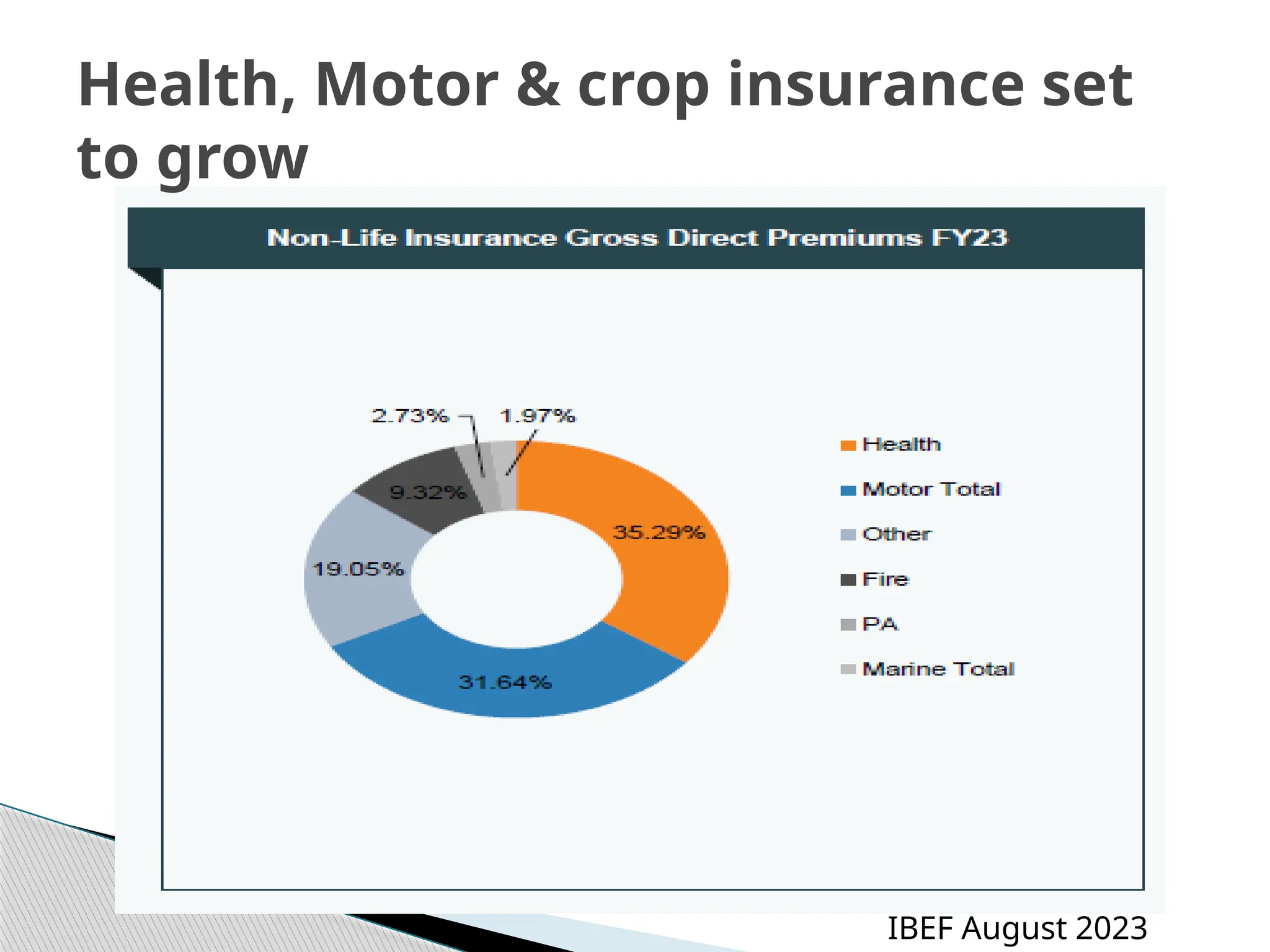

The firstquarter of FY24 saw nonlife players' premium income increase by

17.9% year-over-year to Rs. 64,262.8 crore (US$ 7.72 billion) due to strong

demand for health and motor policies.

The government’s flagship initiative for crop insurance, Pradhan Mantri

Fasal Bima Yojana (PMFBY), has led to significant growth in the premium

income for crop insurance

As per the Insurance Regulatory and Development Authority of India

(IRDAI), India will be the sixth-largest insurance market within a

decade, leapfrogging Germany, Canada, Italy and South Korea.

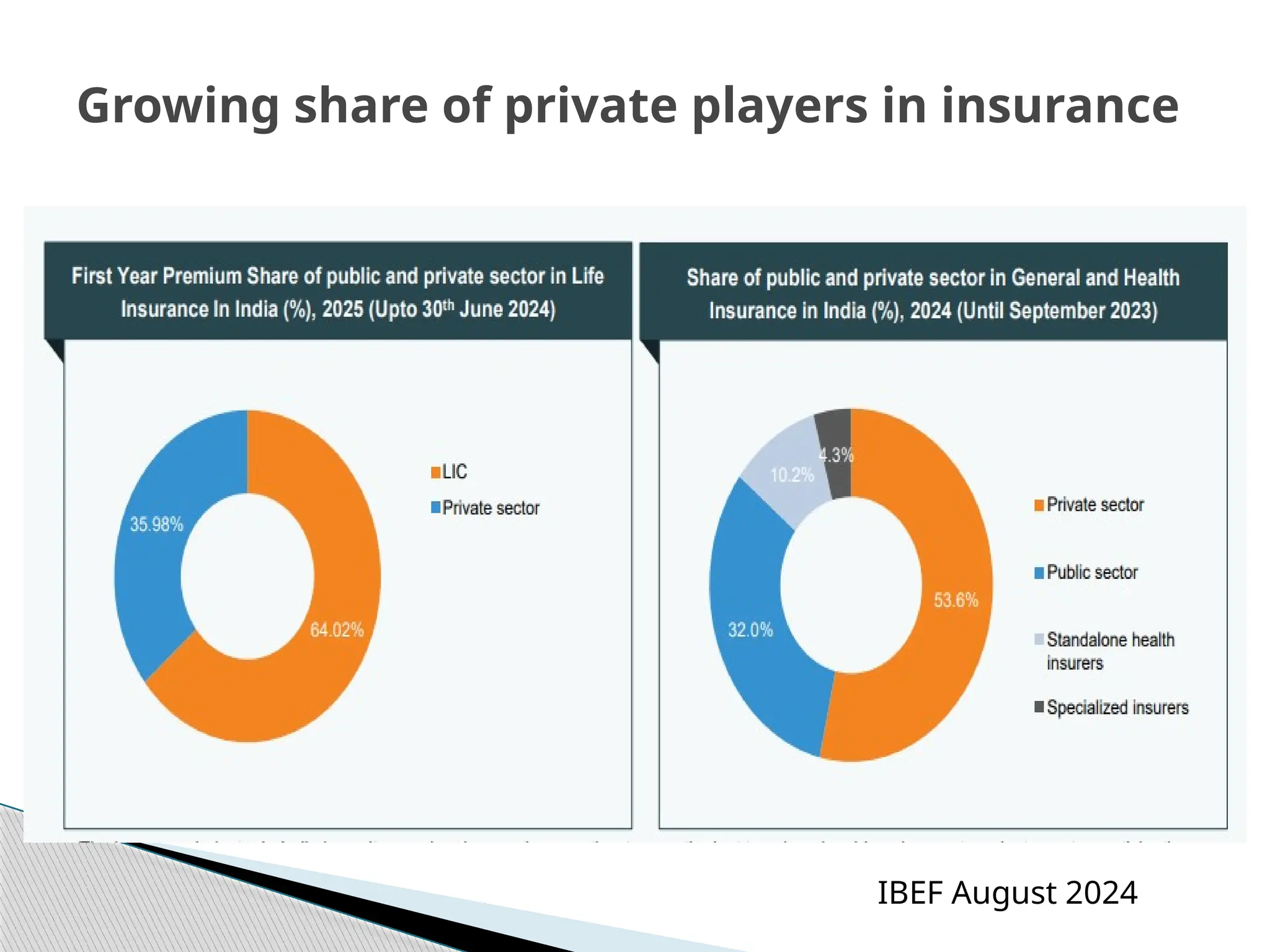

India allowed private companies in insurance sector in 2000, setting a limit

on FDI to 26%, which was increased to 49% in 2014 and further increased

to 74% in the Union Budget (Feb 2021).

The market share of private sector companies in the non-life insurance

market rose from 15% in 2004 to 62% in FY23.

Private insurers like HDFC, ICICI and SBI have been some tough

competitors for providing life as well as non-life products to the insurance

sector in India.

Key facts

26.

