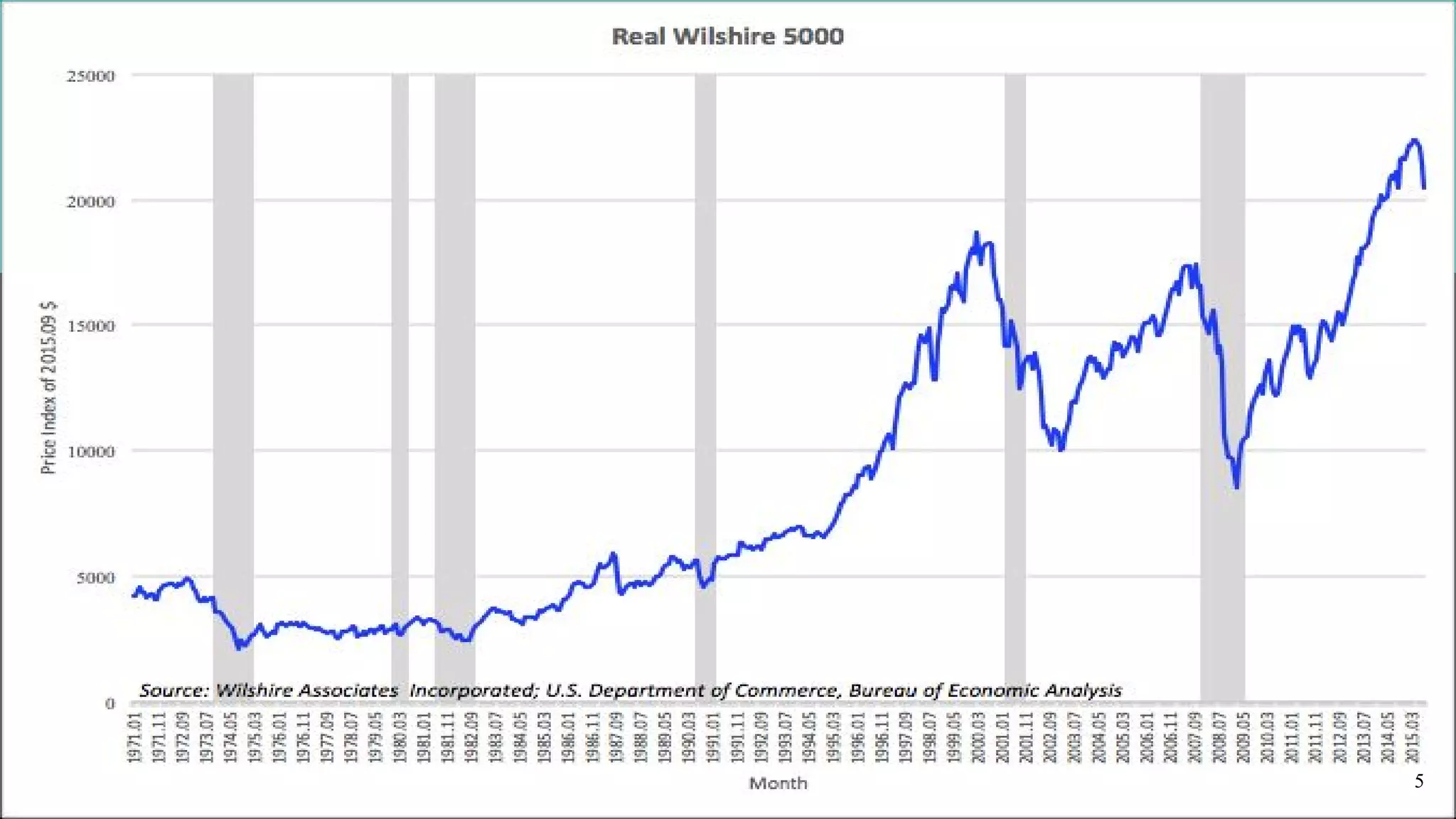

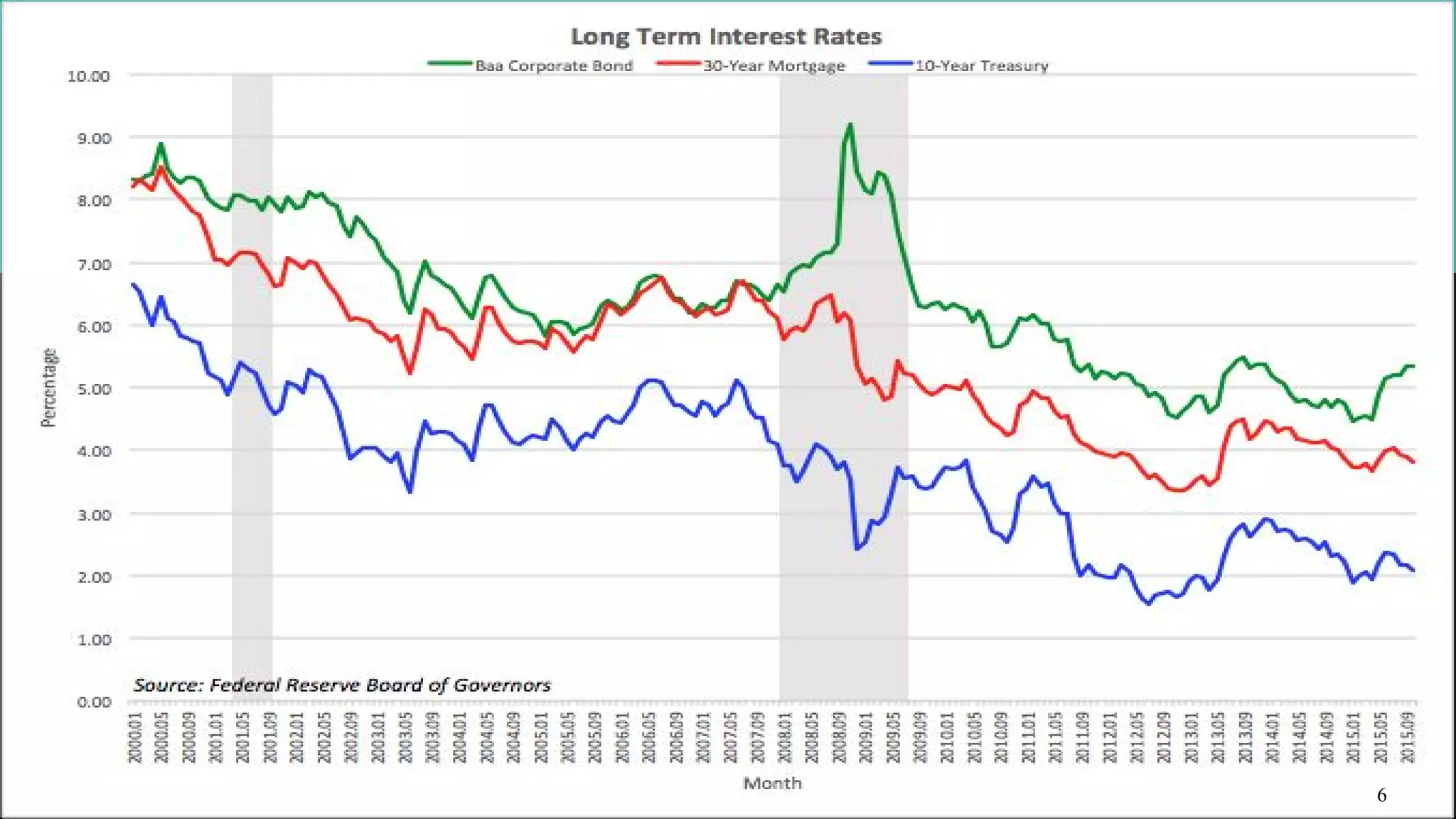

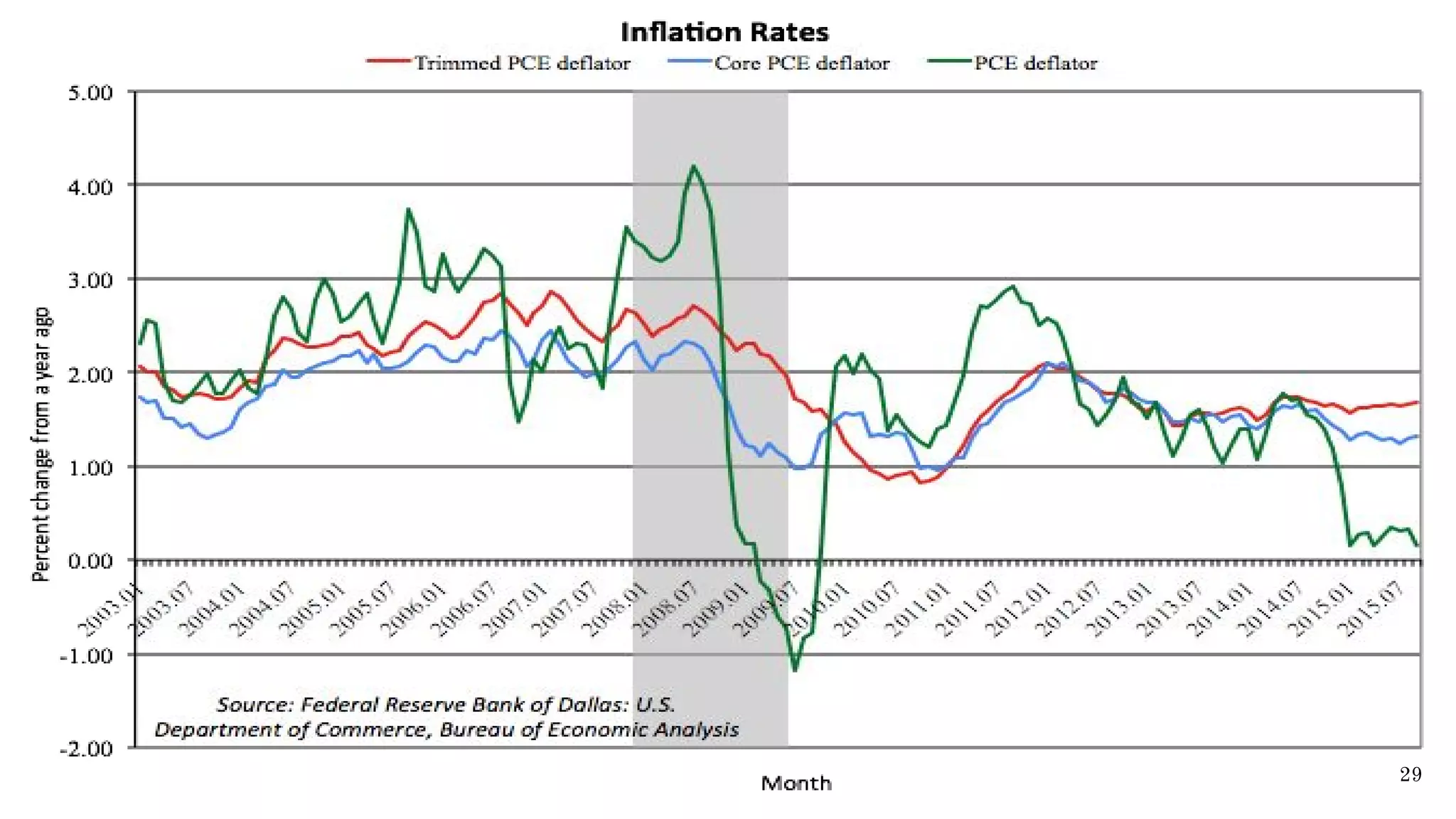

