, Rat Hnalyais

Short-tevm Soleny

CorentRatio

liguidRako

SuickRato

AcidTet

Rata

is a

CLASSIFICATION OFRATIOS

[Salvens Tehos

Tern Solveny

Debl-Equtt Ratio

-Totl Assetato Debt Ratio

Takest Caeraye Rato

Rto

Tonorer/AchvityRetos

dnanty TornoverRatios

Trade Reaivalle TuYnover

Rako

Trade layabuTumoer Rako

-WorkinyGtiaTumaer Rakia

Nel AscaorGfihlbulogd

Toinover Ratio

buunes.

Ratios

Esvnig fakabia

Oferaing Rato

NetPst Rato

Retm on Inetment o

RetnmotitEagd

2.

(I)LI9ujDITY RATI0S

() CumrentKatio = Cunent Aset

(u) Ligud oto SuickRotoQcid Tet Rato

iguid Asseta/Quick fset.

CuYent iabtes

H

Cuet liabillea

SoLvENCY RATioS

Ratio

(L)Debt Debt oy Long-Ter Delt

Shaxholders Funds

(u) Total Asseta o Debt Rato = Totas Asset

Ratio =

Debt

w Debt to Capitad Enmayed Rato e Dest

apialEmhlog

Total Assetu

(w Sntut Coveroge ahos Poft bekose TateteTr

Lateten ng.Term Debt

(EBIT)

3.

NetAsseti

or Gfi

h

d Eml

o

yed

reveneFrom Gpera ti

m

s

(vi

) Ne

t Asset Tornorer Rat

o

or Coad Empl

o

yed nesr

Ne

t Fired Asseta

(v) Fi

x

ed Asseu Tur

n ovey Ratioe Revenue Fr

o

m t

h

i

m

s

Worki

n

g Gotid

CNet Sa)

() dorking apild TurnaurRa

ko

= RevenuAo

m af

era hor

Averae Tr

a

de eyakl

e

a

(ü Trade Tayableu Tornoer

Ra

ho

= Ne

d tredt reheas

Aueray Trade civetla

(Cedt Salw

Trade Reatvabe

TornovrRaho Crlt Revenue fo

n ab

Averag Inventoy

((04S)

) Tnventory TornortrRat

i

o

= Cos

t qRevenufr

o

r

a hns

(T) ACTIVITY /TURNOVER

RATIOS

4.

N PROFITABILITY RATI0S

u)Goss= Gross

wNetot Rato = Net Brotit

Rato

Revenu Fron Gperatma

oY

Reene'FroN erehimna

Cast

Cost Reenu fromserahona +

Reenufom orata

.xlo

xlo

Botit beox Intnt, Tax Dieend

(v)Return on Znestnantabilal Enbloyeal or Yeld om

xl

xlo

Krfit

Reenufiom derokons

5.

the ForMulaa

2Debt

3

Lang- TermBoruings t g- Teom Praitia

NNen- Cwt iabites

+Resenea 4Sush

4)Totl sseta = Nen- Cuent tseeta t Nor lumeat

Iny. +

Cunent Asset

Woyt

t

6) Total iabilhe Shaneholdes t Nm lonent

fl

+ Cunet bab.

(

G) Tota! Debt Nen- Cud i'ab+Ct bab.

Uas.

s.

Nel ired Azvea t workiy Gite

Nel xed tsseth e Fyed Asseti - Datreiatas

6.

Creditort

+ Bi

l

s Payabb

TvadePeyat

l

a Creditort

cl

a

si

n

g

TC

2

f

e

ni

n

g

TP

Ly Trade Reeinasler

Debtors

+ Bi

l

l

s ivalles

2

+ cl

o

si

n

g

) average Tr

a

de Reuivaslaeabeni

g T&t cl

o

i

n

y

T&

- Purehates

Re hn

03) Ne

l Credit orehates

e Tol

a

l orchasu

- Credit ehs,

Total Salu

- Cash Salyo Sas et

n

Cs

h Salus

S Averea Tr

e

de ayabl

a

2

- Gr

o

ss Kef

t

124NCred Sals Net Sos

Thuent

o

y

GossoSs

Rot

CNel eahiny

= Reenu f

r

o

n oerahia

+ Ne

t orehosea

+ Diet ensea

) Ave

ro

oþeni

n

y Jnveny

6 Cost Reee

ro

n operationu CCoCs)

7.

SAveraye Collechim Periede 365 dayy in ayear

12 mentt in ayer

Selliyt Dishibuha

Trode Reuivally Turnoer Raho

( Averaqe Poyable leniod e 36s days/12 mm ta in ayar

Trade Ryatla Tornar pabo

PBIT- Intest- Tax

Praftaftautax +Tar t

Intet

Net prolt Nen- peratiny Exp- en-operehiyhan

Lnt m

Short torn lany

8.

