Bangalore office rental insights april 2014

•

0 likes•622 views

The office rental Insight is a quick guide for Grade A office rental values, absorption, new supply and vacancy trends in major cities in India.

Report

Share

Report

Share

Download to read offline

Recommended

Chennai office rental insights april 2014

The office rental Insight is a quick guide for Grade A office rental values, absorption, new supply and vacancy trends in major cities in India.

Tableau - ANAND CHOKHI DEMO - Lines (3) Bar Chart

This data shows the profit, quantity, and sales amounts for each month from 2011 to 2015. The sums of profit, quantity, and sales are plotted on a line and bar chart to visualize the trends over time for these values grouped by month of the order date.

Delhi office market overview jan 2015

Delhi witnessed strong office leasing growth in 2014, with absorption nearly doubling compared to 2013. The IT/ITeS sector accounted for the majority of demand. Limited new supply was added in 2014, reducing overall vacancy slightly. Rents remained stable across most markets except for a 2% increase in Jasola and 1% decrease in Connaught Place. The outlook for 2015 is continued recovery in demand and stable rents, with new supply helping maintain equilibrium.

Kolkata office market overview jan 2015

The Kolkata office market remained subdued in 2014 with total absorption of around 1.66 million square feet, similar to 2013 levels. Demand was led by the BFSI, IT/ITES, and construction sectors. Limited supply addition of 1.14 million square feet and below-average absorption kept vacancy levels stable. Grade A office rents declined 7% year-over-year across micromarkets except one. Capital values decreased 16% year-over-year in peripheral locations but increased 3% in the CBD due to domestic investor demand. The market is expected to remain stagnant in 2015 until policy level issues are addressed.

Pune office rental insights april 2014

The office rental Insight is a quick guide for Grade A office rental values, absorption, new supply and vacancy trends in major cities in India.

Mumbai office rental insights april 2014

The office rental Insight is a quick guide for Grade A office rental values, absorption, new supply and vacancy trends in major cities in India.

Mumbai Office Rental Insight July 2013

The office rental insight will provide you a quick update on the major trends of Office rentals, vacancy, new supply and market transaction in 2Q 2013.

India office property market overview april 2014

HIGHLIGHTS

• uring 1Q 2014, office absorption in eight major cities was recorded at around 8 MN SF, 7% up from last quarter.

•Bangalore and NCR topped the chart contributing 75% in the total absorption.

•All markets, with the exception of Mumbai, Chennai and Pune, have witnessed increase in office absorption.

•With positive signals emanating from the global economy, which finds resonance in our improved export performance, we anticipate further improvement in sentiments after the elections

Recommended

Chennai office rental insights april 2014

The office rental Insight is a quick guide for Grade A office rental values, absorption, new supply and vacancy trends in major cities in India.

Tableau - ANAND CHOKHI DEMO - Lines (3) Bar Chart

This data shows the profit, quantity, and sales amounts for each month from 2011 to 2015. The sums of profit, quantity, and sales are plotted on a line and bar chart to visualize the trends over time for these values grouped by month of the order date.

Delhi office market overview jan 2015

Delhi witnessed strong office leasing growth in 2014, with absorption nearly doubling compared to 2013. The IT/ITeS sector accounted for the majority of demand. Limited new supply was added in 2014, reducing overall vacancy slightly. Rents remained stable across most markets except for a 2% increase in Jasola and 1% decrease in Connaught Place. The outlook for 2015 is continued recovery in demand and stable rents, with new supply helping maintain equilibrium.

Kolkata office market overview jan 2015

The Kolkata office market remained subdued in 2014 with total absorption of around 1.66 million square feet, similar to 2013 levels. Demand was led by the BFSI, IT/ITES, and construction sectors. Limited supply addition of 1.14 million square feet and below-average absorption kept vacancy levels stable. Grade A office rents declined 7% year-over-year across micromarkets except one. Capital values decreased 16% year-over-year in peripheral locations but increased 3% in the CBD due to domestic investor demand. The market is expected to remain stagnant in 2015 until policy level issues are addressed.

Pune office rental insights april 2014

The office rental Insight is a quick guide for Grade A office rental values, absorption, new supply and vacancy trends in major cities in India.

Mumbai office rental insights april 2014

The office rental Insight is a quick guide for Grade A office rental values, absorption, new supply and vacancy trends in major cities in India.

Mumbai Office Rental Insight July 2013

The office rental insight will provide you a quick update on the major trends of Office rentals, vacancy, new supply and market transaction in 2Q 2013.

India office property market overview april 2014

HIGHLIGHTS

• uring 1Q 2014, office absorption in eight major cities was recorded at around 8 MN SF, 7% up from last quarter.

•Bangalore and NCR topped the chart contributing 75% in the total absorption.

•All markets, with the exception of Mumbai, Chennai and Pune, have witnessed increase in office absorption.

•With positive signals emanating from the global economy, which finds resonance in our improved export performance, we anticipate further improvement in sentiments after the elections

Ncr office rental insights april 2014

The office rental Insight is a quick guide for Grade A office rental values, absorption, new supply and vacancy trends in major cities in India.

Colliers Quarterly-Bengaluru-Q1 2017

In Q1 2017, occupiers mainly continued expansion in

southern peripherals. Though we expect occupier

demand to remain upbeat in these locations, the

upcoming new supply is unlikely to meet the rising

demand in coming quarters resulting in upward

pressure on rents. Absorption of pre-committed

spaces coupled with expected demand upsurge is

likely to outpace the upcoming supply pipeline of 8.1

mn sq ft (757,160 sq m) by the year end.

India Office Property Market Overview July 2013

The occupiers’ demand remained cautious regarding expansion plans in almost all cities amid global economic crisis. The six major cities ie; Mumbai, NCR, Bengaluru, Chennai, Kolkata and Pune recorded an overall absorption of around 6.93 million sq ft which is approximately 15% less than 1Q 2013. Top ranking city for highest absorption rate continues to be Bangalore, Mumbai and NCR region with levels of 2.5 mln sq. ft., 1.41 mln sq. ft. and 1.45 mln sq. ft respectively.

Commercial Rental Property Management Ppt.

The document provides quarterly commercial property market reports for major Indian cities including Mumbai, Delhi, Bangalore and Kolkata. It summarizes office space supply and rental values across different sub-markets in each city. It also discusses growth drivers for the commercial and retail sectors in India and outlines the business model, funding requirements and profitability projections for a proposed commercial real estate startup.

