1. Credit Views

London

London, 29 November 2012

Market Analysis

BFA-Bankia offers a benign exit option

Credit to subordinated bondholders

Global Credit • The EC has approved the restructuring plans of the four nationalised

Head of Global Credit Research entities

Javier Serna The initial EUR47bn identified by Oliver Wyman has been reduced to EUR37bn due to capital

javier.serna@bbva.com

+44 207 648 7581 management actions. BFA-Bankia will receive EUR18bn, NCG Banco EUR5.4bn, Catalunya

Banc EUR9bn and Banco de Valencia EUR4.5bn.

Europe

Head of European Credit Research

• Following the announcement by the EC, Bankia unveiled its updated

& Covered Bonds

Agustín Martín strategic plan

agustin.martin@bbva.com

+44 207 397 6087 The group aims to be profitable from 2013 and expects to report a net profit of EUR1.2bn in

2015. Pre-provision income should stand at EUR4.1bn and RoE at 10%. The number of

Guilherme Balieiro

guilherme.balieiro@bbva.com

branches will be downsized by 39% to c. 2,000 and headcount by 28% to c. 14,500.

+44 207 397 6075

• The BFA-Group’s recapitalisation stands at EUR18bn and will be carried out

Financials

David Golin *

by mid-December 2012

david.golin@bbva.com During the call management stated that BFA will be recapitalised by means of ESM bonds.

+44 207 648 7501

However, there is still uncertainty on both the timing and on in which form Bankia will receive

Antonio Vilela * capital from its holding company.

antonio.vilela@bbva.com

+44 207 648 7682 • BFA-Bankia group has disclosed the losses to be imposed on subordinated

Corporates bondholders

Ana Greco

ana.greco@bbva.com

Subordinated bondholders will receive a generous exit offer. Tier 1 debt will be swapped into

+44 207 648 7669 Bankia shares at 61% of par value and Upper Tier 2 at 54%. For LT2 bonds, the group’s

restructuring could permit the exchange into shares at 84% or into a senior BFA zero coupon

Sabrina Ran

sabrina.ran@bbva.com bond.

+44 207 397 6082

• An important step towards the resolution of the Spanish banking crisis, in

Public Sector

Mercedes Ferrer our view

mercedes.ferrer@bbva.com Bear in mind that the largest capital shortfall of the domestic banking system is related to

+44 207 648 7655

BFA-Bankia group. Its imminent recapitalisation and restructuring, with most of its problematic

* Author/s of this report real-estate assets transferred to the bad bank should ensure its solvency and viability. This

should boost confidence in the rest of the sector, in our view.

PLEASE SEE IMPORTANT DISCLOSURES ON THE LAST THREE PAGES OF THIS REPORT

2. Credit Views

London, 29 November 2012

The EC approves the restructuring plans

of the four nationalised Spanish banks

The EC has just approved the recapitalisation plans for the four nationalised banks, BFA-Bankia,

NCG, Catalunya Banc and Banco de Valencia (BdV). The disbursement of capital by the ESM to

the FROB will take place in the first half of December. Subsequently, the FROB will inject the

capital into the banks once the necessary corporate operations have been completed.

It is important to highlight that although OW identified a capital shortfall of EUR47bn in these four

entities, the capital needs of the entities will be reduced by the transfer of real estate assets to the

SAREB, the assumption of losses by the subordinated bondholders and restructuring measures

(asset disposals). This will reduce the capital needs of the four entities by EUR10bn to EUR37bn, of

which EUR18bn for BFA-Bankia, EUR5.4bn for NCG, EUR9bn for Catalunya Banc and EUR4.5bn for

BdV.

According to the restructuring plans, by 2017 the balance sheet of each bank will be reduced by

more than 60% compared to 2010. In particular, the banks will refocus their business models on

retail and SME lending in their historical core regions.

Finally it is important to note that if NCG Banco and Catalunya Banc are not sold before 2017, the

entities will be liquidated (orderly resolution plan). This does not apply to BFA-Bankia as it is a

systemic institution. Also, during the call Mr Almunia clearly stated that the liquidation of BdV

would have been more expensive than selling it to CaixaBank despite the support provided for

the transaction.

The EC will disclose the capital requirements for the Group 2 banks, (CEISS, BMN, Caja3 and

Liberbank) on 20 December.