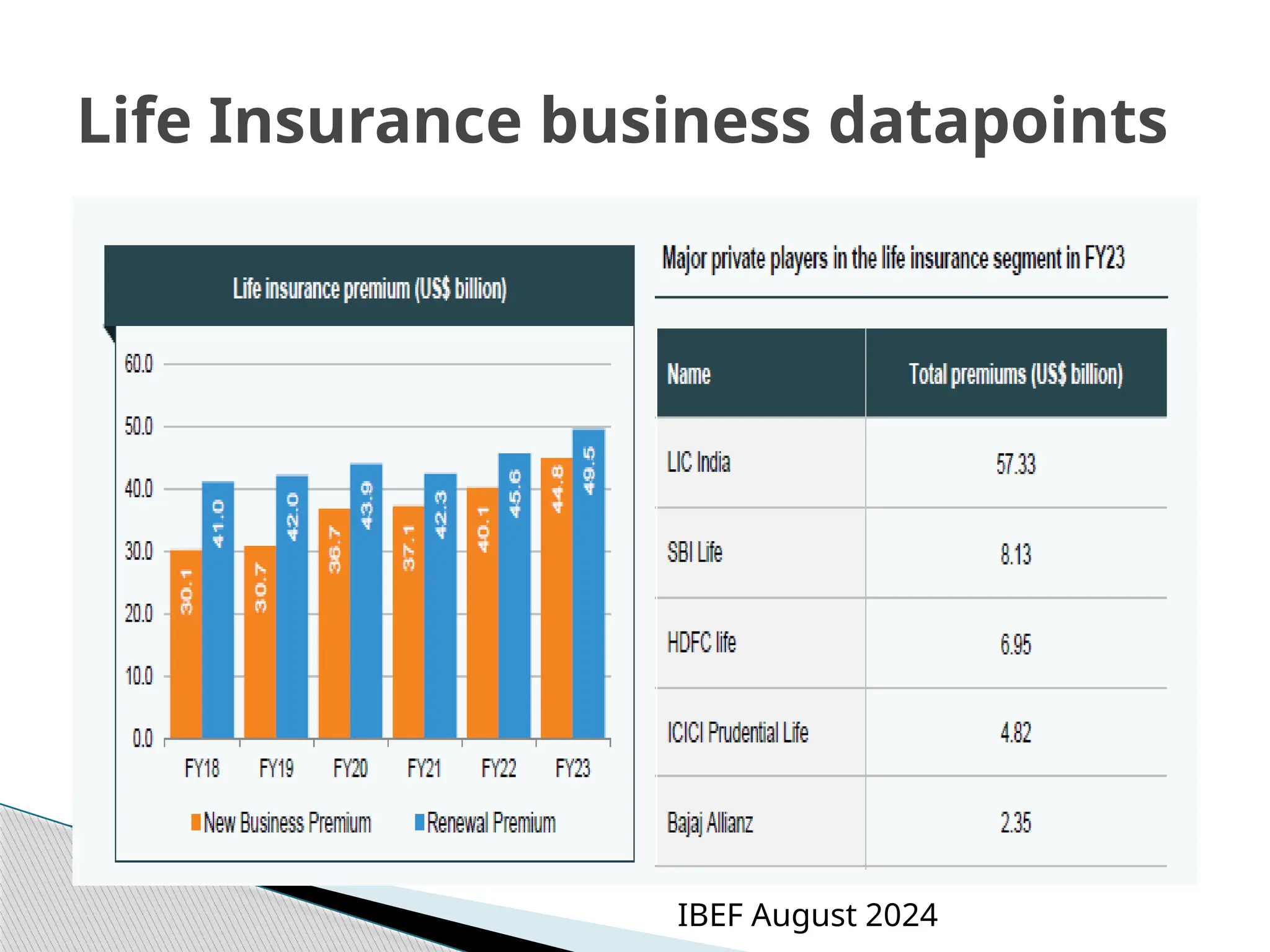

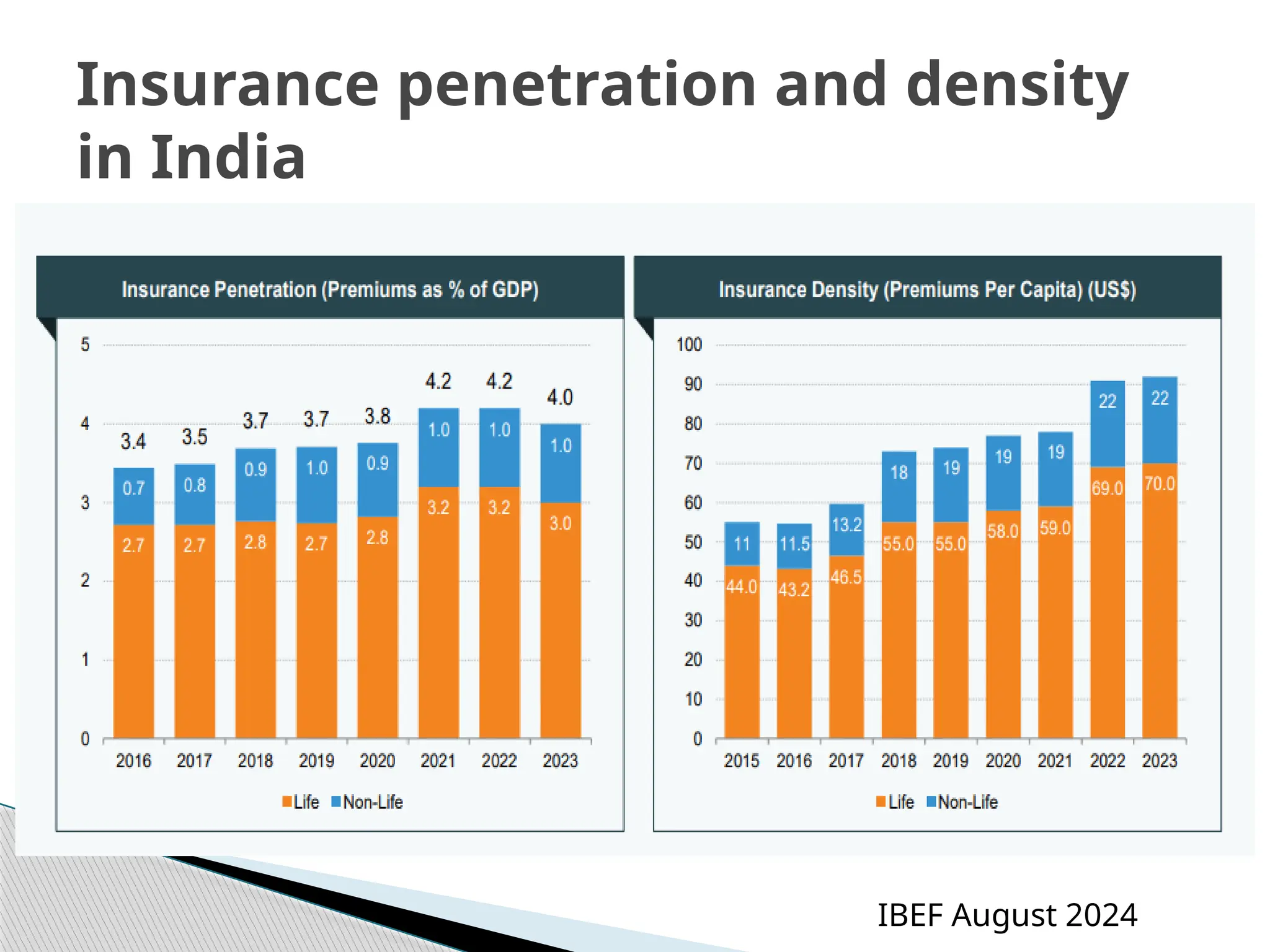

The lifeinsurance industry is expected to increase at a

CAGR of 5.3% between 2019 and 2023. India’s insurance

penetration was pegged at 4.2% in FY21, with life

insurance penetration at 3.2% and non-life insurance

penetration at 1.0%. In terms of insurance density,

India’s overall density stood at US$ 78 in FY21.

Life Insurance trends

27.

