Download to read offline

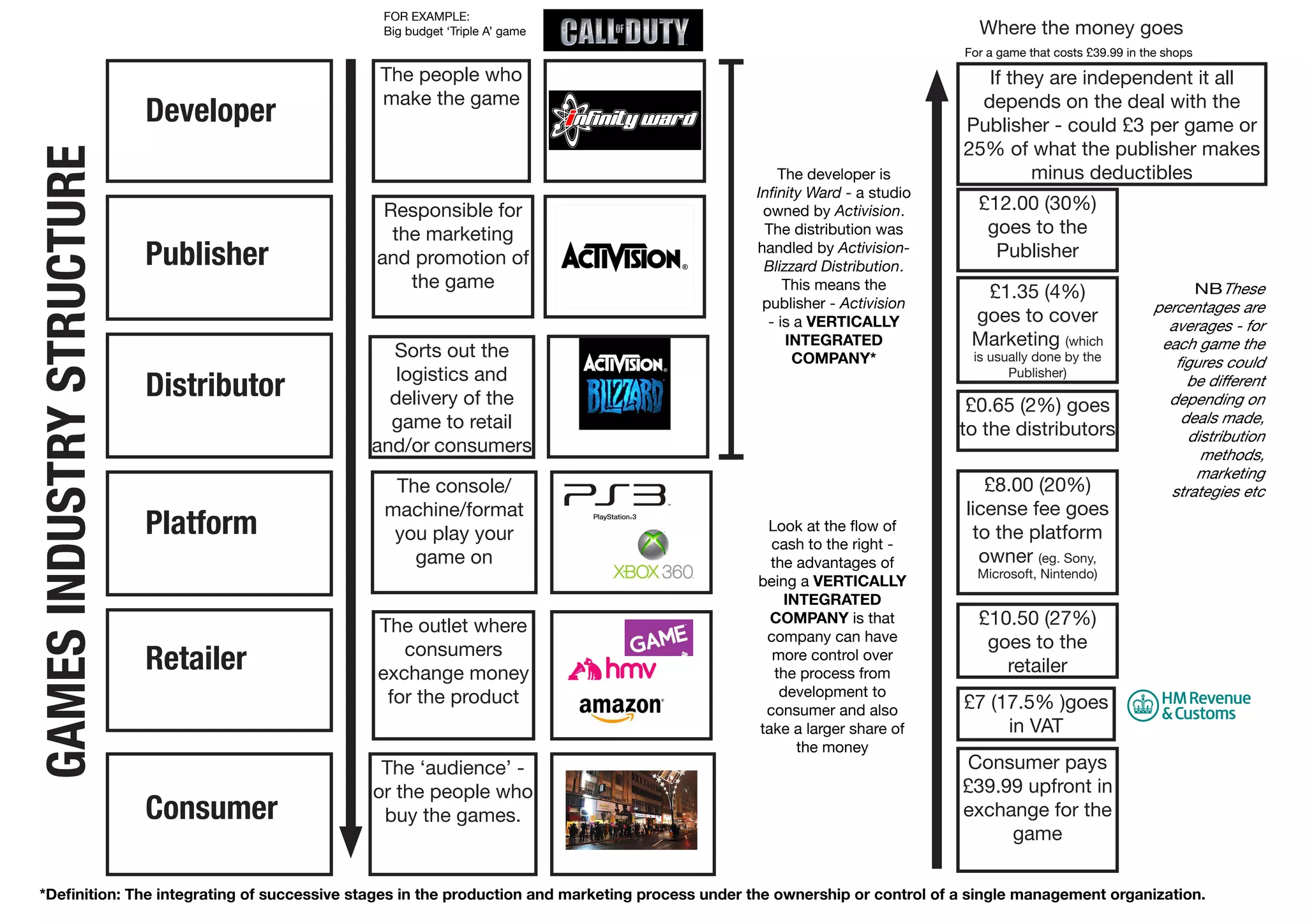

The document outlines the key players in the video game industry structure, including developers, publishers, distributors, retailers, platforms, and consumers. It then provides an example of how revenue from a £39.99 game is typically distributed, with the largest shares going to publishers (30%), retailers (27%), and developers (17.5%). The document notes that vertically integrated companies, which control multiple stages of development and distribution, have more control over the process and can retain a larger portion of profits.