Bankia unveiled its new strategic plan following the EC

announcement

Following the announcement of the European Commission’s approval of the restructuring plans

of the four nationalised banks, Bankia updated its 2012-2015 strategic plan. The key elements of

this plan are set out below:

• A EUR17,959mn injection of state aid (including the EUR4,500mn already injected).

• The group aims to be profitable starting 2013 and to report a net profit of EUR1.2bn in 2015.

• The bank is targeting new lending for c. EUR52bn up to 2015, of which 84% to corporates.

• Divestment of non-core businesses and non-core strategic assets.

• The number of branches should be downsized by 39% (from 3,117 to c. 1,900-2,000) and

headcount by 28% (from 20,589 to 14,500).

• Operating expenses should decline by 26% to EUR1.8bn. The group’s cost-to-income ratio

should therefore stand at c. 40-45% by 2015.

• Average total assets should decline by 20%, pre-provision income should stand at

c.EUR4,100mn.

• RoE of 10%.

• Excess capital above the 9% core Tier 1 target (EBA) of EUR4.5bn. The group’s risk-weighted

assets should contract from EUR166bn to EUR112bn.

PLEASE SEE IMPORTANT DISCLOSURES ON THE LAST THREE PAGES OF THIS REPORT

Page 2

3. Credit Views

London, 29 November 2012

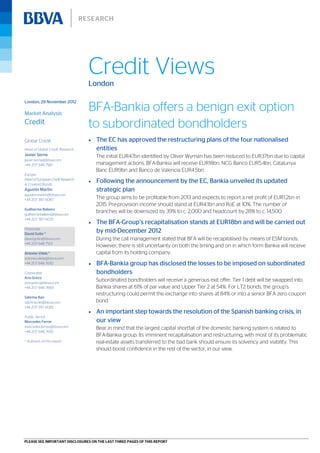

Mostly developer lending to be transferred to SAREB

As at June 2012, the group had EUR57.2bn of commercial real-estate risk (EUR15.9bn real-estate

assets and EUR41.3bn developer loans). After applying the discount to the transfer price to SAREB

(around 49%), this exposure will have a net value of EUR29.3bn, of which EUR24.6bn will comply

with the eligibility criteria to be transferred to the SAREB. The remaining exposure of EUR4.7bn on

Bankia’s books is therefore negligible.

Figure 1

Reduction of real estate risk after transfer to SAREB (EUR bn)

57.2

Real Estate

Assets Discount due

15.9

to transfer

price to

SAREB

27.9

Real Estate

Developer Assets

41.3 transferred

29.3 to SAREB

24.6

4.7

Total gross Net real estate risk Net real estate risk

real estate risk after discount on on the balance sheet

(Data as of 30 June) transfer to SAREB after transfer to SAREB

Source: BFA Group data

Following the transfer of assets to the bad bank, Bankia’s EUR144.6bn loan portfolio at the

end

en d of 2012 will be mainly retail -focused (62%). Corporates should represent 33% and real -

retail- real-

developers

estate developers will just represent just 2%.

Update on the liquidity profile

The BFA-Bankia group has disclosed that it has EUR45.3bn of debt maturities, of which EUR32.8bn

by 2017. According to the entity, liquid assets stood at EUR12.2bn in October 2012, but taking into

account the capital increase (EUR13.5bn as EUR4.5bn has been already injected) and the

EUR24.6bn government-guaranteed debt issued by SAREB in exchange for assets transferred,

liquid assets will increase to EUR40.3bn. This figure also takes into consideration the EUR10bn

reduction in liquid assets due to the fact that Bankia’s eligible OC would be below 25% as a

consequence of transfer of assets to SAREB. Therefore the issuer will be requested to amortize

retained covered bonds.

Liquid assets will thus cover 89% of the debt maturities or 120% of debt maturities up to 2017.

The entity has a LTD ratio of 164% in June 2012, which should decrease to 143% at the end of

2012e after transferring the real estate assets to SAREB. The group has a target LTD ratio of 120%

in 2015.

PLEASE SEE IMPORTANT DISCLOSURES ON THE LAST THREE PAGES OF THIS REPORT

Page 3

4. Credit Views

London, 29 November 2012

As regards the group’s reliance on the ECB and its exit strategy, the entity has stated that this

money is currently funding its bond portfolio and the exposure will decline as government

securities mature.

