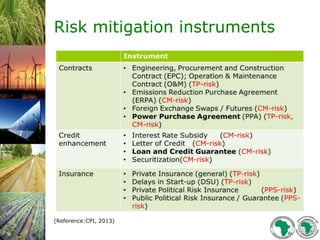

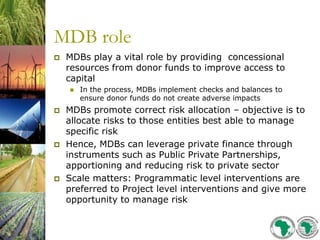

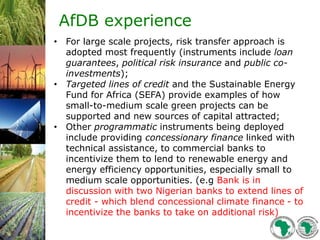

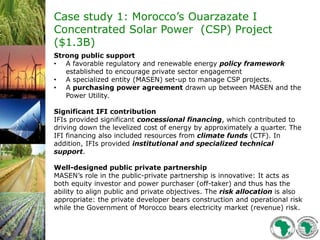

This document discusses risk management instruments that can mobilize private finance for development projects. It outlines the main types of risk that projects face, including political, technical, commercial and outcome risks. It then describes various risk mitigation instruments that can be used, including loan guarantees, political risk insurance, and public co-investments. The document also discusses risk coverage gaps in Africa and the role that multilateral development banks can play in leveraging private finance by allocating risks appropriately between public and private entities. It provides two case studies of projects utilizing such risk management: a concentrated solar power project in Morocco and a geothermal development project in Kenya.