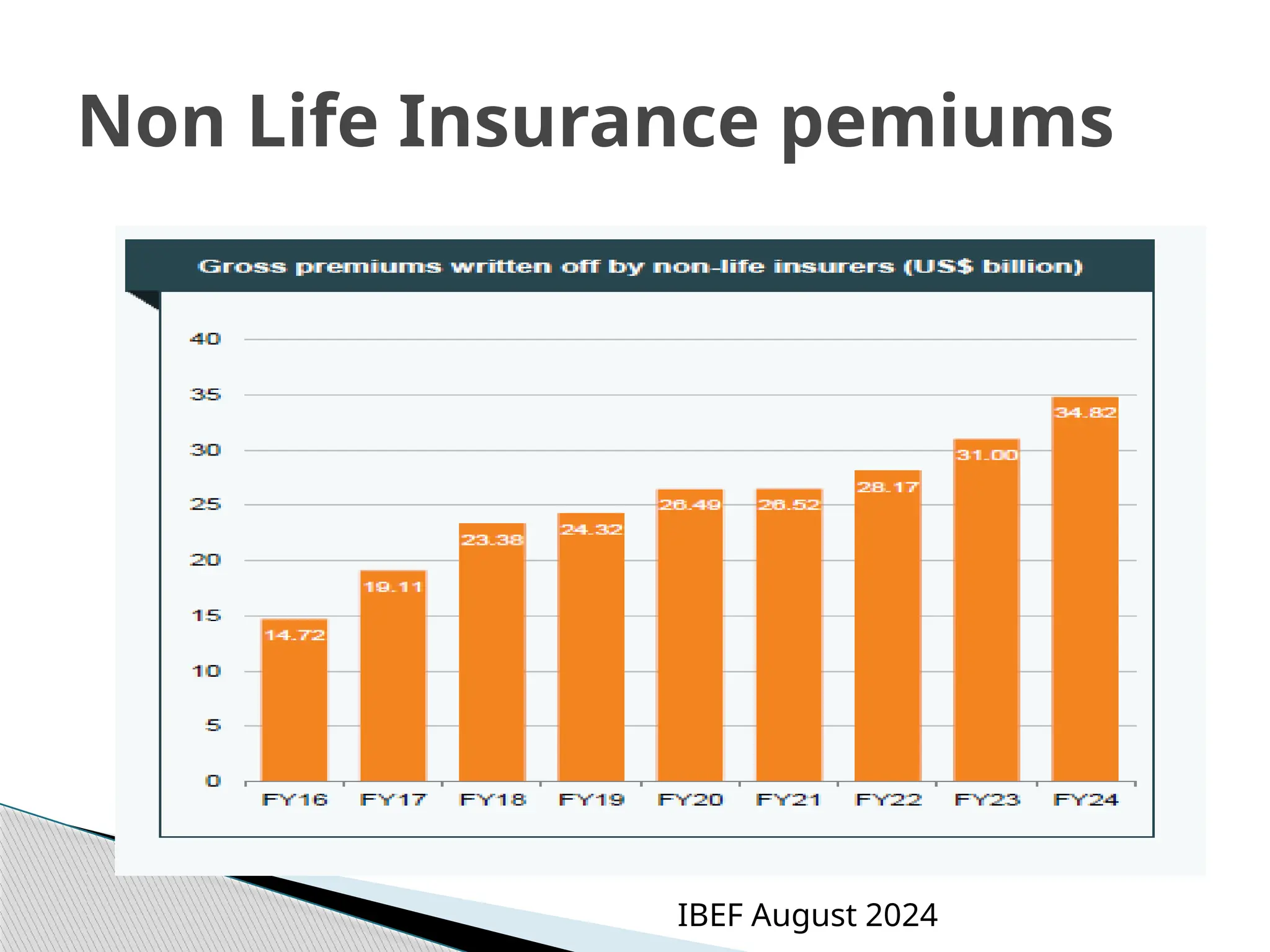

India isthe 4th largest general insurance market in Asia and the 14th

largest globally.

In FY23, non-life insurers (comprising general insurers, standalone health

insurers and specialized insurers) recorded a 16.4% growth in gross direct

premiums. In India, gross premiums written off by non-life insurers reached

US$ 31 billion in FY23 and US$ 10.95 billion in first quarter of FY24*, from

US$ 28.14 billion in FY22, driven by strong growth from general insurance

companies.

Going forward, general insurance companies will be key beneficiaries of the

opening-up of economies, especially with improved trade activity increasing

demand for motor and health insurance. Strong growth in the automotive

industry over the next decade is expected to boost the motor insurance

market

Non life insurance trends

The governmenthas approved 100% FDI for insurance

intermediaries and increased FDI limit in the insurance

sector to 74% from 49% under the Union Budget 2021-22.

The relaxation of foreign investment rules has received a

positive response from the insurance sector, with many

companies announcing plans to increase their stakes in

joint ventures with Indian companies.

Over the coming quarters, there could be a series of joint

venture deals between global insurance giants and local

players.

Increasing investments including FDI in Insure-tech,

Robust demand ,Policy support, Attractive opportunities

Promising future lies ahead

37.

Insurance market –attractive?

Growing middle class

Young insurable population

Growing awareness of the need for

insurance

Retirement planning a big opportunity

Growth in premia expected at 12-15%

over next 3-5 years

38.

Bhima Vahak:Bima Vahaks (women centric)have to

be deployed in each gram panchayat

Bhima Vistaar :The first of its kind all-in-one

affordable insurance product, Bima Vistaar —

offering life, health and property cover — is likely to

be rolled out soon.

Bhima Sugam :simplifying buying insurance on a

single platform

New initiatives for Insurance: Insurance trinity

set to have soft launch soon- IRDAI Chairman

https://www.newindianexpress.com/business/2024/Oct/22/first-phase-

of-bima-insurance-trinity-will-be-ready-for-soft-launch-soon-irdai-chief

39.

Recent Trends

Newdistribution channels – bancassurance,

online distribution have increased reach and

reduced costs

Growing Market share of Private players

Differentiated Banks – non-exclusive tie-ups for

distribution

Launch of apps:HDFC ERGO General Insurance, Policybazaar's

PBPartners, Canara HSBC Life Insurance App

Traditional products are being customised to

meet specific needs: Micro Insurance

40.

Growth drivers andOpportunities

New distribution channels

B30 cities and other non-metros are a large

potential market

Growth in Financial industry

Innovation and efficiency

Increasing competition

Foreign players bringing expertise and capital

IPOs

Use of Technology for customization and

distribution

Mutual fundis a mechanism for pooling the

resources by issuing units to the investors and

investing funds in securities in accordance with

objectives as disclosed in offer document.

Investments in securities are spread across a

wide cross-section of industries and sectors and

thus the risk is reduced.

Regulated by SEBI

What are Mutual Funds?

43.