Figure 2

Impact of recapitalisation plan on BFA Group’s liquidity

Liquid assets – Dec 2012e (EUR bn) Wholesale maturities

Liquid assets (October) 12.2 Covered bonds (roll-over capacity) 30.5

SAREB bonds 24.6 Rest of maturities 14.8

Impact of transfer to SAREB on covered bonds (10.0) Total BFA Group maturities 45.3

Capital injection, BFA Group (net)* 13.5 Of which, maturing before end 2017 32.8

Total liquid assets 40.3

* Net of the €4.5 bn already injected

Source: BFA Group data

The recapitalisation will amount to EUR18bn, less than OW’s EUR24.7bn

Oliver Wyman initially estimated a capital shortfall for BFA-Bankia group of EUR24.7bn. The

injection of public aid to be made in December 2012 stands at EUR18bn. As can be seen in Figure

3 below, this is the result of the EUR200mn capital relief derived from the transfer of assets to the

bad bank and the benefit of EUR6.5bn which will come from the liability management transaction.

The EUR4.5bn already injected in September 2012 (after the severe losses that the group

experienced in 1H12 following which the group had to be recapitalised as its capital fell below the

minimum regulatory level) also has to be deducted from the original EUR24.7bn.

During the call the management stated the BFA will be recapitalised in the form of ESM bonds

and before the end of the year. However nothing was said about the type of instrument that will

be utilised to recapitalise Bankia, or the timing.

Figure 3

Group recapitalisation – determination of final capital needs (EUR bn)

BFA Group capital needs – Oliver Wyman adverse scenario 24.7

-/+ Impact on capital needs due -/+ to transfer of assets to SAREB -0.2

-/+ Hybrid instruments -6.5

Capital to be contributed by shareholders 18.0

Of which, injected in September 2012 4.5

Source: BFA Group data

Losses imposed on subordinated bondholders are

less than expected

Subordinated bondholders will receive a generous exit offer, Tier 1 debt will be swapped into

Bankia shares at 61% of par value, and Upper Tier 2 at 54%. LT2 bonds can be either swapped into

shares at a 14% discount or into senior BFA zero coupon bonds with a discount of 1.5% per month

until the maturity date of the LT2 security. In our view, given the discount rate, the second option

would be applied only to low duration BFA bonds.

The process for assessing the haircut to applied to each security is as follows: the economic value

will be determined by discounting a bond’s cash flow by using a discount rate of 20% for Tier 1

securities, (15% UT2 and 10% LT2). 10 points have then been added to the economic value, being

the maximum premium allowed by the Memorandum of Understanding and a further 20 points

as equity will be given instead of cash.

PLEASE SEE IMPORTANT DISCLOSURES ON THE LAST THREE PAGES OF THIS REPORT

Page 4

5. Credit Views

London, 29 November 2012

This method of calculating the terms of the exchange explains why subordination rights appear

not to have been respected given that the haircut applied to UT2 is higher than applied to the

preference shares. We are in touch with the issuer on this and will pass on any further information

provided.

We have to acknowledge that haircuts applied to hybrids and subordinated debt are less than

either our estimates or those implied by market levels. Management has said that the timing of

the exchange has not been decided yet. In particular, at this stage it is still uncertain if it will be

implemented before or after the recapitalisation.

However, during the conference call, Bankia’s management stated that the dilution risk deriving

from the issue of new shares has already been taken into consideration when the terms of the

exchange were set.

From our conversation with management, we understood that the liability management will be

initially implemented on a voluntary basis. However we recall that according to the

Memorandum of Understanding “steps will be taken to minimise the cost to taxpayers of bank

restructuring. After allocating losses to equity holders, the Spanish authorities will require burden

sharing measures from hybrid capital holders and subordinated debt holders in banks receiving

public capital, including by implementing both voluntary and, where necessary, mandatory

Subordinated Liability Exercises (SLEs). Banks not in need of State aid will be outside the scope of

any mandatory burden sharing exercise. The Banco de España, in liaison with the European

Commission and the EBA, will monitor any operations converting hybrid and subordinated

instruments into senior debt or equity”.

The risk here is therefore that a subsequent mandatory liability management exercise could

follow the initial voluntary one. That said, we expect the participation rate in the voluntary

exercise to be substantial. The distinction here between voluntary or mandatory exchange offer is

important as the second is a restricting credit event and therefore triggers CDS contracts.