HDFC Securities' Top NCD picks for June

This document provides a summary of various tax-free and taxable bonds available for retail investors in India. It includes details such as the issuer, bond series, coupon rate, tenure, credit rating, last traded price and yield for each bond. The average daily trading volumes and yield to maturity are also specified. The document concludes with notes on credit ratings, listings, face values and other terms for retail investors to be aware of.

Chennai Office Property Market Overview Jan 2017

Steady decline in headline vacancy rates, increase in rents in CBD and SBD, pushed the occupiers to peripheral areas. In our opinion peripheral markets should continue to gain the occupier preference as most of the new supply is concentrated in this micro markets.

Chennai Office Property Market Overview Jan 2017

Steady demand for office space in Chennai is expected to continue in 2017. While vacancy rates have declined, rents have increased in the city center (CBD) and surrounding areas (Off-CBD), pushing occupiers to peripheral areas along Old Mahabalipuram Road (OMR). An estimated 2.8 million square feet of new supply will be added in 2017, concentrated in OMR, further stimulating demand. Continued absorption of existing and upcoming supply is forecast to keep overall vacancy stable while driving rental increases of 5-10% across most markets in Chennai.

Larsen & Toubro Outthink - 2016, IIM Rohtak Final Round

This presentation was prepared for Larsen and Toubro's Outthink -2016 case study competition. The case was based on project finance, where participants were asked to perform a feasibility analysis of a real estate project.

Colliers Quarterly Kolkata Q1 2017

We expect tenant favourable conditions to attract

domestic companies and Information Technology

majors to expand operations mainly in the New

Town, Rajarhat and Sector V micromarkets. Rents

are likely to register a 3-5% dip in Sector V and

peripheral areas of New Town and Rajarhat as

property owners are likely to remain flexible on rents

to boost occupancy in their buildings.

India Office Property Market Overview October 2015

Office market absorption in India reached 30 million square feet year-to-date, an 11% increase over the previous year. Major cities like Bengaluru, Gurgaon and Mumbai are expected to see continued office space uptake in the coming quarter. Rents remained stable across most markets except some areas of Gurgaon, Bengaluru and Pune which saw declines. The report provides an overview of the office markets in key cities like Mumbai, Delhi, Gurgaon, NOIDA, Chennai, Bengaluru, Kolkata, Pune and includes statistics on absorption, vacancy, rents and major transactions.

Telecommunication in India

In this presentation I have explained about telecommunication in India.

topics covered are as under

Telecom Industry Overview

Major Players in Telecom Sector

Emerging Trends in Telecom Market

Growth Avenues

Role of Cost & Management Accountant in Telecom sector

Q & A session.

http://www.airtel3gplans.com/airtel-3g-plans/all-airtel-3g-plans-details/

Technology Smart City Opportunity - India

With a new governmental push towards building smart cities in India, there lies a huge technological and business opportunity. The report takes a detailed look at these.

Mumbai Real Estate Outlook Report H1 2015

This is our third edition of the flagship half yearly report - India Real Estate.

It presents a comprehensive analysis of the residential and office market performance of the Mumbai Metropolitan Region for the period between January–June 2015 (H1 2015).

Mumbai Real Estate Outlook January - June 2014

- Housing launches in Mumbai declined 38% in the first half of 2014 compared to the same period in the previous year, while housing absorption declined 25%. However, launches and absorption are forecast to increase 10% and 49% respectively in the second half of 2014.

- The demand-supply gap has led to a large inventory of over 213,000 unsold housing units. The time taken to liquidate this inventory has more than doubled from 5 quarters to 12 quarters over the last two years.

- Peripheral areas like Central Suburbs and Western Suburbs continue to be the largest markets, though their share of new launches has declined. The unsold inventory is highest in the expensive South Mumbai market, though it accounts

decompositionExample of classical decompositionMovingCenteredRawQu.docx

decompositionExample of classical decompositionMovingCenteredRawQuarterSales(Y)AverageAverageIndices15021003707576.250.918032786948077.580156082.586.250.6956521739612090901.3333333333710090951.0526315789880100

Input DataForecasting : Decomposition of the Trend and SeasonalitySeasonalYear 1Year 2Year 3Year 4IndexThis Moving Average isQ10.880.840.900.87Centered Between Quarters 2 and 3.Q20.890.880.960.91The next one is centered between 3 and 4,Q30.971.031.011.00and so on.Q41.251.221.171.214.0MovingCenteredRawSeasonalDe-seasPredicted(Y - Y-hat)=(25+28+35+50 ) /4 = 34.5yearQuarterSales (Y)AverageAverageIndicesIndexSales (Yd)Sales (Y-hat)Error11250.870737265728.7118.196.8=(28+35+50+39 ) /4 = 38.012280.908779919730.8124.493.5133534.5036.250.970.999780524435.0132.992.0145038.0040.001.251.214099355641.1847.422.6=(34.50+ 38.0 ) /2 = 36.25253942.0044.500.880.870737265744.7939.28-0.3264447.0049.500.890.908779919748.4246.49-2.5275552.0053.631.030.999780524455.0157.20-2.2= 35 / 36.25 = 0.97287055.2557.251.221.214099355657.6676.81-6.8395259.2562.000.840.870737265759.7260.36-8.43106064.7568.500.880.908779919766.0268.50-8.53117772.2576.381.010.999780524477.0281.41-4.431210080.5085.501.171.214099355682.37106.21-6.24138590.5094.750.900.870737265797.6281.443.641410099.00104.000.960.9087799197110.0490.509.5415111109.000.9997805244111.02105.625.44161401.2140993556115.31135.614.4-0.1BIASCalculated on output pageand copied here.