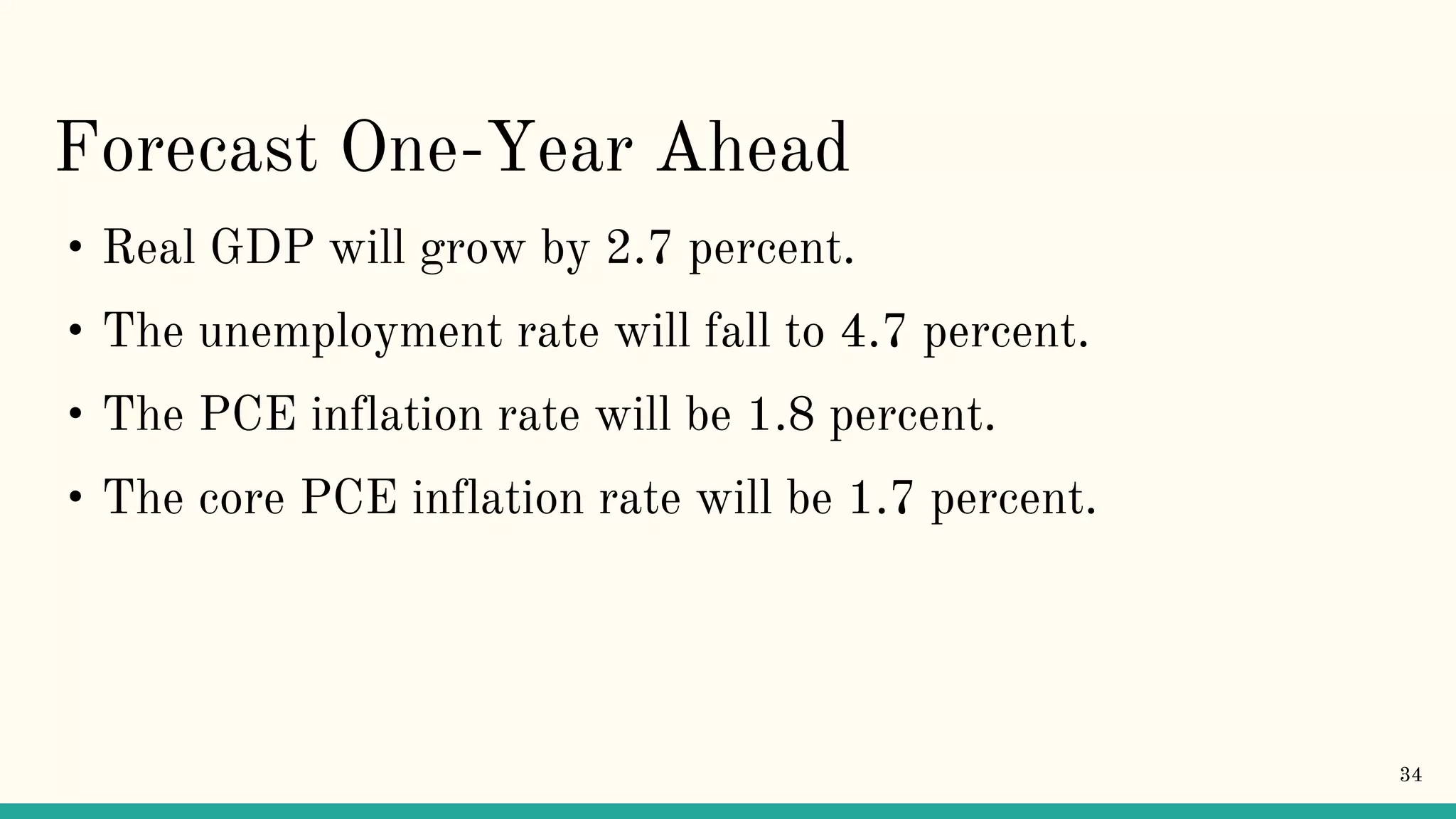

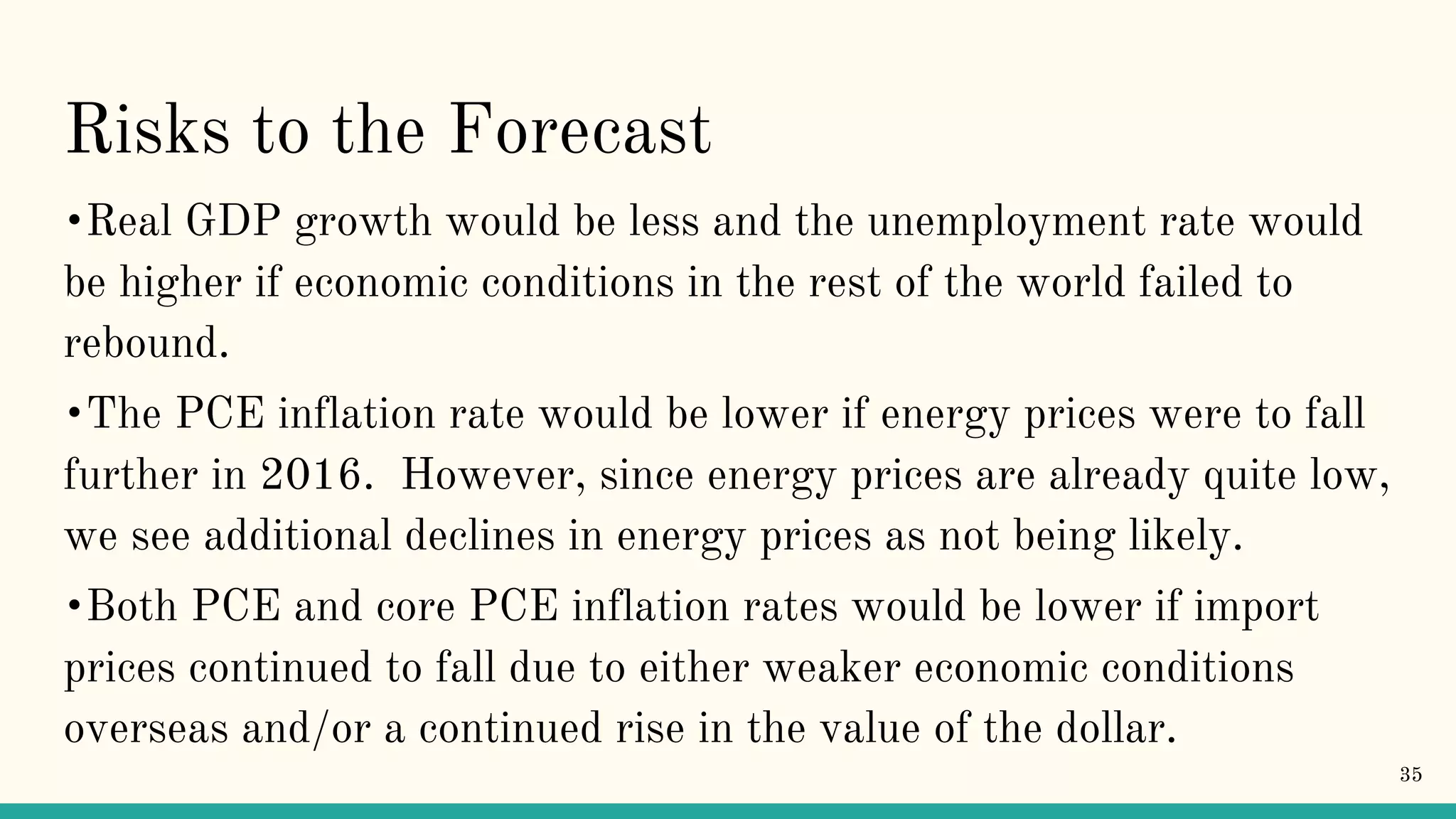

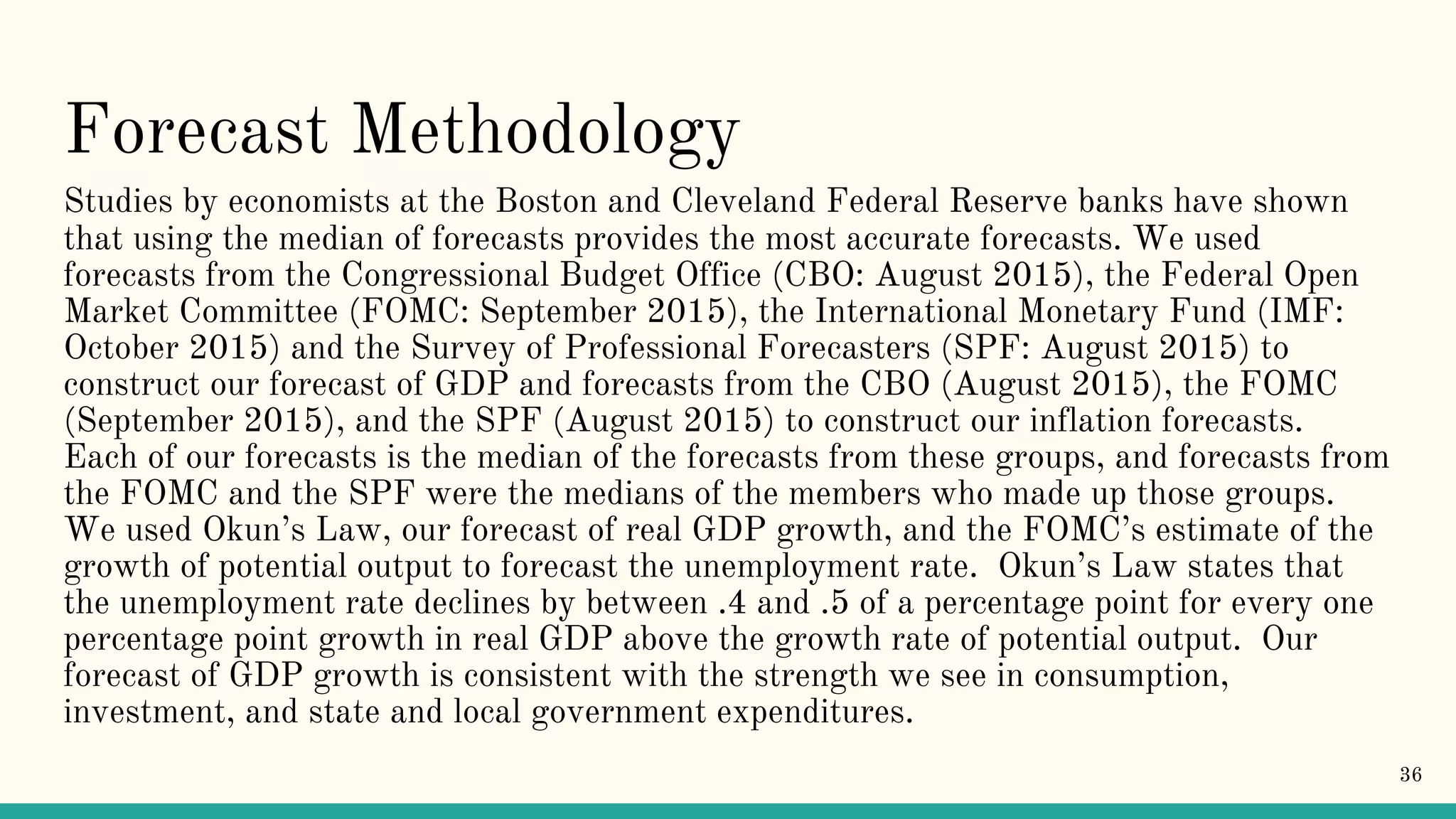