Provides expertadvice for management of financial

assets

Risk diversification

Economies of scale

Transparency and accountability led by regulatory

oversight

Flexibility based on investor preference and risk

appetite

https://www.youtube.com/watch?v=annVByCpYCw

Key features and significance

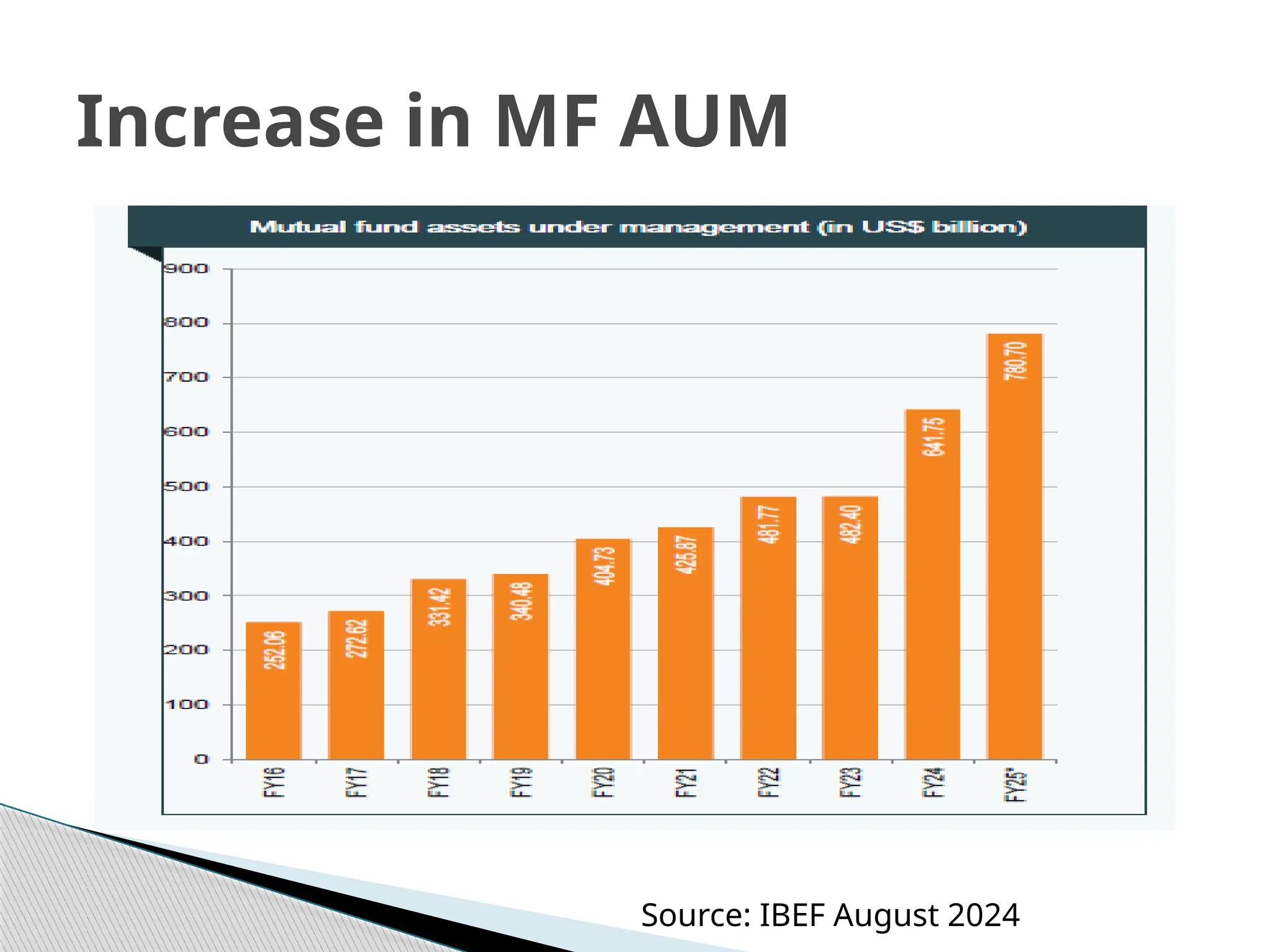

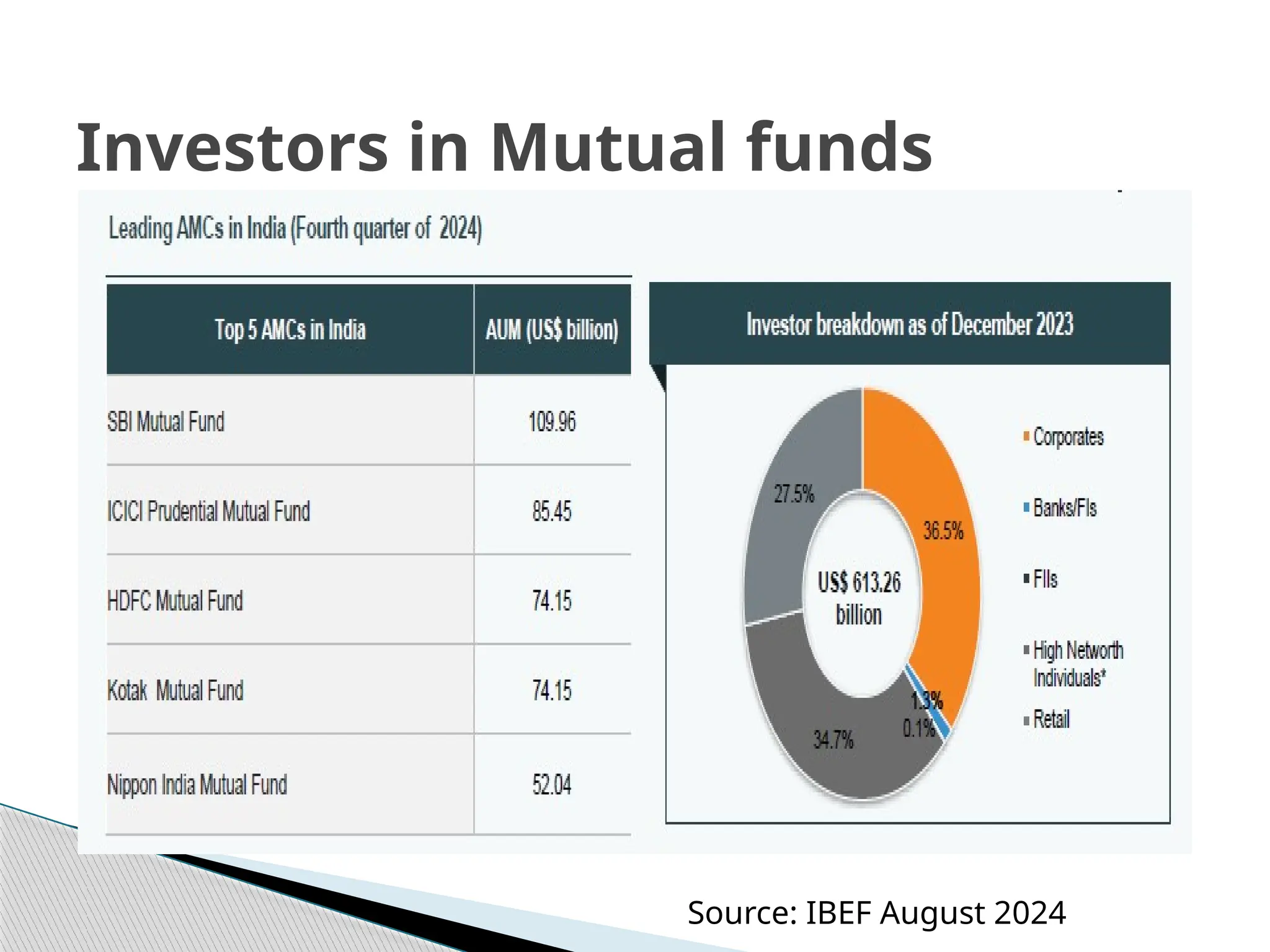

Key facts &Growth drivers Mutual

Funds.

As of 31st

October 2024, AUM managed by the mutual funds industry stood

at Rs. 67.26 Trillion, which is around a two-fold increase in the span of five

years.

The MF Industry’s AUM has grown from Rs. 26.33 trillion as on October

31, 2024 to Rs. 67.26 trillion as on October 31, 2024

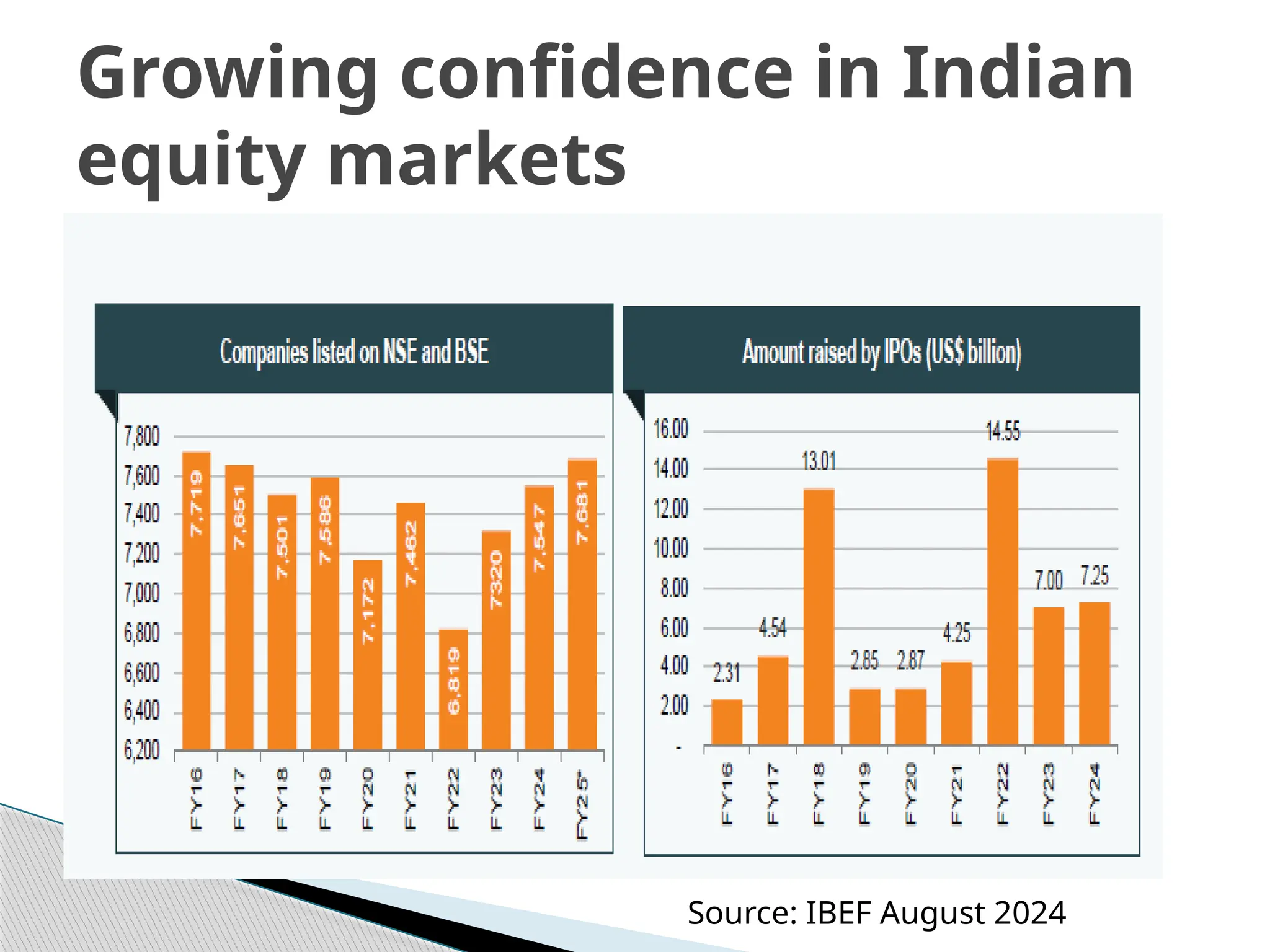

Indian equity markets performing well along with fastest growing GDP

Large number of company listings and IPOs

Increasing number of UHNWI and HNWIs in India (Ultra High network

Individuals) UHNWI expected to go from 12,069 in 2022 to 19,119 in

2027(58% growth)