Input Data

Sales (Y)

Quarter

$ Million

Sales

Output

Sales (Yd)

Quarter

$ Million

Deseasonlized Sales

Sheet3SUMMARY OUTPUTRegression StatisticsMultiple R0.9797R Square0.9598Adjusted R Square0.9569Standard Error6.1049Observations16ANOVAdfSSMSFSignificance FRegression112457.95912457.959334.2670.000Residual14521.77437.270Total1512979.733CoefficientsStandard Errort StatP-valueLower 95%Upper 95%Lower 95.0%Upper 95.0%Intercept14.84193.20144.63600.00047.975521.70837.975521.7083Quarter6.05320.331118.28300.00005.34316.76335.34316.7633Reseasonalize the predicted YdRESIDUAL OUTPUTValues to predict the true salesDeseasonalizedSeasonal(Multiply by the seasonal index)ObservationPredicted Sales (Yd Hat)ResidualsIndexPredicted Y120.89517.81620.87118.19226.94833.86230.90924.49333.00142.00621.00032.99439.05462.12821.21447.42545.1078-0.31820.87139.28651.1610-2.74440.90946.49757.2142-2.20211.00057.20863.2674-5.61151.21476.81969.3206-9.60100.87160.361075.3737-9.35120.90968.501181.4269-4.41001.00081.411287.4801-5.11451.214106.211393.53334.08510.87181.441499.586510.45120.90990.5015105.63975.38471.000105.6216111.69283.61901.214135.61

Perform regression with desasonalized sales to get the underlying trend (Output Sheet)

1

2

3

4

5

6

7

1Rent RollUnit TypeUnit DescriptionNumber of UnitsArea Per Unit (sqft)Monthly Rent/UnitTotal Area (sqft)Monthly Gross Rent/sqftMonthly Gross RentAnnual Gross RentA-11 BR/1BA726887501.0A-21 BR/1.5 BAA-2A1 BR/1 BATotal

2Additional Revenue Sources# of UnitsMonthly Rent/UnitTotal Monthly RentTotal Annual RentGarages2.1Direct AccessAss.

Country Club of Louisiana Baton Rouge Home Sales Q3 2011 vs Q3 2014

Country Club of Louisiana Baton Rouge Home Sales Q3 2011 vs Q3 2014

Country Club of Louisiana Pinterest Board Photos:

http://www.pinterest.com/billdcobb/country-club-of-louisiana-baton-rouge/

Published by Bill Cobb, Greater Baton Rouge's Home Appraiser

225-293-1500

homeappraisalsbatonrouge.com

Based on information from Greater Baton Rouge Association of REALTORS®\MLS for period 07/01/2011 to 09/30/2014, extracted on 10/22/2014.

Global Services Fact Sheet

Looking for an overview of the global services market? Look no further - this 6-page deck offers details on the business process services (BPS), IT services (ITS), and shared services/global in-house center (GIC) markets.

Real Time Gross Settlement

Real time gross settlement systems (RTGS) are specialist funds transfer systems where transfer of money or securities takes place from one bank to another on a "real time" and on "gross" basis. It can be defined as the continuous (real-time) settlement of funds transfers individually on an order by order basis (without netting).

Top investments destination in mumbai mmr jan-jun15

Mumbai property prices are amongst the highest in the country. Slow property sales and inflated pricing has led to buyers postponing their property buying decision considerably resulting in an inventory pile-up of 46 months. Find the detailed analysis for January - June 2015 period.

Results presentation 4Q15

TIM Brasil faced a challenging year in 2015 with slowing GDP growth, high inflation, and a deteriorating currency. However, through maintaining infrastructure investment and focusing on efficiency, TIM was able to defend its EBITDA performance. TIM also repositioned its marketing approach with a new portfolio focused on value, SIM card consolidation, and quality. This helped TIM reduce its dependency on community effects and focus on the evolving middle class segment. Key highlights included expanding 4G coverage leadership, growing data users and revenues, improving network quality, and executing an ongoing efficiency program.

Colliers radar delhi gurgaon and noida the three aces_june 2018

The National Capital Region (NCR), is consistently the second largest office market with 20% share of the annual nationwide leasing volume over the past five years. In our opinion, the NCR should retain its dominance in office demand over the next five years. We expect Delhi to see a facelift with redevelopment projects over the coming years. The satellite city Gurugram should remain the preferred city among corporate occupiers against the backdrop of a business-friendly environment, healthy new supply and infrastructure improvements. NOIDA is likely to come out of its image of affordable technology hub and rise as an emerging commercial market. We advise new entrants to choose well- established micromarkets in Delhi and Gurugram while occupiers looking for affordability should start exploring NOIDA for their large requirements and backend operations. In our opinion, investors should keep the momentum upbeat taking cues from the infrastructure initiatives and optimistic business conditions in the region.

Colliers Radar | Special economic zones in india

The uncertainty regarding the continuity of fiscal incentives is an area of growing concern among various stakeholders in Special Economic Zones (SEZs). Although more than 40.0 million sq ft (3.8 million sq m) of new supply is scheduled for completion before the mandatory deadline of 2020 to qualify for income tax benefits in SEZs, it seems unlikely that all the projects will be completed by then. We advise first-time entrants to pre-commit spaces only in projects that are in advance stages of construction to avoid last-minute delays in starting operations which may lead to disqualification for direct tax benefits. Regardless of optimism among the stakeholders about a further extension of income tax benefits, until this is certain, developers should schedule the completion of construction three to six months in advance

More Related Content

Similar to Bangalore office rental insights april 2014

Ncr office rental insights april 2014

The office rental Insight is a quick guide for Grade A office rental values, absorption, new supply and vacancy trends in major cities in India.

Colliers Quarterly-Bengaluru-Q1 2017

In Q1 2017, occupiers mainly continued expansion in

southern peripherals. Though we expect occupier

demand to remain upbeat in these locations, the

upcoming new supply is unlikely to meet the rising

demand in coming quarters resulting in upward

pressure on rents. Absorption of pre-committed

spaces coupled with expected demand upsurge is

likely to outpace the upcoming supply pipeline of 8.1

mn sq ft (757,160 sq m) by the year end.

India Office Property Market Overview July 2013

The occupiers’ demand remained cautious regarding expansion plans in almost all cities amid global economic crisis. The six major cities ie; Mumbai, NCR, Bengaluru, Chennai, Kolkata and Pune recorded an overall absorption of around 6.93 million sq ft which is approximately 15% less than 1Q 2013. Top ranking city for highest absorption rate continues to be Bangalore, Mumbai and NCR region with levels of 2.5 mln sq. ft., 1.41 mln sq. ft. and 1.45 mln sq. ft respectively.

Commercial Rental Property Management Ppt.

The document provides quarterly commercial property market reports for major Indian cities including Mumbai, Delhi, Bangalore and Kolkata. It summarizes office space supply and rental values across different sub-markets in each city. It also discusses growth drivers for the commercial and retail sectors in India and outlines the business model, funding requirements and profitability projections for a proposed commercial real estate startup.

HDFC Securities' Top NCD picks for June

This document provides a summary of various tax-free and taxable bonds available for retail investors in India. It includes details such as the issuer, bond series, coupon rate, tenure, credit rating, last traded price and yield for each bond. The average daily trading volumes and yield to maturity are also specified. The document concludes with notes on credit ratings, listings, face values and other terms for retail investors to be aware of.