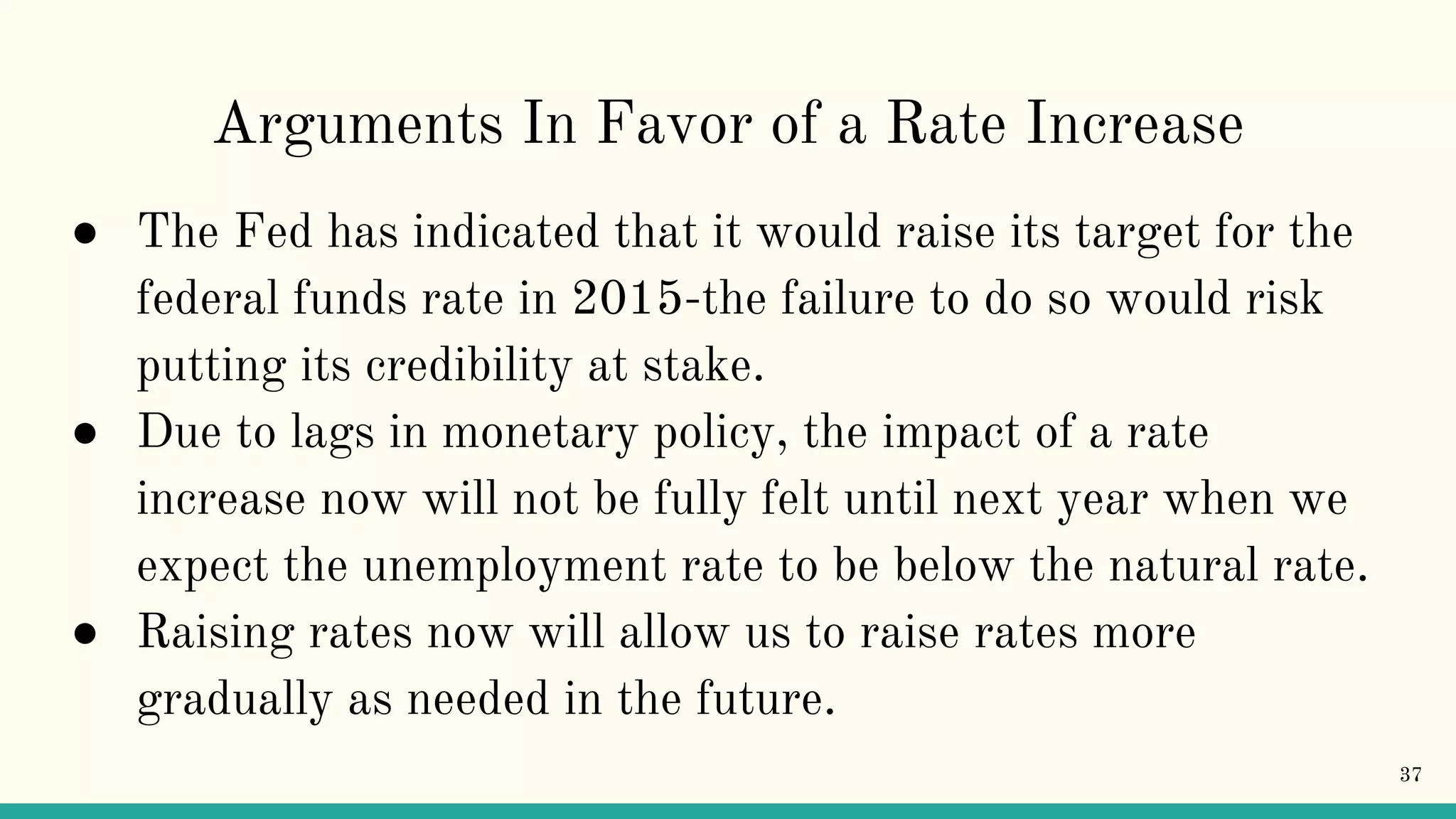

The document provides an overview of the current economic conditions in the United States, risks to the economy, a one-year forecast, and a policy recommendation from the Federal Reserve. It finds that aggregate demand is strengthening, labor markets are improving but still show some slack, and inflation remains below target. The forecast predicts real GDP growth of 2.7%, unemployment falling to 4.7%, and both overall and core PCE inflation around 1.7-1.8%. The policy recommendation is to raise the target federal funds rate range to 0.25-0.5% while continuing other quantitative easing programs.