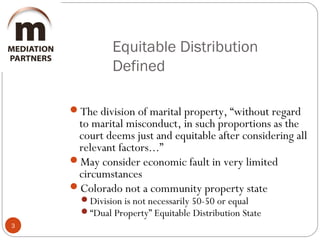

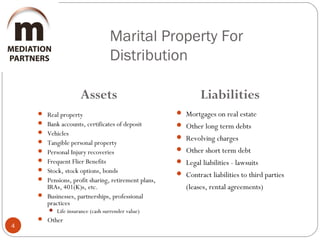

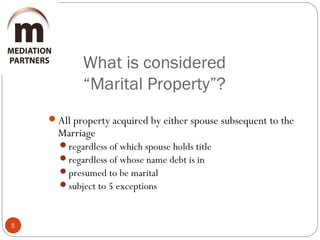

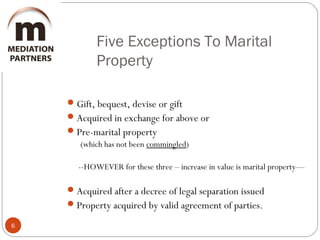

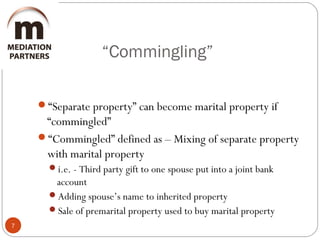

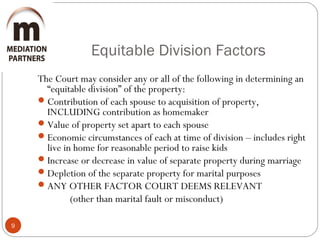

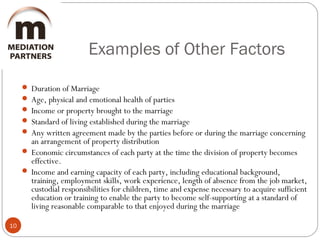

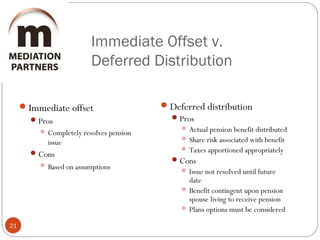

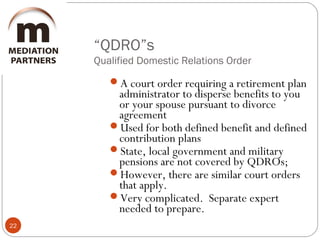

This document discusses division of property and debts in divorce cases. It defines equitable distribution as the division of marital property without regard to fault. Marital property subject to distribution includes real estate, vehicles, bank accounts, businesses, pensions, and other assets acquired during the marriage. Exceptions include gifts, inheritances, and pre-marital property not commingled. The court considers factors like contribution, duration of marriage, health, and standard of living in making an equitable division. Valuation of assets may require appraisals. Pensions are usually marital property divided either through immediate offset or deferred distribution using a Qualified Domestic Relations Order.