Chennai Office Property Market Overview Jan 2017

Steady decline in headline vacancy rates, increase in rents in CBD and SBD, pushed the occupiers to peripheral areas. In our opinion peripheral markets should continue to gain the occupier preference as most of the new supply is concentrated in this micro markets.

Chennai Office Property Market Overview Jan 2017

Steady demand for office space in Chennai is expected to continue in 2017. While vacancy rates have declined, rents have increased in the city center (CBD) and surrounding areas (Off-CBD), pushing occupiers to peripheral areas along Old Mahabalipuram Road (OMR). An estimated 2.8 million square feet of new supply will be added in 2017, concentrated in OMR, further stimulating demand. Continued absorption of existing and upcoming supply is forecast to keep overall vacancy stable while driving rental increases of 5-10% across most markets in Chennai.

Larsen & Toubro Outthink - 2016, IIM Rohtak Final Round

This presentation was prepared for Larsen and Toubro's Outthink -2016 case study competition. The case was based on project finance, where participants were asked to perform a feasibility analysis of a real estate project.

Colliers Quarterly Kolkata Q1 2017

We expect tenant favourable conditions to attract

domestic companies and Information Technology

majors to expand operations mainly in the New

Town, Rajarhat and Sector V micromarkets. Rents

are likely to register a 3-5% dip in Sector V and

peripheral areas of New Town and Rajarhat as

property owners are likely to remain flexible on rents

to boost occupancy in their buildings.

India Office Property Market Overview October 2015

Office market absorption in India reached 30 million square feet year-to-date, an 11% increase over the previous year. Major cities like Bengaluru, Gurgaon and Mumbai are expected to see continued office space uptake in the coming quarter. Rents remained stable across most markets except some areas of Gurgaon, Bengaluru and Pune which saw declines. The report provides an overview of the office markets in key cities like Mumbai, Delhi, Gurgaon, NOIDA, Chennai, Bengaluru, Kolkata, Pune and includes statistics on absorption, vacancy, rents and major transactions.

Telecommunication in India

In this presentation I have explained about telecommunication in India.

topics covered are as under

Telecom Industry Overview

Major Players in Telecom Sector

Emerging Trends in Telecom Market

Growth Avenues

Role of Cost & Management Accountant in Telecom sector

Q & A session.

http://www.airtel3gplans.com/airtel-3g-plans/all-airtel-3g-plans-details/

Technology Smart City Opportunity - India

With a new governmental push towards building smart cities in India, there lies a huge technological and business opportunity. The report takes a detailed look at these.

Mumbai Real Estate Outlook Report H1 2015

This is our third edition of the flagship half yearly report - India Real Estate.

It presents a comprehensive analysis of the residential and office market performance of the Mumbai Metropolitan Region for the period between January–June 2015 (H1 2015).

Mumbai Real Estate Outlook January - June 2014

- Housing launches in Mumbai declined 38% in the first half of 2014 compared to the same period in the previous year, while housing absorption declined 25%. However, launches and absorption are forecast to increase 10% and 49% respectively in the second half of 2014.

- The demand-supply gap has led to a large inventory of over 213,000 unsold housing units. The time taken to liquidate this inventory has more than doubled from 5 quarters to 12 quarters over the last two years.

- Peripheral areas like Central Suburbs and Western Suburbs continue to be the largest markets, though their share of new launches has declined. The unsold inventory is highest in the expensive South Mumbai market, though it accounts

decompositionExample of classical decompositionMovingCenteredRawQu.docx

decompositionExample of classical decompositionMovingCenteredRawQuarterSales(Y)AverageAverageIndices15021003707576.250.918032786948077.580156082.586.250.6956521739612090901.3333333333710090951.0526315789880100

Input DataForecasting : Decomposition of the Trend and SeasonalitySeasonalYear 1Year 2Year 3Year 4IndexThis Moving Average isQ10.880.840.900.87Centered Between Quarters 2 and 3.Q20.890.880.960.91The next one is centered between 3 and 4,Q30.971.031.011.00and so on.Q41.251.221.171.214.0MovingCenteredRawSeasonalDe-seasPredicted(Y - Y-hat)=(25+28+35+50 ) /4 = 34.5yearQuarterSales (Y)AverageAverageIndicesIndexSales (Yd)Sales (Y-hat)Error11250.870737265728.7118.196.8=(28+35+50+39 ) /4 = 38.012280.908779919730.8124.493.5133534.5036.250.970.999780524435.0132.992.0145038.0040.001.251.214099355641.1847.422.6=(34.50+ 38.0 ) /2 = 36.25253942.0044.500.880.870737265744.7939.28-0.3264447.0049.500.890.908779919748.4246.49-2.5275552.0053.631.030.999780524455.0157.20-2.2= 35 / 36.25 = 0.97287055.2557.251.221.214099355657.6676.81-6.8395259.2562.000.840.870737265759.7260.36-8.43106064.7568.500.880.908779919766.0268.50-8.53117772.2576.381.010.999780524477.0281.41-4.431210080.5085.501.171.214099355682.37106.21-6.24138590.5094.750.900.870737265797.6281.443.641410099.00104.000.960.9087799197110.0490.509.5415111109.000.9997805244111.02105.625.44161401.2140993556115.31135.614.4-0.1BIASCalculated on output pageand copied here.

Input Data

Sales (Y)

Quarter

$ Million

Sales

Output

Sales (Yd)

Quarter

$ Million

Deseasonlized Sales

Sheet3SUMMARY OUTPUTRegression StatisticsMultiple R0.9797R Square0.9598Adjusted R Square0.9569Standard Error6.1049Observations16ANOVAdfSSMSFSignificance FRegression112457.95912457.959334.2670.000Residual14521.77437.270Total1512979.733CoefficientsStandard Errort StatP-valueLower 95%Upper 95%Lower 95.0%Upper 95.0%Intercept14.84193.20144.63600.00047.975521.70837.975521.7083Quarter6.05320.331118.28300.00005.34316.76335.34316.7633Reseasonalize the predicted YdRESIDUAL OUTPUTValues to predict the true salesDeseasonalizedSeasonal(Multiply by the seasonal index)ObservationPredicted Sales (Yd Hat)ResidualsIndexPredicted Y120.89517.81620.87118.19226.94833.86230.90924.49333.00142.00621.00032.99439.05462.12821.21447.42545.1078-0.31820.87139.28651.1610-2.74440.90946.49757.2142-2.20211.00057.20863.2674-5.61151.21476.81969.3206-9.60100.87160.361075.3737-9.35120.90968.501181.4269-4.41001.00081.411287.4801-5.11451.214106.211393.53334.08510.87181.441499.586510.45120.90990.5015105.63975.38471.000105.6216111.69283.61901.214135.61

Perform regression with desasonalized sales to get the underlying trend (Output Sheet)

1

2

3

4

5

6

7

1Rent RollUnit TypeUnit DescriptionNumber of UnitsArea Per Unit (sqft)Monthly Rent/UnitTotal Area (sqft)Monthly Gross Rent/sqftMonthly Gross RentAnnual Gross RentA-11 BR/1BA726887501.0A-21 BR/1.5 BAA-2A1 BR/1 BATotal

2Additional Revenue Sources# of UnitsMonthly Rent/UnitTotal Monthly RentTotal Annual RentGarages2.1Direct AccessAss.