Liquidity Ratios

Liquidity refersto the ability of the firm to meet its current liabilities as they

becomedue for payment. The liquidity ratios, therefore, are also called 'short

term solvency ratios. These ratios are used to assess the short-term financial

position.

Current Ratio or Working Capital Ratio

This ratio is used to assess the fim's ability to meet its short-term liabilities on

time.

Current Ratio =

" Acurrent ratio of 2 : Iis supposed to be an idea ratio. The higher the ratio, the

better it is, because the firm will be able to pay its current liabilitymore easily.

Current Assets

Current Llabillties

" The reason of assuming2 :las the ideal ratio is that the current assets include

such assets as inventory, trade receivables etc., from which full amount cannot

be realized in case of need. Hence, even if half the amount is realized from the

current assets on time, the firm can still meet its current liabilities in full.

" Inventoriesexcluding loose tools, stores & parts.

" Net Trade receivables are considered.

Quick Ratio or Acid Test Ratio or Liquid Ratio

This ratio indicates whether the firm is in a position to pay its current liabilities

within a month or if they have to be paid immediately.

Liquid Ratio = LiquldAssets

Current Llablities

" Aliquid ratio ofl:lis supposed to be an idea ratio. The higher the ratio, the

better it is, because the firm will be able to pay its current liability more easily.

" This ratio is better test of short-term financial position of the company than the

current ratio, as it considers only those assets which can be easily and readily

converted into cash.

ACCOUNTING RATIOS

" Liquid Assets = Current Assets - Inventories - Prepaid Expenses & Advance Tax

Activity Ratios or Turnover Ratios

These ratios measure the efficiency and rapidity of the resources of the

company, like inventory, fixed assets, working capital, trade receivables etc.

These ratios are generally calculated on the basis of revenue from operations

or cost of revenue from operations.

Inventory Turnover Ratio

Inventory Turnover Ratio

This ratio indicates whether inventory has been efficiently used or no.

Cost of Revenue from Operations

Average Inventory

" The higher the ratio, the better it is, since it indicates that inventory is selling

quickly.

" This ratio can be used for comparing the efficiency ofsales policies of two firms

doing same type of business.

Trade Receivables Turnover Ratio

This ratio indicates the spced with which the amount is collected from the trade

receivables.

Trade Receivables Turnover Ratio

" Gross TR are to be considered.

Credlt Revenue from Operations

Average Trade Recetvables

" The higher the ratio, the better it is, since it indicates that amount from trade

receivables is being collected morequickly.

" The more quickly the trade receivables pay, the less the risk from bad debts, and

so the lower the expenses of collection and increase in the liquidity of the fim.

By comparing the trade receivables turnover ratio of the current year with the

previous year, it may be assessed whether the Sale policy of the management is

efficient or not.

Trade Payable Turnover Ratio

This ratio indicates the speed with which the amount is being paid to trade

payables.

Net Credit Purchases

Average Trade payables

Trade Payables Turnover Ratio =

" The higher the ratio, the better it is, since it will indicate that the trade payables

are being paid more quickly which increases the credit worthiness of the firm.

Working Capital Turnover Ratio

This ratio reveals how efficiently Working Capital has been utilization in making

Revenue from operations.

Working Capital Turnover Ratio - Revenue from Operations

Working Capttal

Solvency Ratios

These ratios are calculated to assess the ability of the firm to meet its long-term

liabilities as and when they become due.

These ratios reveal as to how much amount in a business has been invested by

proprietors and how much amount has been raised from outside sources.

Solvency ratios disclose the firm's ability to meet the interest costs regularly

and long-term indebtedness at maturity.

Debt Equity Ratio

This ratio indicates the proportion of funds which are acquired by long-term

borrowings in comparison to sharcholder's funds.

Debt

Debt Equity Ratio=-

Long-term Debts

Shareholder's Funds or net worth

" Ifthedebt-equity ratio is more than 2:1,it showsa rather riskyfinancial position

from the long-term point of view, as it indicates that more and more funds

invested in the business are provided by long-term lenders.

" Debts =Long-term Borrowings + Long-term Provisions

Total Assets to Debt Ratio

This ratio expresses the relationship between total assets and long-term debts.

Total Assets to Debt Ratin - otal Assets

" I measures the extent to which long-term debts are covered by assets which

indicates the margin of safety available to providers of long-term loans.

" A higher total assets to debt ratio implies the use of lower debts in financing the

assets which means a larger safety margin for lenders and vice versa.

Proprietary Ratio

Debt

This ratio indicates the proportionoftotal assets funded by ownersorshareholders.

Proprietary Ratio = Equity

Total Assets

" A higher proprietary ratio is generally treated an indicator of sound financial

position from long-term point of view, because it means that a large proportion

of total assets is provided by equity and hence the firm is less dependent on

external source of finance and vice versa.

Interest Coverage Ratio

This ratio indicates how many times the interest charges are covered by the profits

available to pay interest charges.

