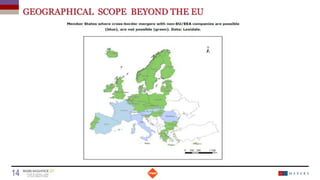

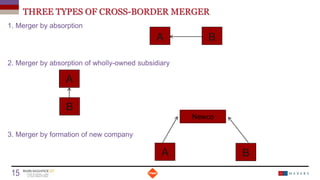

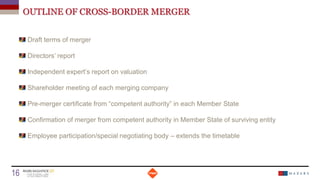

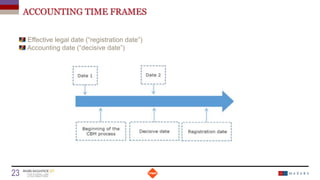

This document discusses cross-border mergers and corporate migration within Europe. It provides an overview of cross-border mergers, including definitions, the EU Merger Directive, reasons for mergers, and requirements. It also examines issues with implementing the Directive, different types of mergers and competent authorities, creditor protection, employee participation systems, and uses of cross-border mergers. Finally, it analyzes barriers to corporate migration within Europe and developments around the transfer of corporate seats.

![UK METHOD OF MERGER

Can UK companies merge under domestic law?

UK “scheme of arrangement”

Court can sanction compromise or arrangement

between company and (i) class of creditors or (ii)

class of members

Requires majority in number representing 75 % in

value

Court discretion - “the [scheme] proposal is such

that an intelligent and honest man, a member of the

class concerned, acting in respect of his interests

might reasonably approve” (Re Dorman Long & Co

[1934])

Date

17 Titre de la présentation

It’s Merger, Jim, but not as we know it …](https://image.slidesharecdn.com/2015-12carlconventionbruxelles2015-bdlighterpptemplatemarcalliancecrossbordermergers-151221154333/85/2015-MarcAlliance-Conference-17-320.jpg)

![UK SCHEME OF ARRANGEMENT

Alternative to takeover offer

75% majority, rather than 90% acceptances for “squeeze-out”

“cancellation” scheme avoided stamp duty (but now repealed)

Extra powers for court to make provision (s.900 CA 2006)

transfer to transferee company of whole or part of undertaking and of property or liabilities

of transferor

“…the dissolution, without winding up, of any transferor company”

Part 27 Companies Act 2006 implements Third Company Law Directive – but relies on scheme

of arrangement

Impact Assessment – anticipated take-up of CBMs of “less than 1%”

But

ITAU BBA International Ltd [2012] - section 900 and Part 27 a “dead letter”

Date

18 Titre de la présentation](https://image.slidesharecdn.com/2015-12carlconventionbruxelles2015-bdlighterpptemplatemarcalliancecrossbordermergers-151221154333/85/2015-MarcAlliance-Conference-18-320.jpg)

![UNIVERSAL SUCCESSION

Universal succession not recognised in

English law? National Bank of Greece and

Athens SA v Metliss [1958]

Can universal succession merger exist

between two English companies?

Nokes v Doncaster Amal. Collieries [1940]

Part VII FSMA 2000 – schemes for

insurance portfolio transfers

Likely approach of English courts to CBM?

Allow the transfer…but transferee

inherits the breaches

Easier for UK company to merge under

EU law than under UK law!

Date

19 Titre de la présentation](https://image.slidesharecdn.com/2015-12carlconventionbruxelles2015-bdlighterpptemplatemarcalliancecrossbordermergers-151221154333/85/2015-MarcAlliance-Conference-19-320.jpg)

![COMMUNICATION BETWEEN NATIONAL REGISTRIES

“[T]he registry for the registration of

the company resulting from the

cross-border merger shall notify,

without delay, the registry in which

each of the companies was required to

file documents that the cross-border

merger has taken effect. Deletion of

the old registration, if applicable, shall

be effected on receipt of that

notification, but not before.”

Article 13, Cross-Border Mergers Directive

Date

24 Titre de la présentation](https://image.slidesharecdn.com/2015-12carlconventionbruxelles2015-bdlighterpptemplatemarcalliancecrossbordermergers-151221154333/85/2015-MarcAlliance-Conference-24-320.jpg)