People shifting from physical asset classes to Financial asset class

In 2023, India’s gross savings was 30% of its GDP

Note: HNWI: Investible assets more than Rs 5 crores

VHNWI: Investible assets between Rs 5 crores and Rs 25 crores

UHNWI: Investible assets more than Rs 25 crores

Source: AMFI accessed on 18th

Nov, 2024 &

IBEF August 2024

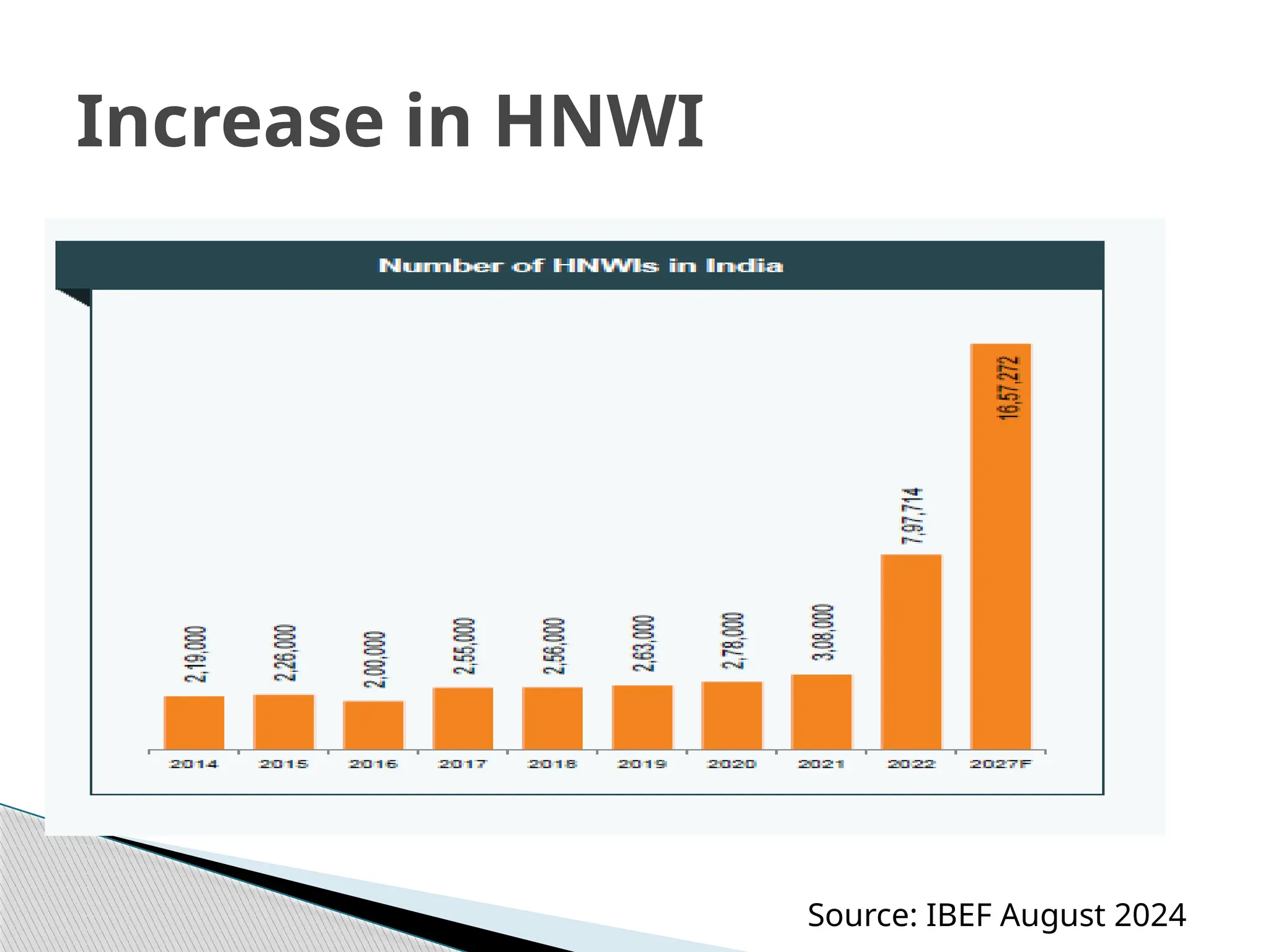

The numberof Ultra High Net Worth Individuals (UHNWI) is estimated to

increase from 12,069 in 2022 to 19,119 in 2027. India’s UHNWIs are likely to

expand by 58.4% in the next five years.

In 2021, India’s gross savings was at 29.3% of GDP amounting to US$ 930.56

billion. In 2022, India’s gross savings stood at 29.84% of GDP.

India is expected to be the fourth largest private wealth market globally

by 2028.

Low penetration

Rising middle class incomes

Reduction in interest rates may induce investors to invest in Mutual funds

rather than in Fixed deposits

Trend is clearly seen in people investing in financial assets rather than

physical assets

Millennials and Retirees : two ends of the spectrum – needing customized

solutions

Leverage technology & greater dependence on financial advisors

Opportunities and Challenges –

Mutual Funds

a companyregistered under the Companies Act, 1956

engaged in the business of loans and advances,

acquisition of shares/ stocks/ bonds/ debentures/

securities issued by Government or local authority

or other marketable securities of a like nature, leasing,

hire-purchase, insurance business, chit business

financial assets constitute more than 50 per cent of the

total assets

& income from financial assets constitute more than 50

per cent of the gross income

What is a NBFC?

55.

NBFC cannotaccept demand deposits

NBFC not part of payment and settlement

system

Cannot issue cheques drawn on self

Depositors not covered by DICGC insurance

Difference between bank and NBFC

56.

Credit intermediation;

niche financing;

alternative to banking credit, last mile servicing

Can be classified into:

A)asset liability structures

B) systemic importance

C) activities undertaken

Importance of NBFCs

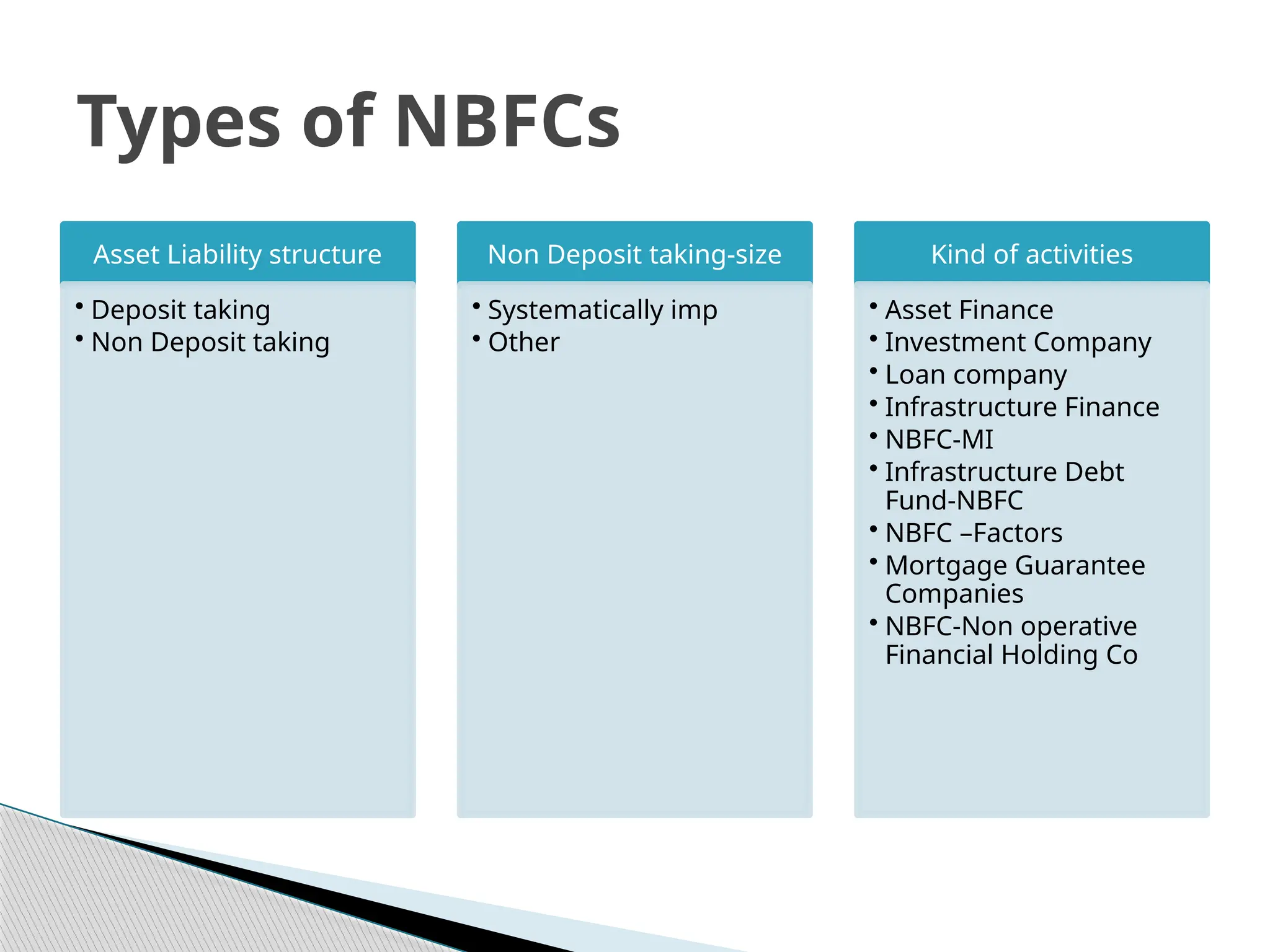

Asset Liability structure

•Deposit taking

• Non Deposit taking

Non Deposit taking-size

• Systematically imp

• Other

Kind of activities

• Asset Finance

• Investment Company

• Loan company

• Infrastructure Finance

• NBFC-MI

• Infrastructure Debt

Fund-NBFC

• NBFC –Factors

• Mortgage Guarantee

Companies

• NBFC-Non operative

Financial Holding Co

Types of NBFCs

59.