PBIT

Interest Coverage Ratio = Fired Interest Charges on Debt

" An interest coverage ratio of 6 to 7 times is considered appropriate.

" This ratio measures the margin ofsafety for long-term lenders.

" The higher the ratio, more secure the lender is in respect of payment of interest

regularly.

Debt to Capital Employed Ratio

This ratio indicates the proportion of funds provided by long-term lenders in

comparison to the total capital employed in the business.

Debt to Capital Employed Ratio = Long term Debts

Capital Employed

" Capital Employed (LiaApproach): Equity +Debt

" Ahigh debt to capital employed ratio shows a rather risky financial position as

it indicates that more and more funds invested in the business are provided by

long-term lenders. t shows the lenders are at high risk and vice versa.

" Capital Employed (Assets Approach): Non-Current Assets +Working Capital

Fixed Assets Turnover Ratio

This ratio reveals how efficiently the fixed assets are being utilized in generating

sales.

Fixed Assets Turnover Rotio - Revenue from Operations

Net Fired Assets

" Compared with the previous year, ifthere is increase in this ratio, it will indicate

that there is better utilization of fixed assets,.

Net Assets Turnover Ratio or Capital Employed Turnover Ratio

This ratio reveals how efficiently Net Assets or Capital Employed has been

utilization in making Revenue from operations.

Net Assets Turnover Ratio = Revenue from Operatlons

Net Assets or Capltal Emplo yed

" Ahigh Net Assets turnover ratio shows efficient use of Net Assets resulting into

higher profitability. A low Net Assets turnover ratio indicates under-utilisation

of Net Assets.

Equtty

9.

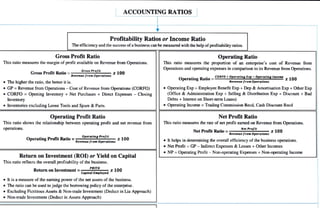

Gross Profit Ratio

GrossProfit Ratio =

" The higher the ratio, the better it is.

The efficiencyand the successofabusiness can be measured with the help ofprofitability ratios.

This ratio measures the margin of profit available on Revenue from Operations.

Gross Proflt

Revenue from Operattons

Inventories excluding Loose Tools and Spare &Parts.

Operating Profit Ratio

" GP =Revenue from Operations -Cost of Revenue from Operations (CORFO)

CORFO = Opening Inventory + Net Purchases + Direct Expenses Closing

Inventory

Operating Profit Ratio=

Profitability Ratios or Income Ratio

This ratio shows the relationship between operating profit and net revenue from

operations.

Operattng Profit

Revenue from Operations

ACCOUNTING RATIOS

Return on Investment =

PBITD

Capital Employed

100

Return on Investment (RO) or Yield on Capital

This ratio reflects the overall profitabilityof the business.

X100

" Non-trade Investment (Deduct in Assets Approach)

x 100

It is a measure of the earning power of the net assets of the business.

" The ratio can be used to judge the borrowing policy of the enterprise.

Excluding Fictitious Assets &Non-trade Investment (Deduct in Lia Approach)

Operating Ratio

This ratio measures the proportion of an enterprise's cost of Revenue from

Operations and operating expenses in comparison to its Revenue from Operations.

Operating Ratio=o+operating Exp-Operatlng Income

Revenue from Operatlons

" Operating Exp =Employee Benefit Exp +Dep &Amortisation Exp +Other Exp

(Office &Administration Exp + Selling &Distribution Exp + Discount + Bad

Debts + Interest on Short-term Loans)

" Operating Income =Trading Commission Recd, Cash Discount Recd

Net Profit Ratio

This ratio measures the rate of net profit earned on Revenue from Operations.

Net Proft

Net Profit Ratio =

Revenue from Operations

* 100

" It helps in determining the overallefficiency of the business operations.

Net Profit = GP Indirect Expenses & Losses + Other Incomes

" NP =Operating Profit - Non-operating Expenses + Non-operating Income

![[DSC Europe 25] Elena Menshikova - AI-Powered Operational Excellence: Revolut...](https://cdn.slidesharecdn.com/ss_thumbnails/es6nholbqy3zaao2c2yd-2-elena-menshikova-data-ai-in-decision-making-260115093812-4fba8b38-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Srba Markovic - From Pilot to Production: Overcoming AI Deplo...](https://cdn.slidesharecdn.com/ss_thumbnails/yjjmrtytmwbalxlba7px-4-srba-markovic-from-pilot-to-production-overcoming-ai-deployment-blockers-with-260114111931-4a892d44-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Ivica Milaric - The Future of Gaming and AI Tools.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/tijgzsmgse2kj2y5pzzp-5-ivica-milaric-the-future-of-gaming-x-ai-tools-260114111931-87c2b3ac-thumbnail.jpg?width=640&height=640&fit=bounds)