PLEASE SEE IMPORTANT DISCLOSURES ON THE LAST THREE PAGES OF THIS REPORT

Page 5

6. Credit Views

London, 29 November 2012

Market & Client Strategy

Director

Antonio Pulido

ant.pulido@bbva.com

+34 91 374 31 81

Global Credit

Head of Global Credit Research

Javier Serna

javier.serna@bbva.com

+44 207 648 7581

Credit Europe

Head of European Credit Corporates Americas

Research & Covered Bonds Ana Greco

ana.greco@bbva.com

Agustín Martín +44 207 648 7669

New York

agustin.martin@bbva.com Jose Bernal

+44 207 397 6087 jose.bernal@bbvany.com

Sabrina Ran

sabrina.ran@bbva.com +1 212 728 1561

Guilherme Balieiro

guilherme.balieiro@bbva.com +44 207 397 6082

+44 207 397 6075 Mexico

Public Sector Edgar Cruz

Financials Mercedes Ferrer edgar.cruz@bbva.com

David Golin mercedes.ferrer@bbva.com +52 55 5621 9774

david.golin@bbva.com +44 207 648 7655

+44 207 648 7501

Antonio Vilela

antonio.vilela@bbva.com

+44 207 648 7682

PLEASE SEE IMPORTANT DISCLOSURES ON THE LAST THREE PAGES OF THIS REPORT

Page 6

7. Credit Views

London, 29 November 2012

Important Disclosures

The BBVA Group companies identified by the research analysts’ names included on the front page of this report have participated in or contributed to its

preparation, including the information, opinions, estimates, forecasts and recommendations therein.

For recipients in the European Union, this document is distributed by Banco Bilbao Vizcaya Argentaria, S.A. (hereinafter called "BBVA"). BBVA is a bank

supervised by the Bank of Spain and by Spain’s Stock Exchange Commission (CNMV), registered with the Bank of Spain with number 0182.

For recipients in Mexico, this document is distributed by BBVA Bancomer, S.A. Institución de Banca Múltiple, Grupo Financiero BBVA Bancomer (hereinafter

called “BBVA Bancomer”). BBVA Bancomer is a bank supervised by the Comisión Nacional Bancaria y de Valores de México.

For recipients in USA, this document is being distributed by BBVA Securities Inc. (hereinafter called “BBVA Securities”), a subsidiary of Banco Bilbao Vizcaya

Argentaria, S.A. (“BBVA”) registered with and supervised by the U.S. Securities and Exchange Commission and a member of the Financial Industry Regulatory

Authority (“FINRA”) and the Securities Investor Protection Corporation. U.S. persons wishing to execute any transactions should do so only by contacting a

representative of BBVA Securities in the U.S. Unless local regulations provide otherwise, non-U.S. persons should contact and execute transactions through a

BBVA branch or affiliate in their home jurisdiction.

BBVA and BBVA Group companies or affiliates (art. 42 of the Royal Decree of 22 August 1885 Code of Commerce), are subject to the BBVA Group Policy on

Conduct for Security Market Operations which establishes common standards for activity in these entities’ markets, but also specifically for analysis and

analysts. This BBVA policy is available for reference at the following web site: www.bbva.com.

Analysts residing outside the U.S. who have contributed to this report are not registered with or qualified as research analysts by FINRA or the New York

Stock Exchange and may not be considered “associated persons” of BBVA Securities (as such term is construed by the rules of FINRA). As such, they are not

subject to NASD Rule 2711 restrictions on communications with subject companies, public appearances and trading of securities held in research analysts’

accounts.

BBVA or any of its affiliates beneficially owned at least 1 % of the common equity securities of the following companies covered in this report: N/A.

In the past twelve months, BBVA or one or more of its affiliates managed or co-managed public offerings of the following companies covered in this

report: N/A.

In the past twelve months, BBVA or one or more of its affiliates has received compensation for investment banking services from the following

companies covered in this report: N/A

In the next three months, BBVA or one or more of its affiliates expects to receive or intends to seek compensation for investment banking services from

the companies covered in this report: Bankia.

BBVA or one or more of its affiliates makes a market/provides liquidity in the securities of the following companies covered in this report: N/A.

BBVA is subject to a Code of Conduct for Security Market Operations, which details the standards of the above-mentioned overall policy for the EU.

Among other regulations, it includes rules to prevent and avoid conflicts of interests with the ratings given, including information barriers. This Code of

Conduct for Security Market Operations is available for reference in the ‘Corporate Governance’ section of the following web site: www.bbva.com.

