Asset Managers and ESG

•

2 likes•187 views

This document summarizes the results of a survey conducted by Callan Institute regarding asset managers' approaches to environmental, social, and governance (ESG) investing. The survey found that larger asset management firms are more likely to have formal ESG policies and sign the UN Principles for Responsible Investment. Over half of firms surveyed do not have an ESG policy, but interest is growing. Larger firms see greater opportunities in ESG strategies and expect increasing client demand from the US, Canada, and Europe.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to Asset Managers and ESG

Similar to Asset Managers and ESG (20)

More from Callan

More from Callan (17)

Recently uploaded

Recently uploaded (20)

Asset Managers and ESG

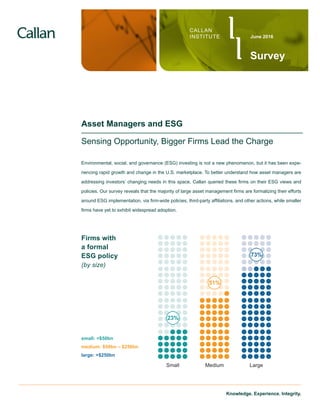

- 1. Knowledge. Experience. Integrity. CALLAN INSTITUTE Survey June 2016 Asset Managers and ESG Sensing Opportunity, Bigger Firms Lead the Charge Environmental, social, and governance (ESG) investing is not a new phenomenon, but it has been expe- riencing rapid growth and change in the U.S. marketplace. To better understand how asset managers are addressing investors’ changing needs in this space, Callan queried these firms on their ESG views and policies. Our survey reveals that the majority of large asset management firms are formalizing their efforts around ESG implementation, via firm-wide policies, third-party affiliations, and other actions, while smaller firms have yet to exhibit widespread adoption. Small 23% Medium 51% Large 73% Firms with a formal ESG policy (by size) small: <$50bn medium: $50bn – $250bn large: >$250bn

- 2. 2 Part of being a sound fiduciary was another popular reason for adopting ESG with 56% 26% of those not adopting ESG feel ESG factors are already accounted for in their current investment process 41%of all respondents have a formal ESG policy Has your firm signed the Principles for Responsible Investment (PRI)? 40% Yes 53% No 7% Not Sure Results reflect responses from 180 asset management firms representing more than $42 trillion in assets under management (AUM). While more than half of asset management firms (56%) do not have a formal ESG policy, and a similar percentage (53%) have not signed on to the United Nations Principles for Responsible Investment (PRI), the firms that have pursued these initiatives cite growing client demand as the primary motivation. For this survey we examined managers by size groups: small (less than $50 billion), medium ($50 - $250 billion), and large (greater than $250 billion). A greater proportion of large firms (73%) versus small firms (23%) have a formal ESG policy at the firm level (as opposed to on a strategy level). The same trend is true for PRI signatories: 82% of large firms versus 20% of small firms. Further, larger firms tend to be more established in the space: more than one-quarter (27%) of large firms created their ESG policy more than a decade ago, compared to 21% of medium firms and 16% of small firms. 59% cite client demand as their reason for adopting ESG 16% Small 62% 22% 27% Large 36% 21% Medium 42% 37% 37% When was your firm’s ESG policy established? Within past 2 years 3–10 years ago > 10 years ago 35% of firms with no ESG policy have considered adopting one within the last year Note: Multiple responses allowed.

- 3. 3Knowledge. Experience. Integrity. What research process is utilized at your firm? Managers with an ESG Policy by Research Process Quantitative, factor/model driven approach Combination of fundamental & quantitative Fundamental, bottom-up research* * this includes basic screening 10% 31% 59% QuantitativeComboFundamental 53% 51% 33% How is research organized within your firm? Multiple boutique model Central research platform Team-based approach Managers with an ESG Policy by Research Organization 11% 60% Multiple boutique Central Team-based59% 45% 36% 29% We also posed questions around research processes and discovered that firms with fundamental, bottom-up research are less likely to have a formal ESG policy (33%) than those with a quantitative approach (53%) or that use a combination of research processes. Research organization also mattered. Asset management firms that implement a multiple boutique model are more likely to have a formal ESG policy (59%) than those with centrally organized research (45%) or team- based approaches (36%). Respondent Perspective “We believe that responsible investing is a core component of traditional investing. Governed, sustainable businesses have the potential to generate strong results over time.”

