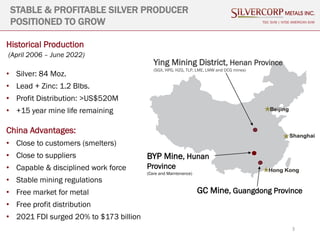

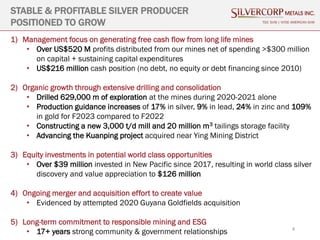

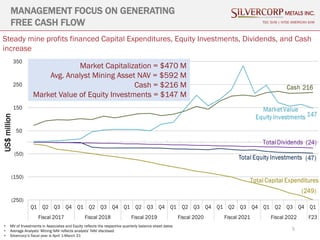

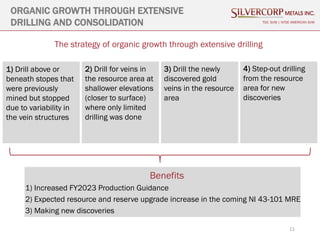

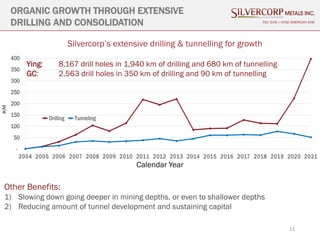

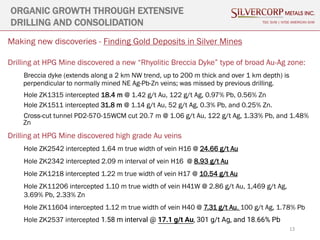

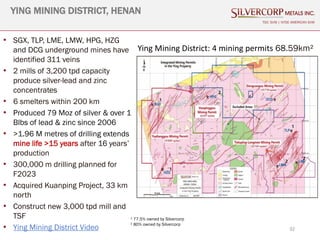

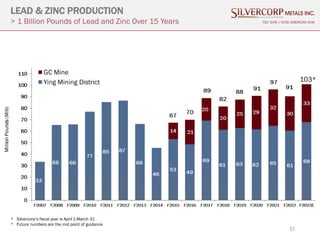

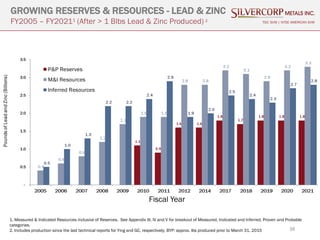

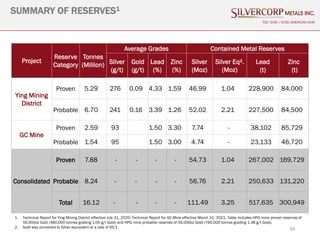

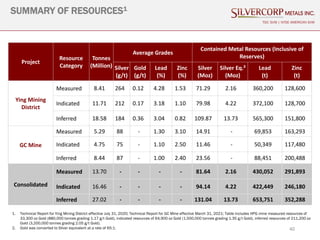

Silvercorp is a stable and profitable silver producer positioned for growth. It has a 15+ year mine life remaining at its operations in China. Through extensive drilling and consolidation efforts, Silvercorp is pursuing organic growth which has led to increased reserves and resources as well as new discoveries. This includes discovering gold deposits at its silver mines. Silvercorp also focuses on generating free cash flow which it uses to reinvest in its business, make equity investments, pay dividends, and increase its cash position.