BBVA Bancomer is subject to a Code of Conduct and to Internal Standards of Conduct for Security Market Operations, which details the standards of the

above-mentioned overall policy for Mexico. Among other regulations, it includes rules to prevent and avoid conflicts of interests with the ratings given,

including information barriers. This Code and the Internal Standards are available for reference in the ‘Grupo BBVA Bancomer’ subsection of the

‘Conócenos’ menu of the following web site: www.bancomer.com.

BBVA Securities is subject to a Capital Markets Code of Conduct, which details the standards of the above-mentioned overall policy for USA. Among

other regulations, it includes rules to prevent and avoid conflicts of interests with the ratings given, including information barriers.

Page 7

8. Credit Views

London, 29 November 2012

Exclusively for Recipients Resident in Mexico

In the past twelve months, BBVA Bancomer has granted banking credits to the following companies covered in this report: N/A.

In the past twelve months, BBVA Bancomer has granted Common Representative services to the following companies covered in this report: N/A.

As far as it is known, a Director, Executive Manager or Manager reporting directly to the BBVA Bancomer General Manager has the same position in the

following companies that may be covered in this report: N/A.

BBVA Bancomer S.A. Institución de Banca Múltiple, Grupo Financiero BBVA Bancomer acts as a market maker/specialist in: MexDer Future Contracts (US

dollar [DEUA], 28-day TIIEs [TE28], TIIE Swaps, 91-day CETES [CE91]), Bonos M, Bonos M3, Bonos M10, BMV Price and Quotations Index (IPC), Options

Contracts (IPC, shares in América Móvil, Cemex, CPO, Femsa UBD, Gcarso A1, Telmex L) and Udibonos.

BBVA Bancomer, and, as applicable, its affiliates within BBVA Bancomer Financial Group, may hold from time to time investments in the securities or

derivative financial instruments with underlying securities covered in this report, which represent 10% or more of its securities or investment portfolio, or 10%

or more of the issue or underlying of the securities covered.

Ratings System, Distribution and History

Meaning of Ratings

We have three ratings for bonds based on our current expectations of relative returns over a six month period: i.) Buy – we expect the bond to outperform its

peer group, sector or relevant benchmark; ii.) Hold - we expect the bond to perform in-line with its peer group, sector or relevant benchmark; and iii.) Sell - we

expect the bond to underperform its peer group, sector or relevant benchmark. Factors which may influence our ratings include: current market prices and

conditions, operating issues and financing needs which may impact an issuer’s ability to service its debts, macroeconomic trends and outlook for interest

rates, specific features of an issue, and the potential for a change in rating by credit rating agencies.

Analyst Certification

The Research analysts included on the front page of this report hereby certify that (i) the views expressed in this report accurately reflect their personal views

about the subject companies and their securities and (ii) no part of my compensation was, is, or will be, directly or indirectly, related to the specific

recommendations or views expressed in this report.

Page 8

9. Credit Views

London, 29 November 2012

Disclaimer

This document and the information, opinions, estimates, forecasts and recommendations expressed herein have been prepared to provide BBVA Group’s

customers with general information and are current as of the date hereof and subject to changes without prior notice. Neither BBVA nor any of its affiliates is

responsible for giving notice of such changes or for updating the contents hereof.

This document and its contents do not constitute an offer, invitation or solicitation to purchase or subscribe to any securities or other instruments, to

undertake or divest investments, or to participate in any trading strategy. Neither shall this document nor its contents form the basis of any contract,

commitment or decision of any kind.

Investors who have access to this document should be aware that the securities, instruments or investments to which it refers may not be appropriate

for them due to their specific investment goals, financial positions or risk profiles, as these have not been taken into account to prepare this report.

Therefore, investors should make their own investment decisions considering the said circumstances and obtaining such specialized advice as may be

necessary. Other than the disclosures relating to BBVA Group, the contents of this document are based upon information available to the public that has

been obtained from sources considered to be reliable. However, such information has not been independently verified by BBVA or any of its affiliates and

therefore no warranty, either express or implicit, is given regarding its accuracy, integrity or correctness. To the extent permitted by law, BBVA and its

affiliates accept no liability of any type for any direct or indirect losses or damages arising from the use of this document or its contents. Investors

should note that the past performance of securities or instruments or the historical results of investments do not guarantee future performance.