Country Club of Louisiana Baton Rouge Home Sales Q3 2011 vs Q3 2014

Country Club of Louisiana Baton Rouge Home Sales Q3 2011 vs Q3 2014

Country Club of Louisiana Pinterest Board Photos:

http://www.pinterest.com/billdcobb/country-club-of-louisiana-baton-rouge/

Published by Bill Cobb, Greater Baton Rouge's Home Appraiser

225-293-1500

homeappraisalsbatonrouge.com

Based on information from Greater Baton Rouge Association of REALTORS®\MLS for period 07/01/2011 to 09/30/2014, extracted on 10/22/2014.

Global Services Fact Sheet

Looking for an overview of the global services market? Look no further - this 6-page deck offers details on the business process services (BPS), IT services (ITS), and shared services/global in-house center (GIC) markets.

Real Time Gross Settlement

Real time gross settlement systems (RTGS) are specialist funds transfer systems where transfer of money or securities takes place from one bank to another on a "real time" and on "gross" basis. It can be defined as the continuous (real-time) settlement of funds transfers individually on an order by order basis (without netting).

Top investments destination in mumbai mmr jan-jun15

Mumbai property prices are amongst the highest in the country. Slow property sales and inflated pricing has led to buyers postponing their property buying decision considerably resulting in an inventory pile-up of 46 months. Find the detailed analysis for January - June 2015 period.

Results presentation 4Q15

TIM Brasil faced a challenging year in 2015 with slowing GDP growth, high inflation, and a deteriorating currency. However, through maintaining infrastructure investment and focusing on efficiency, TIM was able to defend its EBITDA performance. TIM also repositioned its marketing approach with a new portfolio focused on value, SIM card consolidation, and quality. This helped TIM reduce its dependency on community effects and focus on the evolving middle class segment. Key highlights included expanding 4G coverage leadership, growing data users and revenues, improving network quality, and executing an ongoing efficiency program.

Similar to Bangalore office rental insights april 2014 (20)

Larsen & Toubro Outthink - 2016, IIM Rohtak Final Round

Larsen & Toubro Outthink - 2016, IIM Rohtak Final Round

India Office Property Market Overview October 2015

India Office Property Market Overview October 2015

decompositionExample of classical decompositionMovingCenteredRawQu.docx

decompositionExample of classical decompositionMovingCenteredRawQu.docx

Country Club of Louisiana Baton Rouge Home Sales Q3 2011 vs Q3 2014

Country Club of Louisiana Baton Rouge Home Sales Q3 2011 vs Q3 2014

Top investments destination in mumbai mmr jan-jun15

Top investments destination in mumbai mmr jan-jun15

More from Surabhi Arora, MRICS

Colliers radar delhi gurgaon and noida the three aces_june 2018

The National Capital Region (NCR), is consistently the second largest office market with 20% share of the annual nationwide leasing volume over the past five years. In our opinion, the NCR should retain its dominance in office demand over the next five years. We expect Delhi to see a facelift with redevelopment projects over the coming years. The satellite city Gurugram should remain the preferred city among corporate occupiers against the backdrop of a business-friendly environment, healthy new supply and infrastructure improvements. NOIDA is likely to come out of its image of affordable technology hub and rise as an emerging commercial market. We advise new entrants to choose well- established micromarkets in Delhi and Gurugram while occupiers looking for affordability should start exploring NOIDA for their large requirements and backend operations. In our opinion, investors should keep the momentum upbeat taking cues from the infrastructure initiatives and optimistic business conditions in the region.

Colliers Radar | Special economic zones in india

The uncertainty regarding the continuity of fiscal incentives is an area of growing concern among various stakeholders in Special Economic Zones (SEZs). Although more than 40.0 million sq ft (3.8 million sq m) of new supply is scheduled for completion before the mandatory deadline of 2020 to qualify for income tax benefits in SEZs, it seems unlikely that all the projects will be completed by then. We advise first-time entrants to pre-commit spaces only in projects that are in advance stages of construction to avoid last-minute delays in starting operations which may lead to disqualification for direct tax benefits. Regardless of optimism among the stakeholders about a further extension of income tax benefits, until this is certain, developers should schedule the completion of construction three to six months in advance

Colliers radar india office trends to watch for in 2018

The commercial real estate market in India remained robust in 2017 despite economic disruptions. Office leasing volume was around 42.8 million sq ft excluding pre-commitments, marginally higher than 2016. Bengaluru accounted for the largest share of leasing at 36% followed by NCR at 18%. Demand is expected to be driven by the technology, engineering, manufacturing and finance sectors. Flexibility, collaboration, workspace efficiency and cost effectiveness will be key focus areas for corporate real estate heads in 2018. Flexible office spaces are expected to continue growing while pre-commitments of large office spaces and built-to-suit developments will remain popular strategies. Occupiers may also explore expanding to tier 2 and 3 cities to access cheaper

Colliers Radar- New growth centre in south Chennai_2020

Pallavaram - Thoraipakkam Road (PTR), the 11 km stretch located in the Old Mahabalipuram Road (OMR) Post-Toll market is gearing up to entice numerous multinational companies and small and medium enterprises to Chennai. Being strategically placed and well connected to the key office markets of the OMR and Grand Southern Trunk (GST) Road, this link road is likely to disrupt the linear growth pattern of the OMR. The PTR is now emerging as a strong new growth centre in the OMR district. Over the next three years, we expect 11.5 million sq ft (1.06 million sq m) of office space supply to see completion in Chennai. Of this total, 58% is concentrated along the PTR. We expect that by 2020 the improved infrastructure and new offices with modern amenities should greatly enhance the area’s appeal to prospective tenants. In our opinion, occupiers looking for expansion within Special Economic Zones (SEZs) should take advantage of huge upcoming supply in this corridor. For relocation and consolidation, occupiers can either pre-commit or opt for built-to-suit options in PTR to hedge against future rent rises.

