Downloaded 37 times

![28 29

THE ASIA VIDEO INDUSTRY REPORT 2023

Certain types of “service provider[s]” –

which now covers intermediary service,

caching service, hosting service and

information location tools service – are

presumed to be exempt from liability if 2

conditions are satisfied:

a. An explicit announcement and actual

compliance of service-terminating

measures have been made; and

b. Compliance with the statutory

conditions provided for each type of

service provider.

For hosting service and information

location tools services, the amended

Copyright Act introduces a new notice and

take down procedure allowing copyright

owners to issue a copyright infringement

notice to such service providers and

counter-claims against such notice.

6.

CHINA

China’s Third Amendment of Copyright

Law ("Third Amendment"), effective

since 1 June 2021, is a major reform in

response to the increasing number of

copyright infringement lawsuits in China,

including cases of digital piracy.

Some key highlights below:

• In response to previous criticisms

relating to the assessment of damages,

new legislation has increased the

amount of statutory damages payable

within the range of CNY 500 (USD 77)

to CNY 5 million (around USD 770,000)

and introduced punitive damages

consistent with its trade marks and

patent laws. Where appropriate,

punitive damages of up to 5 times the

determined damages may be awarded.

• Copyright authorities can also impose

fines on infringers proportionate to

the illegal business turnover; conduct

investigations; and seize suspected

infringing articles.

7.

HONG KONG

The Hong Kong Copyright (Amendment)

Bill 2022 has been gazetted. If

enacted, it will introduce an exclusive

technology-neutral communication

right for copyright owners and criminal

sanctions against infringement relating to

the new communication right.It also will

introduce two additional statutory factors

for the court to consider when assessing

whether to award additional damages to

copyright owners in civil cases involving

copyright infringements that will to help

deter infringement.

The Bill also introduces “safe harbour”

provisions for online service providers

to protect their activities and incentivise

them to cooperate with copyright owners

in combatting online piracy.

by Andy Leck

Head of the Intellectual Property and

Technology Practice Group in Singapore, Baker McKenzie

We at Baker McKenzie appreciate the challenges of staying innovative and profitable in an

increasingly regulated global landscape. Working across borders, our Media and Entertainment

practice brings together intellectual property and technology specialists to advise on a wide

range of complex cross-border matters to help clients keep the show on the road. We advise on

all aspects of intellectual property in the media and entertainment space, including development

agreements, brand strategy, designs and complex copyright questions associated with moral

rights, content production, distribution and transactions.

COMMENTARY

The rapid development of copyright laws

across the region recognises the need for

better and smarter regulations to guard

against the misappropriation of content

by bad actors.

While the industry cannot solely depend

on existing laws and regulations to catch

up with rapidly evolving technology,

the increased amount of effective

site-blocking in a number of countries

and updated copyright laws across the

region show a greater awareness of these

issues among governments. For example,

YouGov surveys in Malaysia show that

consumers move away from piracy when

faced with site-blocking pages. Indonesia

too, has seen a downward trajectory of

streaming piracy since the introduction of

its site-blocking regime.

Nonetheless, as technology continues

to march forward and more content

continues to be pirated before it is even

released, an effective strategy to reduce

theft and combat piracy in APAC can

only be achieved through consistent

enforcement, disruption and consumer

education and outreach.

PIRACY

IN

ASIA](https://image.slidesharecdn.com/asia-video-industry-report-2023-230102044026-b645e604/85/Asia-Video-Industry-Report-2023-pdf-15-320.jpg)

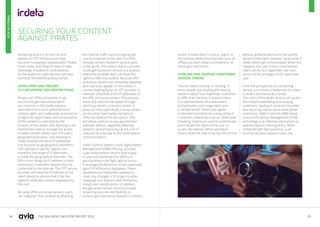

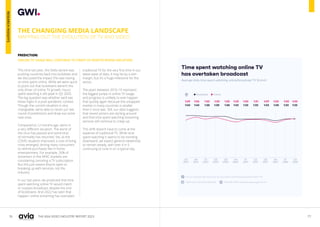

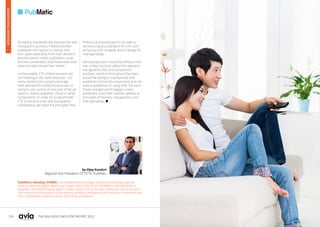

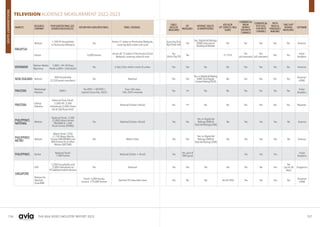

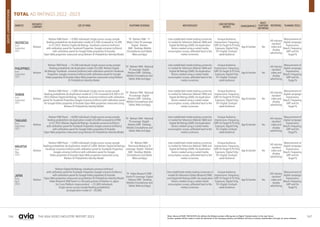

![160 161

THE ASIA VIDEO INDUSTRY REPORT 2023

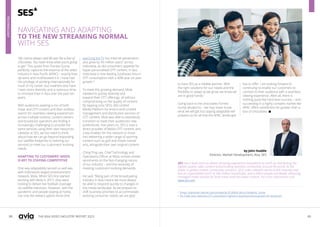

SYNDICATED MEDIA SURVEYS 2022-2023

MARKETS

RESEARCH

COMPANY

SURVEY SAMPLE SIZE PANEL COVERAGE METHODOLOGY DEMOGRAPHICS

CAB/SAT

MEASURED

DTT SOFTWARE

REACH &

FREQUENCY

HONG KONG Nielsen Media Index 6,000+ All area Face-to-Face/Online 12 - 64 Yes Yes Clear Decisions Yes