The market prices of securities or instruments or the results of investments could fluctuate against the interests of investors. Investors should be aware

that they could even face a loss of their investment. Transactions in futures, derivatives, options on securities or high-yield securities can involve high

risks and are not appropriate for every investor. Indeed, in the case of some investments, the potential losses may exceed the amount of initial

investment and, in such circumstances, investors may be required to pay more money to support those losses. Thus, before undertaking any

transaction with these instruments, investors should be aware of their operation, as well as the rights, liabilities and risks implied by the same and the

underlying securities. Investors should also be aware that secondary markets for the said instruments may not exist.

BBVA or any of its affiliates’ salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to its clients

that reflect opinions that are contrary to the opinions expressed herein. Furthermore, BBVA or any of its affiliates' proprietary trading and investing businesses

may make investment decisions that are inconsistent with the recommendations expressed herein. No part of this document may be (i) copied, photocopied

or duplicated by any other form or means (ii) redistributed or (iii) quoted, without the prior written consent of BBVA. No part of this report may be copied,

conveyed, distributed or furnished to any person or entity in any country (or persons or entities in the same) in which its distribution is prohibited by law.

More specifically, this document is in no way intended for, or to be distributed or used by an entity or person resident or located in a jurisdiction in which the

said distribution, publication, use of or access to the document contravenes the law which requires BBVA or any of its affiliates to obtain a licence or be

registered. Failure to comply with these restrictions may breach the laws of the relevant jurisdiction.

The remuneration system concerning the analysts responsible for the preparation of this report is based on multiple criteria, including the revenues obtained

by BBVA and, indirectly, the results of BBVA Group in the fiscal year, which, in turn, include the results generated by the investment banking business;

nevertheless, they do not receive any remuneration based on revenues from any specific transaction in investment banking.

In the United Kingdom, this document is directed only at persons who (i) have professional experience in matters relating to investments falling within article

19(5) of the financial services and markets act 2000 (financial promotion) order 2005 (as amended, the "financial promotion order"), (ii) are persons falling

within article 49(2) (a) to (d) (“high net worth companies, unincorporated associations, etc.”) of the financial promotion order, or (iii) are persons to whom an

invitation or inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000) may otherwise

lawfully be communicated (all such persons together being referred to as "relevant persons"). This document is directed only at relevant persons and must

not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this document relates is available only

to relevant persons and will be engaged in only with relevant persons.

BBVA Hong Kong Branch (CE number AFR194) is regulated by the Hong Kong Monetary Authority and the Securities and Futures Commission of Hong

Kong.

This document is distributed in Singapore by BBVA’s office in this country for general information purposes and it is generally accessible. In this respect, this

document does not take into account the specific investment goals, the financial situation or the need of any particular person and it is exempted from

Regulation 34 of the Financial Advisors Regulation (“FAR”) (as required in Section 27 of the Financial Advisors Act (Chapter 110) of Singapore (“FAA”))

BBVA, BBVA Bancomer and BBVA Securities are not authorised deposit institutions in accordance with the definition of the Banking Act 1959 nor are they

regulated by the Australian Prudential Regulatory Authority (APRA)

General Disclaimer for Readers Accessing the Report through the Internet

Internet Access

In the event that this document has been accessed via the internet or via any other electronic means which allows its contents to be viewed, the following

information should be read carefully:

The information contained in this document should be taken only as a general guide on matters that may be of interest. The application and impact of laws

may vary substantially depending on specific circumstances. BBVA does not guarantee that this report and/or its contents published on the Internet are

appropriate for use in all geographic areas, or that the financial instruments, securities, products or services referred to in it are available or appropriate for

sale or use in all jurisdictions or for all investors or counterparties. Recipients of this report who access it through the Internet do so on their own initiative and

are responsible for compliance with local regulations applicable to them.

Changes in regulations and the risks inherent in electronic communications may cause delays, omissions, or inaccuracy in the information contained in this

site. Accordingly, the information contained in the site is supplied on the understanding that the authors and editors do not hereby intend to supply any form

of consulting, legal, accounting or other advice.

All images and texts are the property of BBVA and may not be downloaded from the Internet, copied, distributed, stored, re-used, re-transmitted, modified or

used in any way, except as specified in this document, without the express written consent of BBVA. BBVA reserves all intellectual property rights to the fullest

extent of the law.

Page 9