- 4. 4 41% of respondents say ESG strategies present a market opportunity going forward Looking forward, all sizes of asset management firms expect client interest in ESG investing will grow. However, just 41% of the respondents see this marketplace shift as an opportunity. Again, larger firms tend to be more optimistic about future growth, with nearly 100% sensing slight or significant increases in client interest. Asset managers that project growth in client interest expect to see that interest coming from the U.S. and Canada (72%) and Europe (57%). This reflects the survey respondent population, who are primarily based in the U.S. and Europe, but may also reflect the notion that European investors are further along in integrating ESG into investment decision making than their North American counterparts. Over the next 3-5 years, how do you expect client interest in ESG to change? Where is this increased interest likely to come from?* Increase Slightly Increase Significantly Small Medium Large U.S. and Canada Europe Asia Emerging Australia 72% 57% 16% 5% 4% 100% 88% 76% * Multiple responses allowed. Around one-third of managers with a formal ESG policy expect it will help them achieve higher risk-adjusted returns and improved risk profiles over the long term Respondent Perspective “We believe that environmental, social and governance (“ESG”) issues play an important role in the global economy, both from a business and investment perspective.” “Incorporating ESG factors into the research process is part of ensuring all risks and opportunities that could influence the growth potential of the company in question have been considered.”

- 5. 5Knowledge. Experience. Integrity. Size matters larger asset management firms are taking more actions on ESG 96% of respondents are active managers Respondents by Size How many unique strategies does your firm manage? We provide further detail on the demographics of respondent firms for reference. Rough- ly half of the 180 asset management firms that responded to our survey are small (less than $50 billion in assets), and around a quarter are either medium ($50 – $250 billion) or large (greater than $250 billion). Respondent firms had a median of $56 billion and an average of $232 billion in AUM. The vast majority of respondent firms actively manage their strategies (96%). As one would expect, the smaller respondent firms manage fewer unique strategies. Key Takeaways For asset management firms, it’s clear that size matters when it comes to ESG in- tegration. Large firms are more likely than smaller firms to have formal, firm-wide ESG policies, be PRI signatories, and have significant expectations of growing client interest in the space. Small <$50bn 53% Medium $50bn – $250bn 25% Large >$250bn 22% 0 - 5 6 - 10 11 - 25 Over 25 Small Medium Large 100% 65% 30% 8% 37% 29% 26% 5%

- 6. 6 Certain information herein has been compiled by Callan and is based on information provided by a variety of sources believed to be reliable for which Callan has not necessarily verified the accuracy or completeness of or updated. This report is for informational pur- poses only and should not be construed as legal or tax advice on any matter. Any investment decision you make on the basis of this report is your sole responsibility. You should consult with legal and tax advisers before applying any of this information to your particular situation. Reference in this report to any product, service or entity should not be construed as a recommendation, approval, affiliation or endorsement of such product, service or entity by Callan. Past performance is no guarantee of future results. This report may consist of statements of opinion, which are made as of the date they are expressed and are not statements of fact. The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to subsidiaries or parents, or post on internal web sites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business. If you have any questions or comments, please email institute@callan.com. About Callan Associates Callan was founded as an employee-owned investment consulting firm in 1973. Ever since, we have empowered institutional clients with creative, customized investment solutions that are uniquely backed by proprietary research, exclusive data, ongoing education and decision support. Today, Callan advises on more than $2 trillion in total assets, which makes us among the largest independently owned invest- ment consulting firms in the U.S. We use a client-focused consulting model to serve public and private pension plan sponsors, endowments, foundations, operating funds, smaller investment consulting firms, investment managers, and financial intermediaries. For more information, please visit www.callan.com. About the Callan Institute The Callan Institute, established in 1980, is a source of continuing education for those in the institu- tional investment community. The Institute conducts conferences and workshops and provides pub- lished research, surveys, and newsletters. The Institute strives to present the most timely and relevant research and education available so our clients and our associates stay abreast of important trends in the investments industry. © 2016 Callan Associates Inc. About The Author Mark R. Wood, CFA, is a Vice President and U.S. equity investment consultant in Callan’s Global Manager Research group. Mark is responsible for research and analysis of U.S. equity investment managers and assists plan sponsor clients with U.S. equity manager searches. He meets regularly with investment managers to develop an understanding of their strategies, products, investment policies, and organizational structures. As a member of Callan’s ESG Committee, Mark covers matters related to sustainable investing. Mark joined Callan in 2013. Prior to joining the Global Manager Research group, Mark worked as the Senior Research Analyst for Cook Street Consulting, Inc., a boutique consulting firm based in Denver, CO. He was responsible for investment manager searches and due diligence for U.S. equity, fixed income, and target date asset classes. Mark graduated from the University of Colorado, Boulder in 2007 with a BS in Finance and Business Administration. He has earned the right to use the Chartered Financial Analyst designation.

- 7. Corporate Headquarters Callan Associates 600 Montgomery Street Suite 800 San Francisco, CA 94111 800.227.3288 415.974.5060 www.callan.com Regional Offices Atlanta 800.522.9782 Chicago 800.999.3536 Denver 855.864.3377 New Jersey 800.274.5878