Colliers Radar Report - Impact of Artificial Intelligence on Indian Real Estate

Artificial intelligence and automation have the potential to disrupt many industries including real estate. However, AI is expected to complement human roles rather than replace them, and drive productivity and value creation. The convergence of AI, the internet of things, and alternative workplace solutions such as activity-based and agile working will transform buildings and the workplace. Offices of the future are expected to be more efficient, collaborative, and healthier. Indian enterprises should embrace AI early on and invest in skills development, while developers should offer flexible workspaces and prepare for increasing automation. Overall, high rents and poor infrastructure pose greater risks to the Indian property market than AI.

Colliers radar india coworking space - the new kid on the block

India offers a great opportunity for coworking space operators to profit from rising demand for flexible, innovative and collaborative workspace designs. We estimate that more than 1.2 million sq ft were leased by coworking operators in India in 2016, which accounted for 3% of the overall leasing volume. Although it represents only a small share of the total leasing demand, coworking operators are planning to lease 8 to 9 million sq ft by 2020.

We foresee that the concentration of coworking spaces will intensify further in Bengaluru, Mumbai, and Gurugram thanks to the availability of adequate infrastructure and opportunities for start-ups in those cities. We recommend occupiers, especially small and medium enterprises, to consider use of flexible space for their office requirements in order to benefit from an integrated networking environment, greater cost-effectiveness and more innovative workspace design.

Colliers Quarterly Pune Q1 2017

With most of the new supply scheduled for

completion in 2018, vacancy in Pune market is likely

to remain tight in the short term. We cannot rule out

the possibility of further increase in rent as the

additional supply infusion may not meet the pent-up

demand of the last few quarters. In our opinion, the

market is likely to remain tilted in property owners'

favour for a while. In our view, developers should

expedite completion of projects under construction

and plan more new projects to profit from the

untapped demand in the market.

Colliers Quarterly Hyderabad Q1 2017

Amid surging office demand in this re-established IT

hub, most of the upcoming quality office spaces

have been pre-committed by occupiers, creating a

severe supply shortage. Hyderabad's average office

rent is likely to surge in 2017, as en-bloc

completions are still 12-15 months away. We advise

developers to expedite construction and undertake

new projects to meet the heightened occupier

demand to retain the city's image of an affordable

Information Technology and Information Technology

and enabled services (IT-ITeS) location.

Colliers Quarterly Gurgaon Q1 2017

Average rents in Gurgaon's office market are expected to remain stable in 2017. Demand is projected to strengthen from the technology and banking sectors. Significant new supply coming online will help keep prime area rents in check, while submarkets like Golf Course Extension Road may see a 2-5% correction. Demand was strong in Q1 2017 especially from IT/ITeS firms, though overall leasing volume declined slightly year-over-year. New completions were concentrated on Golf Course Extension Road, with more supply slated for delivery there and along NH8 by year-end. Vacancy rates may rise slightly due to new inventory, and occupiers are considering more affordable areas as well.

Colliers Quarterly-Chennai-Q1 2017

Due to limited availability of quality supply in

preferred micromarkets, peripheral areas of the city

are likely to grow in coming quarters. With

significant new supply scheduled for completion

along Pallavaram-Thoraipakkam Road by 2020, we

expect this corridor to become the next hotspot for

Information Technology and Information Technology

enabled Service (IT-ITeS) occupiers due to its

proximity to Old Mahabalipuram Road (OMR)-Pre

Toll area and Grand Southern Trunk (GST) Road. We

recommend big occupiers looking for large floor

plates in Special Economic Zones (SEZs) to consider

Chennai to benefit from the upcoming SEZ supply in

OMR-Post Toll micromarket.

India Office-Property-Market-Overview-Q1 2017

The latest report by Colliers Research titled ‘India Office Property Market Overview Q1 2017’ is now out and ready for download. Notwithstanding the demonetisation of high-value currency notes in November 2016, the economy recovered faster than expected and early projections suggest a growth of 7.1% in the fiscal year ending March 2017. All the key economic indicators suggest that India’s consumption based recovery is on track, and the economy is benefiting from an upswing in demand and output. Although five months on from demonetisation occupiers' markets across India's major cities have seen no discernible adverse impact, we expect demand to firm up driven by the strengthening economy. Gross office take-up in India amounted to 9.3 million sq ft (863,998 sq m) in Q1 2017. The Bengaluru (Bangalore) market maintained its top position across nine cities despite low vacancy and recorded an overwhelming share of 37% in total absorption. Mumbai and Delhi NCR followed with shares of 18% and 17% respectively in total absorption. Chennai, Pune, Hyderabad and Kolkata accounted for 11%, 9%, 6% and 2% respectively in the overall leasing volume.

Coworking space: The New Kid on the Block

The latest radar report by Colliers Research titled "Coworking space: The New Kid on the Block" is out and ready for download. India offers a great opportunity for coworking space operators to profit from rising demand for flexible, innovative and collaborative workspace designs. We estimate that more than 1.2 million sq ft was leased by major coworking operators in India in 2016, which accounted for 3% of the overall leasing volume. Although it represents only a small share of the total leasing demand, coworking operators are planning to lease 8 to 9 million sq ft by 2020.

Mumbai Office Property Market Overview Jan 2017

Although rents are likely to remain stable across

most micromarkets, we believe availability of Grade

A buildings at affordable rent will remain a concern

for the next several years. Thus instead of focusing

purely on spatial requirements, companies should

consider taking advantage of flexible office spaces

and formulate a forward-looking workplace strategy.

Gurgaon Office Property Market Overview Jan 2017

Tenant appetite for higher quality offices has been

reflected in new leases being executed at abovemarket

rates in select Grade A buildings. We expect

a similar trend in 2017. Due to a dearth of quality

office space in other technology-driven markets like

Pune and Bengaluru, we may see supply-led demand

in coming quarters resulting in increased absorption

volumes.

Delhi Office Property Market Overview Jan 2017

Leasing remained healthy in 2016 despite the flight

of cost-conscious tenants to Delhi's satellite cities.

Demand continued to be driven by the financial

services and manufacturing companies. We expect

0.3 million sq ft (27,870 sq meters) of Grade A office

supply to be delivered in Q1 2017 mainly in the CBD.

We expect a correction in rents especially in grade B

buildings due to tenants' preference for premium

buildings.