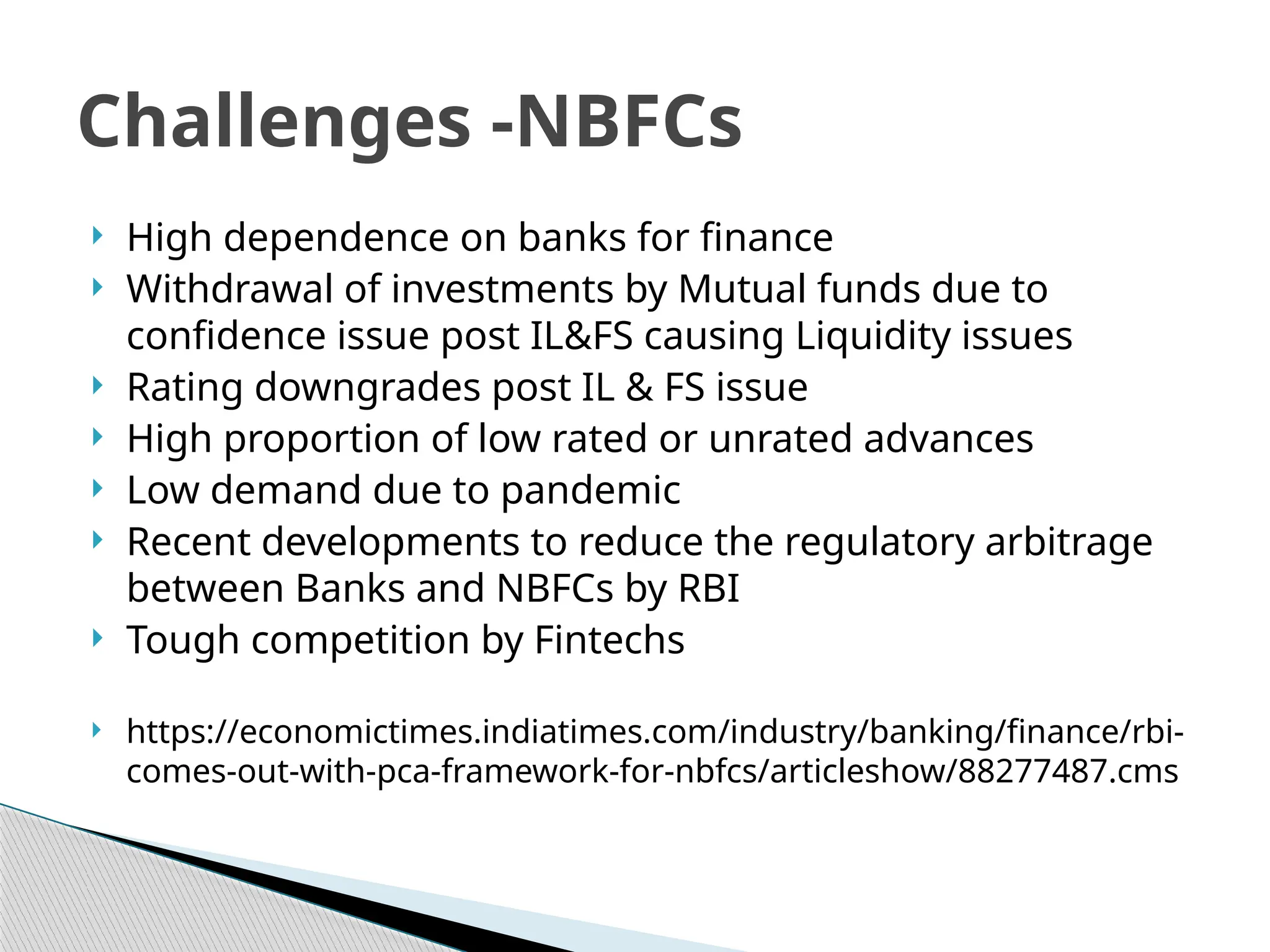

High dependenceon banks for finance

Withdrawal of investments by Mutual funds due to

confidence issue post IL&FS causing Liquidity issues

Rating downgrades post IL & FS issue

High proportion of low rated or unrated advances

Low demand due to pandemic

Recent developments to reduce the regulatory arbitrage

between Banks and NBFCs by RBI

Tough competition by Fintechs

https://economictimes.indiatimes.com/industry/banking/finance/rbi-

comes-out-with-pca-framework-for-nbfcs/articleshow/88277487.cms

Challenges -NBFCs

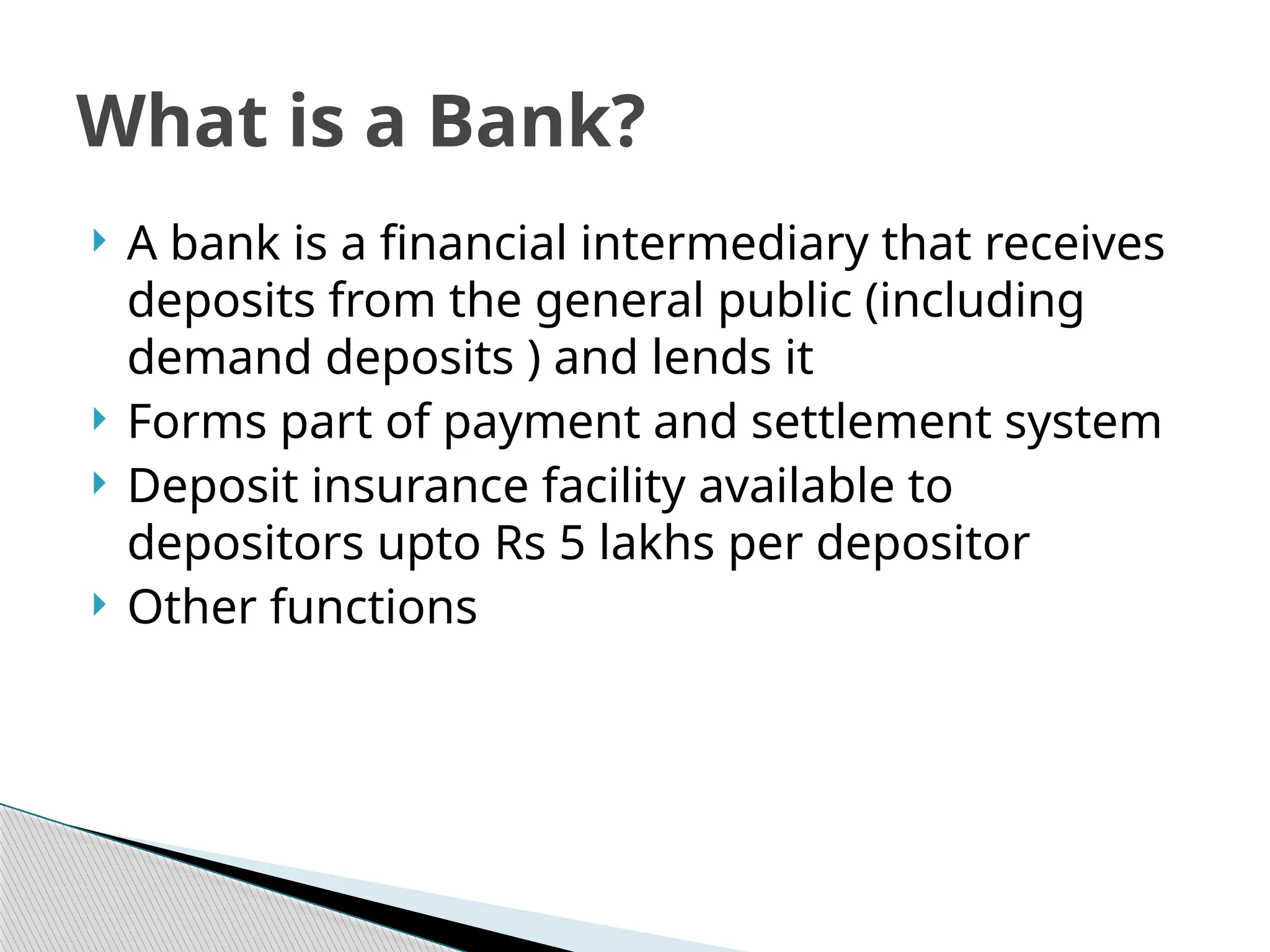

A bankis a financial intermediary that receives

deposits from the general public (including

demand deposits ) and lends it

Forms part of payment and settlement system

Deposit insurance facility available to

depositors upto Rs 5 lakhs per depositor

Other functions

What is a Bank?

62.