AUSTRALIA Nielsen Consumer & Media View 30,000 National Online 14+ Yes Yes Clear Decisions No

NEW ZEALAND Nielsen

Consumer & Media

Insights

10,000 National

Recruited: CATI/Online

All survey completed Online

15+ Fused withTAM data Fused withTAM data Clear Decisions Yes

INDONESIA11 cities Nielsen Consumer & Media View 17,000 Indonesia,11 cities

Face-to-face/Phone interview

(during COVID-19)/Online Survey

10+ Yes Yes Clear Decisions Yes

MALAYSIAPeninsular only Nielsen Consumer & Media View 10,000 Peninsular Malaysia Only

Face-to-face or

CATI (Rural)/Online (Urban)

15+ Fused withTAM data Fused withTAM data Clear Decisions Yes

MALAYSIAEast Malaysia Nielsen Consumer & Media View 2,000

East Malaysia [Kota Kinabalu

(Sabah) & Kuching (Sarawak)]

Face-to-face 15+ Yes Yes Clear Decisions Yes

MYANMAR Nielsen Media

Myanmar

Consumer & Media View 5,300+ National CAPI/ CATI 10 - 64 Yes Yes Clear Decisions No

PHILIPPINES National Urban Nielsen Consumer & Media View 10,000 National Urban CATI-CAWI/Face-to-Face CAPI 10+ Yes Yes Clear Decisions Yes

SINGAPORE Nielsen Consumer & Media View 4,200+ National Face-to-face/Online/ CATI 15+ Yes Yes Clear Decisions

Yes

(Print only)

THAILAND Nielsen Consumer & Media View 9,000+ National Face-to-Face/Online 12+ Yes Yes Clear Decisions No

TAIWAN Nielsen Media Index 10,000 National Face-to-Face/Online 12 - 65 Yes Yes Clear Decisions Yes

BANGLADESH Kantar

National Media Survey

(NMS) -TGI

16,200 National Face-to-Face 15+ Yes No ThinkMedia Yes

SRI LANKA Kantar

National Demographic

& Media Survey

(NDMS) -TGI

12,500 National Face-to-Face/CAPI 6+ Yes No QuestPlus No

VIETNAM Kantar Media

Media Habit Survey

(MHS) -TGI

6 Cities (Urban)

9,352 & National

(exc 6 cities)

7,200

6 cities & National Face-to-Face/Self completed 15 - 54 Choices 4 Yes

CHINA Sinomonitor CMMS/H3/MMMS

CMMS - 120,000+

H3 - 12,400+

MMMS - 30,000+

CMMS - National,108 cities (tier 1-5)

H3 - National,20 cities (tier 1-3)

MMMS - National,46 cities (tier 1-3)

Face-to-Face/Self

completed/Online

CMMS - 15-64

H3 - 18-50

MMMS - 15-64

Yes No

Telmar

DataTile

No

INDIA IMRB India 51,000 National Face-to-Face/Self completed 15 - 55 ABC

MEASUREMENT

GUIDE](https://image.slidesharecdn.com/asia-video-industry-report-2023-230102044026-b645e604/85/Asia-Video-Industry-Report-2023-pdf-81-320.jpg)

The Asia Video Industry Report 2023 highlights the role of the Asia Video Industry Association (AVIA) in strengthening the video industry ecosystem by addressing piracy and regulatory challenges in the region. It emphasizes the importance of collaboration among industry members to navigate evolving market dynamics, including the impacts of COVID-19 and changing consumer preferences. The report also discusses ongoing regulatory developments in various Asian countries, advocating for self-regulation and a balanced approach to content oversight to foster growth and innovation.

![[Research];[Digital marketing market]_2](https://cdn.slidesharecdn.com/ss_thumbnails/adma-digital-marketing-yearbook-2009-090823041957-phpapp02-100517235501-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[rokonz.com] Glossary of Semantic SEO Part-3.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/rokonz-260123200835-55123e1e-thumbnail.jpg?width=640&height=640&fit=bounds)

![[rokonz.com] Glossary of Semantic SEO Part-2.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/rokonz-260123200719-92199ba8-thumbnail.jpg?width=640&height=640&fit=bounds)

![[rokonz.com] Glossary of Semantic SEO Part-1.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/rokonz-260123200456-440e4060-thumbnail.jpg?width=640&height=640&fit=bounds)