Pune Office Property Market Overview Jan 2017

Demand-supply gap is likely to remain a concern in

coming quarters. While a few grade A office

buildings are likely to see completion towards the

end of 2017, we expect upward pressure on rents at

least in H1 2017. Tenants looking for quality assets

should find their options limited this year given that

most of the new supply is likely to enjoy high precommitment

rates from existing occupiers.

India Office Property Market Overview_Jan 2017

The latest report by Colliers Research titled "India Office Property Market Overview - Trends to watch for in 2017" is now out and ready for download. India recorded 41.6 million sq ft (3.9 million sq metres) of gross office leasing transactions in 2016. With a modest increase of 3.5% over 2015, the data indicates a robust occupier market. Bengaluru (Bangalore) remained on a high growth trajectory and maintained its leading status among the key cities by retaining a 31% share followed by Delhi-NCR, which represented 18% of the total occupier demand. Despite the fact that many forecasters have revised down their 2017 estimates for India’s GDP to 6.8-7.0% due to short-term adverse repercussions of demonetization, we believe the outlook for the office sector remains positive in 2017. In our view, the policy changes that the government is implementing should help improve business confidence in India resulting in robust office leasing demand in coming years. We predict an average annual rental growth of 4.6% in 2017. Firm demand should absorb new supply in technology-driven markets, keeping vacancy low.

Gurgaon office market overview jan 2015

Gurgaon remained the most active office market in NCR in 2014, accounting for 67% of absorption. However, absorption declined 13% YoY to 4.73 million sq ft due to cautious market sentiments. IT/ITeS was the largest demand driver, increasing its share of absorption to 62%. New supply also declined, dropping to 3.2 million sq ft in 2014 from 4.53 million sq ft in 2013 as developers focused on completing existing projects. Office rents increased 6% on average across micro-markets such as NH8, Golf Course Extension Road, and Sohna Road. Gurgaon is expected to remain the preferred office destination in NCR, with leasing dominated by large IT/IT

India office-trends-to-watch-for-in-2015

1. Office absorption in Mumbai picked up towards the end of 2014, though total absorption of 3.12 million sq ft was still 44% lower than 2013.

2. BFSI continued to be the dominant sector in Mumbai, occupying 39% of office space, while Western suburbs remained the most preferred location.

3. Vacancy levels fell to 14% in 2014 from 14.5% in 2013, despite limited new supply of 3.3 million sq ft added during the year. Rents witnessed a 4% annual increase due to low vacancy.

4. The outlook for 2015 is positive with demand expected to rise in the first half of the year, while new supply entering the market in the second half will

India Residential Property Market Overview May 2014

HIGHLIGHTS

• Restricted sales transactions were observed in major cities like Mumbai, Delhi, Gurgaon and NOIDA during 1Q 2014. However, an increase in the number of enquiries for residential properties has been seen across the markets.

• Chennai, Bengaluru and Pune markets remained active and witnessed ample new project launches.

• Capital values remain stable in most cities. However select micro markets with inherent demand witnessed increases in the range of 2 - 5% Q-o-Q.

• With the new Government in place and business confidence gaining momentum, we anticipate an increase in residential sales in the coming quarter.

More from Surabhi Arora, MRICS (20)

Colliers radar delhi gurgaon and noida the three aces_june 2018

Colliers radar delhi gurgaon and noida the three aces_june 2018

Colliers radar india office trends to watch for in 2018

Colliers radar india office trends to watch for in 2018

Colliers Radar- New growth centre in south Chennai_2020

Colliers Radar- New growth centre in south Chennai_2020

Colliers Radar Report - Impact of Artificial Intelligence on Indian Real Estate

Colliers Radar Report - Impact of Artificial Intelligence on Indian Real Estate

Colliers radar india coworking space - the new kid on the block

Colliers radar india coworking space - the new kid on the block

India Residential Property Market Overview May 2014

India Residential Property Market Overview May 2014

Recently uploaded

BEST FARMLAND FOR SALE | FARM PLOTS NEAR BANGALORE | KANAKAPURA | CHICKKABALP...

BEST FARMLAND FOR SALE | FARM PLOTS NEAR BANGALORE | KANAKAPURA | CHICKKABALP...knox groups real estate

welcome to knox groups real estate company in Bangalore. best farm land for sale near Bangalore and madhugiri . Managed farmland near Kanakapura and Chickkabalapur get know more details about the projects .Knox groups is a leading real estate company dedicated to helping individuals and businesses navigate the dynamic real estate market. With our extensive knowledge, experience, and commitment to excellence, we deliver exceptional results for our clients. Discover the perfect foundation for your agricultural aspirations with KNOX Groups' prime farm lands. These aren't just plots; they're the fertile grounds where vibrant crops flourish, livestock thrives, and unique agricultural ventures come to life. At KNOX, we go beyond selling land we curate sustainable ecosystems, ensuring that your journey toward agricultural success is seamless and prosperous.Kumar Codename Fireworks at Hadapsar Link Road, Pune - PDF.pdf

Codename Fireworks developed by Kumar Properties is a new residential development that offers 2/3 BHK premium residences with easy access to proposed ring road, airport, metro station.

For More Details:

Visit Here: kumar.developerprojects.com

SVN Live 6.17.24 Weekly Property Broadcast

The SVN® organization shares a portion of their new weekly listings via their SVN Live® Weekly Property Broadcast. Visit https://svn.com/svn-live/ if you would like to attend our weekly call, which we open up to the brokerage community.

Living in an UBER World - June '24 Sales Meeting

June 2024 Lancaster County Sales Meeting for Berkshire Hathaway HomeServices Homesale Realty covering the following topics: 1. VA Suspends Buyer Agent Payment Plan (article), 2. Frequently Used Terms in title, 3. Zillow Showcase Overview, 4. QuickBuy commission promotion, 5. Documenting Cooperative Compensation, 6. NAR's Code of Ethics - Mass Media Solicitations, 7. Is it really cheaper to rent? 8. Do's and Don't's when Terminating the Agreement of Sale, 9. Living in an UBER World

Anilesh Ahuja Pioneering a Paradigm Shift in Real Estate Success.pptx

Anilesh Ahuja journey is a testament to the power of vision, resilience, and unwavering determination. As a visionary leader, he continues to inspire and empower others to dream big and challenge the status quo. His legacy extends far beyond the realm of real estate, leaving an indelible mark on the industry and the world at large.

Stark Builders: Where Quality Meets Craftsmanship!

