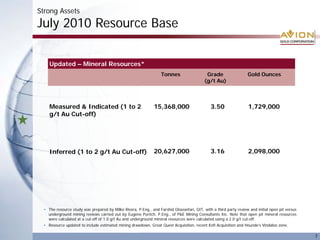

Avion Gold Inc. is a gold producer in Mali with plans to increase production from 75,000 ounces in 2010 to 200,000 ounces by 2012. The company acquired additional gold assets in 2010 that increased its total resource base to over 3.9 million ounces. Avion is significantly undervalued compared to its peers based on cash flow and net asset value multiples. Management intends to continue growing production and resources through exploration and development of its large land package.