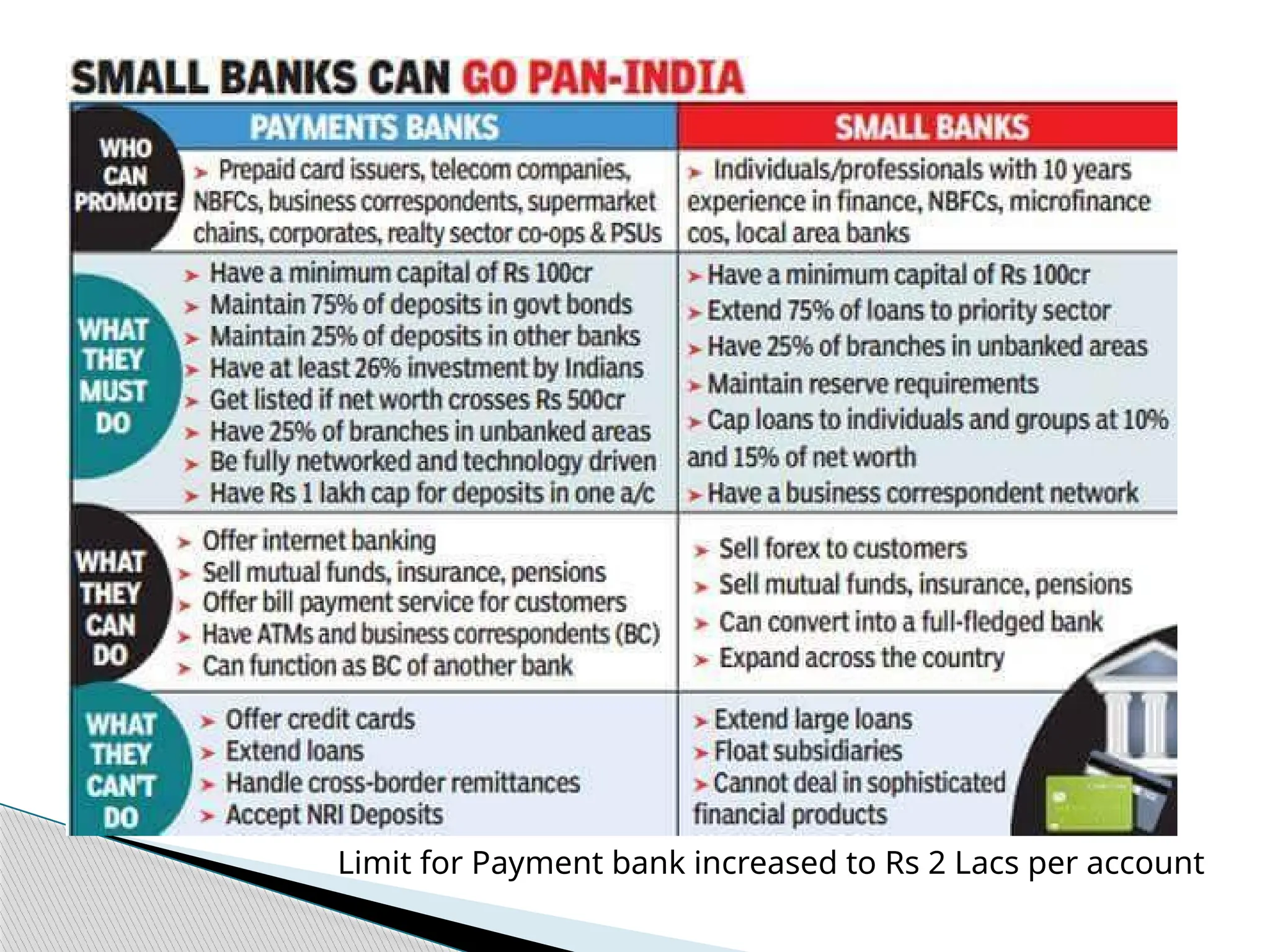

Public Sector (12)Private Sector (21) Foreign (45)

Small Finance (12) Payments (4)

Others including

Regional Rural (43) ,

Local Area (3) ,

Cooperative

Types of Banks

63.

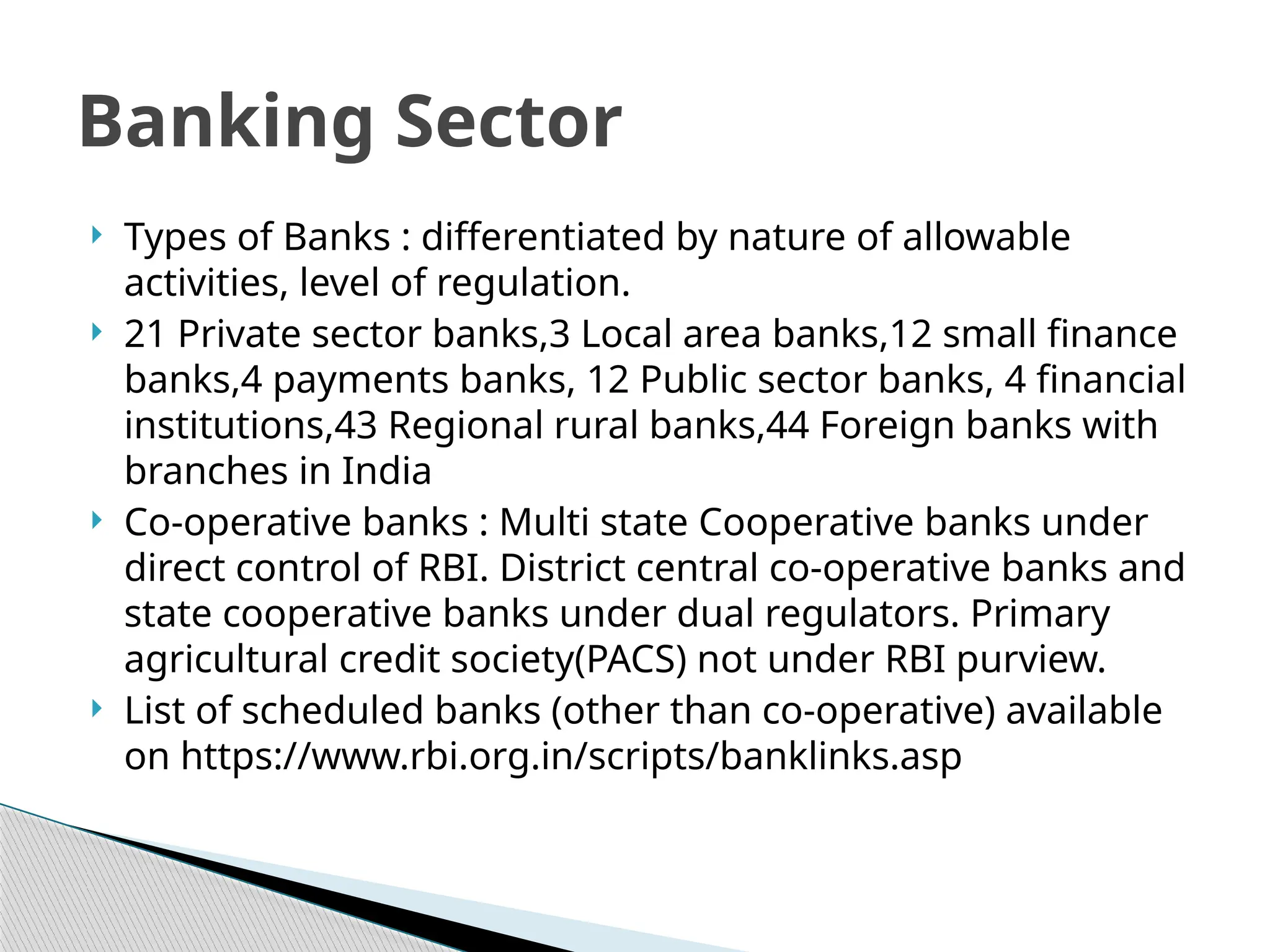

Types ofBanks : differentiated by nature of allowable

activities, level of regulation.

21 Private sector banks,3 Local area banks,12 small finance

banks,4 payments banks, 12 Public sector banks, 4 financial

institutions,43 Regional rural banks,44 Foreign banks with

branches in India

Co-operative banks : Multi state Cooperative banks under

direct control of RBI. District central co-operative banks and

state cooperative banks under dual regulators. Primary

agricultural credit society(PACS) not under RBI purview.

List of scheduled banks (other than co-operative) available

on https://www.rbi.org.in/scripts/banklinks.asp

Banking Sector

64.

Public sectorbanks hold around 66% of the total

assets of the banking sector

Private sector banks have better profitability than

Public sector banks

Profitability under pressure sue to tough competition

from fintech; especially in retail segment

Increase in bank branches and ATMs (of private

sector banks)

Exposure of private sector banks to sensitive sectors

like Real estate is lowering but still higher than that

of Public sector banks

Key Trends

65.

During andpost pandemic, deposits have grown at a

higher pace than advances(PSBs gathering more

deposits than PVBs); excessive profitability. Low

economic activity and risk aversion causing low credit

growth. This trend has now reversed.

Lending to Retail sector increasing while that to

Industry and agriculture is showing a dip

GNPA ratio of industries is highest with large accounts

going bad from FY 17-18.

Increasing Co-lending arrangements

Issuance of green bonds & Foreign currency bonds by

Banks

Key trends

66.

IBC proceedingsa dominant source of recovery

from NPAs

Retail fraud – a concern

Need to increase investor awareness

Consolidation occurring in the sector in Public

sector banks as well as Private sector banks

Key trends

67.

Increase intechnology enabled solutions

Customer centric approaches

Mobile penetration with low cost internet – a

boost to use of telecom for banking services-

driving financial inclusion

Expected increase in NPAs given the rolling

back of policy measures and the standstill in

asset classification allowed to banks

Notable increase in digital payments like

UPI,NEFT,IMPS

Key trends

68.

Increasing collaborationand competition between

banks and fintechs

Use of technology to reduce costs and provide

transparency, flexibility and last mile financial services

to hinterland driving fintechs

Digital lending, use of blockchain, application of AI and

ML are the emerging areas of influence for fintechs

Regulatory sandbox mechanism (recently for use of

mobile banking on feature phones ) will be a path

breaking initiative.

Mobile banking, Mobile bill payments, Mobile

commerce: to reduce costs and increase volume

Banks and fintechs

Neo Banking:Digital Banks with no physical presence,

reducing infrastructure and administrative costs and

fostering innovation. In India, they are not allowed to

function in solo, they rely on bank partners to provide

services For eg: Razorpay X,Jupiter, Niyo, Open.