At Stark Builders our vision is to redefine the renovation experience by combining both stunning design and high quality construction skills. We believe that by delivering both these key aspects together we are able to achieve incredible results for our clients and ensure every project reflects their vision and enhances their lifestyle.

Although we are not all related by blood we have created a team of highly professional and hardworking individuals who share the common goal of delivering beautiful and functional renovated spaces. Our tight nit team are able to work together in a way where we pour our passion into each and every project as we have a love for what we do. Building is our life.

原版制作(Greenwich毕业证书)格林威治大学毕业证PDF成绩单一模一样

学校原件一模一样【微信:741003700 】《(Greenwich毕业证书)格林威治大学毕业证PDF成绩单》【微信:741003700 】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

【主营项目】

一.毕业证【q微741003700】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【q/微741003700】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

AVRUPA KONUTLARI ESENTEPE - ENGLISH - Listing Turkey

Looking for a new home in Istanbul? Look no further than Avrupa Konutlari Esentepe! Our beautifully designed homes provide the perfect blend of luxury and comfort, making them the perfect choice for anyone looking for a high-quality home in the city.

With a wide range of apartment types available, from 1+1 to 4+1, we have something to suit every need and budget. Each apartment is designed with attention to detail and features spacious and bright living areas, making them the perfect place to relax and unwind after a long day.

One of the things that sets Avrupa Konutlari Esentepe apart from other developments is our focus on creating a community that is both comfortable and convenient. Our homes are surrounded by lush green spaces, perfect for enjoying a peaceful stroll or having a picnic with friends and family. Additionally, our complex includes a variety of social and recreational amenities, such as swimming pools, sports fields, and playgrounds, making it easy for residents to stay active and socialize with their neighbors.

https://listingturkey.com/property/avrupa-konutlari-esentepe/

Deed 3754 S Honeysuckle Mesa AZ 85212 owner Shawn Freeman - Pamela Brown Nota...

Shawn Tyler Freeman Mesa Arizona - Lawsuit Exhibit - 3754 S Honeysuckle Mesa AZ 85212 - Pamela Brown Notary Arizona

Recently uploaded (9)

BEST FARMLAND FOR SALE | FARM PLOTS NEAR BANGALORE | KANAKAPURA | CHICKKABALP...

BEST FARMLAND FOR SALE | FARM PLOTS NEAR BANGALORE | KANAKAPURA | CHICKKABALP...

Kumar Codename Fireworks at Hadapsar Link Road, Pune - PDF.pdf

Kumar Codename Fireworks at Hadapsar Link Road, Pune - PDF.pdf

Anilesh Ahuja Pioneering a Paradigm Shift in Real Estate Success.pptx

Anilesh Ahuja Pioneering a Paradigm Shift in Real Estate Success.pptx

Stark Builders: Where Quality Meets Craftsmanship!

Stark Builders: Where Quality Meets Craftsmanship!

AVRUPA KONUTLARI ESENTEPE - ENGLISH - Listing Turkey

AVRUPA KONUTLARI ESENTEPE - ENGLISH - Listing Turkey

Deed 3754 S Honeysuckle Mesa AZ 85212 owner Shawn Freeman - Pamela Brown Nota...

Deed 3754 S Honeysuckle Mesa AZ 85212 owner Shawn Freeman - Pamela Brown Nota...

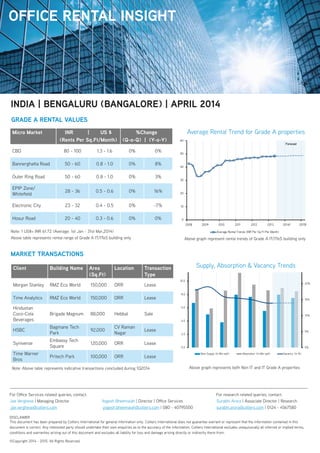

Bangalore office rental insights april 2014

- 1. Micro Market INR | US $ (Rents Per Sq.Ft/Month) %Change (Q-o-Q) | (Y-o-Y) CBD 80 - 100 1.3 - 1.6 0% 0% Bannerghatta Road 50 - 60 0.8 - 1.0 0% 8% Outer Ring Road 50 - 60 0.8 - 1.0 0% 3% EPIP Zone/ 28 - 36 0.5 - 0.6 0% 16% Electronic City 23 - 32 0.4 - 0.5 0% -7% Hosur Road 20 - 40 0.3 - 0.6 0% 0% Client Building Name Area (Sq.Ft) Location Transaction Type Morgan Stanley RMZ Eco World 150,000 ORR Lease Time Analytics RMZ Eco World 150,000 ORR Lease Hindustan Coco-Cola Beverages Brigade Magnum 88,000 Hebbal Sale HSBC Bagmane Tech Park 92,000 CV Raman Nagar Lease Syniverse Embassy Tech Square 120,000 ORR Lease Time Warner Bros Pritech Park 100,000 ORR Lease OFFICE RENTAL INSIGHT GRADE A RENTAL VALUES Average Rental Trend for Grade A properties Supply, Absorption & Vacancy Trends For research related queries, contact: Joe Verghese | Managing Director Yogesh Bheemaiah Surabhi Arora | Associate Director | Research joe.verghese@colliers.com yogesh.bheemaiah@colliers.com | 080 - 40795500 surabhi.arora@colliers.com | 0124 - 4567580 DISCLAIMER This document has been prepared by Colliers International for general information only. Colliers International does not guarantee warrant or represent that the information contained in this document is correct. Any interested party should undertake their own enquiries as to the accuracy of the information. Colliers International excludes unequivocally all inferred or implied terms, conditions and warranties arising out of this document and excludes all liability for loss and damage arising directly or indirectly there-from. INDIA | BENGALURU (BANGALORE) | APRIL 2014 MARKET TRANSACTIONS Note: 1 US$= INR 61.72 (Average: 1st Jan - 31st Mar,2014) Above graph represents both Non IT and IT Grade A properties ©Copyright 2014 - 2015. All Rights Reserved. 0% 5% 10% 15% 20% 25% 0.0 2.0 4.0 6.0 8.0 10.0 12.0 New Supply (In Mln sqft) Absorption (In Mln sqft) Vacancy (In %) 2008 2009 2010 2011 2012 2013 2014F 2015F 0 10 20 30 40 50 60 2008 2009 2010 2011 2012 2013 2014F 2015F Average Rental Trends (INR Per Sq Ft Per Month) Forecast Note: Above table represents indicative transactions concluded during 1Q2014 Above table represents rental range of Grade A IT/ITeS building only Above graph represent rental trends of Grade A IT/ITeS building only