Challenges include lack of trust, limited services,

regulatory hurdles.

Open banking: banking practice that will allow third

party financial providers access to financial data across

the banking sector by use of application programming

interfaces(APIs). Account aggregator service allowed in

India is a step in this direction.

Some new terms related to Banking

Latest trendsin scheduled commercial banks

◦ Stiff competition from Fintech

◦ Higher unsecured lending

◦ Expected to need more capital to face adversity

◦ Issuance of green bonds by AXIS bank

◦ Co-lending agreements

◦ Excessive Liquidity

Latest trends for Small finance Banks

◦ High proportion of unsecured loans

◦ Collection efforts under stress due to COVID pandemic

◦ Lower CASA base, dependent on borrowings and refinance

◦ In need to increase Provision coverage ratios

Banking sector – latest trends

74.

Payment banks

◦Many are yet to break even

◦ Lower interest rates and high initial infrastructure

costs impacting profitability

◦ Generation of capital flows an issue

Co-operative banks

◦ Absence of secondary market for trading shares and

one person –one vote making mobilization of share

capital an issue.

◦ Loan defaults and low capital base is the problem

faced

Banking sector – latest trends

75.

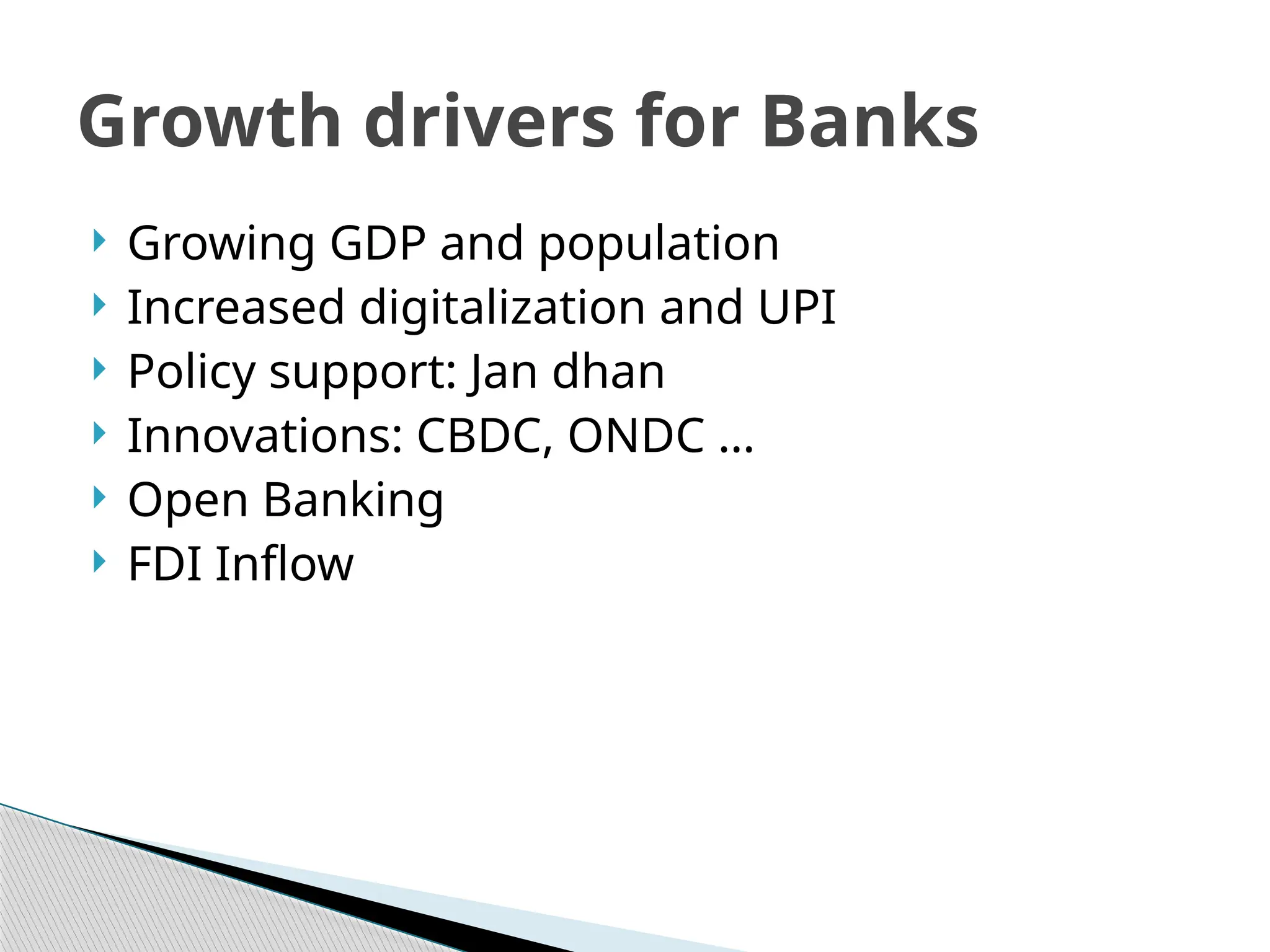

Growing GDPand population

Increased digitalization and UPI

Policy support: Jan dhan

Innovations: CBDC, ONDC …

Open Banking

FDI Inflow

Growth drivers for Banks

76.

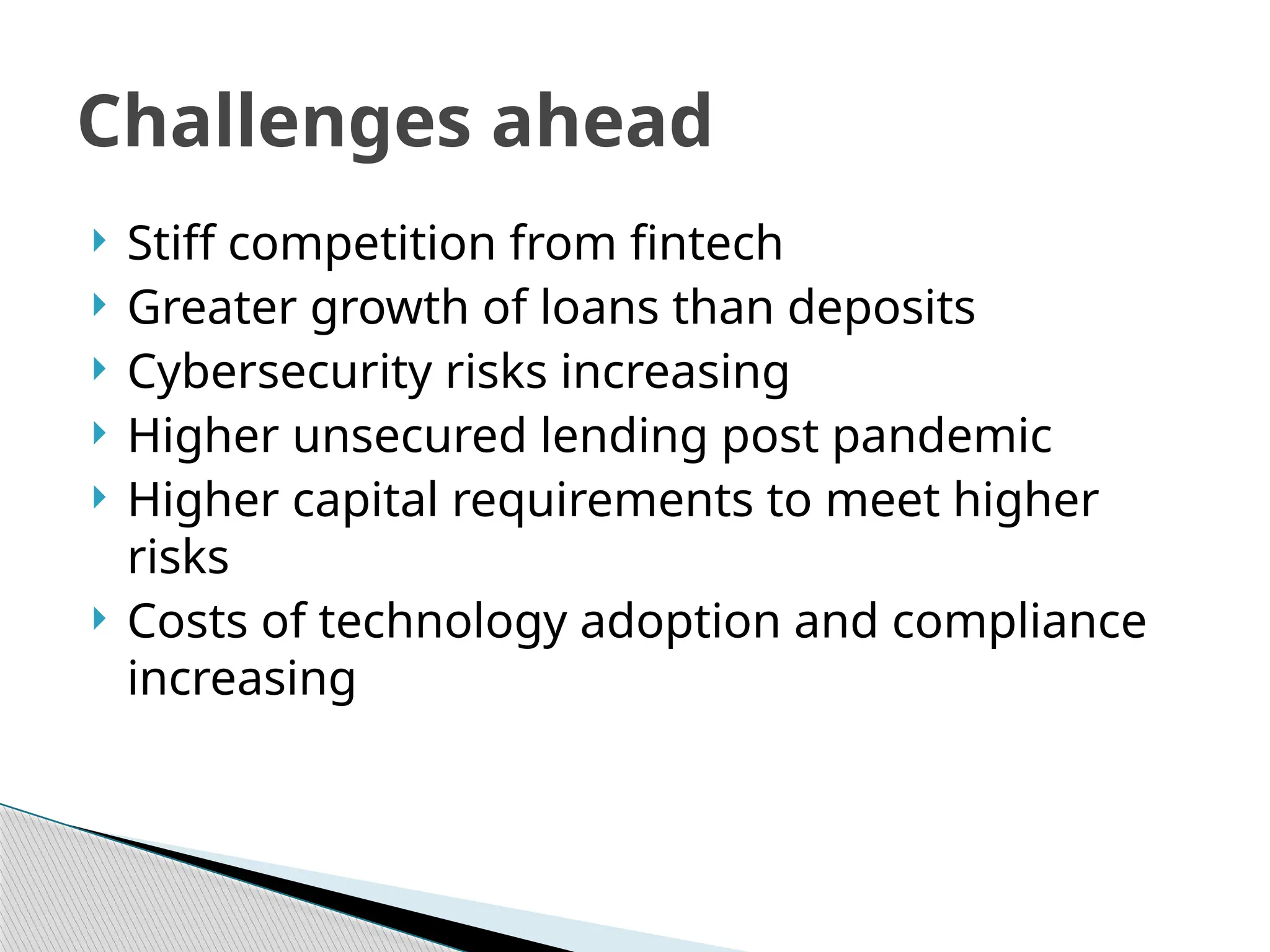

Stiff competitionfrom fintech

Greater growth of loans than deposits

Cybersecurity risks increasing

Higher unsecured lending post pandemic

Higher capital requirements to meet higher

risks

Costs of technology adoption and compliance

increasing

Challenges ahead